My XP

0

Login

المقال الأصلي بقلم روبي بيترسون، باحث في شركة دلفي ديجيتال

الترجمة الأصلية: لوفي، فورسايت نيوز

طوال تاريخ تشفيرلقد كان موضوع التقاط القيمة في سلسلة الكتل موضوعًا مثيرًا للجدال. كان النقاش الأساسي دائمًا بين طبقة البروتوكول وطبقة التطبيق، ولكن هناك طبقة ثالثة في السلسلة يتجاهلها معظم الناس: المحفظة.

وتزعم نظرية "المحفظة السمينة" أنه مع "تقليص حجم" البروتوكولات والتطبيقات، فإن من يملك الموارد الأكثر قيمة، التوزيع وتدفق الطلبات، سوف يكون قادراً على الاستحواذ على المزيد من القيمة. وباعتبارها الواجهة الأمامية النهائية، فلا أحد أكثر قدرة على تحقيق الربح من هذه القيمة من المحفظة.

ستستكشف هذه المقالة نظرية المحفظة السمينة في ثلاث خطوات. أولاً، سنحدد ثلاثة اتجاهات هيكلية ستستمر في دفع عملية تحويل المنتجات إلى سلع أساسية على مستوى البروتوكول والتطبيق. ثانيًا، سنستكشف طرقًا مختلفة لتحقيق الربح من المحافظ، بما في ذلك الدفع مقابل الطلب (PFOF) وخدمات توزيع التطبيقات (DaaS). أخيرًا، سنستكشف سبب تفوق جوبيتر وإنفينكس على المحافظ في المنافسة على المستخدمين.

يمكن اختصار السؤال حول المكان الذي ستتقارب فيه القيمة في نهاية المطاف في مكدس blockchain في إطار عمل بسيط. لكل طبقة مقابلة من المكدس، اسأل نفسك الأسئلة التالية:

إذا زادت رسوم المنتجات في هذا المستوى، فهل سيتجه المستخدمون إلى بدائل أرخص؟

ببساطة، إذا رفعت Arbitrum رسومها، فهل سيتحول المستخدمون إلى بروتوكولات أخرى (مثل Base)، والعكس صحيح؟ وعلى نحو مماثل، على مستوى التطبيق، إذا رفعت dYdX رسومها، فهل سيتحول المستخدمون إلى منصات DEX دائمة غير متمايزة أخرى؟

وباتباع هذا المنطق، يمكننا تحديد الأماكن التي تكون فيها تكاليف التحول أعلى، وبالتالي من يتمتع بقوة تسعير قوية. وعلى نحو مماثل، يمكننا استخدام هذا الإطار لتحديد الأماكن التي تكون فيها تكاليف التحول أدنى، وبالتالي أي طبقة من المجموعة سوف تصبح سلعية بشكل متزايد بمرور الوقت.

في حين كانت البروتوكولات تتمتع تاريخيًا بقوة تسعير قوية، إلا أنني أعتقد أن هذا يتغير. واليوم، هناك ثلاثة اتجاهات هيكلية تعمل على "إضعاف" طبقة البروتوكول بشكل متزايد:

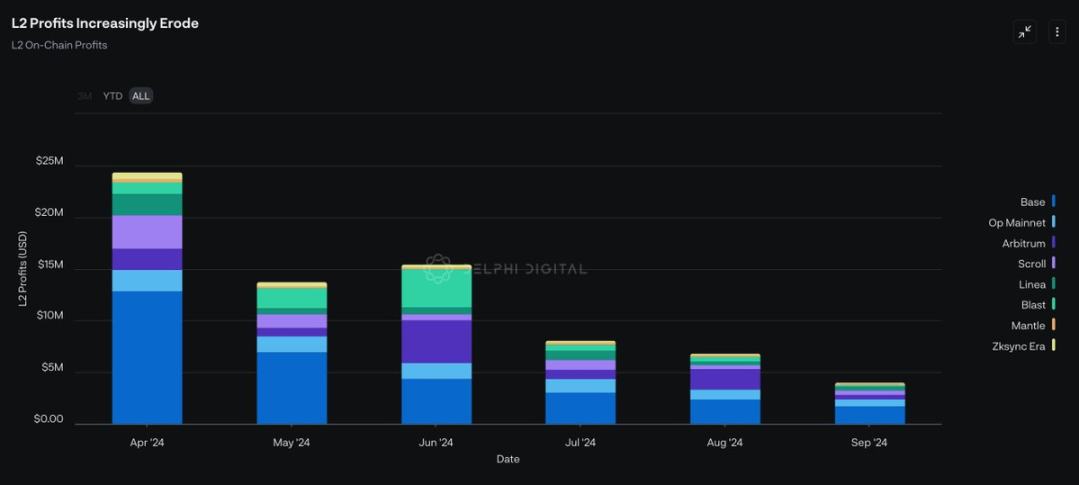

تطبيقات السلاسل المتعددة وتجريد السلسلة: ومع انتشار التطبيقات عبر سلاسل متعددة للحفاظ على القدرة التنافسية، ستصبح تجربة المستخدم عبر سلاسل الكتل غير قابلة للتمييز بشكل متزايد، وبالتالي، فإن تكاليف التبديل على طبقة البروتوكول سوف تنخفض أكثر فأكثر. بالإضافة إلى ذلك، فإن تجريد السلسلة من شأنه أن يقلل من تكاليف التبديل من خلال تجريد الجسور عبر السلسلة. ونتيجة لذلك، لن تكون التطبيقات مقيدة بتأثيرات الشبكة لسلسلة واحدة، بل ستصبح السلاسل مقيدة بشكل متزايد بتوزيع حركة المرور للتطبيقات.

نضوج سلسلة توريد المركبات الكهربائية والإلكترونية الصغيرة: في حين لن يتم القضاء على MEV بشكل كامل، فهناك العديد من المبادرات سواء على مستوى التطبيق أو بالقرب من الطبقة السفلية لإعادة توزيع MEV المستخرجة من المستخدمين. والأمر المهم هو أنه مع استمرار نضوج سلسلة توريد MEV، ستتراكم القيمة أكثر فأكثر على سلسلة توريد MEV ثم يتم الاستحواذ عليها بواسطة التطبيقات ذات تدفق الطلبات الأكثر تميزًا للمستخدم. وهذا يعني أن البروتوكولات ستفقد قوتها التفاوضية، في حين سترتفع مكانة الواجهات الأمامية والمحافظ.

صعود نموذج الوكالة: في عالم حيث يتم تنفيذ المعاملات في المقام الأول من قبل الوكلاء و"المحللين" بدلاً من البشر، فإن جذب هذا التدفق بالوكالة سيصبح ضرورة لبقاء blockchain. ومن المهم، نظرًا لأن الوكلاء و"المحللين" مبرمجون للتركيز على التحسين لتحقيق أفضل تنفيذ، فلن تتنافس البروتوكولات بعد الآن حول الأشياء غير الملموسة مثل "الاتساق". بدلاً من ذلك، فإن رسوم المعاملات والسيولة هي ما يهم، وهو ما لن يؤدي إلا إلى "إضعاف" طبقة البروتوكول حيث تُجبر البروتوكولات على ضغط الرسوم وتحفيز السيولة للبقاء قادرة على المنافسة.

لذا، فلنعد إلى سؤالنا الأصلي: إذا رفع أحد البروتوكولات رسومه، فهل يتركه المستخدمون بحثاً عن بدائل أرخص؟ ورغم أن الإجابة قد لا تكون واضحة اليوم، فإنني أعتقد أنه مع استمرار انخفاض تكاليف التحول، فإن الإجابة بالنسبة لعدد متزايد من البروتوكولات سوف تكون: نعم.

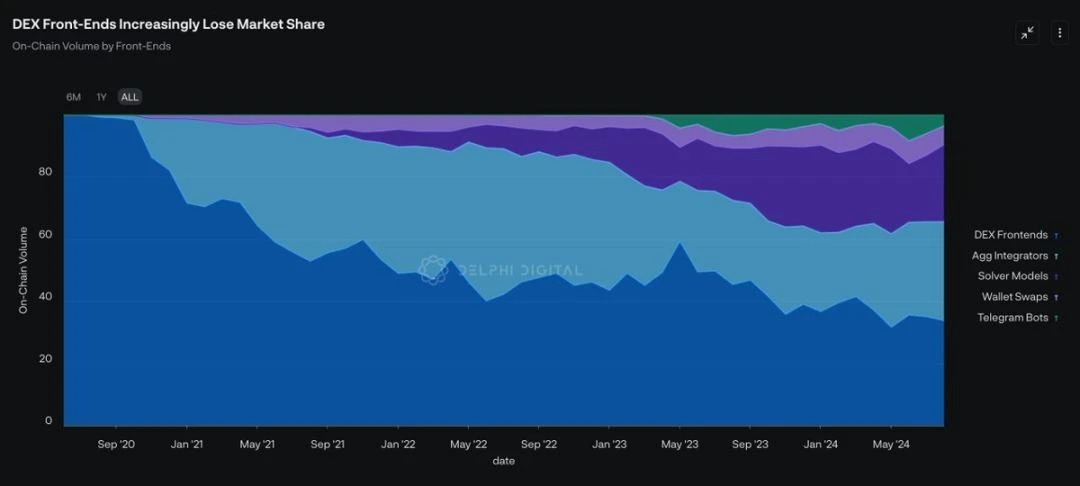

مصدر البيانات: Dune Analytics @0x Kofi

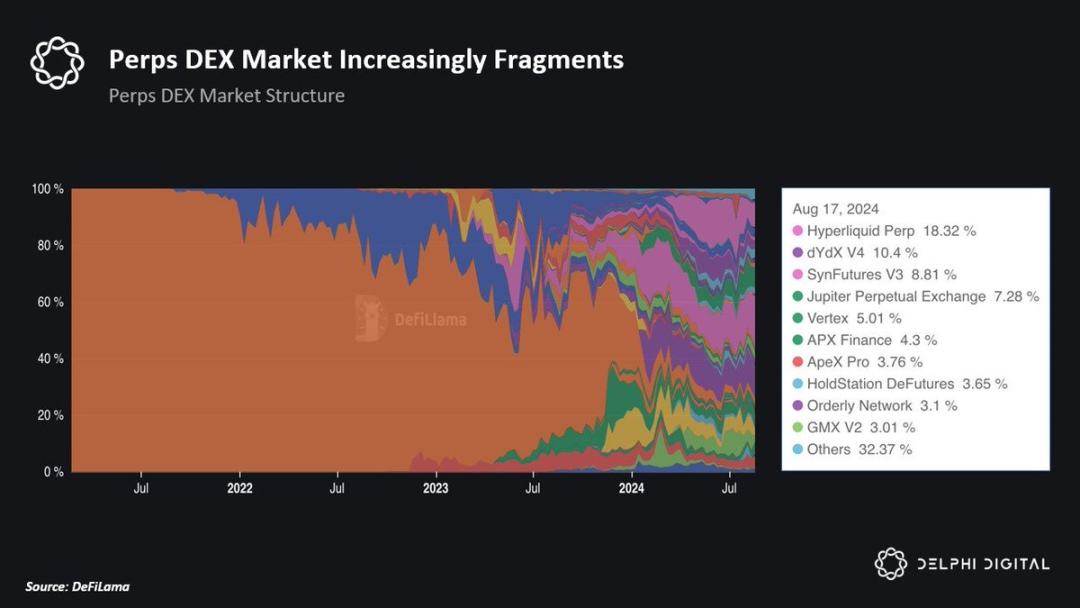

من البديهي أن نتصور أن ضعف البروتوكول يعني أن التطبيقات لابد وأن تصبح أكثر قوة. ورغم أن التطبيقات سوف تستعيد بعض قيمتها بالتأكيد، فإن نظرية التطبيقات الضخمة في حد ذاتها تبسيطية. ذلك أن التطبيقات الرأسية المختلفة تكتسب قيمتها بطرق مختلفة، ولا ينبغي أن يكون السؤال هو هل ستصبح التطبيقات أكثر قوة؟ بل أي التطبيقات على وجه التحديد؟

كما ذكرت في إطار عمل جديد للعملات المشفرة سوق الخنادق، والاختلافات البنيوية الفريدة لتطبيقات التشفير (القابلية للتقسيم، والتركيب، والتقاط القيمة القائمة على الرمز) يمكن أن تقلل من حواجز الدخول والتكاليف للمنافسين الناشئين. لذلك، على الرغم من أن بعض التطبيقات لديها بعض الخصائص التي لا يمكن نسخها بسهولة، فمن الصعب للغاية على تطبيقات التشفير زراعة الخنادق والحفاظ على حصة السوق.

مرة أخرى، نعود إلى إطارنا الأصلي: إذا رفع أحد التطبيقات رسومه، فهل سيتحول المستخدمون إلى بدائل أرخص؟ أعتقد أن 99% من التطبيقات ستواجه هذه المشكلة. لذلك، أتوقع أن تواجه معظم التطبيقات صعوبة في الحصول على القيمة لأن تشغيل مفتاح الرسوم سيؤدي حتماً إلى تحول المستخدمين إلى التطبيق التالي غير المتمايز الذي يقدم حافزاً أكثر سخاءً.

وأخيرا، أعتقد أن صعود وسطاء الذكاء الاصطناعي ومحللي المشكلات سيكون له تأثير مماثل على التطبيقات كما حدث على البروتوكولات. ونظرا لأن الوسطاء و"محللي المشكلات" محسنون في المقام الأول لجودة التنفيذ، أتوقع أن تضطر التطبيقات أيضا إلى التنافس بقوة لجذب تدفق الوسطاء. وفي حين أن تأثيرات شبكة السيولة من شأنها أن تخلق حالة من الغلبة للفائز على كل شيء في الأمد البعيد، فإنني أتوقع أن تشهد التطبيقات في الأمدين القريب والمتوسط سباقا نحو القاع.

وهذا يثير السؤال التالي: إذا استمرت البروتوكولات والتطبيقات في الضعف، فأين ستتجمع القيمة مرة أخرى؟

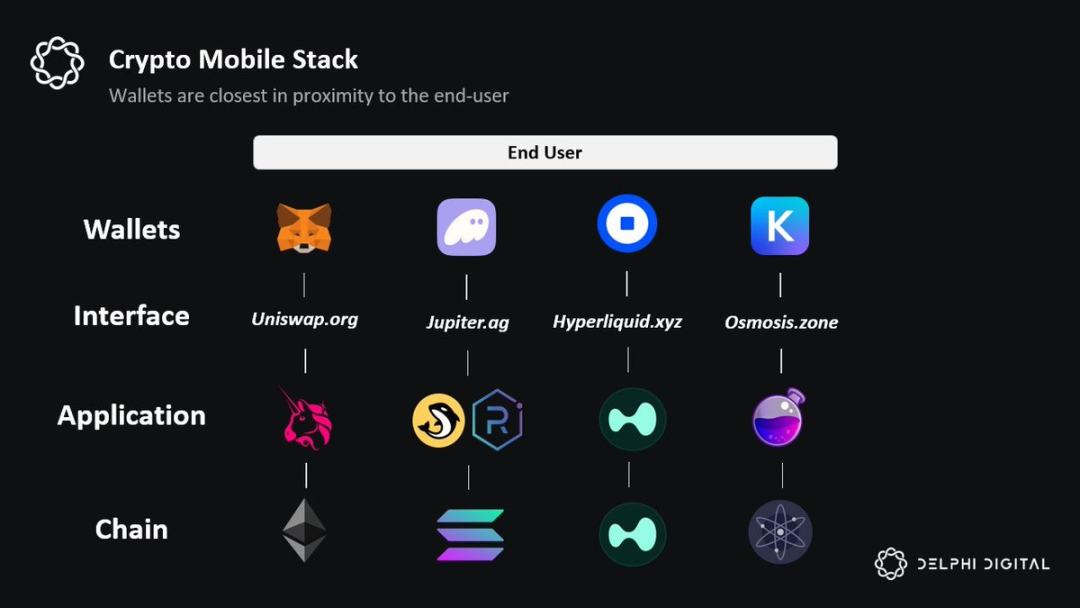

الإجابة الأبسط هي: من يملك المستخدم النهائي هو الفائز. وفي حين يمكن نظريًا أن يكون هذا أي واجهة أمامية بما في ذلك التطبيق، فإن نظرية "المحفظة السمينة" تنص على أنه لا يوجد أحد أقرب إلى المستخدم من المحفظة.

تهيمن المحافظ على تجربة المستخدم على الأجهزة المحمولة للعملات المشفرة: أفضل اختبار حاسم لفهم من يمتلك المستخدم النهائي في شبكة الويب المحمولة هو طرح السؤال التالي: أي تطبيق Web2 يتفاعل معه المستخدمون في النهاية؟ في حين أن معظم المستخدمين "يتفاعلون" مع واجهة Uniswap الأمامية لإجراء المعاملات، فإنهم لا يزالون يصلون إلى هذه الواجهة الأمامية من خلال تطبيق المحفظة. وهذا يعني أنه إذا كانت الأجهزة المحمولة تهيمن على تجربة المستخدم للعملات المشفرة، فإن المحافظ ستستمر فقط في تعزيز اتصالها بالمستخدم النهائي.

المحافظ هي المكان الذي يتواجد فيه المستخدمون: تطبيقات التشفير مالية بطبيعتها. على عكس Web2، فإن كل معاملة تقريبًا على السلسلة هي شكل من أشكال المعاملات المالية. لذلك، تعد طبقة الحساب بالغة الأهمية لمستخدمي التشفير. بالإضافة إلى ذلك، هناك بعض الميزات الفريدة لطبقة المحفظة: المدفوعات، والعائدات الأصلية على ودائع المستخدم الخامل، وإدارة المحفظة الآلية، وحالات الاستخدام الاستهلاكية الأخرى مثل بطاقات الخصم المشفرة.

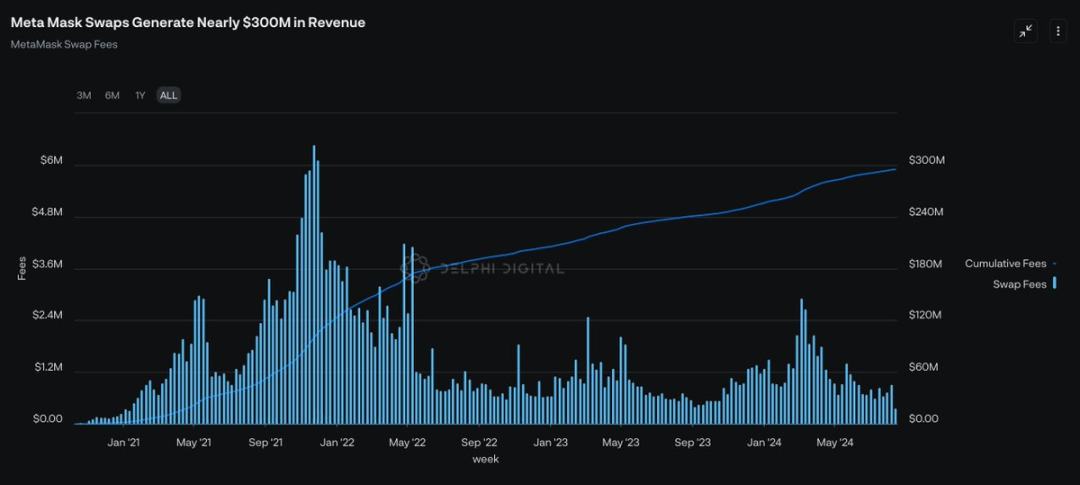

إن تكاليف تبديل المحفظة مرتفعة بشكل مدهش: فبينما من الناحية النظرية، يعد تبديل المحفظة أمرًا سهلاً مثل نسخ ولصق عبارة أساسية، إلا أنه يظل نقطة خلاف نفسية بالنسبة لمعظم الأشخاص العاديين. ونظرًا للمستوى العالي من الثقة التي يتمتع بها المستخدمون في مقدمي المحافظ، أعتقد أن العلامة التجارية و"التقارب" هما مصدران قويان للخنادق على مستوى المحفظة. وبإعادة النظر في سؤالنا الأصلي مرة أخرى: إذا رفعت المحفظة رسومها، فهل سيتحول المستخدمون إلى بدائل أرخص؟ يبدو أن الإجابة هي: "لا". تفرض ميزة المبادلة داخل محفظة MetaMask رسومًا قدرها 0.875%، ولكن لا يزال يستخدمها عدد كبير من المستخدمين.

التجريد التسلسلي: في حين أن التجريد التسلسلي مشكلة شائكة من الناحية الفنية، فإن أحد الحلول الأكثر إقناعًا هو حل مشكلة التجريد التسلسلي على طبقة المحفظة. تبدو فكرة إمكانية الوصول بسهولة إلى أي تطبيق على أي سلسلة من خلال رصيد حساب واحد بديهية بشكل خاص. oneBalance وBrahma وPolaris وParticle Network وCtrl Wallet وCoinbases Smart Wallet كلها تتحرك نحو هذه الرؤية. في المستقبل، أتوقع أن تلبي المزيد من الفرق احتياجات المستخدمين من خلال التجريد التسلسلي على طبقة المحفظة.

التآزر الفريد مع الذكاء الاصطناعي: في حين أتوقع أن يقوم وكلاء الذكاء الاصطناعي بتسليع بقية مجموعة blockchain بشكل متزايد، سيظل المستخدمون بحاجة إلى تفويض الوكلاء لتنفيذ المعاملات نيابة عنهم في النهاية. وهذا يعني أن طبقة المحفظة هي الأنسب لتكون الواجهة الأمامية الرسمية لوكلاء الذكاء الاصطناعي. تشمل الفوائد الأخرى لدمج الذكاء الاصطناعي في طبقة الحساب التخزين الآلي واستراتيجيات زراعة العائد وما إلى ذلك.

الآن بعد أن تناولنا "سبب" إقامة المحافظ لعلاقة مع المستخدم النهائي، دعونا نفكر في "كيفية" تحقيق الدخل من هذه العلاقة.

تتمثل الفرصة الأولى التي تتيح للمحافظ الإلكترونية تحقيق الربح في امتلاك تدفق طلبات المستخدمين. وكما ذكرت من قبل، فبينما ستستمر سلسلة توريد العملات المشفرة في التطور، فإن هناك أمراً واحداً سوف يتحقق حتماً: فالقيمة سوف تنتمي بشكل غير متناسب إلى أولئك الذين يتمتعون بأكبر قدر من القدرة على الوصول إلى تدفق الطلبات.

اليوم، تعد واجهات المستخدم التي تمتلك غالبية تدفق الطلبات من حيث الحجم هي الحلول والبورصات اللامركزية. ومع ذلك، هناك بعض الفروق الدقيقة التي يمكن تمييزها من هذا الرسم البياني وحده. من المهم أن نفهم أن تدفق الطلبات ليس متساويًا. هناك نوعان من تدفق الطلبات: (1) تدفق الطلبات الحساس للرسوم و(2) تدفق الطلبات غير الحساس للرسوم.

بشكل عام، يهيمن المحللون والمجمعون على تدفق الطلبات "الحساسة للرسوم". ونظرًا لأن هؤلاء المستخدمين يتداولون عادةً بأكثر من $100K في الحجم، فإن التنفيذ مهم بالنسبة لهم. لن يقبل هؤلاء المتداولون حتى 10 نقاط أساس من الرسوم الزائدة. وبالتالي، فإن المتداولين "الحساسين للرسوم" هم شريحة عملاء أقل قيمة. وعلى الرغم من أنهم يمثلون غالبية سوق الواجهة الأمامية من حيث الحجم، فإنهم يولدون قيمة أقل بكثير لكل $1 يتم تداولها.

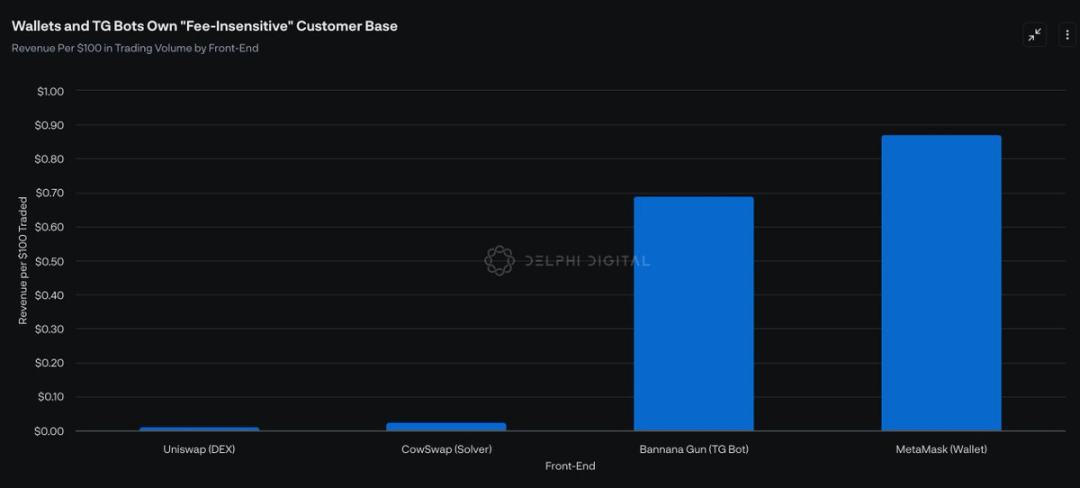

على النقيض من ذلك، المحفظة تبادل and TG Robot have a more valuable user base: “fee-insensitive” traders. These traders do not pay for execution, but for convenience. Therefore, paying 50 basis points for a trade is insignificant to these users. As a result, TG Robot and Wallet Exchange generate much higher revenue per $1 of trading volume.

بالنظر إلى المستقبل، إذا تمكنت المحافظ من الاستفادة من الاتجاهات المذكورة أعلاه واستمرت في امتلاك علاقات مع المستخدم النهائي، أتوقع أن تستمر ميزات التبادل داخل المحفظة في التهام حصة السوق من واجهات المستخدم الأخرى. والأهم من ذلك، حتى لو لم يتمكنوا من زيادة حصة السوق إلا بمقدار 5%، فسيكون لذلك تأثير كبير حيث تولد بورصات المحافظ عائدات أكثر بنحو 100 ضعف لكل $100 يتم تداولها مقارنة بواجهات المستخدم اللامركزية.

الفرصة الثانية للمحافظ للاستفادة من كونها قريبة من المستخدم النهائي هي التوزيع كخدمة (DaaS).

وبالإضافة إلى العمل كواجهة أساسية للمستخدمين للتفاعل على السلسلة، تعتمد التطبيقات في نهاية المطاف على المحافظ كقناة توزيع، وخاصة في شبكة الإنترنت المحمولة. وعلى هذا، وعلى غرار الطريقة التي تجني بها شركة أبل الأموال من خلال نظام التشغيل آي أو إس، يمكن للمحافظ أن تبرم صفقات حصرية مع التطبيقات في مقابل خدمات التوزيع. على سبيل المثال، يمكن لمزود المحفظة أن ينشئ متجر تطبيقات خاص به ويفرض رسومًا على التطبيقات من خلال نوع ما من اتفاقية تقاسم الإيرادات.

وعلى نحو مماثل، يستطيع مزودو المحافظ توجيه المستخدمين إلى تطبيقات محددة في مقابل بعض المشاركة الاقتصادية. وتتمثل ميزة هذا النهج مقارنة بالإعلان التقليدي في أن المستخدمين يستطيعون إجراء عمليات شراء والتفاعل مع التطبيقات بسلاسة من محافظهم. ويبدو أن شركة كوين بيز كانت تستكشف مسارا مماثلا بإطلاق تطبيقات "مميزة" و"مهام" داخل المحفظة.

يمكن للمحافظ أيضًا كسب بعض المكافآت المالية للترويج لسلاسل الكتل الناشئة من خلال رعاية معاملات المستخدمين. على سبيل المثال، ربما تريد Bearachain فقط جذب المستخدمين إلى سلسلة الكتل الخاصة بها. يمكنهم دفع Metamask لرعاية الرسوم عبر السلسلة ورسوم الغاز على Bearachain. نظرًا لأن المحفظة تمتلك المستخدم النهائي في النهاية، فيمكنهم التفاوض على بعض الشروط المواتية.

مع تزايد عدد المستخدمين الذين يستخدمون المحافظ كبوابة أساسية على السلسلة، يمكننا أن نرى تحولاً في الطلب من "مساحة الكتلة" إلى "مساحة المحفظة" حيث يصبح الاهتمام هو المورد الأكثر قيمة في اقتصاد التشفير.

أخيرًا، في حين تتمتع المحافظ بميزة واضحة في السباق لجذب المستخدمين النهائيين، إلا أنني لا أزال متحمسًا لآفاق واجهتين أماميتين بديلتين:

جوبيتر: من خلال مجمع DEX الخاص بهم، تمكنت جوبيتر من بناء علاقات قوية مع المستخدمين النهائيين. يمكن القول إن هذه هي أفضل نقطة بداية لهم لبناء منتجات أخرى ذات صلة في مجال التشفير، بما في ذلك Perps DEX، وLaunchpad، وLST الأصلية، ومؤخرًا، منتج RFQ/Solver. أنا متحمس بشكل خاص لإصدار تطبيق جوبيتر المحمول لأنه يسمح لهم باكتساب المستخدمين النهائيين في بيئة محمولة قبل أن تفعل المحافظ ذلك.

إنفينكس: من خلال العمل كمجمع واجهة أمامية للتطبيقات على سلسلة EVM وSolana، تهدف إنفينكس إلى توفير تجربة شبيهة بـ CEX مع الاحتفاظ بمبادئ مثل عدم الاحتجاز وعدم الإذن. ستوفر إنفينكس في البداية خدمات التداول الفوري والمراهنة، وتخطط لدمج العقود الدائمة والخيارات والإقراض والتداول بالهامش وتعدين العائد ووظائف إدخال العملة الورقية. من خلال تجريد طبقة الحساب واستخدام ميزات مألوفة من Web2 (مثل المفاتيح)، أعتقد أن إنفينكس لديها القدرة على استبدال المحافظ كواجهة أمامية قياسية للعملات المشفرة.

في حين أنه من غير الواضح بالنسبة لي اليوم من سيفوز في نهاية المطاف بالحرب على المستخدمين النهائيين، فقد أصبح من الواضح بشكل متزايد أن (1) اهتمام المستخدم و(2) تدفق الطلبات الحصري سيظلان الموارد الأكثر ندرة وبالتالي الأكثر قابلية للربح في اقتصاد التشفير. سواء كانت محفظة أو بعض الواجهة الأمامية البديلة مثل Infinex أو Jupiter، أتوقع أن ملوك التقاط القيمة في التشفير سيكونون المشاريع التي تمتلك كلا الموردين.

تم الحصول على هذه المقالة من الإنترنت: نظرية "المحفظة السمينة": المستخدمون النهائيون وفرص الربح

اعتبارًا من 27 أكتوبر، كانت إحصائيات BTC وETH وTON على منصة TrendX كما يلي: بلغ عدد مناقشات BTC الأسبوع الماضي 12.74 ألفًا، بانخفاض 12.59% عن الأسبوع السابق؛ وكان السعر يوم الأحد الماضي $68,532، بزيادة 2.13% عن الأحد السابق. كان لدى ETH 3.96 ألف مناقشة الأسبوع الماضي، بزيادة 9.21% عن الأسبوع السابق؛ وكان السعر يوم الأحد الماضي $2,520، بزيادة 1.69% عن الأحد السابق. كان لدى TON 906 مناقشة الأسبوع الماضي، بانخفاض 15.43% عن الأسبوع السابق؛ وكان السعر يوم الأحد الماضي $4.99، بزيادة 0.83% عن الأحد السابق. مع اقتراب موعد الانتخابات الأمريكية في عام 2024، يولي المستثمرون اهتمامًا متزايدًا لديناميكيات السوق، وخاصة آفاق الأصول المشفرة مثل البيتكوين. تجاوز سعر البيتكوين $69,000، وتوقعات السوق لـ...