My XP

0

Login

In 2023, Arthur Hayes and Akshat Vaidya, former head of corporate development at BitMEX, co-founded the investment firm Maelstrom Capital, with Vaidya as investment director. Maelstrom was set up as Hayes family office, with funds coming from Hayes. Because it does not need to deal with LPs (after all, it is all Hayes money), it is not in a hurry to allocate capital to earn management fees, so it has enough patience. This also allows the market to see the different investment styles of family offices and VC institutions.

Hayes said: We want to find projects that are truly high-quality. This is not a game of spray and pray (referring to investing in a wide range of projects and then praying that a project will succeed) because we have no external LPs (after all, it is our own money, so we have to be cautious). At this moment when the market is maturing but there is still no clear way forward, BlockBeats had the honor of interviewing Akshat Vaidya, co-founder of Maelstrom, to discuss with him the development of family offices in the crypto field and their understanding of the market.

During the interview, BlockBeats asked Maelstrom whether he would participate in the current hot market trend and buy meme coins. Akshat replied that they do not directly participate in meme coin transactions, but indirectly obtain the value brought by the meme coin phenomenon by investing in the infrastructure that supports the creation and dissemination of meme coins.

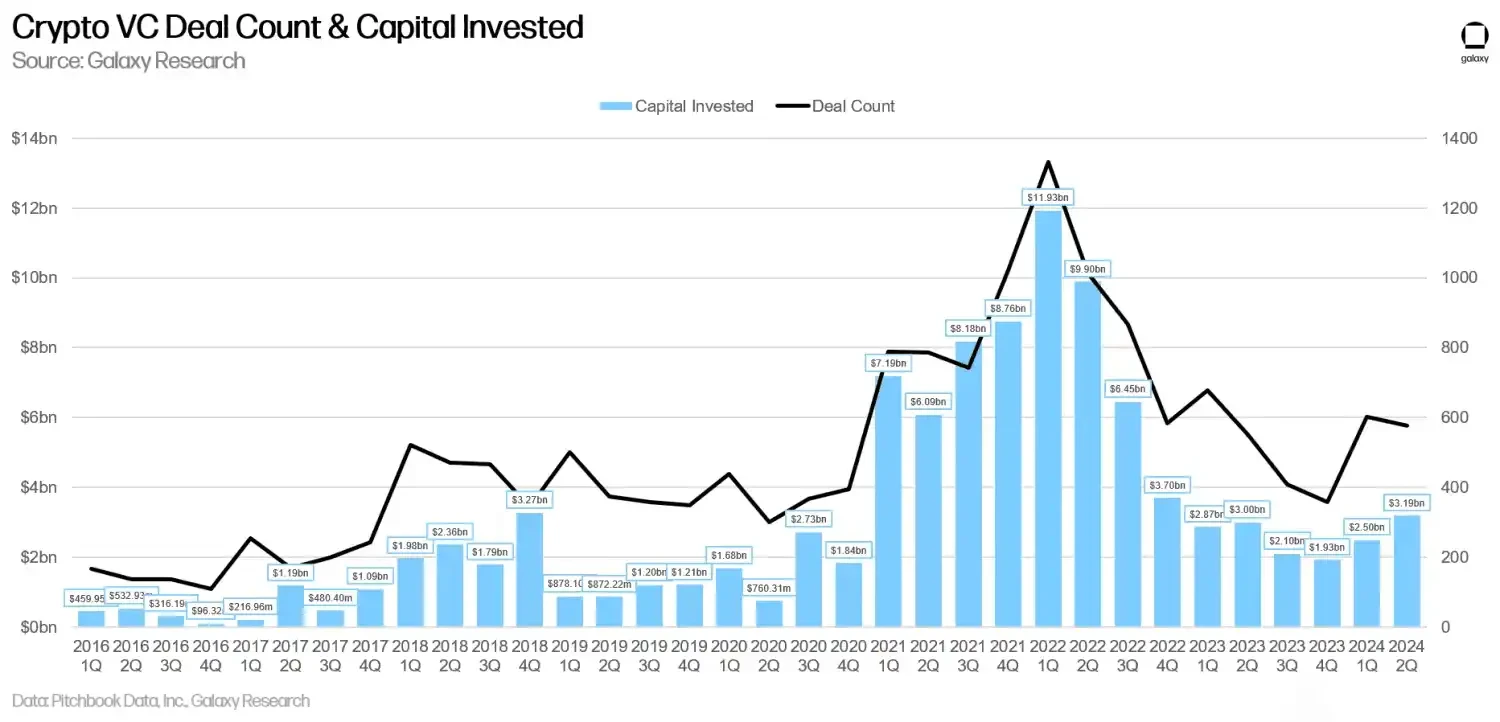

Unlike most people who believe that crypto infrastructure is already too saturated, Maelstroms main investment portfolio is still aimed at infrastructure companies. Hayes and Akshat both believe that infrastructure makes sense during this period of the cycle. Everyone is looking forward to user scale, but the market does not have enough infrastructure to support such a large user scale.

The following is the original interview:

BlockBeats: How did you and Arthur Hayes meet?

Akshat: I started buying Bitcoin in 2013, when Arthur was starting BitMEX. By 2019, BitMEX had become the worlds largest cryptocurrency exchange by annual volume (in nominal dollars), and I decided to leave the traditional financial industry and focus on the Crypto field. At the time, I was living in Chicago and working for a mid-sized private equity firm.

Maelstorm event site, with Akshat in the middle; Image source: X

I remember I stumbled across a job posting for a BitMEX Ventures Investment Assistant and the requirement for applying for the position was Hong Kong applicants only. Despite this, I submitted my application and eventually made it through the interview, which is how I first met Arthur. After joining BitMEX, I initially worked under Arthur for a few levels, and later gradually rose through the ranks to become the companys head of corporate development and mergers and acquisitions.

BlockBeats: Why did you choose to leave BitMEX and start this family fund with Arthur Hayes?

Akshat: In the summer of 2022, I discussed the future direction of BitMEX Ventures with Arthur and proposed to him a concept called Centennial Portfolio. I envisioned creating an investment fund that would leverage Arthurs unique advantage as one of the worlds youngest billionaires – time, to invest in future technologies and scarce assets, including Water Rights and cryptocurrencies. He was interested in the idea, but suggested that we start on a smaller scale and focus on what we do best – cryptocurrencies.

BlockBeats: How much money does Maelstrom manage now? What is the main responsibility of the investment director?

Akshat: We do not publicly disclose our AUM, but it is not difficult to estimate a rough figure based on our public portfolio. I am responsible for proposing investment strategies, executing trades, and managing Maelstroms venture portfolio. In 2022, the team was just me and Arthur. Now, I lead a full-time team of 6 traders, investors, and researchers, and expect to expand the team further in the next bear market.

BlockBeats: What is the difference between the operation of family funds in the Crypto field and VC?

Akshat: As one of the most influential builders in the Crypto space, Maelstrom is able to provide its portfolio companies with hands-on operational support that other investors struggle to provide. Many funds excel in investment decisions, but few are led by people who have successfully built profitable unicorns in the Crypto space.

In contrast, VCs usually have an obligation to deploy capital, so they are more likely to lower their investment standards to ensure that funds can be put into the market. This is also why they usually perform worse than family offices.

In addition, venture capital funds charge their LPs a 2% management fee, so they have an incentive to continuously raise larger funds to maximize management fee income. Family offices do not have this incentive mechanism, so they can focus more on finding high-quality investment opportunities, conducting in-depth due diligence, negotiating better investment terms, and providing substantial help to portfolio companies.

BlockBeats: How much influence does Arthur Hayes and his ideas have on your investment decisions?

Akshat: Our investment team operates independently, and Arthur is the final investment decision maker, approving or rejecting each investment. His macro theory is one of the important references for us to formulate investment strategies. Arthur is more involved in portfolio management. Once we invest in a company, Arthur will become a supporter of the company, and his influence runs through almost the entire portfolio.

BlockBeats: Judging from Maelstrom’s investment portfolio, your investment in the DeFi field is particularly prominent. What is the logic behind this?

Akshat: CeFi has always been seen as a bridge from traditional finance to DeFi. In the long run, we believe that capital formation and value capture will gradually shift to a decentralized system without permission. However, in the short term, the combination of CeFi and DeFi can play to the strengths of both parties. For example, Ethena is a typical case.

BlockBeats: Ethena is a project that Arthur is particularly optimistic about, but it has recently been questioned by the community because the price of the currency has not performed as expected. What do you think is the biggest problem Ethena is facing now? What can or should the team and community do to turn the situation around?

Akshat: All value investors understand that less than 6 months is not enough time to evaluate any serious investment, whether in the cryptocurrency field or other fields. Although this does not constitute investment advice, you still need to do your own research, but in general, profitable protocol investments like Ethena that focus on practical applications are more like long-term layouts in the venture capital stage rather than quick-rich plans.

According to both on-chain and off-chain data, Ethena has been very successful in finding initial product-market fit and has become one of the fastest growing decentralized financial products in history. Since its launch at the beginning of this year, its user base, TVL, and partners have continued to grow, and the product mechanism has also worked as expected in different scenarios (such as the market correction this summer).

The team is focused on creating long-term value. Recently, Ethena announced a partnership with traditional financial giant BlackRock to launch a new UStb product to be used in conjunction with the existing USDe. Ethena will become the only issuer 100% backed by BlackRocks BUIDL, and will expand collateral options through this stablecoin, allowing CEX partners to choose to list USDe, UStb, or both at the same time, which will help promote the realization of long-term value.

BlockBeats: Arthur often promotes some meme coins on X. At the same time, more and more meme trading tools have made meme trading gradually become the main active crypto market in the Chinese community. What do you think is the main development trend of meme coins? Will Maelstrom consider investing in meme projects?

Akshat: We view meme coins as a cultural phenomenon and will never underestimate anything that can bring attention, engineers and resources to the Crypto field. However, Maelstrom, as a venture capital fund focused on building infrastructure for a permissionless future, does not directly participate in meme coin transactions. Instead, we indirectly obtain the value brought by the meme coin phenomenon by investing in the infrastructure that supports the creation and dissemination of meme coins. Arthur is personally keen on meme coin transactions. If you want to know his views on specific meme coins, you can follow his X account.

BlockBeats: The market now has a strong resistance to the concept of VC coin. In Maelstroms opinion, what is the problem with VC coin?

Akshat: The incentives for VC funds drive them to keep raising more funds because they earn money in two ways: 2% management fees and 20% performance share. Most VC funds perform worse than even simple passive investment strategies, so the 2% management fee has become one of the most secure sources of income for VC fund managers. This makes their main goal to raise as large a fund as possible, even if there are no suitable capital deployment opportunities.

In the Crypto field, VC funds usually repeat similar operating modes:

1) Raise VC funds by relying on the successful experience of founders, industry leaders or investors in small-scale investments;

2) Investing in early-stage projects, even when quality investment opportunities are limited;

3) Pushing up valuations in each round of financing and promoting the listing of tokens on highly valued CEXs;

4) Raise a new round of funds as soon as possible, using the unrealized track record to raise funds. Although the fund has performed well on paper, this is mainly due to CEXs like Binance listing key projects at 30x to 50x valuations, and these tokens are not yet fully liquid. Once circulated, the token price tends to fall by 50%-75% or even more.

Ultimately, it is the retail investors and the limited partners of the VC funds who bear the losses. This is one of the reasons why I prefer the family office model, because the incentive mechanism of the family office is completely aligned with the interests of the shareholders (Arthur in Maelstroms case).

BlockBeats: Recently, more and more people in the industry have begun to discuss fundamentals such as profitability and sustainable operation of projects. Do you agree with this new development idea of the industry? In your opinion, has the crypto industry developed to the stage where it must explore a profit model? Will Maelstroms investment strategy and thinking change as a result?

Akshat: Investing in early-stage crypto projects is essentially no different from investing in early-stage startups, whether it is your uncles laundry, your friends consumer application, or a VC-backed technology service company. Before deciding whether to invest in a project, you must conduct a comprehensive due diligence and evaluate the companys founding team, products, roadmap, business model/revenue model, legal strategy, operating conditions, competitive landscape, token value accumulation mechanism, and token economics.

BlockBeats: The Federal Reserve has recently started a rate cut cycle. Do you think this is a key catalyst for a new round of crypto bull market? What impact will the recent situation in the Middle East have on the crypto industry?

Akshat: I personally believe that in the coming months we may face two risks that could lead to higher inflation in the short to medium term:

1. Regulators return to loose monetary policy;

2. Supply-side disruptions could occur (e.g., a Middle East war intensifies and affects the oil supply chain, and a strike by U.S. port workers).

If U.S. economic growth remains strong, regulators have easy tools to combat rising inflation. However, if the U.S. economy slows, the Fed may be caught in a dilemma between tightening policy to control inflation or easing policy to stimulate economic growth. In this scenario, more speculative crypto assets (such as meme coins and early projects) may underperform digital gold (such as Bitcoin) and mature crypto products with actual protocol revenue and cash flow.

BlockBeats: Many people believe that cryptocurrencies are not ready for a new bull run in terms of industry innovation and fundamentals. Do you agree with this view? What do you think are the main drivers of the new cycle?

Akshat: The growth process of the crypto industry is similar to the human genome, a child, or a developing country, which gradually matures through phased rapid growth. I started investing in cryptocurrencies in 2013 and have experienced multiple cycles:

The 2013/2014 cycle was the stage when Bitcoin found initial market fit as a store of value (before that, Bitcoin was still proving to its core users that its decentralized P2P trading system was feasible);

The 2017/2018 cycle focused on exploring the potential of smart contracts after the initial success of Ethereum and other smart contract networks;

The 2021/2022 cycle is about smart contracts (especially Ethereum) finally finding their first real use case (DeFi);

The 2023/2024 cycle focuses on scaling DeFi infrastructure (L1, L2, money markets, etc.) far beyond the initial test cases.

I believe the next cycle will be driven by the following factors:

1. The combination of traditional finance (TradFi) and encryption technology;

2. Governments are beginning to view encryption as a strategic priority;

3. Development of the Decentralized IoT Infrastructure Network (DePIN).

There are many preliminary experiments underway in the DePIN field, and success is only a matter of time, which will attract more users, investors, engineers, and new application scenarios to the Crypto field. As DePIN matures, encryption technology will be integrated into peoples lives in a wider range of fields in ways beyond our imagination.

In addition, there are many long-term catalysts, which are briefly listed below:

The entry of traditional financial giants and the gradual recognition of cryptocurrencies in global investment portfolios;

The world’s wealthiest and most financially and crypto-literate generation (Gen Z and young people) is gradually entering the workplace;

The first millennials to become interested in cryptocurrencies are beginning to inherit the wealth of previous generations;

Long-term risks in the existing monetary system continue to accumulate and gradually intensify.

This article is sourced from the internet: Exclusive Interview with Maelstrom: What is Arthur Hayes’ Family Office Fund buying?

Original author: M6 Labs Original translation: TechFlow The story of Telegram is a modern saga of defiance, innovation, and, ultimately, a bit of hubris. Founded by the vision of Pavel Durov, Telegram became a bastion of free expression and privacy. In an era of increasing government surveillance, the Durov brothers built an encrypted communications platform that is relentlessly censorship-resistant and serves millions of users around the world. Telegram’s unwavering commitment to privacy quickly attracted users who were disillusioned with mainstream platforms and wary of government interference. Yet, almost in a Shakespearean tragedy, Telegram’s unwavering stance on privacy ultimately led to its demise. The platform’s refusal to comply with data requests and its association with controversial campaigns have put it at the center of a global debate over freedom, security, and…