My XP

0

Login

Original author: Minerva

الترجمة الأصلية:كتلة وحيد القرن

It has been a decade since Tether launched the first dollar-backed تشفيرcurrency. Since then, stablecoins have become one of the most widely adopted products in the cryptocurrency space, with a current market cap of nearly $180 billion. Despite this remarkable growth, stablecoins still face several challenges and limitations.

This post delves into the problems with existing stablecoin models and attempts to predict how we can end the currency civil war.

Before we dive in, let’s cover some basics to better understand what stablecoins are.

When I started researching stablecoins a few years ago, I was confused by people describing them as debt instruments. But as I dug deeper into how money is created in the current financial system, it started to make sense to me.

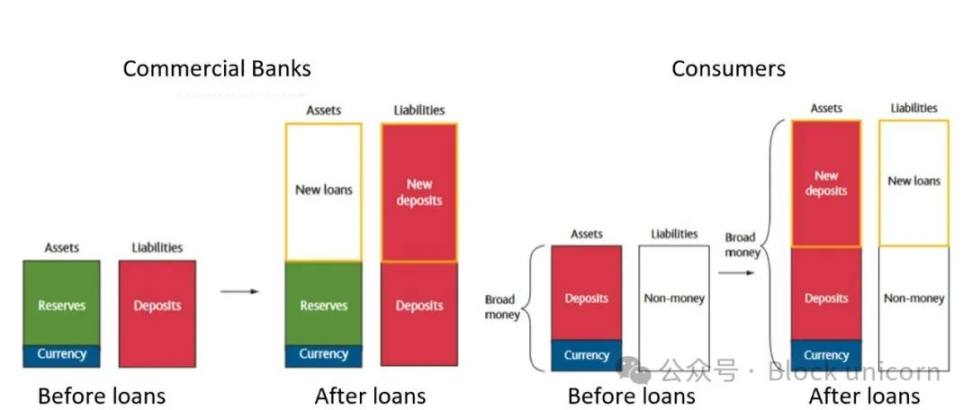

In a fiat currency system, money is primarily created when commercial banks (hereinafter referred to as “banks”) provide loans to customers. But this does not mean that banks can create money out of thin air. Before creating money, banks must first receive something of value: your promise to repay the loan.

Let’s say you need financing to buy a new car. You apply for a loan from your local bank, and once approved, the bank makes a deposit to your account that matches the loan amount. This is when new money is created in the system.

When you transfer these funds to the person selling the car, the deposit may be transferred to another bank if the seller has an account at another bank. However, the money remains within the banking system until you start repaying the loan. Money is created through lending and destroyed through repayment.

Figure 1: Money creation through additional lending

Source: Money Creation in the Modern Economy (Bank of England)

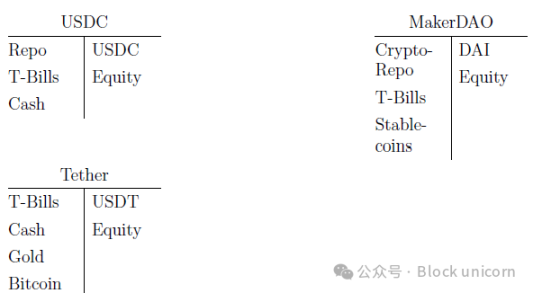

Stablecoins work in a somewhat similar way. Stablecoins are created when an issuer makes a loan and are destroyed through repayments by borrowers. Centralized issuers like Tether and Circle mint tokenized USD, which are essentially digital IOUs issued based on USD deposits made by borrowers. DeFi protocols like MakerDAO and Aave also mint stablecoins through loans, but this issuance is collateralized by crypto assets rather than fiat currency.

Since their debt is backed by various forms of collateral, stablecoin issuers effectively act as crypto banks. Sebastien Derivaux, founder of Steakhouse Financial, further explored this analogy in his study Cryptodollars and the Hierarchy of Money.

Figure 2: Two-dimensional matrix of crypto-dollars

Source: Cryptodollars and the Hierarchy of Money, September 2024

Sebastien uses a two-dimensional matrix to classify stablecoins based on the nature of their reserves (such as RWAs off-chain assets vs. on-chain crypto assets) and whether the model is full reserve or partial reserve.

Here are some notable examples:

USDT: Mainly supported by off-chain reserves. Tether’s model is a partial reserve, because each USDT is not 1:1 backed by cash or cash equivalents (such as short-term Treasury bills), but also includes other assets such as commercial paper and corporate bonds.

USDC: USDC is also backed by off-chain reserves, but unlike USDT, it maintains a full reserve status (1:1 backed by cash or cash equivalents). Another popular fiat-backed stablecoin, PYUSD, also falls into this category.

DAI: DAI is issued by MakerDAO and is backed by on-chain reserves. DAI is partially reserved through its over-collateralization structure.

Figure 3: Simplified balance sheet of current crypto dollar issuers

Source: Cryptodollars and the Hierarchy of Money, September 2024

Like traditional banks, these crypto banks aim to generate attractive returns for shareholders by taking a moderate amount of balance sheet risk — enough to be profitable, but not so high as to jeopardize collateral and risk insolvency.

While stablecoins offer desirable properties such as lower transaction costs, faster settlement, and higher returns than traditional finance (TradFi) alternatives, the existing model still faces many problems.

(1) Fragmentation

According to RWA.xyz, there are currently 28 active stablecoins pegged to the U.S. dollar.

Figure 4: سوق share of existing stablecoins

Source: RWA.xyz

As Jeff Bezos famously said, “Your profit margin is my opportunity.” While Tether and Circle continue to dominate the stablecoin market, the high interest rate environment in recent years has spawned a wave of new entrants seeking to capture a piece of these high profits.

The problem with having so many stablecoin options is that, while they all represent tokenized dollars, they are not interoperable. For example, a user holding USDT cannot seamlessly use it at a merchant that only accepts USDC, even though both are pegged to the dollar. Users can exchange USDT for USDC through centralized or decentralized exchanges, but this adds unnecessary transaction friction.

This fragmented landscape is similar to the pre-central banking era, when individual banks issued their own notes. In that era, the value of banknotes fluctuated based on their credit stability and could even become worthless if the issuing bank failed. The lack of standardization of value led to inefficient markets and made cross-regional trade difficult and costly.

Central banks were created to solve this problem. By requiring member banks to maintain reserve accounts, they ensure that banknotes issued by the banks can be accepted at face value throughout the system. This standardization achieves what is known as monetary currency, which allows people to treat all banknotes and deposits as equivalent, regardless of the creditworthiness of the issuing bank.

But DeFi lacks a central bank to establish monetary uniformity. Some projects, such as M^0 (@m0foundation), are trying to solve the interoperability problem by developing a decentralized crypto dollar issuance platform. I personally have high expectations for their grand vision, but the challenges are significant and their success is still a work in progress.

(2) Counterparty risk

Imagine you have an account at JP Morgan (JPM). Although the official currency of the United States is the U.S. dollar (USD), the account balance actually represents a bank note, which we can call jpmUSD.

As mentioned earlier, jpmUSD is pegged to the US dollar at a 1:1 ratio through JPMs agreement with the central bank. You can redeem jpmUSD for physical cash, or use it interchangeably with other bank notes (such as boaUSD or wellsfargoUSD) within the banking system at a 1:1 exchange rate.

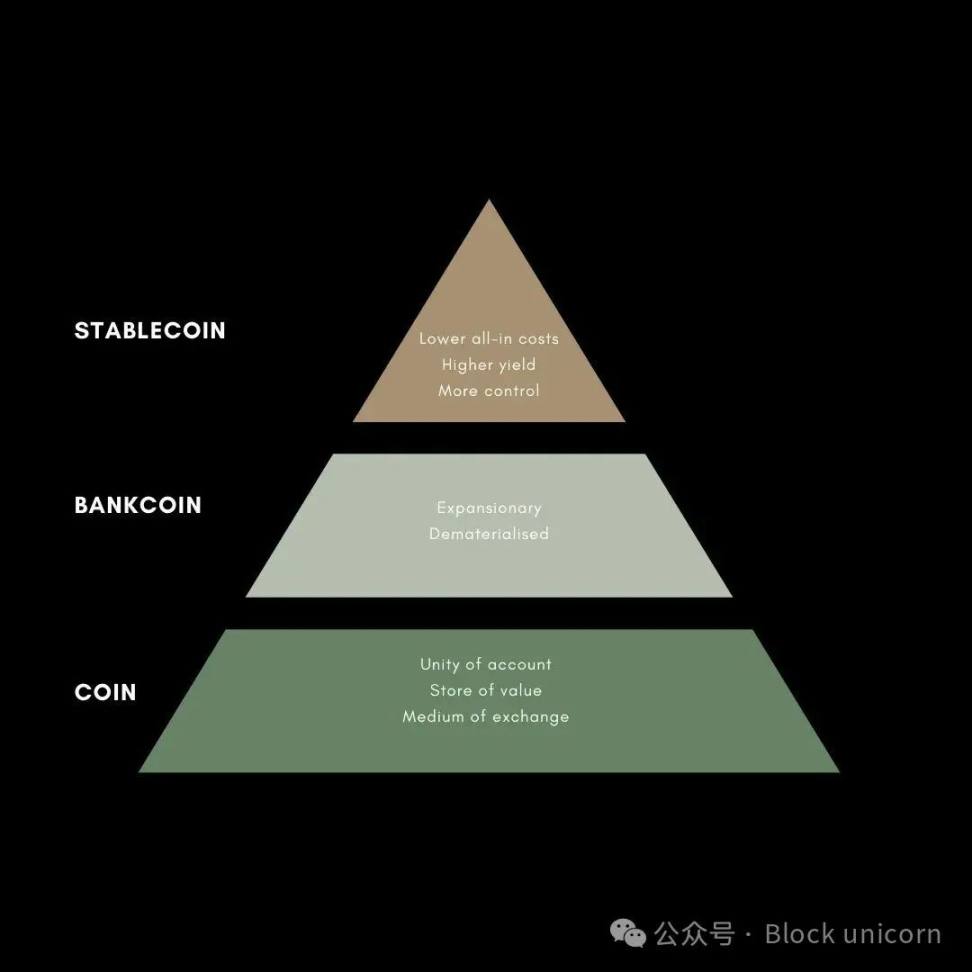

Figure 5: Schematic diagram of the currency hierarchy

Source: #4 | Currency Classification: From رمز مميزs to Stablecoins (Dirt Roads)

Just as we can stack different technologies to create a digital ecosystem, various forms of money can be layered to build a monetary hierarchy. The dollar and jpmUSD are both forms of money, but jpmUSD (or bankcoin) can be considered a layer above the dollar (the token). In this hierarchy, bankcoins rely on the trust and stability of the underlying tokens and are backed by formal agreements from the Federal Reserve and the U.S. government.

Fiat-backed stablecoins such as USDT and USDC can be described as a new layer on top of this hierarchy. They retain the essential qualities of bank coins and tokens while adding the benefits of blockchain networks and interoperability with DeFi applications. While they act as an enhanced payment rail layer on top of the existing currency stack, they are still closely tied to the traditional banking system and therefore carry counterparty risk.

Centralized stablecoin issuers typically invest their reserves in safe and liquid assets such as cash and short-term U.S. government securities. While credit risk is low, counterparty risk is high because only a small portion of bank deposits are insured by the Federal Deposit Insurance Corporation (FDIC).

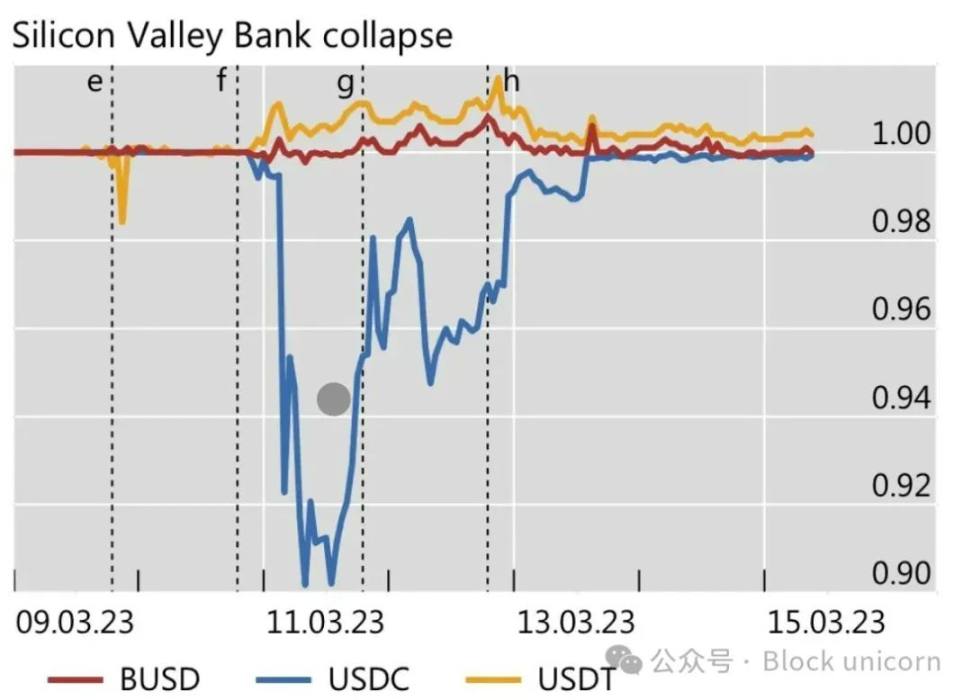

Figure 6: Stablecoin price fluctuations during the SVB crash

Source: Stablecoins and Tokenized Deposits: Implications for the Single Nature of Money (BIS)

For example, of the approximately $10 billion in cash that Circle held at regulated financial institutions in 2021, only $1.75 million (about 0.02%) was covered by FDIC deposit insurance.

When Silicon Valley Bank (SVB) collapsed, Circle was in danger of losing most of its deposits with the bank. If the government does not take extraordinary steps to guarantee all deposits, including those above the $250,000 FDIC insurance limit, USDC could become permanently decoupled from the dollar.

(3) Yield: Race to the bottom

During this cycle, the dominant narrative around stablecoins is the concept of “returning returns to users.”

For regulatory and financial reasons, centralized stablecoin issuers retain all profits generated from user deposits. This leads to a disconnect between the parties that actually drive value creation (users, DeFi applications, and market makers) and the parties that capture the benefits (issuers).

This difference has paved the way for a new wave of stablecoin issuers, who mint stablecoins using short-term wealth or tokenized versions of these assets and redistribute the underlying returns to users through smart contracts.

While this is a step in the right direction, it also creates an incentive for issuers to slash fees in order to capture a larger share of the market. The intensity of this battle for yield is evident when I review the Spark Tokenization Grand Prix tokenized money market fund proposal, which aims to aggregate $1 billion in tokenized financial assets as collateral for MakerDAO.

Ultimately, yields or fee structures cannot be long-term differentiators as they will likely converge towards the minimum sustainable rate required to remain operational. Issuers will need to explore alternative monetization strategies as the issuance of stablecoins does not accrue value in and of itself.

The Romance of the Three Kingdoms is a beloved classic in East Asian culture, set during the late Han Dynasty, a time of war and division among various factions.

A key strategist in the story is Zhuge Liang, who famously came up with the strategy of dividing China into three separate regions, each controlled by three warring powers. His Three Kingdoms strategy was designed to prevent any one kingdom from gaining dominance, thereby creating a balanced power structure to restore stability and peace.

I’m not a sage, but stablecoins may also benefit from a similar trichotomy. The future landscape may be divided into three areas: (1) payments, (2) yields, and (3) the middle layer (everything in between).

Payments: Stablecoins provide a seamless, low-cost way to settle cross-border transactions. USDC is currently in the lead in this regard, and its partnership with Coinbase and Base Layer 2 may further consolidate its position. DeFi stablecoins should avoid competing directly with Circle in the payment field, and should focus on the DeFi ecosystem where they have a clear advantage.

Yield: RWA protocols that issue yield-generating stablecoins should learn from Ethena, which has cracked the code for generating high-yield and relatively sustainable yields through crypto-native and related products. Whether leveraging other delta-neutral strategies or creating synthetic credit structures that replicate traditional finance (TradFi) swaps, there is room for growth in this area as USDe faces scalability ceilings.

Middle layer: For decentralized stablecoins with low returns, there is an opportunity to unify fragmented liquidity. An interoperable solution will maximize DeFi’s ability to match lenders and borrowers and further simplify the DeFi ecosystem.

The future of stablecoins remains uncertain. But a balanced power structure between these three parts could end the currency civil war and bring much-needed stability to the ecosystem. Rather than a zero-sum game, this balance will provide a solid foundation for the next generation of DeFi applications and pave the way for further innovation.

This article is sourced from the internet: A Deep Dive into Existing Stablecoin Models: How to End the Currency Civil War?

Original author: Nancy, PANews The US presidential election has entered the countdown, and the competition between Trump and Harris has entered a white-hot stage. Compared with Trumps high-profile crypto actions, Harris rarely makes a clear statement on cryptocurrencies. Recently, Harris announced a series of economic security plans for black male voters during her campaign, including a promise to support a crypto regulatory framework to protect black male cryptocurrency investments. After the plan was announced, Harris was accused by the crypto community of lack of sincerity and only used cryptocurrencies as a tool to win the election. New policies are proposed to win votes from black men, but the crypto regulatory framework is questioned Pennsylvania is an important battlefield in this years US election. The two evenly matched candidates, Trump and…