My XP

0

تسجيل الدخول

Original article by: Armonio, AC Capital

In this article, we present two interrelated narratives: the first outlines the technical evolution of DeFi liquidity, while the second highlights the transformative impact of on-chain barter from an economic history perspective. Together, our goal is to demonstrate that a profound DeFi revolution is coming, it just takes a little more patience. Those visionary builders who stick with it will eventually be rewarded by the market.

We have carefully tracked the development of the DEX market to illustrate that the emergence of on-chain barter is no accident, and on-chain barter is a real game changer. It represents an important chapter in the history of Web3 builders. Achieving its functionality required a lot of innovation and improvement, not only within DEX, but also at the underlying infrastructure layer.

If on-chain barter becomes an important historical milestone, we believe that all related efforts and contributions should be appropriately commemorated.

Since January 2023, Bitcoin has fallen to lows and rebounded to new highs, driven by ETF approval and new expectations of quantitative easing. However, the prices of most altcoins are not like before, showing stronger upward momentum. Some investors scoff at real innovation and regard the crypto world as a criminal domain. At various conferences, industry insiders even refer to the entire industry as similar to a casino. Many crypto enthusiasts revel in the excitement of PvP (player versus player). While memecoin was sought after in the early stages of the bull market, value tokens have been ignored by the market.

Veteran players feel that this time is indeed different. Some developers are confused and question whether cryptocurrency can really change the real world. Since last year, many have turned their attention to artificial intelligence, while more are still hesitant.

We cannot ignore the impact of venture capital and team greed, misaligned interests, unethical behavior, and short-term thinking. The market has been in a dark forest for a long time. In addition to the code, there are not many rules to regulate participants. These problems have existed for a long time and are not enough to explain the weakness of this round of bull market. Therefore, we put forward an additional reason: the self-inflation within the crypto market is no longer sufficient to provide the necessary liquidity for our crypto ecosystem.

Therefore, we propose an additional reason: the self-inflation within the crypto market is no longer sufficient to provide the necessary liquidity for our crypto ecosystem. See the figure below:

The above chart shows the activity of various cryptocurrencies. If we look at the proportion of transactions, we can see that in the past one or two years, most transactions are in USD stablecoins. If the market value of USD stablecoins cannot be expanded, as new coins continue to be issued, the liquidity pool will be drained.

Historically, altcoins rarely lack liquidity because tokens can become liquidity for others during Bitcoin and Ethereum bull markets. But now, most trading pairs are stablecoins pegged to the US dollar. Even if the value of Bitcoin or Ethereum explodes, it will not be useful. The status of stablecoins makes it difficult for BTC and ETH to inject liquidity into other tokens.

All stablecoins and other compliant financial instruments pegged to the dollar are bait. Cryptocurrencies follow the Wall Street clock.

In October 2014, Tether began to offer a stable digital currency that bridges the gap between cryptocurrencies and fiat currencies, providing the stability of traditional currencies and the flexibility of digital currencies. Now it has become the third largest token by market capitalization. In addition, USDT has the most trading pairs in the index, 10 times more than Ethereum or wBTC.

In September 2018, Circle partnered with Coinbase to launch USD Coin (USDC) under the Centre Consortium. It is pegged to the US dollar, and each USDC token is pegged to the US dollar reserve at a ratio of 1:1. As an ERC-20 token, USDC can be seamlessly traded and integrated with various decentralized applications.

On December 10, 2017, the Chicago Board Options Exchange (CBOE) took the lead in launching Bitcoin futures. Even if it is settled only in US dollars, it can have an impact on the spot price of Bitcoin, especially since the current Bitcoin holdings already account for 28% of the global market.

Wall Street not only affects the crypto market physically, but also psychologically. Do you remember when we started paying attention to the Feds attitude, Greyscales trust write-downs, the FOMCs dot charts, and the cash flow of the BTC-ETF? All this information affects our behavior psychologically. Stablecoins are bait cast by the US government. Since we accept stablecoins pegged to the US dollar as a means of providing liquidity, it has begun to accumulate consensus, replace the liquidity role of crypto native tokens, compete and weaken the credit of other tokens, and the US dollar has gradually dominated the market for universal equivalents.

In this way, we lose our own market rhythm.

I am not blaming the stablecoins pegged to the US dollar. On the contrary, this is the natural result of fair competition and market selection. Tether and Circle help investors invest in assets pegged to the US dollar directly on the chain, allowing them to bear risks equivalent to the US dollar and providing investors with more choices.

We all struggle with liquidity!

Liquidity is a fundamental feature of the market, and any innovation that can improve market liquidity is a major historical progress.

According to organizational theory, a market is defined as a structured environment for the exchange of goods, services, and information between buyers and sellers. This environment is guided by established rules, norms, and institutions to facilitate coordination, reduce transaction costs, and support efficient economic interactions.

Liquidity is critical to market organization because it directly affects the efficiency, stability, and attractiveness of markets. High liquidity reduces transaction costs by minimizing slippage and increasing trading volume. Liquid markets also exhibit greater price elasticity and help find more accurate price information. Information economics emphasizes the role of markets in information discovery. In an ideal market, information flows freely, enabling participants to make informed decisions, optimize resource allocation, and achieve equilibrium prices. Highly liquid markets produce reliable information that helps allocate resources more efficiently.

Whether it is price discovery efficiency, price stability and resilience, or lower transaction costs, these characteristics enhance the markets ability to attract participants. Therefore, improving liquidity is essential for any market.

Money was an innovation designed to alleviate liquidity problems.

Academically, there are two mainstream theories about the origin of money. One holds that money is a convenient means of transaction, which is accepted by the general public and scholars. The other comes from David Graebers Debt: The First 5000 Years. He believes that money originates from debt relations, but at the same time also recognizes the role of money as a universal equivalent.

In addition to Glyn Daviss A History of Money: From Antiquity to the Present Day and Karl Marxs Capital: Volume I, there are other sources that take a similar view of the origins and evolution of money.

For example, Niall Ferguson points out in The Rise of Money: A World Financial History that the development of money also originated from societys need for an efficient exchange system, starting with barter and gradually evolving into a more complex system using objects with intrinsic value.

Similarly, in Felix Martin鈥檚 Money: The Unauthorized Biography, the author touches on the concept of money as a social technology that developed out of the need for a more efficient system of exchange. Martin, like Marx, sees money as a universal equivalent that originated as a common commodity in the age of barter.

Finally, David Graeber鈥檚 Debt: The First 5000 Years offers a unique perspective, arguing that money evolved from systems of debt and obligations that predate the invention of money itself. However, Graeber鈥檚 view remains consistent with the core idea that money was created as a universal equivalent to facilitate the exchange of goods and services.

These sources further emphasize the role of money as a medium of exchange, echoing the views of Davis and Marx.

To sum up, the academic consensus on money is that the function of money after its birth is a general equivalent and a product for solving market liquidity. The disagreement lies in whether the starting point of the currency carrier is a commodity or a debt.

Currency is the answer of ancient elites to the problem of market liquidity before the emergence of the Internet of Value. Currency is a means to increase liquidity.

The old forces that used to equate money with liquidity rarely tried to improve the organizational structure of the market to achieve better liquidity conditions, and they never considered market liquidity without money. Perhaps it was because they were like fleas trapped in a covered box for too long and forgot how high they could jump.

The primary goal of any market is to provide the most accurate prices and the most efficient allocation of resources. Every component, mechanism, and structure is designed to achieve this purpose. Since ancient times, humans have continuously created new ways to make markets more efficient.

Over the centuries, the market has undergone tremendous changes. The price generation mechanism has undergone many upgrades. In order to meet different economic needs, the market has developed various settlement procedures, such as dealer markets, order-driven markets, brokerage markets, and dark pool markets.

With the advent of blockchain technology, we have encountered new limitations and viable solutions to the old liquidity game. We have had to create innovative ways to solve exchange needs and provide liquidity for tokens.

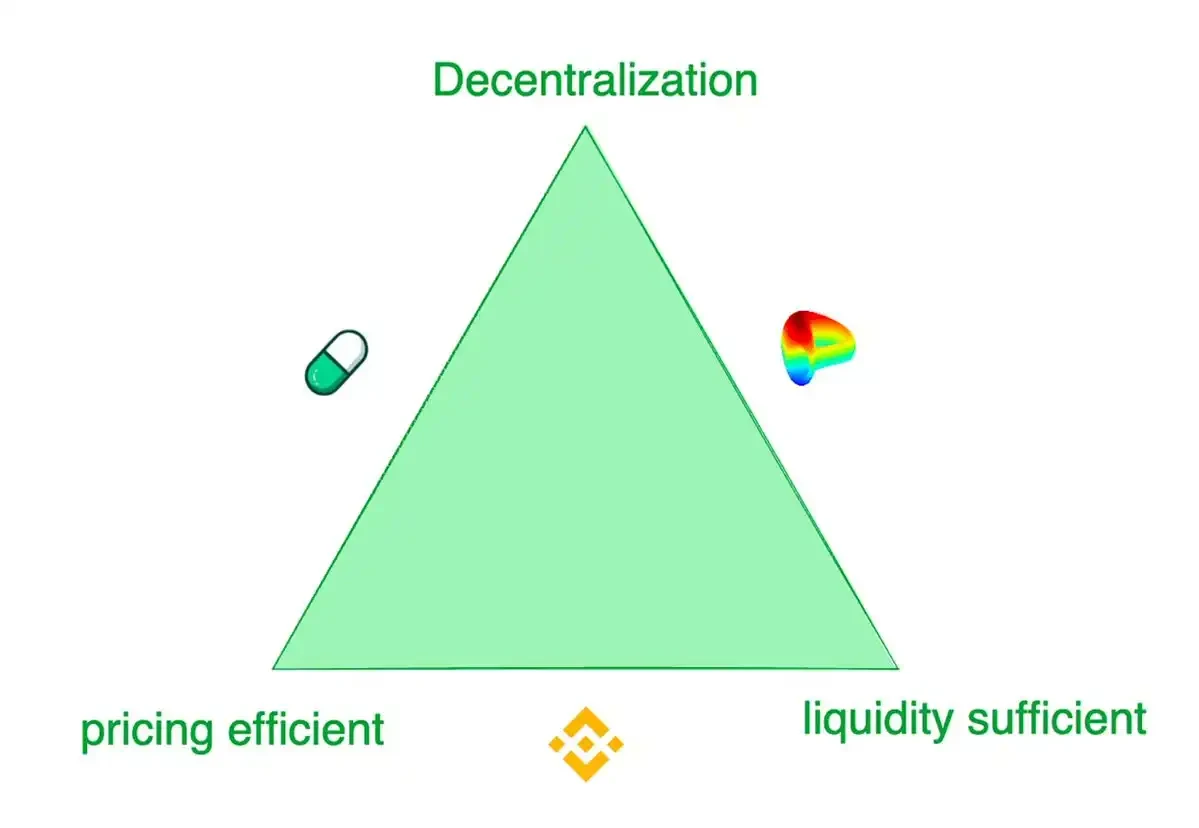

To summarize, contemporary token trading platforms face a trilemma: 1) sufficient liquidity, 2) effective pricing, and 3) decentralization.

The exchange trilemma

While centralized exchanges like Binance offer the best trading experience, they are also plagued by risks such as fraud and monopoly. In contrast, decentralized exchanges cater to different demand scenarios. For example, Pump.fun offers extremely sensitive token supply curves, while Curve offers the best liquidity in most cases, rather than price discovery sensitivity. These exchanges adopt various models to meet the trading preferences of their different target customers.

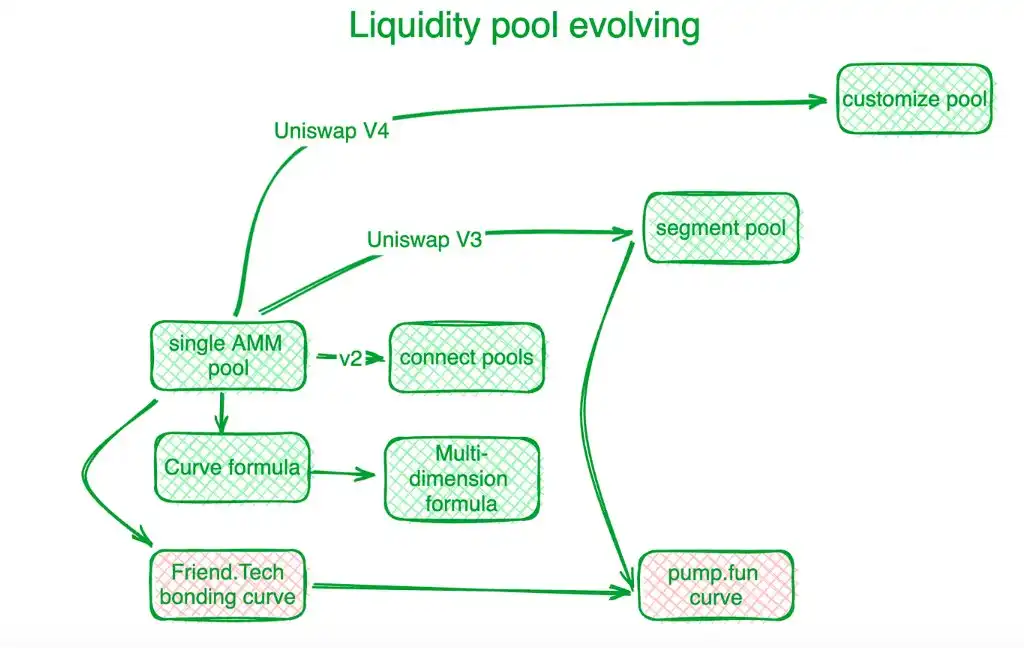

Decentralized exchanges have made significant progress in solving this trilemma and other on-chain trading challenges through innovative solutions. Uniswap is a benchmark in this niche industry. The innovation of the joint curve marks the beginning of a new era. Before Uniswaps X*Y=C curve, decentralized exchanges used order books to settle on-chain trading needs. Subsequent automated market makers (AMMs) followed Uniswaps exploration direction and created liquidity pools. In Uniswap V2, liquidity in different trading pair pools was connected algorithmically. Uniswap V3 introduced segmented liquidity pools, allowing users to define the price range where they want to provide liquidity. Uniswap V4 further advances this by providing customized solutions for liquidity pools.

Curve Protocol, which focuses on stablecoin trading, has developed its own supply liquidity curve to provide more token liquidity around a predetermined equilibrium point. To meet the challenges of joint liquidity pools, Curve Protocol invented a multi-dimensional formula that enables users to place more than two tokens in a liquidity pool, thereby sharing liquidity among all tokens in the pool. In practice, CEXs show better liquidity and pricing efficiency. On-chain pricing systems usually lag behind off-chain CEXs. Hashflow established a professional market maker pool (PMM) with the help of oracles to connect on-chain and off-chain liquidity.

However, traditional bonding curves are costly for small-scale tokens. Friend.tech designed a steeper bonding curve to accommodate small investors who prefer price appreciation over ample liquidity. As the value of a token increases, investor preferences shift toward liquidity. Inspired by this, Pump.fun uses a steeper curve when the token value is low, but as the value increases, the curve shifts to a different slope or even a different curve.

The Evolution of Liquidity Pools

MEV is another arena for decentralized trading platforms.

Maximum Extractable Value (MEV) refers to the profit that a miner or validator earns through its ability to arbitrarily include, exclude, or reorder transactions within the blocks it generates. It can be considered as a liquidity cost. In a liquidity pool, each exchangeable token (liquidity) is distributed along a price scale, and the liquidity of each price span is limited. Those who are able to interact with the liquidity pool contract earlier gain an advantage by obtaining better prices. In this way, MEV is intrinsically linked to the liquidity problem.

MEV is manifested in decentralized transactions by sorting transactions to obtain favorable liquidity. This competition improves the efficiency of on-chain transactions, but also harms the interests of all parties. In order to retain as much transaction value as possible in decentralized trading platforms and return it to participants more completely, developers have built algorithms and mechanisms at the application level to intercept MEV generated by transactions.

As a veteran in the field of MEV management, Flashbots focuses on the distribution of node revenue. In order to ensure the transparency and efficiency of MEV distribution, they established a MEV auction system at the node level. Eden Network pursues similar goals. KeeperDAO combines MEV extraction and staking, allowing participants to benefit from MEV while protecting users from its negative impact. Jito Labs, a liquidity staking project on the Solana network, also solves this problem.

Projects led by Cow Protocol, including UniswapX and 1inch Protocol Fusion, all use auction interaction rights to keep MEV within the transaction process instead of migrating it to the node accounting level. Intercepting MEV protects active traders and AMM liquidity pools, eliminating the previous dilemma of DEX bribing nodes and MEV loss.

As mentioned earlier, token liquidity is scattered in various custom pools controlled by different protocols on different blockchains or layer 2 solutions. Polygon proposed a concept of aggregation layer to collect liquidity from different layers. Initially, some DEX aggregators emerged to integrate liquidity from these different pools. However, after accumulating enough traffic, a more effective approach is to create platforms that promote competition, such as 1inch and Cow Protocol.

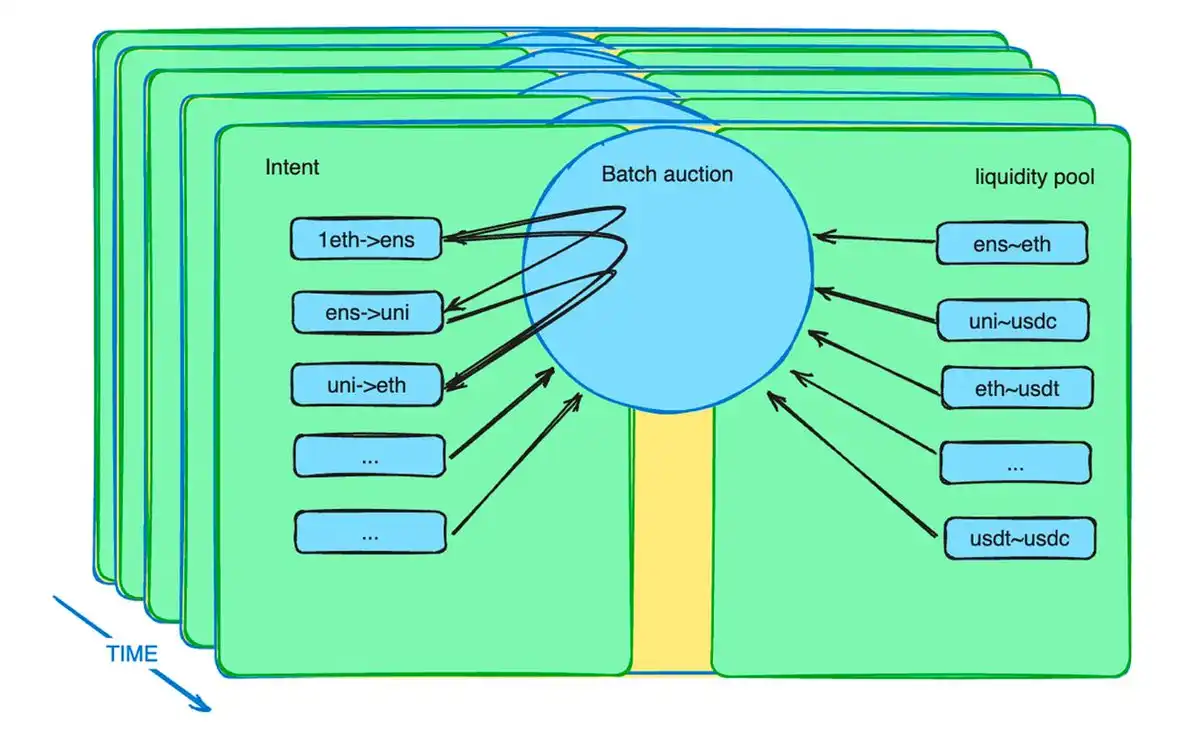

Furthermore, the batch auction mechanism enhances the role of agents. It introduces a new market mechanism to ease liquidity constraints. In practice, traders can place orders at a limited price within a specified period. The batch auction smart contract collects these orders and bundles them into a batch. The smart contract then allows agents to bid on these batches. The agent who offers the best price will win the opportunity to settle all potential trades within the batch.

CoW protocol batch auction mechanism description

Batch Auction Draft from Cow Protocol

After years of DEX development, the industry has accepted methods such as batching, auctions, and order matching to optimize trading results for all participants. The specific implementation of auction mechanisms varies, but in general, they shift the complexity of optimizing exchange results to professional participants and redistribute the remainder to relatively unsophisticated exchangers.

Batch auction diagram

This type of auction can solve many DEX problems in multiple ways.

In addition to the MEV redistribution mentioned in the previous section, batch auctions can do much more than that. What traders send to smart contracts is not instructions, but an intention. This intention can last for several minutes. These intentions are packaged into a batch and proposed to a group of competing specific trading agents. We know that there are a lot of intentions and a variety of liquidity pools, and optimization is a difficult problem. Professional things are left to professionals, which can improve system efficiency.

Batch auctions maximize their value efficiency by sacrificing time efficiency (each transaction intention lasts for a few minutes by default), forming differentiated competition with CEX.

Whats more? Barter is back!

As the ancestor of all cryptocurrencies, Bitcoin defines itself as a currency. The decentralized market is an emerging field without clear consensus constraints. Barter is a cryptocurrency-native trade model that naturally fits into this environment.

DEX is often referred to as an exchange platform. In its trading model, there is no predetermined universal equivalent role. Traders do not have to use fiat currency or stablecoins as intermediaries. At the liquidity pool level, any trading pair is allowed. Traders can use any token they like to exchange for other tokens and bear the cost of liquidity inefficiency.

However, there are significant limitations to relying solely on liquidity pools for bartering. There are not enough pairs for all types of bartering. Due to the structure of liquidity pools, liquidity deployment times are long and it is difficult to find an equilibrium price. Therefore, liquidity must be deployed over a wider range of prices, which leads to scarcity compared to the limited-time demand of intent. This is where intent and batch auctions come into play.

Assume that there are multiple potential trading intentions that can meet each others needs, supplemented by liquidity from the fund pool. In this case, barter transactions will return to the market in a more efficient state. As the scalability of web3 infrastructure increases and more commodities and financial instruments join web3, batch auction smart contracts will capture thousands or even millions of trading intentions per second. Any token can be used as a means of liquidating other tokens. We will get rid of the liquidity limitations imposed by the US dollar in the general context.

The resurgence of barter represents a renaissance, responding to market demands.

Historically, when money was invented, it was difficult for traders to find direct barter opportunities that met their immediate needs. Therefore, they exchanged goods for a universal equivalent (money), and then purchased what they really needed in another transaction. Once this exchange model became widely accepted, it forced real barter needs to be split into at least two steps, and the direct barter market was completely replaced.

Today, on-chain barter demand exists in the form of short-term intentions. Batch auction smart contracts collect these intentions. Anyone, whether human or AI agent, can meet the entire transaction demand as long as they provide the best bid. If the intention is matched, there is no need for a stablecoin pegged to the US dollar. The token retains its utility and shares liquidity as before. This matching of barter demand is based on the global market and a stronger information matching ability, which is based on the cultural tradition of cryptocurrency barter.

In the short term, the existence of intention time span enables arbitrageurs to transfer liquidity across chains and from off-chain to on-chain. For example, an algorithm that finds price gaps between different chains or between DEX and CEX can buy at a lower price and sell at a higher price within a specified time. It may need to use financial instruments to hedge market risks to achieve a risk-free state. However, in the future, when on-chain, off-chain, and cross-chain transactions can be synchronized, all transactions can be executed at the same time. This can eliminate risk costs and provide traders with the best experience.

The reason is simple. If we look back at the history of money, the right to coin was originally private. According to Debt: The First 5000 Years, debts can be personal. Even in modern times, as detailed in A Monetary History of the United States, 1867-1960, private individuals could once mint silver coins. Today, however, all credit is issued by the Federal Reserve. Even Bitcoin is denominated in dollars, which is a misfortune of the times. The dollar has overshadowed cryptocurrencies. Barter trading provides an opportunity to recapture this status, which is the era of the importance of barter resurgence.

The development of DEX gives us the confidence that we will eventually surpass centralized exchanges (CEX). In the last DeFi summer, it was widely believed that DEX would surpass CEX in due time. How many people still hold this belief today? If we study the development of DEX, the introduction of batch auctions is no coincidence. This is a well-thought-out step towards solving the liquidity problem and a phased result of the continuous technological iteration of DEX. DEX has evolved from just having a liquidity pool to a comprehensive liquidity system with different participant roles, specialized components, and permissionless composability. This progress was achieved through the efforts of predecessors. Relaxing time constraints and creating conditions that differentiate from centralized trading platforms have allowed us to see more possibilities. It even restored my confidence in DEX surpassing CEX.

A business cycle has passed, and although the DeFi giants remain unchanged on the outside, they have transformed on the inside. Batch auctions are an important milestone, as important as the invention of liquidity pools. I believe they can realize the dream of DEX surpassing CEX. When barter becomes the main trading mode again, we can regain control of our own market rhythm.

When discussing the future with many industry leaders, I found that there is a general confusion in the market. The markets lack of attention to technology has led to a general lack of confidence.

I still remember that in late 2018 and early 2019, when I was eating hot pot in Chengdu, I chatted with a friend about the bright future of DeFi and Ethereum. He talked enthusiastically about the future of DeFi and Ethereum. Although the price of ETH was less than $90 at the time, his eyes were shining with excitement.

Come to think of it, when did the development of an industry fall to the point where it needs to be defined by the wallets of speculators?

DEX is just a small part of the vast DeFi industry. If we look closely, we will find that DeFi and other fields are undergoing significant and exciting progress. As long as technology continues to advance and develop and never stops, what do we have to worry about? Dreams will definitely come true.

To all the industry builders who are forging ahead, I have only one sentence from an ancient Chinese poem to give to you: Dont worry about having no friends on the road ahead, for everyone in the world knows you.

This article is sourced from the internet: On-chain barter: getting back to the rhythm of crypto

ذات صلة: مستثمرو الإيثريوم يتمسكون بالعملة مع ارتفاع سعر الإيثريوم إلى ما يزيد عن $3,000

في ملخص تداول الإيثريوم عند $3,177 يقترب من مستوى تصحيح فيبوناتشي 23.6% المعروف بأنه دعم حاسم. أظهر حاملو الإيثريوم مرونة وتفاؤل، مع انخفاض الودائع النشطة إلى أدنى مستوى في ثمانية أشهر. انتقل معظم العرض إلى محافظ حاملي الأجل المتوسط، مع فقدان المستثمرين قصيري الأجل لهيمنتهم. تحاول الإيثريوم (ETH) حاليًا البقاء فوق الدعم الفني والنفسي الحاسم عند $3,000. من المرجح أن يكون هذا ممكنًا فقط عندما يختار حاملو الإيثريوم الابتعاد عن البيع والاحتفاظ، وهو ما يحدث. مستثمرو الإيثريوم ينتقلون إلى الاحتفاظ يحوم سعر تداول الإيثريوم عند $3,177 فوق أرضية الدعم $3,000، حيث يُظهر حاملو الإيثريوم الآن المزيد من التفاؤل أكثر من ذي قبل. تظهر علامات هذه المرونة في تحول العرض وتغير السلوك. فقد شهدت الودائع التي تم رصدها على السلسلة انخفاضًا...