Task

Ranking

已登录

Bee登录

Twitter 授权

TG 授权

Discord 授权

去签到

下一页

关闭

获取登录状态

My XP

0

登入

Original article by Robbie Petersen, Researcher at Delphi Digital

原文翻譯:魯夫、前瞻新聞

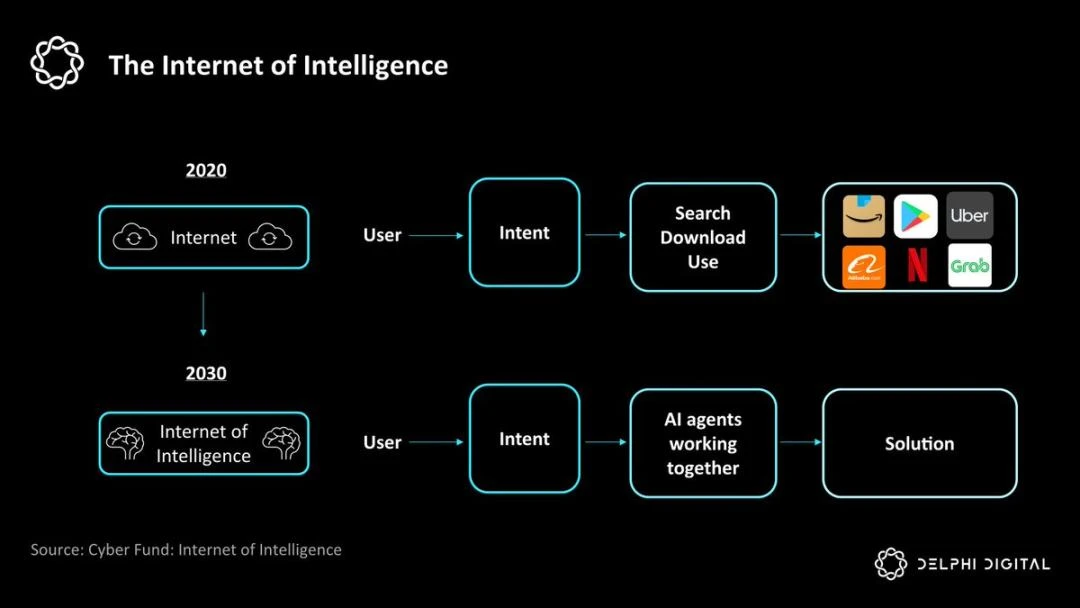

One framework for understanding the success of the Internet is to view it through the lens of orchestration. Fundamentally, we can attribute the success of the most valuable Internet applications to their ability to orchestrate human intent at a more granular level. Amazon orchestrates commercial intent, Facebook, Instagram, and Twitter orchestrate social intent, Uber and Doordash orchestrate ride-hailing and delivery intent, and Google orchestrates informational search intent by matching queries to relevant web content.

One clear trend is that AI agents represent the next logical evolution of large-scale coordination. While today our intentions are fulfilled by searching on the internet, downloading, and interacting with applications, it is reasonable to assume that in the near future our intentions will be executed by a network of AI agents working on our behalf.

Importantly, this shift toward an agent-coordinated economy raises a fundamental question: what kind of infrastructure will ultimately underpin this evolution?

In this article, we will (1) explore the bull and bear case studies of AI agents trading in 加密貨幣currencies; (2) outline the logical paths taken by AI agents; and (3) explore value capture in this emerging agent economy.

There has been a lot of speculation about why blockchain could be the economic foundation for the agent economy. However, as is the case with most emerging crypto verticals, the bull case has been reduced to a catch-all narrative that lacks nuance. Today, the popular argument that “agents can’t have bank accounts, so they’ll use crypto wallets instead” seems to ignore the fundamental value proposition of cryptocurrency. Regardless of accessibility, it is entirely possible for agents to have bank accounts under a FBO (For Benefit Of) account structure. For example, companies like PayPal already manage millions of subaccounts under a single FBO account structure. They can manage AI agents in the same way: each agent has their own virtual subaccount, tracked by the platform but aggregated at the bank level. Notably, Stripe recently announced that they will be adding support for agent transactions under a similar structure.

https://twitter.com/jeff_weinstein/status/1857161398943642029

Furthermore, the argument that this would undermine the autonomy of AI agents is somewhat simplistic. At the end of the day, someone manages the private keys of AI agents, so they are not fully autonomous anyway. While in theory the private keys of AI agents could be stored in a trusted execution environment (TEE), this is both expensive and impractical operationally. Moreover, even allowing agents to be 100% autonomous does not bring practical freedom, as they need to serve humans at the end of the day.

On the contrary, the real pain points that drive proxy transactions in traditional fields and on blockchain are as follows:

Settlement Times: Traditional payments face delays of days and batch processing limitations, especially in cross-border transactions. This lack of instant settlement severely hinders AI agents that need real-time responses to operate efficiently. Blockchain Solutions: Public blockchains provide near-instant settlement finality through atomic transactions, enabling real-time agent-to-agent interactions with no counterparty risk. These transactions settle 24/7, regardless of geography or banking hours.

Global accessibility: Traditional banking infrastructure creates huge barriers for developers around the world, with 70% of developers outside the United States facing challenges using payment channels. Blockchain solutions: Public blockchain infrastructure is inherently borderless and permissionless, enabling global proxy deployment without the need for traditional banks. Anyone with internet access can participate in the network, regardless of geographic location.

Unit Economics: The fee structure of traditional payment systems (3% + fixed fee) makes small transactions economically infeasible, creating a barrier for AI agents that need to make frequent small transactions. Blockchain Solutions: High-performance blockchains enable small transactions at minimal cost, allowing agents to efficiently conduct high-frequency, low-value transactions.

Technology Accessibility: Traditional payment infrastructure lacks programmatic APIs and has strict PCI compliance requirements. Systems designed for human interaction through web forms and manual input create significant barriers to automated agent operations. Blockchain Solutions: Blockchain infrastructure provides native programmatic access through standardized APIs and smart contracts, without the need for forms or manual input. This enables reliable automated interactions and avoids PCI compliance overhead.

Multi-agent scalability: Traditional systems have difficulty managing multiple AI agents that require independent funds and accounts, resulting in high costs for banking relationships and complex accounting requirements. Blockchain solutions: Blockchain addresses can be easily generated programmatically, allowing for efficient fund segregation and multi-agent architecture. Smart contracts provide flexible, programmable fund management without the overhead of traditional banks.

While the technical advantages of cryptocurrencies are certainly compelling, they are not necessarily a prerequisite for a wave of intermediary commerce. Despite the limitations of traditional payment methods, they benefit from massive network effects. Any new infrastructure needs to offer compelling advantages to drive adoption, not just marginal improvements.

Looking ahead, we anticipate that agent adoption will occur in three distinct phases, with increasing levels of agent autonomy in each phase:

We are currently in the first phase. Perplexity’s recently launched “Buy with Pro” feature provides a glimpse into how humans will increasingly transact with AI agents. Their system allows AI bots to research products, compare prices, and execute purchases on behalf of users by integrating with traditional credit cards and digital wallets like Apple Pay.

While this process could theoretically leverage cryptocurrency, there doesn’t seem to be a clear benefit. Luke Saunders notes that the question of whether cryptocurrency is necessary comes down to the level of autonomy required of the agent. Currently, these agents are not autonomous enough. They don’t independently manage resources, take on risks, or pay for other services; they are simply research assistants who help you before you decide to buy. It’s not until the later stages of agent adoption that the limitations of traditional channels become apparent.

The next stage is for agents to autonomously initiate transactions with humans. This is already happening on a small scale: AI trading systems execute trades, smart home systems buy electricity at the best price through time-of-use pricing, and automated inventory management systems place replenishment orders based on demand forecasts.

However, over time we are likely to see more complex business cases for human-machine interaction emerge, potentially including:

Payments and Banking: AI agents optimize bill payments and cash flow, detect fraud and dispute charges, automate expense categorization, and maximize interest while reducing expense expenses through intelligent account management.

Shopping and Consumers: Price monitoring and automated purchasing, subscription optimization, automated refund claims, and smart inventory management for household items.

Travel and transportation: flight price monitoring and rebooking, smart parking management, ride-sharing optimization, and automated travel insurance claims processing.

Home Butler: Smart temperature, predictive maintenance scheduling, and automatic consumables replenishment based on usage patterns.

Personal Finance: Automatic tax optimization, portfolio rebalancing, and bill negotiation with service providers.

Importantly, while these use cases will certainly begin to expose the shortcomings of traditional paths as agents begin to manage resources on behalf of humans and make decisions autonomously, most of these transactions can still theoretically be executed under frameworks such as Stripe’s Agent SDK.

However, this phase will mark the beginning of a more fundamental shift: as agents optimize spending in real time, we will see a move to granular usage-based pricing rather than fixed monthly or annual service fees. In other words, in a world where agents become increasingly autonomous, they will need to pay for things like compute resources, query fees for API access, LLM inference costs, transaction fees, and other usage-based pricing for external services.

As the unit economic flaws of card payments became apparent, cryptocurrencies evolved from marginal improvements to being a leapfrog feature better than traditional channels.

The final phase represents a shift in the way value flows in the digital economy. Agents will transact directly with other agents, creating complex autonomous commercial networks. While this has only recently emerged in the speculative corners of the cryptocurrency market, we will see more complex use cases emerge:

Resource 市場: Compute agents negotiate with storage agents for optimal data placement, energy agents trade grid capacity with consumer agents in real time, bandwidth agents auction network capacity to content delivery agents, and cloud resource agents perform real-time arbitrage between providers.

Service optimization: Database agents negotiate query optimization services with computing agents, security agents purchase threat intelligence from monitoring agents, cache agents exchange space with content prediction agents, and load balancing agents coordinate with extension agents.

Content and data: Content creation agents license assets from media management agents, training data agents negotiate with model optimization agents, knowledge graph agents trade verified information, and analytics agents purchase raw data from collection agents.

Business operations: Supply chain agents coordinate with logistics agents, inventory agents negotiate with purchasing agents, and customer service agents sign contracts with professional support agents.

Financial services: Risk assessment agents trade insurance with underwriting agents, finance agents optimize returns with investment agents, credit scoring agents sell verification materials to loan agents, and liquidity agents coordinate with market making agents.

This phase requires infrastructure that is fundamentally designed for machine-to-machine commerce. The traditional financial system is built on manual identity verification and oversight, which inherently hinders an economy dominated by agent-to-agent commerce. In contrast, stablecoins, with their programmability, borderlessness, instant settlement, and support for microtransactions, become essential infrastructure.

The evolution towards an agency economy will inevitably create winners and losers. In this new paradigm, several different layers of the technology stack become key points of value capture:

Interface layer: Similar to the competition for end users in the traditional payment environment, these players will likely compete for the interface layer where end users express “proxy intent”. These front ends will gradually evolve from simple payment tools to comprehensive platforms that combine identity, authentication, and transaction capabilities. There are several players that can capture value from this, including: (1) device manufacturers like Apple, because of their hardware security and identity integration capabilities (2) consumer fintech super apps like PayPal and Block’s Cash App, because they have large user bases and existing closed-loop payment networks (3) AI-native interfaces like ChatGPT, Claude, Gemini, and Perplexity, because proxy trading is a logical extension of their existing chatbots, and (4) existing crypto wallets, which can use crypto-nativeness as a first-mover advantage (although less likely).

Identity Layer: A key challenge of the agent economy is distinguishing between human and machine actors. This is especially important in a world where agents begin to disproportionately manage valuable resources and make autonomous decisions. While Apple has an advantage here, Worldcoin is pioneering interesting solutions with its Orb hardware and World ID protocol. By providing verifiable proof of personhood, Worldcoin can indirectly become one of the biggest winners of this trend, providing a platform for application developers to ensure that all users are human. While it may be difficult to see the value today, it will become increasingly clear in the future.

Settlement Layer (Blockchain): If blockchain can replace traditional paths as the canonical settlement layer for AI agents, then blockchains that facilitate agent transactions will capture value at scale.

Stablecoin issuance layer: Given the liquidity network effect, it is reasonable to assume that stablecoins are likely to capture value regardless of which stablecoin the proxy uses. USDC currently appears to be in the best position as Circle is rolling out developer-controlled wallets and stablecoin infrastructure to support proxy transactions.

In the end, the biggest losers may be apps that fail to adapt quickly to the agency economy. In a world where agents, not humans, facilitate transactions, traditional moats will disappear. Whereas humans make decisions based on subjective preferences, brand loyalty, and user experience, agents make decisions purely for performance and economic outcomes. This means that as the lines between apps and agents blur, value will flow to the companies that provide the most efficient, best-performing services, not those that build the best user interfaces or strong brands.

As competition moves away from subjective differentiation and toward objective performance metrics, users (both humans and agents) will benefit the most.

This article is sourced from the internet: Delphi Researcher: Evolution Path and Value Capture of AI Agent Economy

相關:Web3初學者係列:我從Uniswap程式碼中學到的合約開發技巧

最近寫了一篇去中心化交易所開發教學https://github.com/WTFAcademy/WTF-Dapp,參考了Uniswap V3的程式碼實現,學習了許多知識點。之前開發過簡單的NFT合約,這是我第一次嘗試開發Defi合約。相信這些技巧對於想要學習合約開發的新手來說會有很大的幫助。合約開發者可以直接去 https://github.com/WTFAcademy/WTF-Dapp 貢獻程式碼,為 Web3 做出貢獻~ 接下來我們就來看看這些小技巧,有的甚至可以稱得上是噱頭技巧。合約部署的合約地址可以變得可預測 當我們部署合約時,通常會得到一個看似隨機的地址。因為和nonce相關,所以合約地址是…