My XP

0

Login

Original|Odaily Planet Daily ( @OdailyChina )

Author: Wenser ( @wenser2010 )

In December 2017, when the market value of the cryptocurrency industry reached $500 billion, Ethereum co-founder Vitalik raised a series of industry questions , including banking services, censorship-resistant commercial transactions, practical use case Dapps, real interest rates, anti-inflation, and payment channels. In the end, he believed that in terms of the development of the industry, although there has been some progress in these areas, compared with the market value data, it is far less than expected.

Today, the market value of cryptocurrency has fallen back to around US$2.4 trillion after breaking through US$3 trillion in November 2021. Mass Adoption is still a long way off. VC coins have been criticized as blood-sucking machines with high FDV and low circulation in their ups and downs. Different tracks such as L1, DeFi, GameFi, NFT, SocialFi, DAO, Infra, L2, etc. have appeared and then fallen silent one after another. Meme coins have returned to the center of the encryption stage since 2013 and will continue to shine in 2024 after the Bitcoin spot ETF and Ethereum spot ETF have been approved.

Looking back, the cryptocurrency industry took root from Bitcoin and gradually grew into a towering tree with many branches. In front of this towering tree, there may be the next cold winter, or the next warm spring. On this still small but fertile decentralized land, there is always new light of ideals and miracles of wealth waiting for us.

In this series of articles, Odaily Planet Daily will briefly review and analyze the past venture capital cycles of the crypto industry. Although it is inevitable that some parts will be missed, it can also serve as a supplementary perspective for readers reference.

(Note: This article is the first part, covering the “three summers” before 2022: Ethereum, exchanges, public chain fever, DeFi/GameFi/NFT. The second part will tell the story of the most recent cycle and try to abstractly summarize the trend changes and the methodology behind multiple rounds of venture capital cycles.)

After the Bitcoin pioneering period from 2013 to 2015, Bitcoin has gradually become the stage for mining machine manufacturers and leading exchanges. The ups and downs of the market call for another diffusion of innovation.

When it comes to the venture capital cycle from 2016 to 2018, Ethereum is an unavoidable topic of discussion. It is precisely because of its emergence and subsequent success that it has established another industry monument for the cryptocurrency industry in addition to Bitcoin, and thus opened the industrys first wave of craze – IC0 (initial coin offering), which has enabled countless projects to obtain initial start-up funds of varying sizes, and the cryptocurrency industry has quickly entered a chaotic development period with a mix of good and bad. Idealists live in the same room with liars, robbers, and thieves, and sentimentalists and profit-seekers are drinking and chatting with each other. This is always the case in the wild period of the industry, with lies and truth intertwined, and innovation and scams are only one step away.

On July 22, 2014, Ethereum ICO was launched. The fundraising price that year was 1 BTC for 2,000 ETH. No permission was required, no VC, and no lock-up. In the end, this ICO raised more than $18 million in the form of Bitcoin, and the price of a single ETH was about $0.3.

It is worth mentioning that Ethereum co-founder Vitalik was only 20 years old at the time. The idea of Ethereum originated from a white paper he sent to his friends at the end of 2013, in which he mentioned I suggest designing a new Bitcoin. This new Bitcoin will be based on a general programming language and can be used to create a variety of applications, such as social, trading, games, etc., and these things have been fulfilled one by one today, which once again proves his amazing insight into the development trend of the cryptocurrency industry.

Photos of Vitalik playing with IBM computers when he was a child

In addition, one of the important reasons why Vitalik joined the cryptocurrency industry is said to be because the Life Siphon skill of the Warlock, a character in the World of Warcraft game that he loved as a child, was deleted by the game developer Blizzard. Since then, the world has lost a die-hard player of World of Warcraft, but gained a believer in decentralization.

In December of the same year, Xiao Feng, CEO of Wanxiang Blockchain Lab and partner of Distributed Capital, accidentally learned about Vitalik and gave a special introduction to Ethereum in a speech, which also laid the groundwork for the Shanghai Upgrade of Ethereum. It is mentioned in the article: Ethereums mainnet was launched in July 2015. Before the mainnet was launched, the tokens held by the foundation and other official organizations were locked. There was about 18 million US dollars in the account. After spending a certain amount, there was still money in the account. I remember that there should be 3 million US dollars in the account at that time. After all, the mainnet was not launched yet, and everyone would ask if the money was enough. In fact, there was no performance crisis at that time. Then some people would still ask, can your money support the launch of the mainnet? If not, what should we do? It happened that Vitalik was also in Shanghai at that time and came to our office. Then I heard that he was in a meeting last night, and voices from all sides were asking him how to explain it, but he did not answer on the spot.

When I heard about this, it was not actually for investment, but for such a great cause, to help this young man. We all really just wanted to help him.

Our idea at the time was very simple. First, we could give $500,000 in cash. Secondly, we also made it clear to the community that we could continue to support after giving out $500,000. Later, after we signed such a donation agreement with the Ethereum Foundation and gave the money to the other party, the Ethereum Foundation promised to give us the tokens at the price at the time of our donation when their tokens could be unlocked after the mainnet was launched. Our idea at the time was to support them. In case the mainnet could not be launched, it didn’t matter. We supported such a great idea and did not think about it from an investment perspective. Despite this, Vitalik said in a later interview: The $500,000 from Wanxiang at the time became the lifeline of Ethereum.

Perhaps, as the saying goes, greatness cannot be planned, the development of Ethereum was supported by Xiao Feng and Wanxiang Group, which was simply due to the latters idea of wanting to help young people like Vitalik realize a great idea. It sounds easy, but the crypto industry at that time did need a new benchmark to rebuild industry confidence after experiencing the baptism of the 2013 bear market, and Ethereum came at the right time.

On July 30, 2015, the first phase version of Ethereum, Frontier, was released, the first Ethereum block was mined, and the Ethereum blockchain network, adhering to the vision of world computer, officially began its operation.

Although Ethereum’s market value evaporated by as much as $500 million in June of the following year due to a hacker attack on The DAO (the world’s first DAO organization, which lost $60 million worth of Ethereum due to an attack after completing a $150 million crowdfunding campaign), with the support of leaders like Vitalik, early founding members of Ethereum including Gavin Wood, and the Ethereum global community including Chinese cryptocurrency mining and capital institutions, it successfully completed the hard fork upgrade and smoothly passed the crisis.

On May 19, 2017, the price of Ethereum broke through the $100 mark for the first time, which also meant that the return on investment of early Ethereum investors reached an astonishing 300 times (although this date would later become one of the dark moments of the crypto industry).

In addition to once again proving the correctness of investing in Ethereum, it also laid the foundation for the ICO craze in the crypto industry to be detonated again.

In June 2017, Binance launched the IC0 of its platform coin BNB. As of July 2, the IC0 ended and a total of $15 million worth of digital assets were raised. On September 1, Binance announced that it had received $15 million in financing from Black Hole Capital and PanCity Capital.

In August 2017, Binance launched its first ICO, and 500 million TRX coins were sold out in 53 seconds at a price of about $0.01. They were subsequently launched on platforms such as RenRenICO and ICO 365. According to people familiar with the matter, TRX raised about 7,000 bitcoins in this round of ICO, which was worth about $200 million at the time.

In September 2017, Cardano (ADA, said to be named after Ada Lovelace, the daughter of Lord Byron, a famous British poet and mathematician who is known as the first programmer in human history) raised more than US$62 million at a price of US$0.0024 per token after more than two years of IC0, and officially completed TGE at a price of US$0.02 in October.

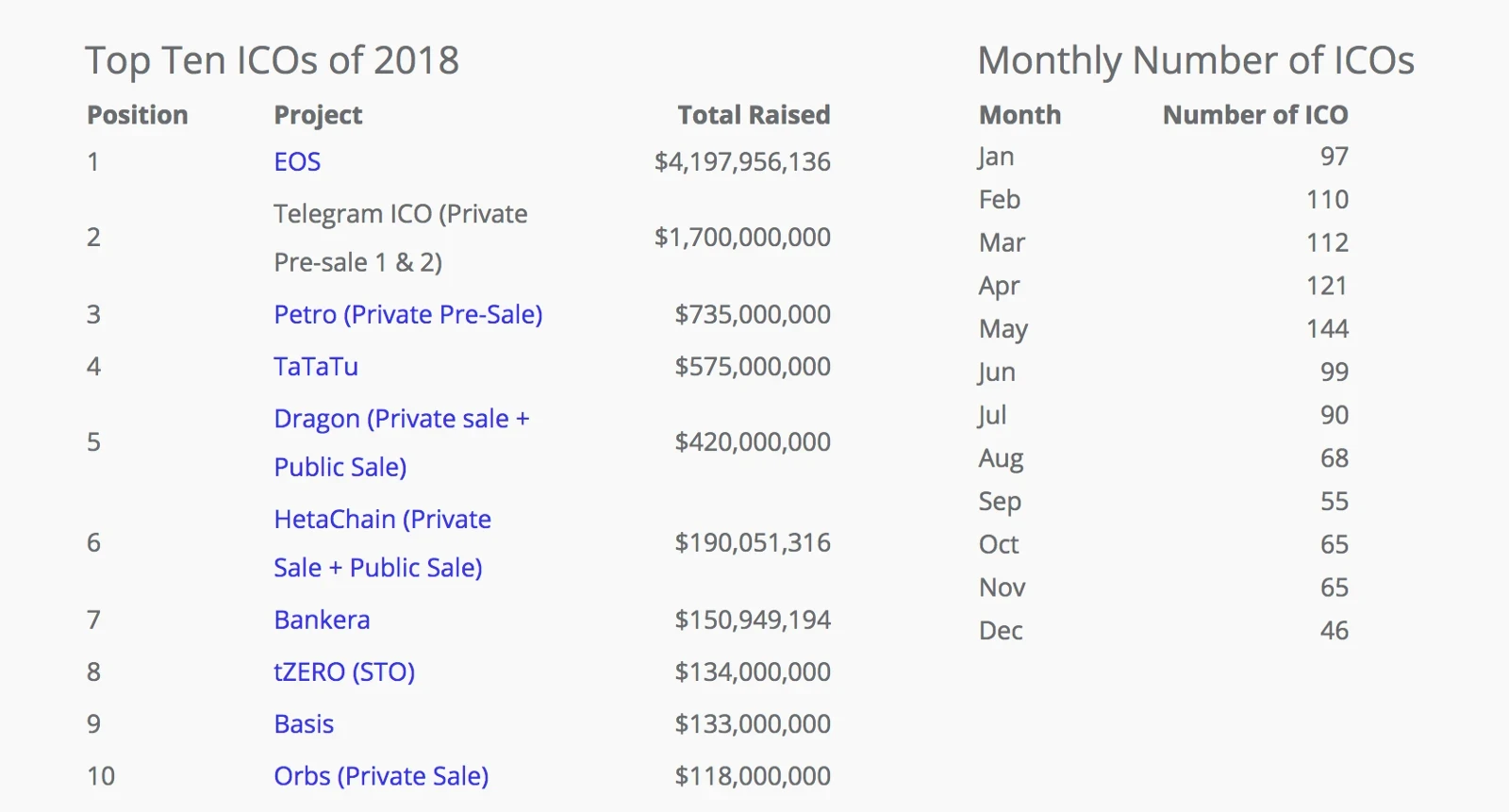

Top 10 ICO Projects in 2017

Along with the increasingly frenzied ICO activities, there are endless fake projects such as white paper first and air coin speculation, which has become the fuse for regulatory intervention.

On September 4, 2017, the People’s Bank of China and seven other departments jointly issued the “Announcement on Preventing Risks of Token Issuance and Financing”, declaring IC0 an illegal activity, known as the “94 Incident”. While facing regulatory pressure from countries around the world, the cryptocurrency industry is still continuing its development, especially Binance, which quickly completed the transfer from Shanghai to Japan and began to gradually withdraw users from related regions, laying a solid foundation for becoming the “world’s largest cryptocurrency exchange”.

However, judging from the fundraising methods of the crypto industry at that time, the value coins that are now sought after by major VCs and other investment institutions can be regarded as Meme coins to some extent at that time because of their more decentralized fundraising methods, lower issue prices, and token names and token symbols with Meme attributes.

In addition, according to the 2017 China Internet Finance Investment and Financing Analysis Report, based on the equity financing that can be observed and monitored, the number of equity investment and financing cases in the blockchain field increased from 4 in 2016 to 29 in 2017, an increase of 625%. In terms of overall market value, according to Coinmarketcap data, the global digital currency market value exceeded US$600 billion per day at the end of December 2017, with a total of 1,334 digital currencies.

On January 17, 2018, Binance’s registered users exceeded 6 million; more than 97% of them were foreign users, covering more than 180 countries around the world. Soon, Binance’s trading volume exceeded Huobi and OKcoin (OKX’s predecessor Ouyi), becoming the world’s largest digital currency trading platform. Since then, Binance, OKcoin, and Huobi have become a three-legged tripod, and the investment landscape created by the exchange’s venture capital department is about to begin, and will receive more and more attention as the exchange’s voice continues to increase.

It is worth noting that the ICO chaos also triggered regulatory attention around the world at that time. In early 2018, Gibraltar announced that it would launch the worlds first ICO regulatory law, which also attracted close attention from regulators in the UK and Singapore; the Swiss Financial Market Supervisory Authoritys new regulatory rules set three categories of ICO digital tokens, and asset-based digital tokens are regarded as securities; Russian government departments proposed that the nominal capital of ICO project initiators must be at least 100 million rubles; at the same time, the United States has adopted the use of existing securities regulations to regulate ICO events.

This is obviously necessary. According to a research report by Bloomberg in July 2018, about 78% of IC0 projects were identified as scams before trading; as of July 2018, funds raised by popular high-quality projects accounted for 70% of IC0 funds (in US dollars). The subsequent emergence of IE 0, ID 0, and even various fund-raising and asset issuance methods are, to some extent, variants or updated iterations of IC0.

In 2018, thanks to the founder BMs halo of origin and the traffic and funds of Chinese investors brought by early Bitcoin evangelists such as Li Xiaolai, the EOS project raised $185 million in the first five days of IC0. After launching the 21 Super Node Campaign voted by EOS holders, various representative figures and the capital behind them, including Xue Manzi, Baozou Gongqinwang, Lao Mao, Yi Lihua, Ant Mining Pool, etc., announced their entry into the EOS node election, bringing EOS super high market attention and capital liquidity. Finally, on June 2 of that year, EOSs one-year IC0 successfully ended with an impressive record of raising $4.2 billion.

Top 10 ICO Projects in 2018

As Xu Chaoyi, managing partner of BKFund and director of strategic management department of Distributed Capital, mentioned in an exclusive interview with 36Kr in 2018: In 2018, among the projects that BKFund focused on in the primary market of blockchain, the first tier was industry public chains; the second tier was industry vertical public chains; and specific vertical applications could only be ranked in the third tier, which was more inclined to migrate traditional Internet applications to blockchain network systems. In addition, he was also frank about the logic behind this investment preference: In fact, in the blockchain industry, the highest valuation is the underlying protocol layer or public chain, and the valuation of the upper platform layer will be lower, including the business layer above the vertical industry, the imagination and valuation will be much lower.

On the one hand, this is because the crypto industry is still in its early stages and there is a large gap in infrastructure construction. On the other hand, to a large extent, due to the example of Ethereum, countless individuals and capital institutions have entered the market, wanting to emulate Xiao Feng and Wanxiang, who once received super high returns due to their strong support for Ethereum. Investing in the next Ethereum was the obsession of countless people at that time, which was also one of the reasons why projects such as Cosmos and Polkadot were so popular later.

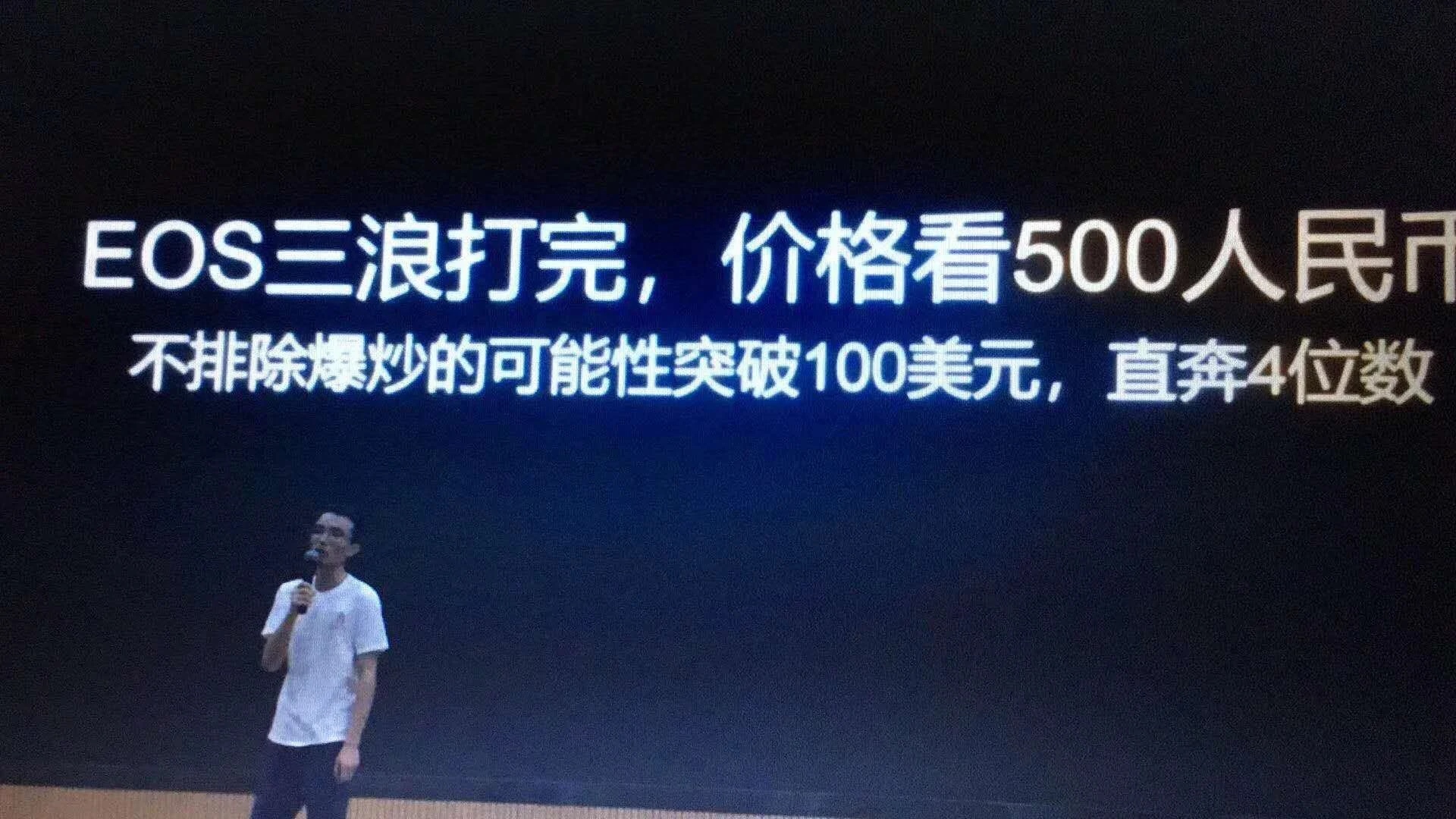

But it is obvious that after the third wave, EOS is expected to break through 1,000 US dollars is destined to be just a fantasy during the market bubble period, and the price of fantasy is heavy, even tragic, just as the story that EOSs price trend later told people: The market is not subject to personal will.

EOS Three Waves Classic Speech

After experiencing a new high in market value of over $850 billion at the beginning of the year, the crypto industry once again ushered in a new round of cleaning – Bitcoin fell from more than $18,000 at the beginning of the year to around $3,200 at the end of the year, a year-on-year decline of about 82%; Ethereum fell below $100 from its high of nearly $1,500 at the beginning of the year, with the lowest price reaching around $83. The bull-bear cycle transition and the market position test are happening all the time in the crypto industry.

Although, judging from the investment and financing data in the first half of the year, the arrival of the crypto winter is not as urgent as imagined, and it is even slightly hot – according to Securities Daily, in the first half of 2018, the enthusiasm for investment and financing in the blockchain field has risen, with a total of 222 financings. Among them, the number of investment and financings received by the United States and China is 179, accounting for 80.6% of the global total. Although China has received 141 financings in the blockchain field, far exceeding the 38 in the United States, the financing amounts are not much different, at 6.4 billion yuan and 6.7 billion yuan respectively. From the perspective of the financing stage, there were 107 seed/angel round financings in the blockchain field, accounting for 48.2% of all rounds, and the total financing amount was 1.6 billion yuan, accounting for only 10% of all rounds; from the perspective of the country where the financing projects are located, my country’s seed/angel, Pre-A, and A round financing events were 73, 9, and 16 respectively, while the United States had 18, 0, and 6 events respectively.

As 2019 began, investment and financing in the crypto industry became more rational. Specifically , the scale of financing funds fell by nearly 40% compared to 2018, with a total of 653 financing events and a total financing amount of nearly US$4.7 billion (approximately RMB 32.9 billion). In addition, there were 35 public mergers and acquisitions in 2019, with a total merger and acquisition amount of more than US$3 billion.

In general, the crypto industry in 2019 is more like a transitional period of connecting the past and the future. Although investment and financing are relatively active, they are mainly concentrated in the field of digital assets represented by exchanges and financial applications: In February, the exchange Kraken received an investment of US$100 million; in October, A.TOP Asia Exchange received an investment of 50,000 bitcoins from potato, and this amount of financing even ranked TOP 1 among the disclosed projects (Note: The financing news was questioned by the market); Indian payment giant PhonePe received an investment of US$101 million and 4.05 billion rupees in July and October respectively. In addition, Rapyd and Ripple, two payment companies, also received investments of US$100 million and US$200 million in the second half of the year, respectively. Overall, exchanges accounted for 20% of the total financing events with 129 financings, becoming the category with the highest financing frequency that year; the total amount of financing was about US$2.22 billion, accounting for about 40% of the total financing amount that year.

In addition, from the perspective of investment institutions , 2019 is also a year of transformation – overseas investment institutions are gradually competing with Chinese investment institutions. The US investment institution Digital Currency Group has become the worlds most active investment institution with 14 investments. Even the US cryptocurrency exchange Coinbase, founded in 2012, and its subsidiary Coinbase Ventures, founded in 2018, are at the top of the list of institutions with 6 investments respectively, which also lays the groundwork for the start of the next wave of DeFi.

2019 Institutional Investment Data Ranking

Starting from 2020, the wave of the times belonging to cryptocurrency will continue to rise and fall in different tracks, attracting the attention of the whole world.

After the emergence of Ethereum, a major question that people have long been asking is: What can Ethereum do? As the consensus value of Bitcoin continues to rise with its spread, people have put forward higher and more requirements for the practicality of the Cryptocurrency 2.0 system including Ethereum.

Although the crash in March 2020 poured cold water on the market, DeFi Summer has quietly arrived with the high activity of Compound and Aave (formerly ETHLend) in the money market business, and the successive issuance of coins by platforms such as Curve, SushiSwap, Uniswap, and 1inch in the exchange business.

The concept of Liquidity Mining first proposed by Synthetix (SNX) in July 2019 was truly realized through the issuance of the governance token COMP by Compound Protocol; Yearn Finances governance token YFI became the first crypto asset in history whose price exceeded that of Bitcoin, making yield farming gradually popular. The concept of staking has thus officially entered the stage of history and has gradually become a major paradigm in the industry.

Users can be rewarded with the protocols native tokens by providing liquidity for the DeFi protocol, which has directly triggered a new round of cryptocurrency issuance boom – many projects need to consider attracting users and increasing liquidity through tokens, and issuing tokens has become one of the most effective means of competition in the market.

After all, the pursuit of wealth is the unforgettable original intention of every player in the crypto industry.

According to industry data , global crypto investment and financing continued to maintain rapid growth in 2020, with 434 investment and financing events throughout the year, and many projects completing multiple rounds of financing during the year; the total amount of investment and financing disclosed throughout the year reached US$3.566 billion (excluding acquisitions).

According to Arcane Research, the locked-in scale of DeFi increased by about 2100% throughout the year, and the number of independent addresses increased tenfold throughout the year. However, perhaps due to sufficient market liquidity support, or perhaps the arrival of DeFi Summer has intensified the competition in this field. The total investment and financing of DeFi projects that have experienced breakthrough growth is about US$278 million, accounting for only 7.80% of the total investment and financing amount of the crypto industry. The average single financing under this project is only US$4.8 million, which is the weakest financing track among all sub-tracks. The US$50 million financing announced by the cryptocurrency lending company BlockFi in August of that year was the highest single financing amount in DeFi throughout the year.

But looking back from the perspective of DeFi Summer one year later , the TVL has increased by 58 times, the number of users has increased by nearly 140 times, the total amount of loans has increased by more than 3474.1%, and the DEX transaction volume has increased by 382.5 times. The impact of DeFi on the entire crypto industry is comprehensive and far-reaching. In addition, Polkadot also raised about 43 million US dollars through IC0 that year, becoming another star public chain.

As we enter 2021, events that have a significant impact on the industry can be divided into three categories:

First, in the traditional financial market, Coinbase was successfully listed on the U.S. stock market with the stock code COIN, and is determined to carry out compliance to the end; Roblox was listed on the Nasdaq in the U.S. stock market, bringing the concept of metaverse into the spotlight, and Facebook directly changed its name to Meta.

Second, in the cryptocurrency industry, the FTX system (including FTX Exchange, crypto quantitative trading institution Alameda Research, and a series of investment projects including Solana) has gradually emerged and become a new force in cryptocurrency exchanges. FTX Exchange once jumped to the position of the second largest exchange in the industry, but at the same time it also laid the seeds for the 2022 crash.

Third, in terms of specific track projects, there is the gold-making frenzy brought by GameFi Summer led by Axie Infinity and the game union YGG, and NFT Summer led by blue-chip NFTs such as BAYC and CryptoPunks and NFT trading platform Opensea (which lasted until May 2022 and ended with the sale of Gas by Otherside, which burned 10,000 ETH).

In addition, Web3 has entered peoples vision in a more understandable and inclusive manner, and has gradually gained popularity with the vigorous promotion of Ethereum co-founder, Polkadot founder Gavin Wood, and a16z investor Chris Dxion, becoming the latest synonym for the cryptocurrency industry.

Moreover, Solana, which was founded in 2017 by former Qualcomm, Intel and Dropbox engineers and uses the Proof of History (PoH) mechanism as a tool to improve network efficiency, has also shined this year. After obtaining US$25 million in funds in previous private placements and IC0s, it received US$40 million in funds provided by OKX and MEXC in March respectively; in June, it received US$314 million in funds led by a16z and Polychain Capital , and participated in by institutions and individuals including 1kx , Alameda Research , Blockchange Ventures , CMS Holdings , Coinfund , CoinShares , Collab Currency , MGNR ( Memetic Capital ), Multicoin Capital , ParaFi Capital , Sino Global Capital , Jump Trading , Boys Noize , etc. Because it claims to far exceed the TPS operating efficiency of Ethereum, it is expected to be the next Ethereum killer.

As an investor deeply involved in Solana, Multicoin Capital has also reaped thousands of times of investment returns. However, soon, after entering 2022, the market will tell everyone a truth – What makes you successful will also become your lesson. The intuitive result of path dependence is profit and loss come from the same source.

Sky Mavis, the parent company behind Axie Infinity, a popular NFT game that has driven the gold rush in Southeast Asia, completed a $7.5 million round of financing in May of that year, led by Libertus Capital, with participation from Blocktower Capital, Konvoy Ventures, Derek Schloss of Collab Currency, Stephen McKeon, and Dallas Mavericks owner Mark Cuban. The next round of financing will not be until April 2022, a year later, but by then the amount of financing will have increased significantly to $150 million. Axie Infinity, founded in 2017, had previously achieved the milestone of AXS token listed on Binance in early November 2020 with the title of the most active game in blockchain. At that time, its monthly active users were only about 7,000. A few months later, it has become the synonym for the GameFi industry and successfully created the so-called Play-To-Earn (P2E for short, that is, earning while playing) model, laying the foundation for the subsequent emergence of STEPN.

As for BAYC at that time, although it performed well due to the pursuit of sports and entertainment stars including Curry and Dog, and the floor price once exceeded 55 ETH, as the protagonist of NFT Summer, it had not yet obtained financing.

This year, the absolute protagonist in the NFT field is Opensea. After completing a $2 million seed round of financing in 2018 and a $2.1 million strategic round of financing in 2019,

In March 2021, OpenSea completed a $23 million Series A financing led by a16z, with participation from Cultural Leadership Fund and many angel investors including Ron Conway, Mark Cuban, Tim Ferriss, Belinda Johnson, Naval Ravikant, Ben Silberman, etc. In July, it completed another $100 million Series B financing led by a16z, with a post-investment valuation of $1.5 billion. And this is still several months away from the peak of the NFT bubble period, and Opensea will continue to perform.

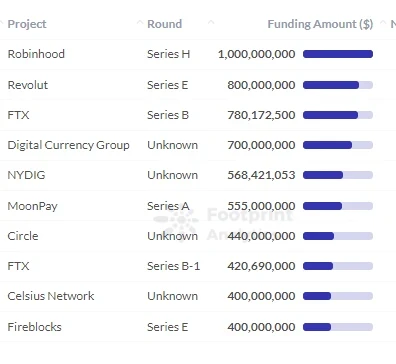

According to Footprint Analytics , there were 1,045 financings in 2021, with a total financing amount of US$30.27 billion, a growth rate of nearly 790% compared to 2020. In terms of the financing scale of specific projects, stock brokerage company Robinhood, exchange FTX and application service platform Revolut ranked the top three in the CeFi field; decentralized autonomous organization BitDAO, asset trading platform FalconX and decentralized aggregation exchange 1inch ranked the top three in the DeFi field.

It is worth mentioning that the DAO organization received great attention at this time. Seed Club, Bankless DAO, FWB and others were once regarded as benchmark organizations of the DAO organization, but they were eventually falsified by the market to a certain extent.

CeFi funding rankings

In November 2021, the market value of the cryptocurrency industry finally broke through 3 trillion amidst the rapid growth. After experiencing the baptism of May 19 that year, another bull market has arrived, and another wave of new narratives is ready to go, and the stories of more venture capital cycles are still continuing.

Cryptocurrency industry market value exceeds 3 trillion

Looking back at the crypto venture capital cycle from 2016 to 2021, every stage, every bull and bear market, and every cycle has its own main theme and version of the answer. There are endless projects and roles that have come to the fore. Some people have retired successfully, some have disappeared without a trace, some are still active today, and some are still looking for their own wealth code.

In the next article from 2022 to 2024, which is the closest to this cycle, we will continue to track the people, events, and things in the wave of the crypto industry venture capital cycle, and strive to summarize some lessons learned for the venture capital industry while summarizing the past for readers to learn from. If you have friends who want to communicate, you are welcome to contact us. It would be great if you can provide more perspectives and information.

See you in the evolution of our crypto venture capital cycle (Part 2).

Blockchain’s 10 Years of Upheaval

Ethereum 2.0 amidst the competition of interests and power

The Last Miner: A 10,000-Word Review of Ethereum’s 8-Year Mining History

This article is sourced from the internet: The Evolution of Crypto Venture Capital Cycle (Part 1): Rebuilding a New World

In the cryptocurrency market, data has always been an important tool for people to make trading decisions. How can we clear the fog of data and discover effective data to optimize trading decisions? This is a topic that the market continues to pay attention to. This time, OKX specially planned the Insight Data column, and jointly with Coingecko, CoinGlass, AICoin and other mainstream data platforms, starting from common user needs, hoping to dig out a more systematic data methodology for market reference and learning. The following is the fourth issue, jointly presented by the OKX Web3 team and the Coingecko team on the theme of Quickly Getting Started with the On-Chain World. It covers the basics of getting started, filtering out noise, screening for high-quality opportunities, etc. We hope it…