本报告所提及的关于市场、项目、货币等的信息、观点和判断仅供参考,不构成任何投资建议。

The crypto asset market after March 2024 seems to be passively becoming a second-rate performance with the theme of waiting. All the actors, creators and producers seem to have forgotten the plot, the plot and the original theme, and only craned their necks to wait for a certain audience to enter and whether there will be a hurricane tonight.

From mid-March to the end of August, more than five months have passed, and the price of BTC has fluctuated repeatedly in the new high consolidation zone. During this period, the global market has experienced repeated and downward inflation, ambiguous and clear expectations for US dollar interest rate cuts, unpredictable speculation on whether the economy will have a soft landing or a hard landing, and dramatic market fluctuations caused by trend changes that pushed different investors to adjust their positions.

Against this backdrop, some BTC investors in the crypto market conducted their first major sell-off to lock in profits and drain liquidity, interspersed with speculative short selling, panic selling, and changes in risk appetite caused by market sentiment, which led to position adjustments between Altcoins and BTC.

This is the nature of the market movement we have observed during this period.

After 5 and a half months of ups and downs, the crypto market has entered a low period. Spot liquidity has been greatly reduced, leverage has been eliminated, the rebound has been weak, and the rebound price has gradually fallen. Investors are sluggish, and pessimistic and negative emotions are shrouding the crypto market.

This is a result of market movement and also the internal resistance in the next stage. But in our view, the greater resistance lies outside the market – the uncertainty of macro-finance, the hidden worry of a hard landing of the US economy, and the unclear trend of the US equity market.

The crypto market has entered the final stage of clearing, and the market value and long-short hand distribution have entered a state of accumulation, ready for upward movement. However, the funds in the market are relatively weak, and there is no confidence and ability to make independent decisions.

URPD: 2.91 million+ chips poured into the new high consolidation area

The market has been volatile over the past eight months. When we focus our attention on the chain, we can see the orderly results of the chaotic movement.

BitNetwork URPD (3.13)

The URPD indicator is used to describe the statistical analysis of all unspent BTC prices, which can effectively provide insight into the final result of chip allocation. The above figure shows the BTC distribution structure when Bitcoin hit a record high on March 13. At this time, 3.086 million chips were accumulated in the new high consolidation zone (53,000 ~ 74,000 US dollars). As of the closing price on August 31, the number of chips distributed in this range reached 6.002 million, which means that at least 2.916 million+ BTC have been bet in this range in the past 5 months.

BTC URPD (8.31)

In terms of time, it took more than 5 months for BTC to break through in mid-October last year and reach its historical high on March 13. Now, it has been in the new high consolidation zone and sideways for more than 5 months, with the highest price of $72,777 and the lowest price of $49,050, and the band oscillation occurred more than 7 times. This oscillation resulted in the exchange of more than 2.916 million chips (the real data is much higher than this, and the exchange data of centralized exchanges is not fully reflected on the chain), which greatly depleted the liquidity of the market.

BTC realized market value

Through the realized market value compiled at the purchase cost, we can observe that after the market entered the new high consolidation zone in March, although the price failed to achieve further breakthrough, the realized market value is still growing, which means that the large-scale cheap chips have been repriced during this period. Under certain conditions, the repriced BTC can be transformed into support or pressure.

Therefore, we maintain a neutral attitude towards the distribution of URPD. There is indeed a sufficient scale of chips to achieve exchange, and a sufficient scale of funds are optimistic about the future market at this pricing, but the nature of these funds is unknown. Whether they will provide support or pressure to the market in the future remains to be seen.

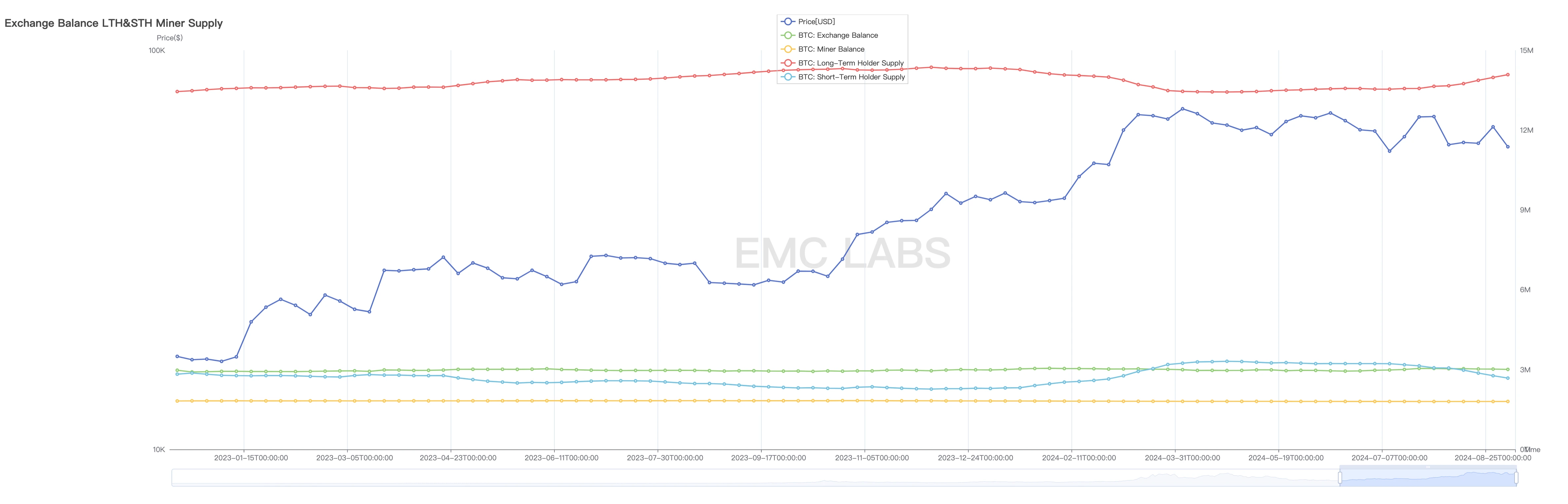

Long and short hands: big sell-off and re-cooling

We view market cycles as large turnovers between long-term and short-term investors over time, during which they convert between BTC and USD.

Long and short position statistics (weekly)

BTC started the rally in mid-October, and the large-scale sell-off of long-term holdings began in December. The market reached a climax in February and March, pushing it to a new high during this period, and then started to adjust, gradually carving out a new high consolidation zone.

Since May, the reduction of long-term holdings has been greatly reduced, and this group has restarted to increase holdings. In the past seven or eight months, the increase has accelerated significantly. From the lowest point to August 31, this group has increased its holdings by 630,000 BTC. The reduction of holdings mainly comes from the selling of short-term holdings and miners.

在 our June report , we pointed out that each bull market will have two major sell-offs, and the second major sell-off will completely drain the market funds and destroy the bull market. What has happened in the past few months is only the first wave of sell-offs. This wave of sell-offs has lasted for more than 5 months and is coming to an end. The on-chain distribution results can clearly show this.

BTC HODL Waves

HODL Waves shows that the number of new coins in March has decreased rapidly, which means that speculative activities have dropped significantly, and the new coins from March to June are also accelerating downward (which is also an important component of the chips in the new high consolidation area). Most of these BTC holders entered the market after the ETF was approved, and should be considered single-cycle long hands. This means that most of the BTC they hold will be converted into long positions, as evidenced by the surge of 470,000 long positions in August. In the foreseeable future, long positions will continue to grow rapidly.

The cooling of BTCs position structure is the result of BTCs return from short-term to long-term during the new high adjustment period. This shift will significantly reduce market liquidity. The decline in liquidity will often push BTC prices further down when funds are scarce, and push prices up when funds are abundant.

Therefore, we can conclude that after more than 5 months of volatility, the market is fully prepared and the price trend is mainly determined by the direction of capital flow (rather than internal chip conversion).

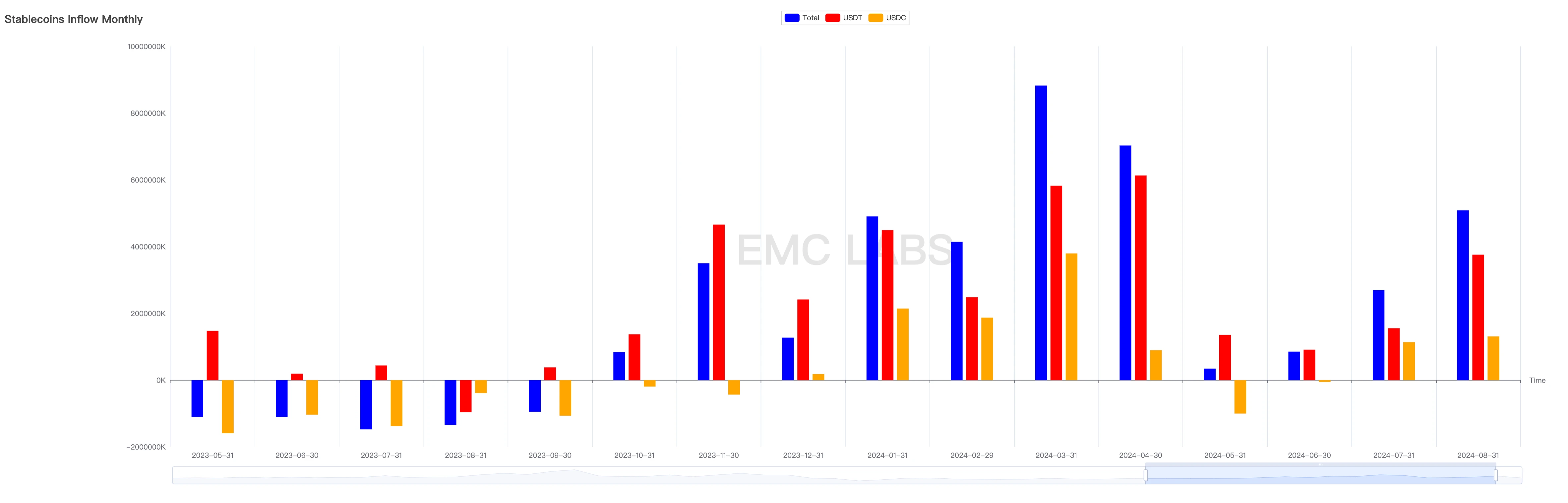

Fund Flow: The ETF Channel Funds That Failed

In the November 2023 report, we proposed that the stablecoin channel fund flow turned positive in mid-October, the first time since February 2022, representing the arrival of a new stage. Since then, BTC has started a round of sharp rise.

Major Stablecoins Inflow and Outflow Statistics (Monthly)

In the past five months of adjustment, May and June were the most scarce months for market funds, with only $1.201 billion inflows recorded in those two months. This pessimistic situation is being reversed, with inflows reaching $2.696 billion and $5.09 billion in July and August, respectively. The entry of these funds indicates their recognition of the new high consolidation range price and their medium- and long-term optimism about the second half of the bull market.

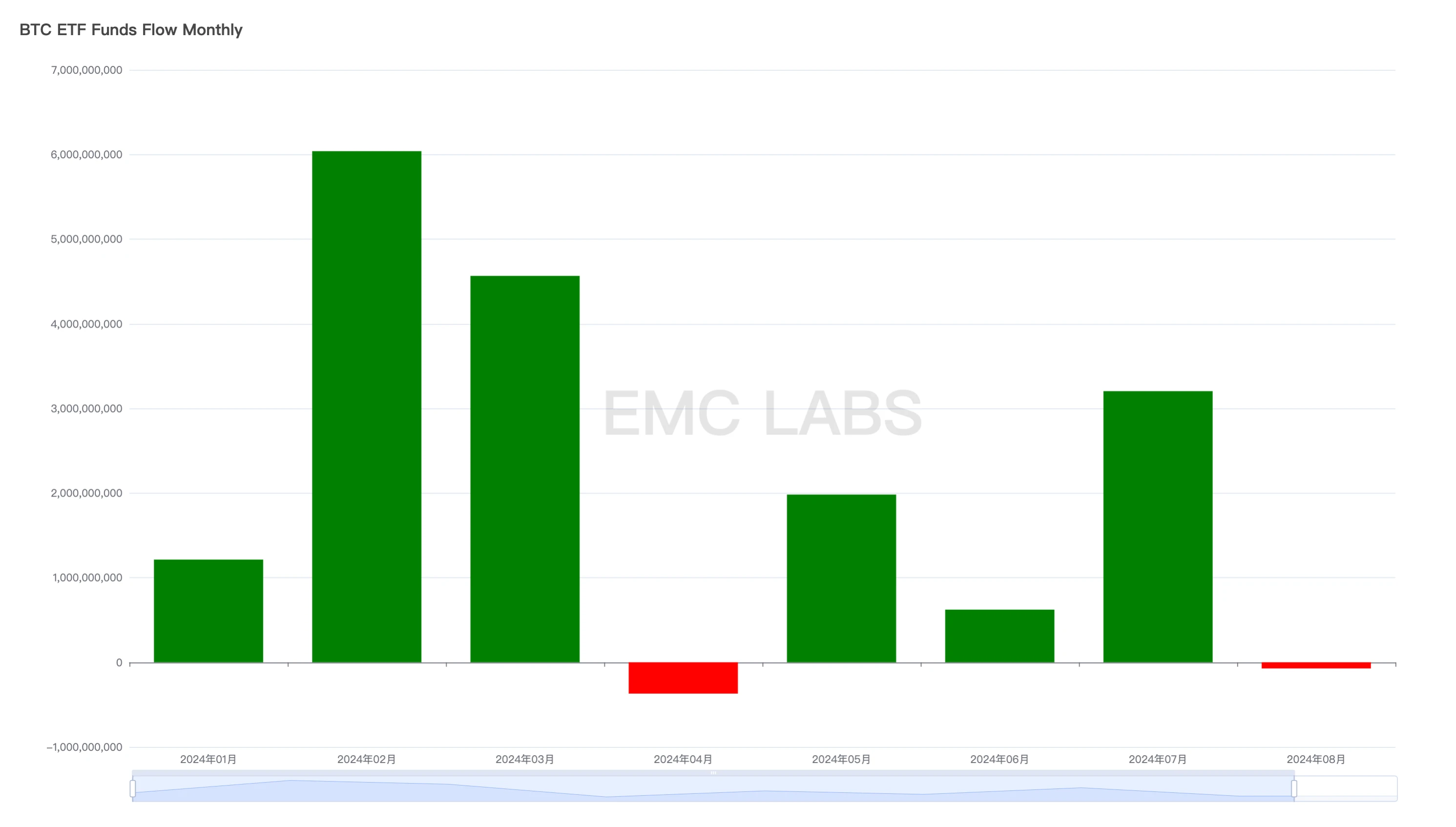

In January this year, after the approval of 11 BTC ETFs in the United States, the funds in this channel began to become an important independent force. In previous reports, we have repeatedly pointed out that the funds in this channel have independent will, and because of their scale and action, they will become an important force in pricing BTC. In the panic selling of the German government in July, the funds in the BTC ETF channel acted decisively and picked up rich and cheap chips.

However, as the US dollar rate hike in August became more and more confirmed, the Japanese yen unexpectedly raised interest rates, and arbitrage traders fiercely closed their positions, causing violent fluctuations in global stock markets, which affected the BTC ETF, which is considered a high-risk asset. The continuous selling from ETF holders at the beginning of the month caused BTC to plummet to $49,000, a new low in several months, and also broke through the lower edge of the new high consolidation zone. Subsequently, the ETF channel funds gradually returned (stablecoin bottom-fishing funds also poured in later), and the BTC price was pulled back to $64,000. By the end of the month, the ETF channel funds returned to outflow, and the BTC price also fell below $60,000 again.

Statistics of overall capital inflow and outflow of 11 BTC ETF Funds in August (Daily)

On a monthly basis, the BTC ETF channel fund inflow this month was -72.83 million US dollars, the second worst month in history, only better than April.

Statistics of overall capital inflow and outflow of 11 BTC ETF Funds (monthly)

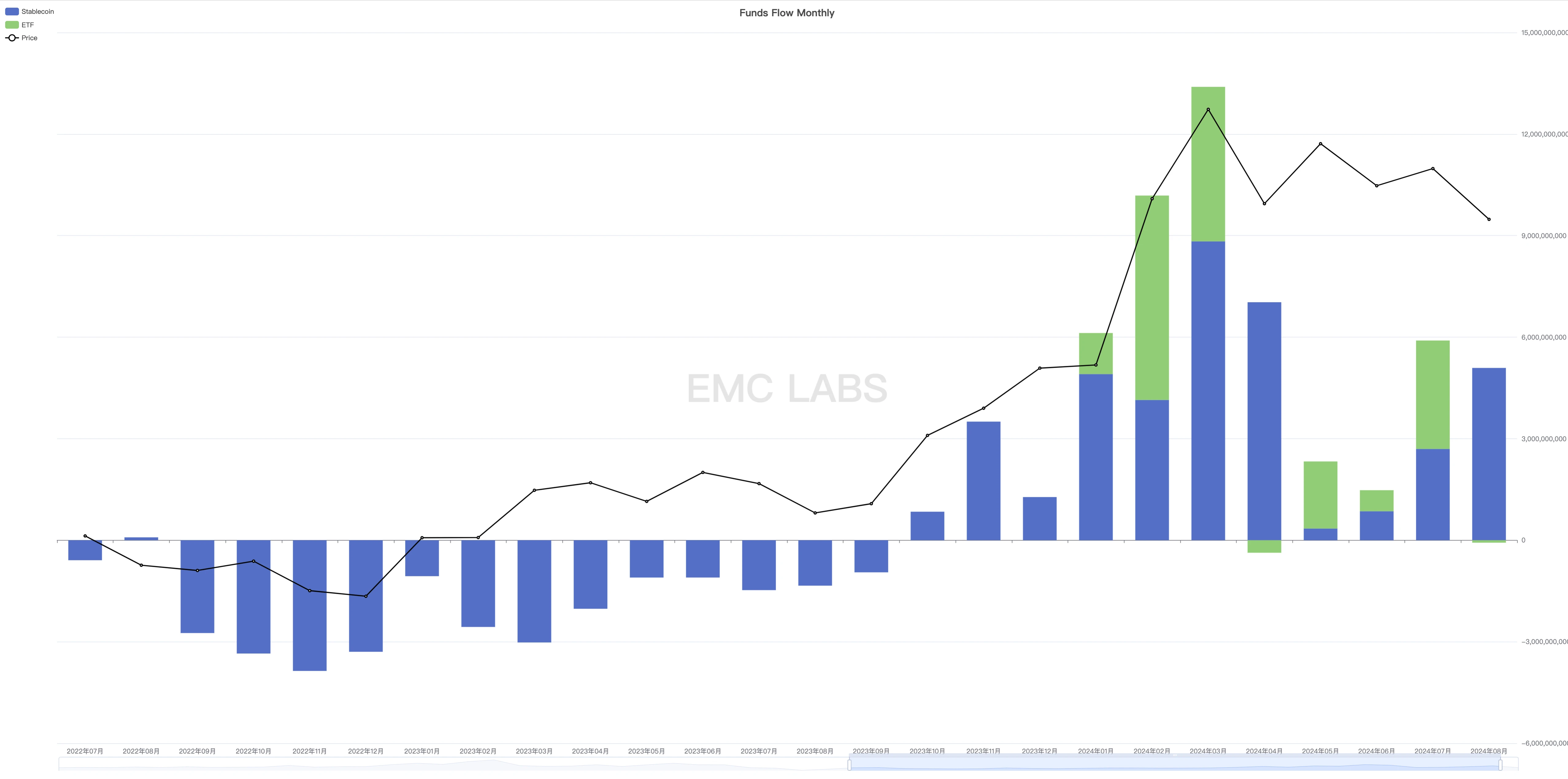

Lets combine the two funds:

Total inflow and outflow of stablecoins and 11 BTC ETF channels (monthly)

Although stablecoins have recorded an increase in inflow for three consecutive months, the ETF channel recorded an outflow this month, resulting in an overall inflow of only $5 billion in August, down from $5.9 billion in July. EMC Labs believes that with the increasingly stable distribution of chips, the inflow of funds is the fundamental reason why BTC was able to pull back to $65,000 in August after the big crash. However, the reduction in capital inflows has caused this months high of $65,050 to be far lower than the $70,000 in July. The reduction in funds is the inflow of funds from the ETF channel, which dropped from $3.2 billion in July to $72.83 million this month.

The attitude of funds in the BTC ETF channel, which is closely connected to the U.S. stock market, has become the most critical factor in determining market trends.

September rate cut: soft landing vs hard landing

Unlike BTC鈥檚 weak performance in August, although it also experienced violent fluctuations, the US stock market still showed amazing resilience during the same period. The Nasdaq recorded a monthly increase of 0.65%, while the Dow Jones Industrial Average hit a record high. During this period, there was a lot of discussion about whether to raise interest rates by 25 or 50 basis points in September, but the real focus of traders was actually the core issue of whether the US economy will have a soft landing or a hard landing.

According to the current trend of US stocks, EMC Labs believes that the market as a whole tends to believe that the US economy will achieve a soft landing, so it has not priced the US stock market downwards under the expectation of a hard landing. Based on the assumption of a soft landing, some funds chose to withdraw from the Big Seven that had previously risen sharply (most of which underperformed the Nasdaq this month) and entered other blue-chip stocks with smaller gains, pushing the Dow Jones Index to a record high.

Based on past experience, we tend to judge that investors in the US stock market regard BTC as a Big Seven asset – although it has a bright future, it is currently overvalued, so there has been a large-scale sell-off, which is roughly synchronized with the sell-off of the Big Seven. However, compared with mainstream funds, the Big Seven is much more attractive than BTC, so after the plunge, the rebound of the Big Seven is stronger than BTC.

Currently, CME FedWatch shows that the probability of a 25 basis point rate cut in September is 69%, and the probability of a 50 basis point rate cut is 31%.

EMC Labs believes that if the 25 basis point rate cut in September is finalized and there are no major economic and employment data indicating that the economy does not meet the characteristics of a soft landing, the US stock market will run steadily. If the Big Seven recovers upward, the BTC ETF will most likely resume positive inflows, pushing BTC upward and hitting the psychological barrier of $70,000 again or even challenging new highs. If major economic and employment data show that the economy does not meet the characteristics of a soft landing, the US stock market will most likely be revised downward, especially the Big Seven, and the corresponding BTC ETF channel funds will most likely not be optimistic. If so, BTC may go down and challenge the lower edge of the new high repair period of $54,000 again.

This speculation is based on the assumption that there will be no trend change in stablecoin channel funds in September. In addition, we are cautious about stablecoins. Although funds in this channel continue to accumulate, we tend to believe that it is difficult for it to push BTC out of an independent market. The most optimistic prediction is that under the background of the upward revision of the seven giants, stablecoin and ETF channel funds are flowing in simultaneously to push BTC upward. If so, breaking through the previous high has a greater probability of success.

结论

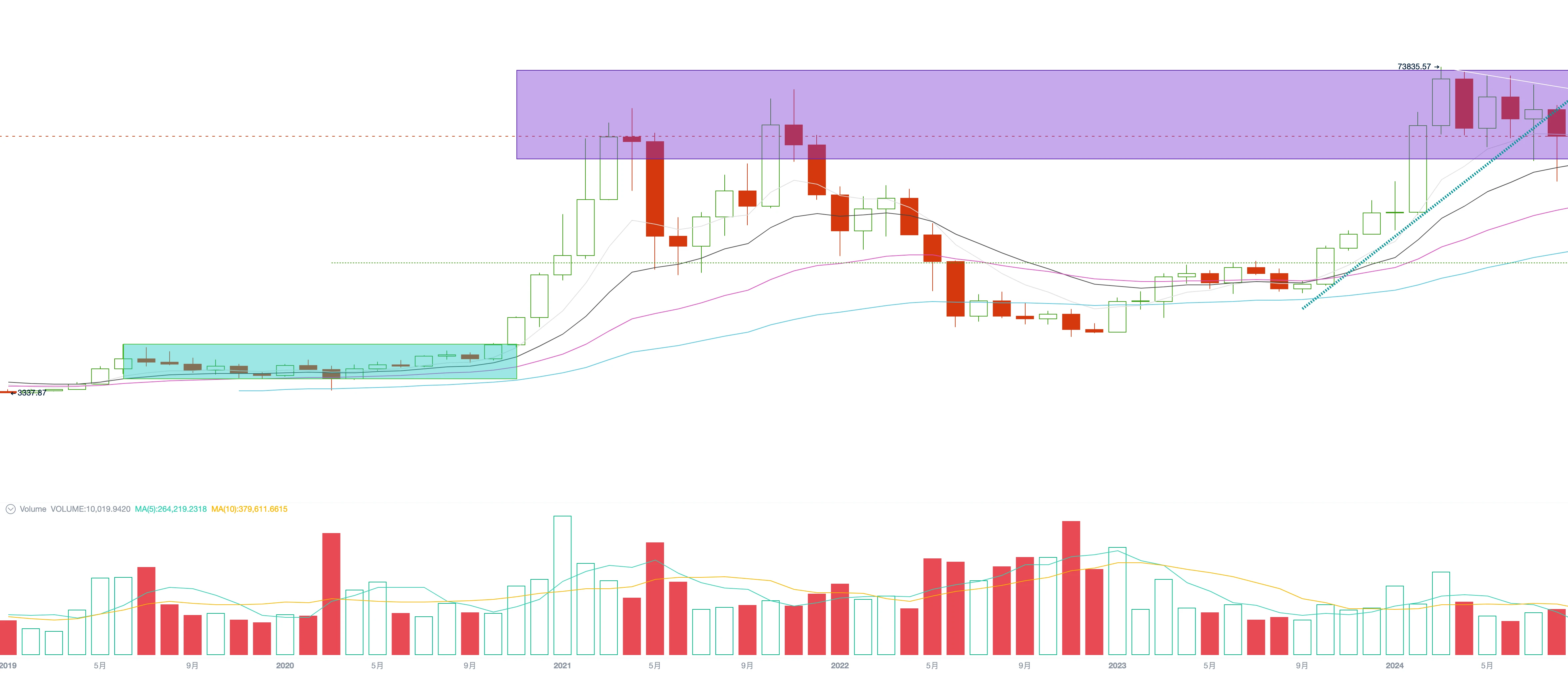

BTC broke through $54,000 in January this year, hit a record high in March, and began to fluctuate and consolidate in the new high consolidation zone in April. It has been more than five months so far, catching up with the six consecutive months of growth since September last year. In terms of time, it is approaching a trend turning point.

BTC monthly chart

BTC monthly chart

This should also be the reason why funds in the stablecoin channel are gradually gathering to reshape buying power.

However, the real breakthrough still depends on the positive macro-financial and core economic data of the United States, and the subsequent re-influx of mainstream funds from the U.S. stock market into the BTC ETF channel.

As the U.S. dollar re-enters the interest rate cut cycle, September becomes the most important month of the year. The U.S. stock and crypto markets will give preliminary answers this month.

EMC Labs 由加密资产投资者与数据科学家于2023年4月创立,专注于区块链行业研究与加密二级市场投资,以行业前瞻、洞察与数据挖掘为核心竞争力,致力于通过研究与投资参与蓬勃发展的区块链行业,推动区块链与加密资产为人类带来福祉。

更多信息请访问: https://www.emc.fund

This article is sourced from the internet: EMC Labs August report: Interest rate cut in September, adjustment of BTC in May+ will reset the trend

Related: The 7th anniversary of a certain An Empire has collected 18 compliance licenses

In celebration of the seventh anniversary of the establishment of Aoan, CEO Richard Teng reviewed the companys development as a leader in the crypto asset industry, emphasizing Aoans achievements in user base, ecological development, security and compliance. The article mentioned that it has more than 210 million users, custody funds of more than $100 billion, and provides a wide range of infrastructure and services to support users in exploring crypto assets. At the same time, Aoan has also made significant efforts in education, security cooperation and user protection, including the establishment of the Academy and the SAFU Fund. Looking to the future, Aoan will continue to lead industry innovation, attract more institutional and retail users, and strive to achieve financial freedom and inclusiveness. Regarding professional sensitivity, Richard Teng mentioned in…