إصدار خاص من SignalPlus Macro Research: فترة الاستراحة

Despite a turbulent start to last week, U.S. stock futures on Friday returned to where they closed the previous week, before Monday’s plunge, and Treasury yields actually rose slightly, though they remain well below July levels. Was all this turmoil just a false alarm?

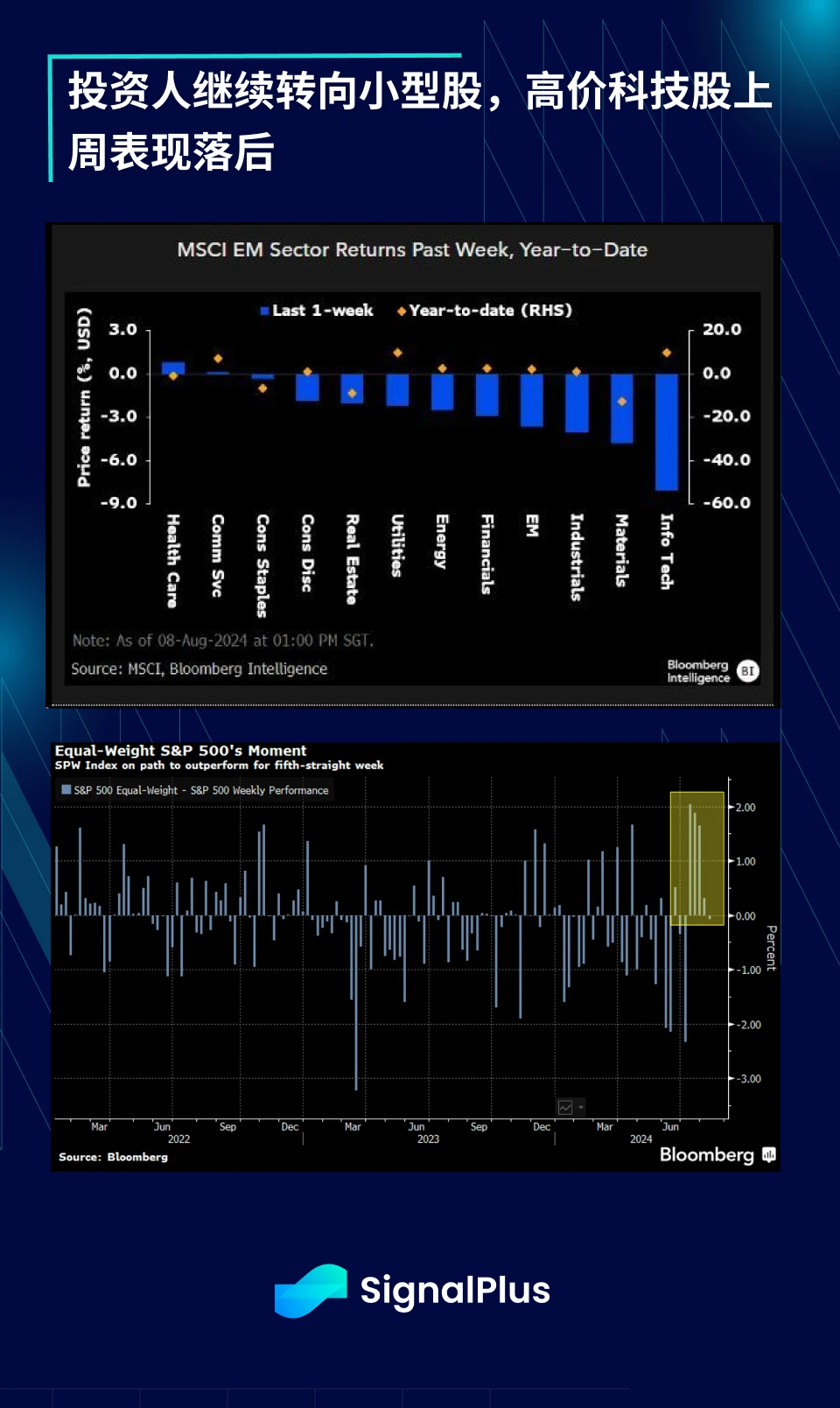

Looking further down, we can see a more obvious rebalancing trend, with high-priced stocks underperforming, and the equally-weighted SPW index outperforming the market-cap-weighted SPX index for the fifth consecutive week. This week, the market will focus on corporate earnings reports, especially the consumer sector, to confirm whether the trend of slowing consumer spending can be confirmed by corporate earnings data.

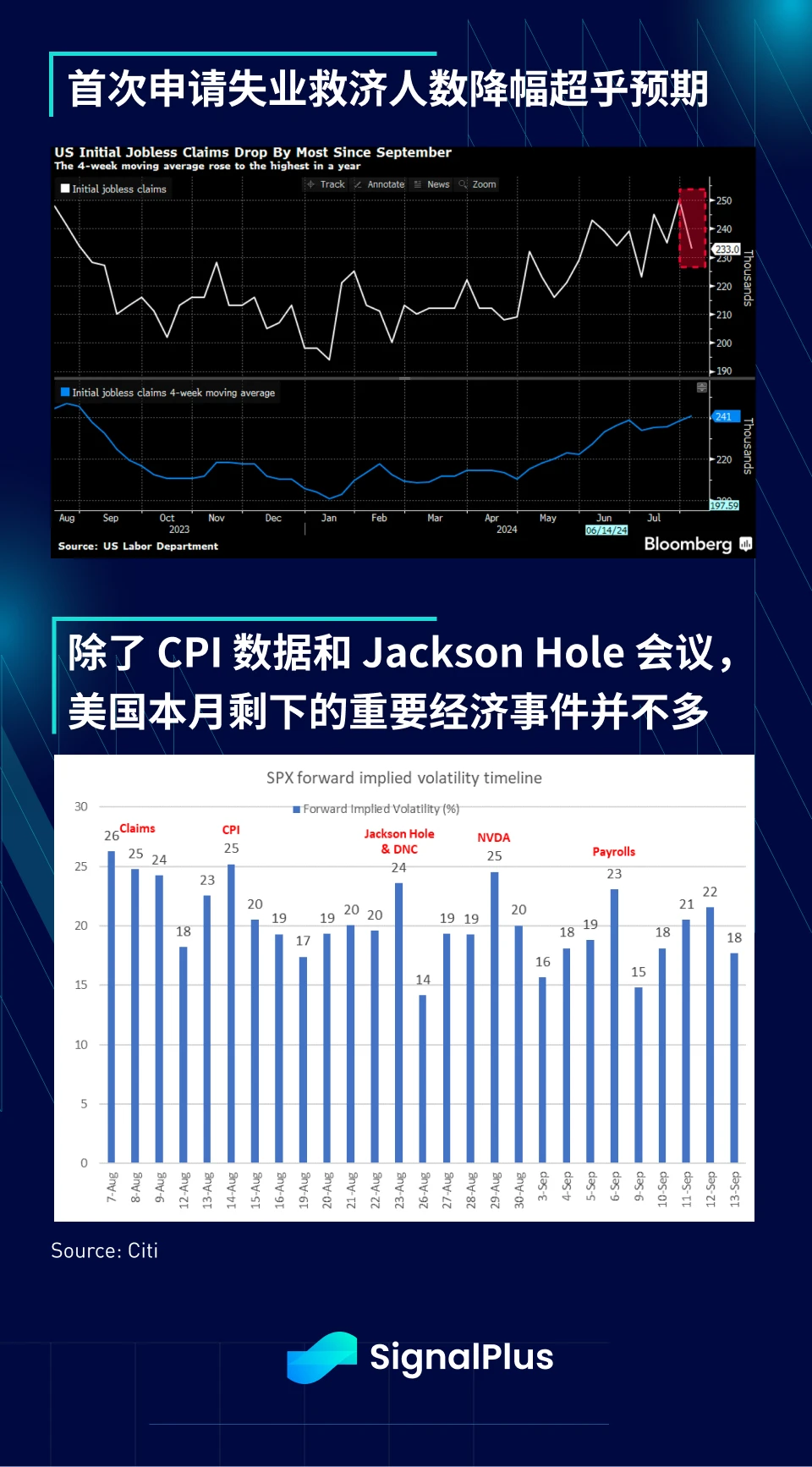

The unexpected drop in first-time unemployment claims last week helped boost market sentiment. There wasn’t much important economic data this week other than PPI/CPI, but the Fed’s current focus on the job market may temporarily reduce the market’s focus on inflation data. Negative supply shocks from tariffs, energy prices, and immigration restrictions could push price data up unexpectedly, but these upward momentum will likely be offset by weak wages and a sharp slowdown in housing prices, bringing inflation back to the Fed’s long-term goal (economists predict a 0.18% month-over-month increase in core CPI). In addition, Fed officials Goolsbee and Daly also tried to downplay recent panic, saying the market “overreacted” to the July jobs report, a view that was also confirmed over the past week.

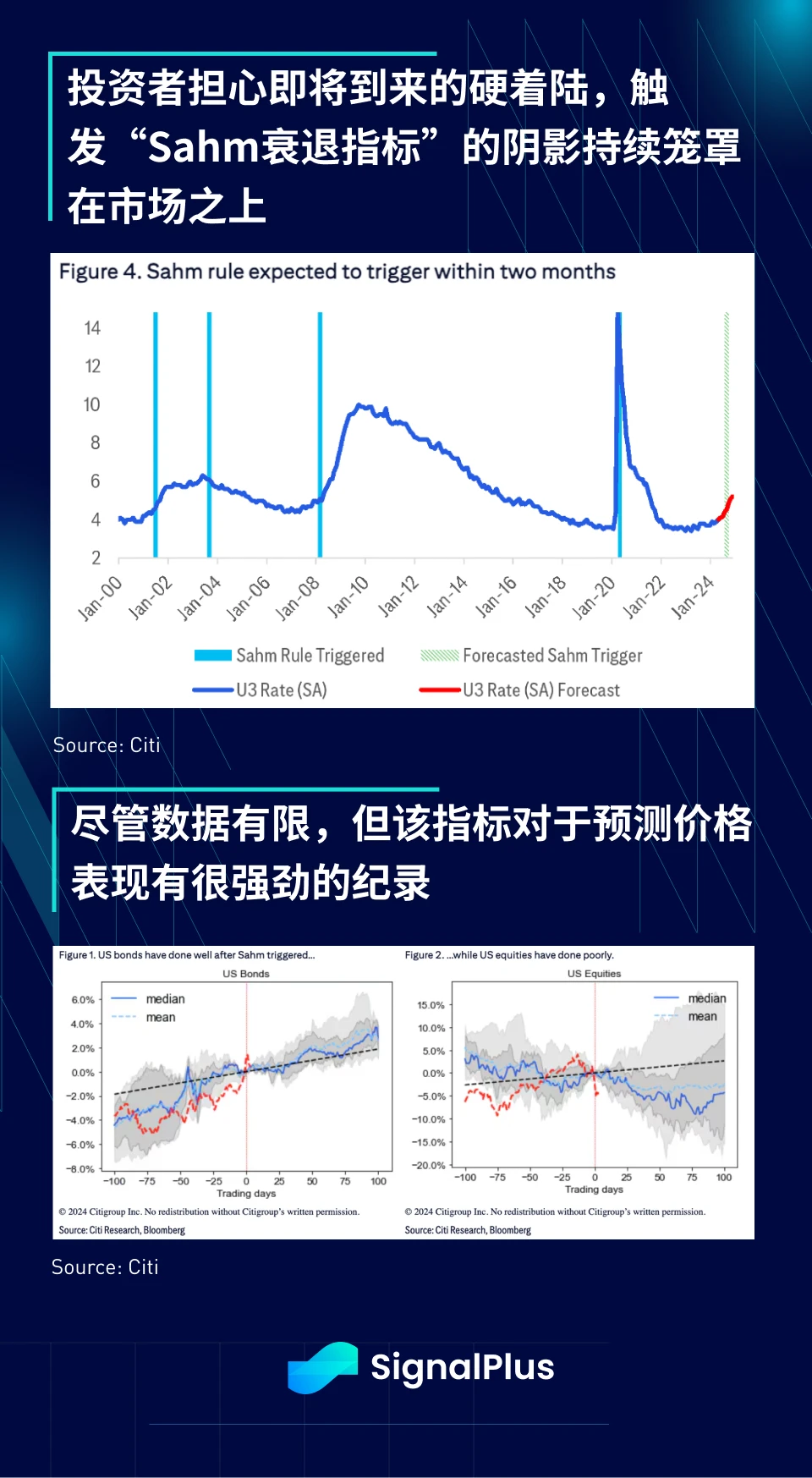

That said, given the magnitude of forced liquidations and losses at the beginning of last week, we expect the market to remain defensive and any counter-trend rallies to be limited, at least until the Jackson Hole conference. In addition, as the oft-cited “Sahm Rule” approaches triggering, investors may need more hard economic data to confirm whether a hard landing is imminent, and this recession indicator has a strong track record of predicting asset price performance despite limited data.

Looking at the market structure, the weakening of internal liquidity has also become a headwind for risk sentiment in the short term. Despite the recent easing of the Peoples Bank of China, global central bank liquidity is actually in a state of withdrawal, and banks excess reserves and reverse repo balances have continued to decline in recent weeks. In addition, as dealers risk appetite has declined, secondary liquidity in the US market has fallen to its lowest level of the year and is unlikely to recover to a large extent until at least the fourth quarter. JPM estimates that three-quarters of the worlds carry trades have been closed, and risk funds may need a long cooling period and re-evaluation before they can start larger-scale risk trades again.

Speaking of carry trades, the situation in Japan seems to have fundamentally changed, and a lower USD/JPY could bring an early end to the hawkish stance of the Bank of Japan. The Bank of Japan was blamed for triggering the risk-off chain reaction last week, so their committee will be forced to take a more cautious approach to further rate hikes, especially as the exchange rate could depress inflation in the coming months. In fact, Bank of Japan Deputy Governor Uchida recently made the following clarifications:

-

“Given the extremely volatile developments in domestic and overseas financial and capital markets, the Bank of Japan needs to maintain an accommodative monetary policy at the current policy rate for the time being.”

-

“When financial and capital markets are unstable, the central bank will not raise policy rates”

-

As the yens depreciation is corrected, the upside risk from higher import prices has been reduced accordingly.

These all strongly suggest that the Bank of Japan will return to a mildly dovish stance for the foreseeable future.

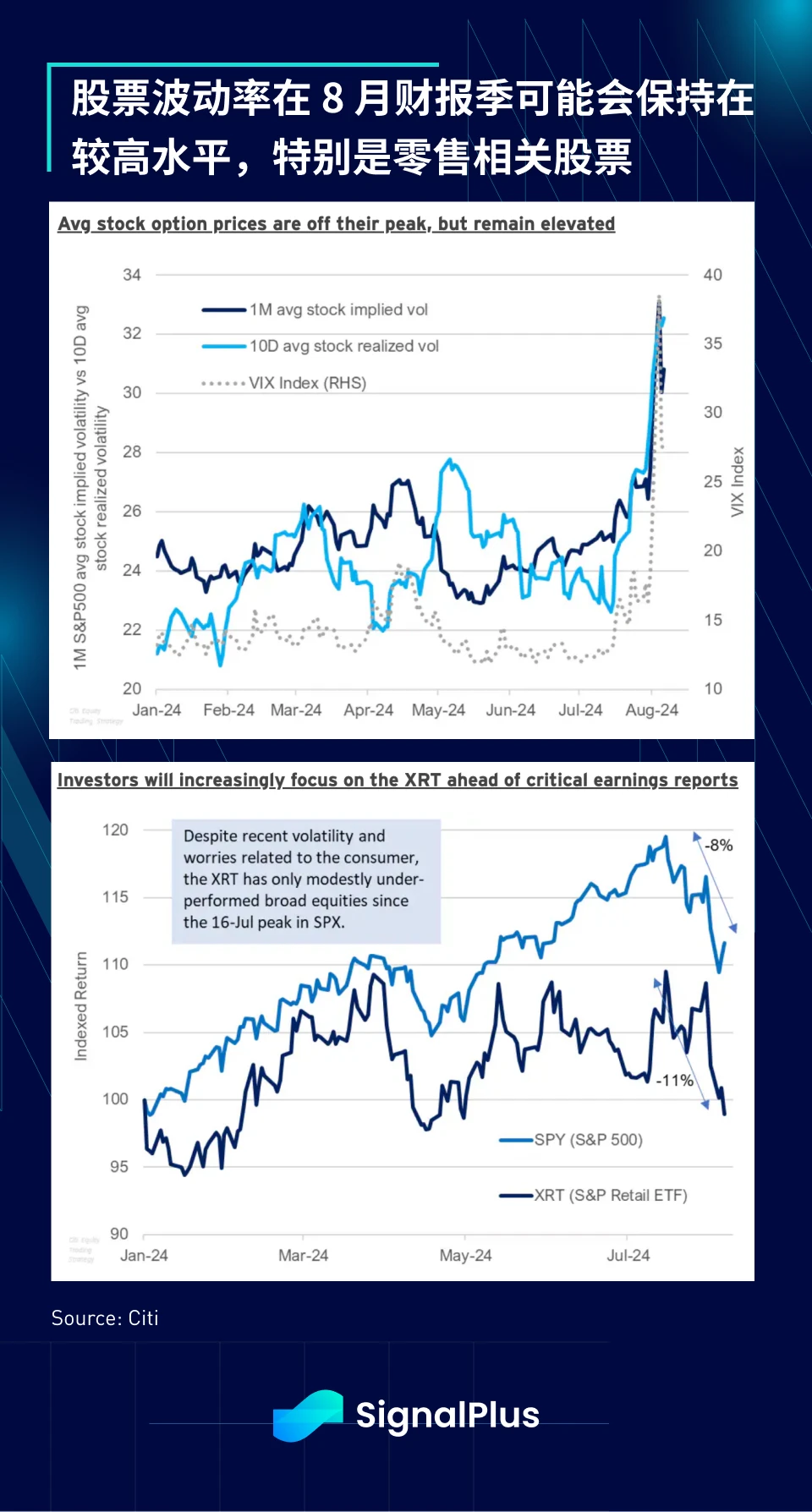

Back in the US, although there are fewer macro events in August, the VIX index is likely to remain high, and individual stocks are expected to see more dramatic price movements around quarterly earnings results. The focus will be on companies such as Walmart and Home Depot to assess consumer purchasing power. Higher-frequency credit card data has already shown weaker retail sales in July. Traders should pay special attention to the performance of consumer sectors (such as the XRT ETF) relative to the overall index to get more signals of further declines in consumer sentiment.

Regarding recession risks, different macro asset classes are showing different predictions based on historical trends, among which US bonds and commodities are the most forward-looking, while stocks and credit do not care about a hard landing.

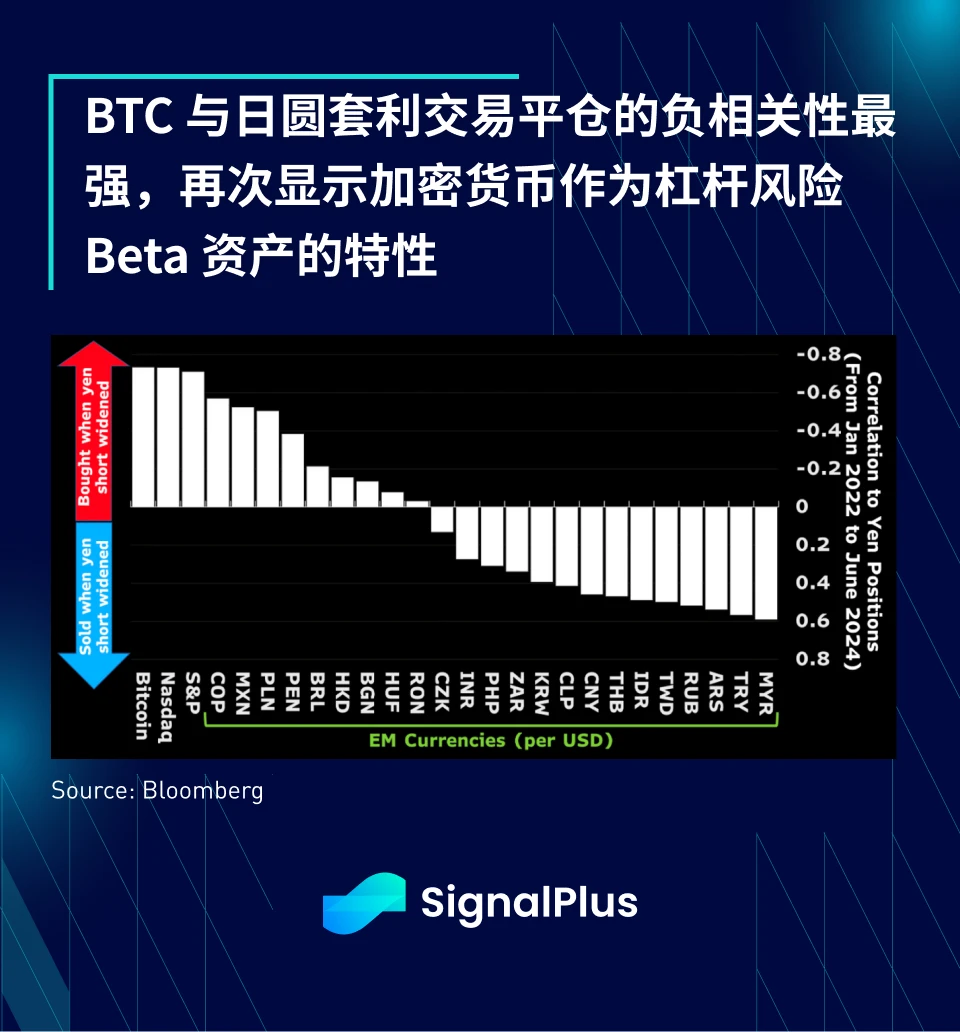

On the crypto side, risk sentiment remains challenged, with BTC being hurt the most by the “unwinding of yen carry trades” based on two-year correlation data, again showing crypto is a frontier risk asset like the leveraged Nasdaq, and we expect prices to continue to move with the ups and downs of overall risk sentiment rather than any “diversification” argument.

In terms of technical signals, on-chain data from 1 3D and Glassnode show that BTC’s cost has fallen below its short-term and 200-day moving averages, with little support above the “real market average” (the total average of all on-chain acquired prices) of about $47K, which is the reference point for the mean reversion model.

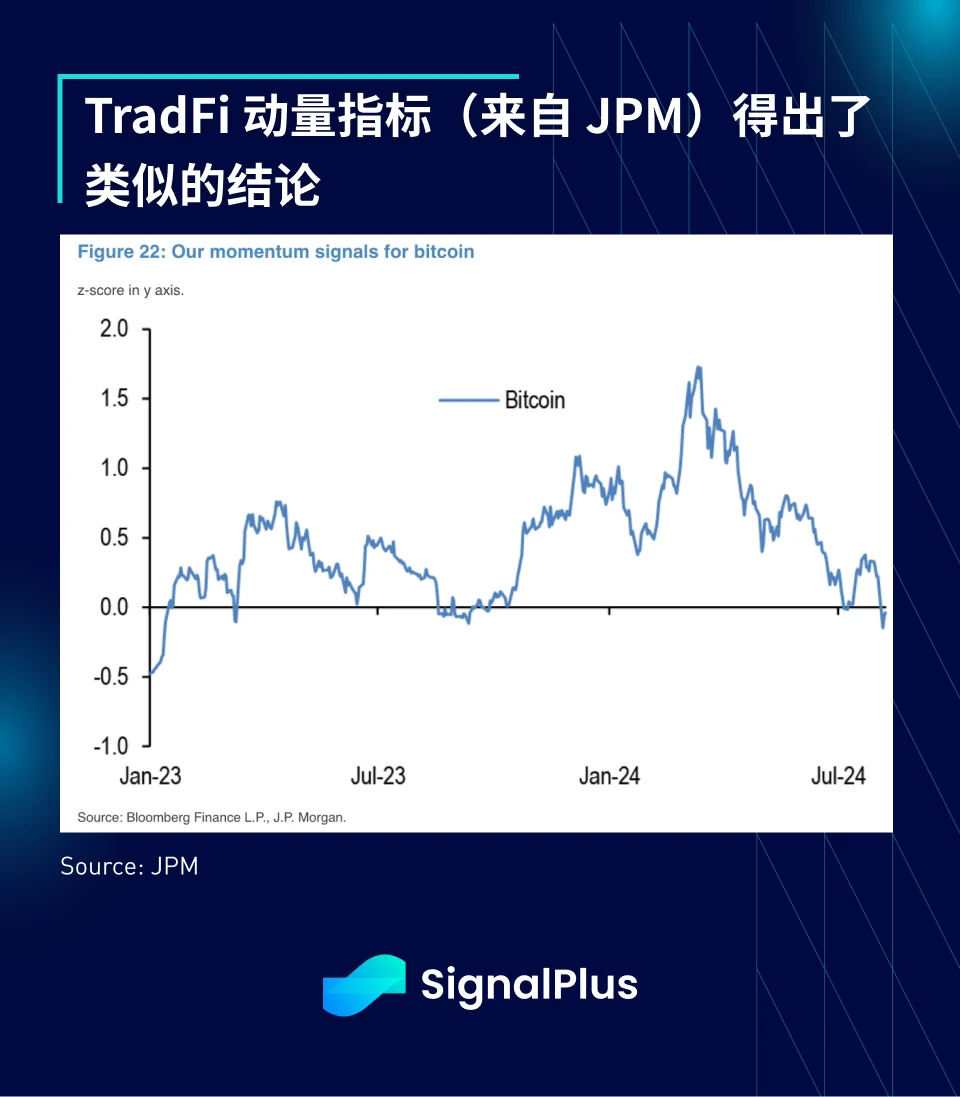

In addition, the on-chain MVRV ratio (market capitalization vs. realized market capitalization) has fallen below its 1-year average, suggesting that the decline may continue. JPMs traditional momentum indicator has reached a similar conclusion.

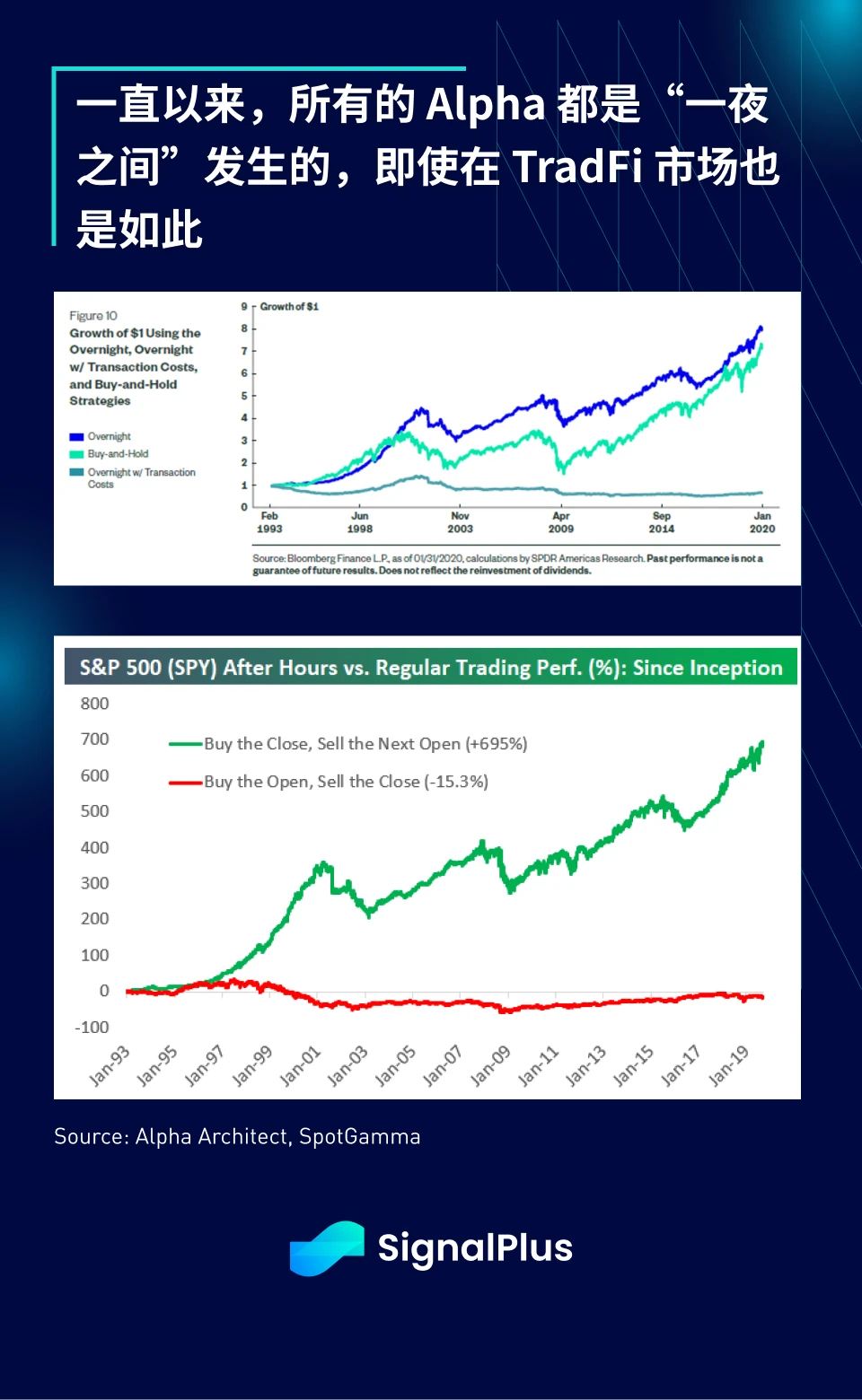

Overall, recent inflows into ETFs have been disappointing, especially for ETH, which has seen a net outflow of $400 million since the product was launched on July 24. In fact, Bloomberg data shows that almost all of BTCs price action since January has occurred during U.S. ETF trading hours, while all cryptocurrency gains this year have occurred during non-trading hours (i.e., Asian hours), as the market has effectively moved ahead of the New York opening.

Anyone who has studied the markets for a long time will realise that this is the same situation with the stock market, i.e. all the “fun” happens before the New York open and the index performance will generally be flat if it is only traded during the “US session”.

So, does this story tell us to buy at the US close and sell at the US open? As always, we are not offering any investment advice here, we can only suggest that our Asian readers should sleep well during bedtime and not stay up late to trade during the US session.

يمكنك استخدام وظيفة لوحة التداول الخاصة بـ SignalPlus على t.signalplus.com للحصول على مزيد من المعلومات حول العملات المشفرة في الوقت الفعلي. إذا كنت ترغب في تلقي تحديثاتنا على الفور، فيرجى متابعة حسابنا على Twitter @SignalPlusCN، أو الانضمام إلى مجموعة WeChat الخاصة بنا (إضافة مساعد WeChat: SignalPlus 123)، ومجموعة Telegram ومجتمع Discord للتواصل والتفاعل مع المزيد من الأصدقاء. الموقع الرسمي لـ SignalPlus: https://www.signalplus.com

This article is sourced from the internet: SignalPlus Macro Research Special Edition: Intermission

Related: Mini Program Revolution: Telegram Mini Program’s Web3 Transformation Journey

Original author : YuppieZombie , Lumos Ngok , Noah Ho introduction Recently, the Telegram ecosystem has developed rapidly and has become a hot topic in the Web3 field. Telegram, a communications giant with 900 million users, has quietly launched mini-programs and robot development functions. Currently, Telegram mini-programs can completely replace most websites, support seamless authorization, integrated payment through 20 payment providers (including Google Pay and Apple Pay), and more customized functions, such as automatic news and news summary information services, and the recently popular Catizen mini-game. In addition, Telegram has also developed the Ton chain to support convenient blockchain transactions. This traffic + payment route similar to WeChat has enabled Telegram to develop rapidly. Chinese users are already very familiar with WeChat Mini Programs. Nowadays, Mini Programs have penetrated into…