Differences in the Staking Business Models of Ethereum and Solana: Starting from Lido and Solayer

Original article by Lawrence Lee, Research Fellow at Mint Ventures

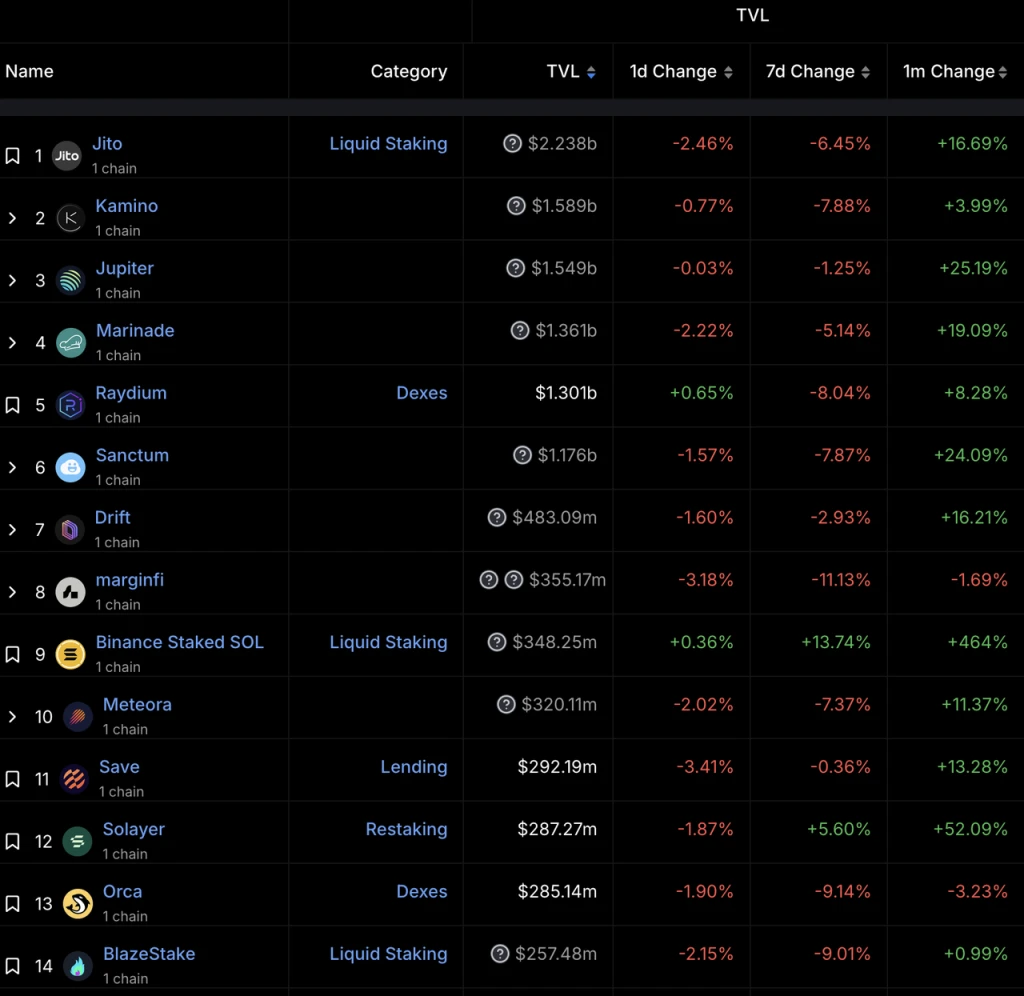

After receiving two rounds of financing, including a $12 million round led by Polychain and financing from Binance labs, the restaking project Solayer on the Solana chain has become one of the few bright spots in the DeFi field in the recent market. Its TVL has also continued to rise and has now surpassed Orca, ranking twelfth in TVL on the Solana chain.

Solana project TVL ranking Source: 德菲拉瑪

The staking track is a 加密貨幣-native sub-track and also the crypto track with the largest TVL. However, its representative tokens such as LDO, EIGEN, and ETHFI have struggled in this cycle. Apart from the Ethereum network on which they are located, are there other reasons?

-

How competitive are the staking and restaking protocols around user staking behavior in the entire staking ecosystem?

-

How is Solayer’s restaking different from Eigenlayer’s restaking?

-

Is Solayer’s restaking a good business?

I hope this article can answer the above questions. Let’s start with staking and restaking on the Ethereum network.

The competitive situation and development pattern of Liquid Staking, Restaking, and Liquid Restaking on the Ethereum network

In this section we will mainly discuss and analyze the following projects:

The Ethereum network’s top liquid staking project Lido, the top restaking project Eigenlayer, and the top liquid restaking project Etherfi.

Lidos business logic and revenue structure

We briefly describe Lidos business logic as follows:

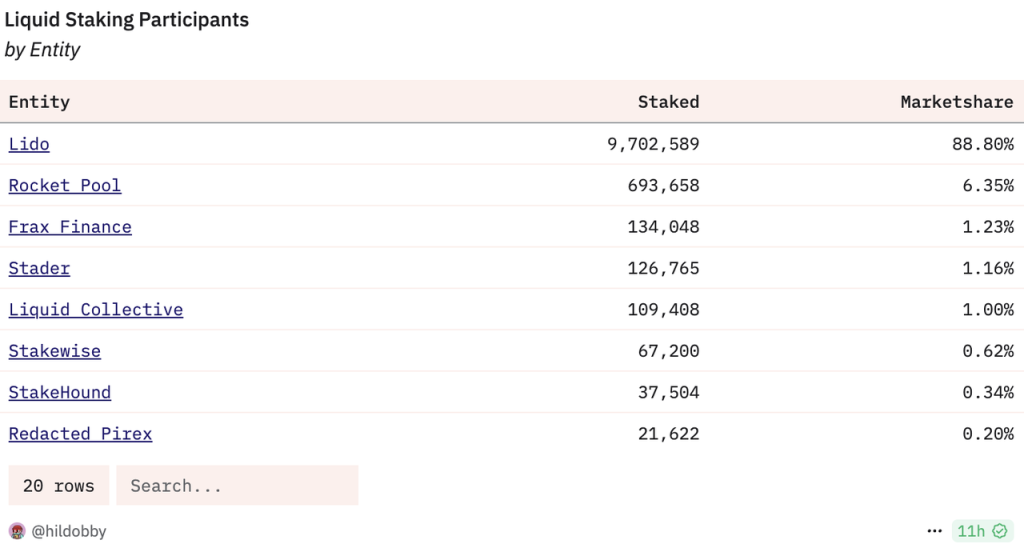

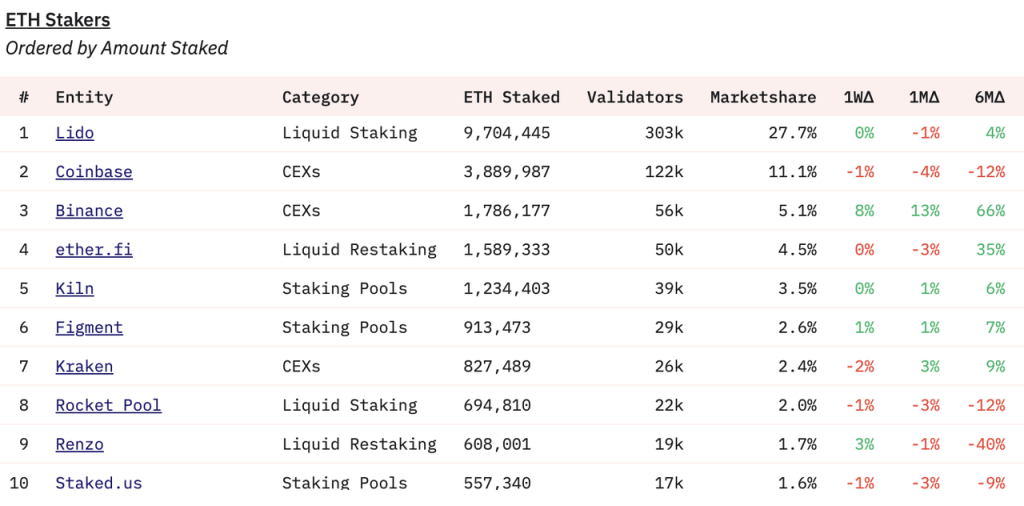

Due to Ethereums insistence on decentralization, ETHs PoS mechanism softly limits the upper limit of a single nodes staking. A single node can only achieve higher capital efficiency by deploying a maximum of 32 ETH. At the same time, staking has relatively high hardware, network and knowledge requirements, and the threshold for ordinary users to participate in ETH staking is high. In this context, Lido has carried forward the concept of LST. Although LSTs liquidity advantage has been weakened after Shapella upgraded and opened withdrawals, LSTs advantages in capital efficiency and composability are still solid, which constitutes the basic business logic of the LST protocol represented by Lido. In the liquid staking project, Lidos market share is close to 90%, leading the market.

Liquid staking participants and market share Source: 沙丘

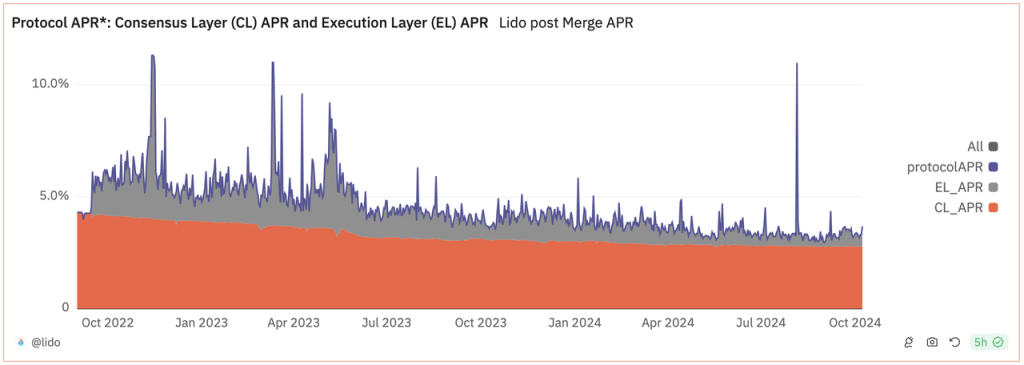

The income of Lido Protocol mainly comes from two parts: consensus layer income and execution layer income. The so-called consensus layer income refers to the income from the PoS issuance of the Ethereum network. For the Ethereum network, this part of the expenditure is paid to maintain the network consensus, so it is called consensus layer income. This part is relatively fixed (the orange part in the figure below); and the execution layer income includes the priority fee and MEV paid by users (for the analysis of the execution layer income, readers can go to Mint Ventures’ previous article to learn more). This part of the income is not paid by the Ethereum network, but by users in the process of executing transactions (or indirectly paid). This part changes with the popularity of the chain and fluctuates greatly.

Lido Protocol APR Source: 沙丘

Eigenlayers business logic and revenue structure

The concept of restaking was proposed by Eigenlayer last year and has become a rare new narrative in the DeFi field and even the entire market in the past year or so. It has also spawned a series of projects with FDV exceeding 1 billion US dollars when they were launched (in addition to EIGEN, there are ETHFI, REZ and PENDLE), as well as many restaking projects that have not yet been launched (Babylon, Symbiotic and Solayer, which we will focus on below). The market enthusiasm is evident (Mint Ventures once conducted 研究 on Eigenlayer last year, and interested readers can go and check it out).

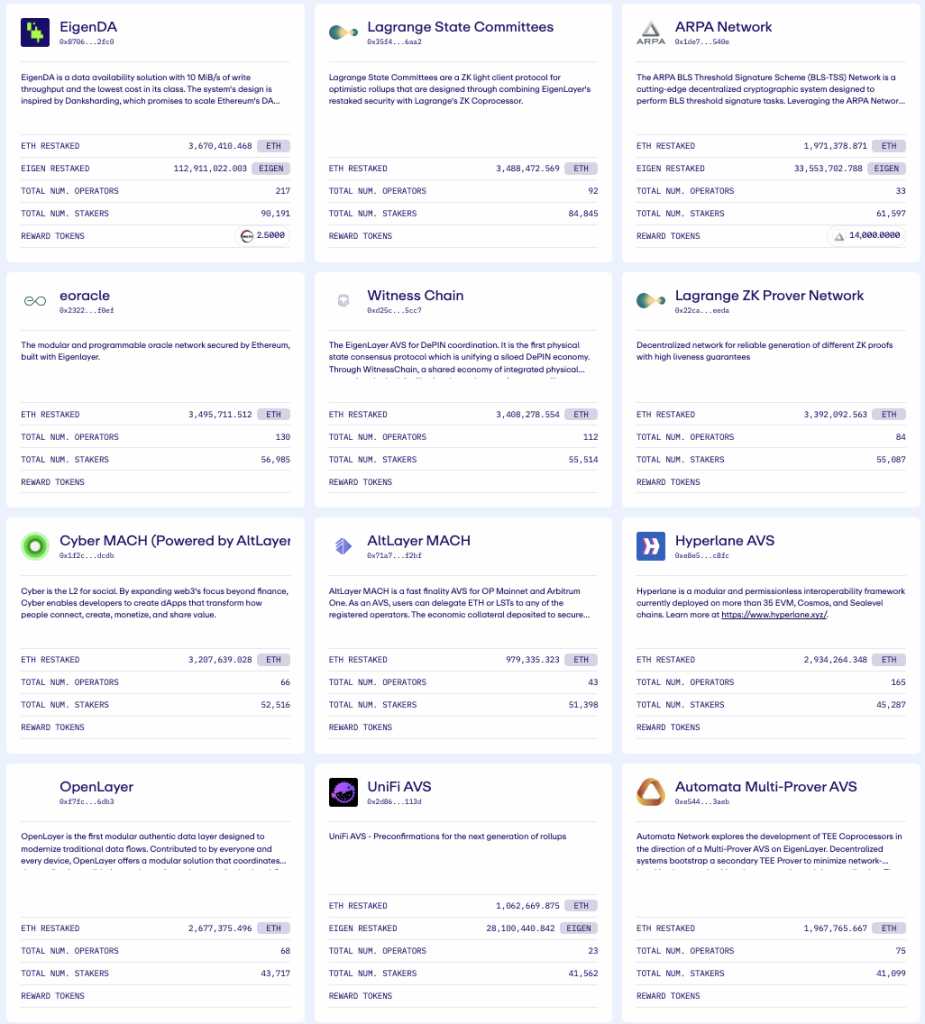

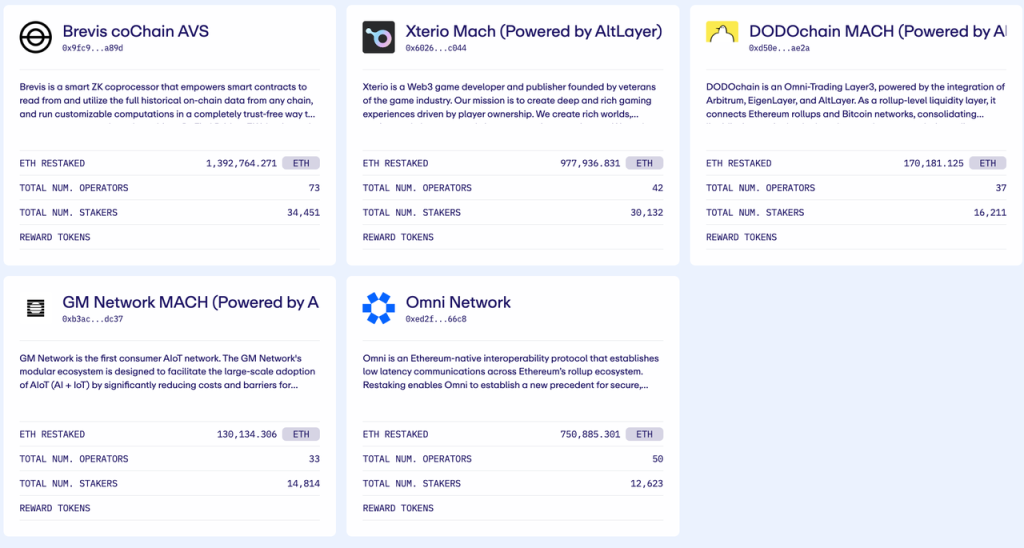

根據其 去中心化金融nition, Eigenlayers Restaking means that users who have already staked ETH can stake their staked ETH again on Eigenlayer (to obtain excess income), hence the name ReStaking. Eigenlayer named its service AVS (Actively Validated Services, literally translated as active verification service in Chinese), which can provide services for various protocols with security requirements, including side chains, DA layers, virtual machines, oracles, bridges, threshold encryption schemes, trusted execution environments, etc. EigenDA is a typical representative of using EigenlayerAVS services.

The protocol currently used by Eigenlayer AVS Source: Eigenlayer official website

Eigenlayers business logic is also relatively simple. On the supply side, they raise assets from ETH stakers and pay fees; on the demand side, protocols with AVS needs pay to use their services, and Eigenlayer, as a protocol security market, matches them and earns a certain fee.

However, looking at all the current restaking projects, the only real benefit is still the tokens (or points) of the relevant protocols. We are not sure whether restaking has obtained PMF: from the supply side, everyone likes the extra benefits brought by restaking; but the demand side is still a mystery: are there really protocols that will purchase protocol economic security services? If so, how much will it be?

Multicoin founder Kyle Samani questions restaking business model Source: X

From the target users of Eigenlayer’s token issuance: oracles (LINK, PYTH), bridges (AXL, ZRO), and DAs (TIA, AVAIL), we can see that staking tokens to maintain protocol security is the core use case of its tokens. Choosing to purchase security services from Eigenlayer will greatly weaken the rationality of its token issuance. Even Eigenlayer itself, when explaining the EIGEN token , used very abstract and obscure language to express the view that “using EIGEN to maintain protocol security” is the main use case.

How to survive Liquid restaking (Etherfi)

Eigenlayer supports two ways to participate in restaking: using LST and native restaking. The method of using LST to participate in Eigenlayer Restaking is relatively simple. After the user deposits ETH in the LST protocol to obtain LST, the LST can be deposited into Eigenlayer. However, the LST pool has a long-term quota. Users who want to participate in restaking during the quota period need to perform native restaking as follows:

-

Users first need to complete the entire process of staking on the Ethereum network by themselves, including fund preparation, execution layer and consensus layer client configuration, setting up withdrawal vouchers, etc.

-

The user creates a new contract account named Eigenpod in Eigenlayer

-

The user sets the withdrawal private key of the Ethereum staking node to the Eigenpod contract account.

It can be seen that Eigenlayers Restaking is a relatively standard restaking. Whether the user deposits other LST into Eigenlayer or native restaking, Eigenlayer does not directly touch the users staked ETH (Eigenlayer does not issue any LRT). The process of Native restaking is a complex version of ETHs native staking, which means similar capital, hardware, network and knowledge thresholds.

Therefore, projects such as Etherfi quickly provided Liquid Restaking 代幣s (LRTs) to solve this problem. The operation process of Etherfis eETH is as follows:

-

The user deposits ETH into Etherfi, and Etherfi issues eETH to the user.

-

Etherfi will stake the received ETH, so as to obtain the basic income of ETH staking;

-

At the same time, they set the nodes withdrawal private key to the Eigenpod contract account in accordance with Eigenlayers native restaking process, so that they can obtain Eigenlayers restaking income (as well as $EIGEN, $ETHFI).

Obviously, the service provided by Etherfi is the best solution for users who hold ETH and want to earn returns: on the one hand, eETH is easy to operate and has liquidity, which is basically the same as Lidos stETH experience; on the other hand, users deposit ETH into Etherfis eETH pool and can obtain: about 3% basic ETH staking income, Eigenlayers possible AVS income, Eigenlayers token incentives (points), and Etherfis token incentives (points).

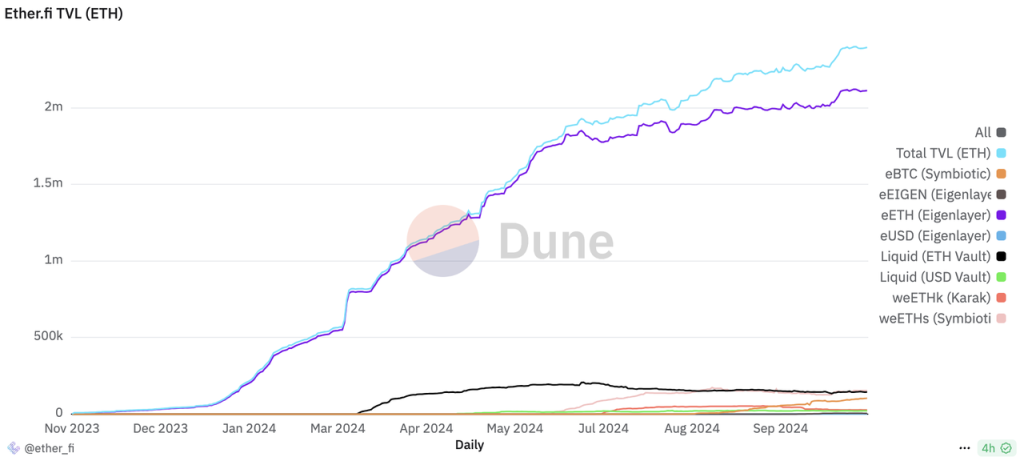

eETH accounts for 90% of Etherfis TVL, contributing more than $6 billion in TVL to Etherfi at its peak, and a maximum FDV of $8 billion, making Etherfi the fourth largest staking entity in just half a year.

Etherfi TVL distribution source: 沙丘

Staking ranking source: 沙丘

The long-term business logic of the LRT protocol is to help users participate in staking and restaking in a simpler and easier way, so as to obtain higher returns. Since it does not generate any income (except its own tokens), the LRT protocol is more like a specific income aggregator of ETH in terms of overall business logic. If we analyze it carefully, we will find that its business logic relies on the following two premises:

-

Lido cannot provide liquid restaking services. If Lido is willing to imitate eETH with its stETH, Etherfi will find it difficult to match its long-term brand advantages, security endorsement, and liquidity advantages.

-

Eigenlayer cannot provide liquid staking services. If Eigenlayer is willing to directly absorb users ETH for staking, it will greatly weaken Etherfis value proposition.

From a purely business logic perspective, it is completely feasible for Lido, as the leader of liquid staking, to provide users with liquid restaking services and a wider range of income sources, and for Eigenlayer to directly absorb user funds and conduct staking restaking more conveniently. So why doesnt Lido do liquid restaking and Eigenlayer do liquid staking?

The author believes that this is determined by the special circumstances of Ethereum. In May 2023, when Eigenlayer had just completed a new round of $50 million in financing, Vitalik wrote a special article titled Dont overload Ethereums consensus and used a series of examples to elaborate on his views on how Ethereums consensus should be reused (that is, how should we restaking).

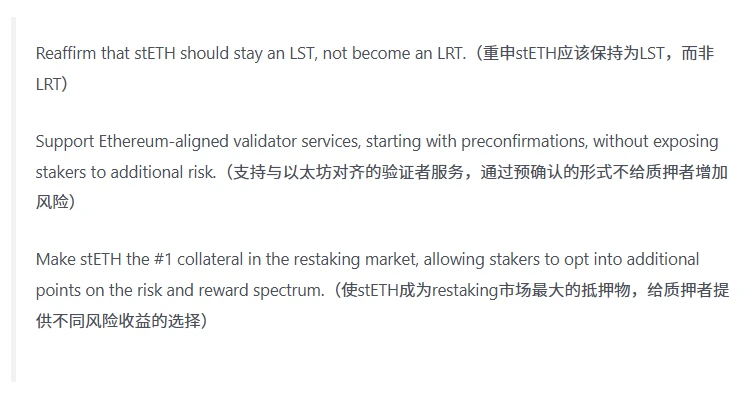

As for Lido, since its scale has long accounted for about 30% of the Ethereum staking ratio, there have been constant voices within the Ethereum Foundation to restrict it. Vitalik has also personally written many articles to discuss the issue of staking centralization. This has forced Lido to make aligning with Ethereum its business focus. Not only has it gradually shut down the business of all chains except Ethereum, including Solana, its de facto leader Hasu published a statement in May this year , confirming the possibility of abandoning his own restaking business, limiting Lidos business to staking, and instead investing in and supporting the restaking protocol Symbiotic, and establishing the Lido Alliance to cope with the competition for its market share from LRT protocols such as Eigenlayer and Etherfi.

來源 of Lido’s position on restaking

As for Eigenlayer, Justin Drake and Dankrad Feist, researchers at the Ethereum Foundation, were hired as consultants by Eigenlayer very early on. Dankrad Feist said that his main purpose of joining was to align Eigenlayer with Ethereum, which may also be the reason why Eigenlayers native restaking process is quite contrary to user experience.

In a sense, Etherfi’s market space was brought about by the Ethereum Foundation’s “distrust” of Lido and Eigenlayer.

Analysis of Ethereum Staking Ecosystem Protocol

Combining Lido and Eigenlayer, we can see that on the current PoS chain, in addition to the token incentives of related parties, there are three long-term sources of income around staking:

-

PoS underlying income, the native tokens paid by the PoS network to maintain network consensus. The yield of this part mainly depends on the inflation plan of the chain. For example, Ethereums inflation plan is linked to the pledge ratio. The higher the pledge ratio, the slower the inflation rate.

-

Transaction sorting income refers to the fees that a node can obtain in the process of packaging and sorting transactions, including the priority fee given by users and the MEV income obtained in the process of packaging and sorting transactions. The yield of this part mainly depends on the activity of the chain.

-

The income from leasing pledged assets is to rent the users pledged assets to other protocols in need, thereby obtaining fees paid by these protocols. This part of the income depends on how many protocols with AVS needs are willing to pay fees to obtain protocol security.

On the Ethereum network, there are currently three types of protocols around staking:

-

Liquid staking protocols such as Lido and Rocket Pool can only obtain the above-mentioned benefits 1 and 2. Of course, users can use their LST to participate in Restaking, but as a protocol, they can only take 1 and 2 above.

-

Restaking protocols represented by Eigenlayer and Symbiotic can only obtain the third type of benefits mentioned above.

-

Etherfi and Puffer are representative liquid restaking protocols. In theory, they can obtain all three of the above benefits, but they are more like LST with aggregated restaking benefits

Currently, the underlying yield of ETH PoS is around 2.8% annualized, which means it will gradually decrease as the ETH staking ratio increases.

The transaction sorting revenue has been significantly reduced with the launch of EIP-4844, and has been around 0.5% in the past six months.

The rental income base of pledged assets is small and cannot be annualized. It is more dependent on the token incentives of EIGEN and related LRT protocols to make this part of the incentive considerable.

For the LST protocol, its revenue base is the number of stakes * the rate of return on stakes. The number of ETH staked is close to 30%. Although this value is still significantly lower than other PoS public chains, from the perspective of decentralization and economic bandwidth of the Ethereum Foundation, it is not hoped that too much ETH will flow into the stake (see Vitalik’s recent blog post . The Ethereum Foundation has discussed whether to set the upper limit of ETH stakes to 25% of the total amount ). The rate of return on stakes is continuously declining, from stabilizing at 6% at the end of 22, often obtaining a short-term APR of about 10%, to only 3% now, and there is no reason to rise in the foreseeable future.

For the above-mentioned protocol tokens, in addition to being constrained by the decline of ETH itself:

The market ceiling of LST on the Ethereum network has gradually become visible, which may also be the reason why the price of LST protocol governance tokens such as LDO and RPL has performed poorly;

For EIGEN, the restaking protocols on other PoS chains, including the BTC chain, are constantly emerging, which basically limits Eigenlayers business to the Ethereum ecosystem, further reducing the potential upper limit of the AVS market size, which is not very clear.

The unexpected emergence of the LRT protocol (the FDV of ETHFI at its peak exceeded 8 billion, exceeding the historical highest FDV of LDO and EIGEN) further diluted the value of the above two in the staking ecosystem;

For ETHFI and REZ, in addition to the above factors, the excessively high initial valuation brought about by their listing during the market boom is a more important factor affecting the price of their tokens.

Solana Staking and Restaking

The operating mechanism of the Solana networks liquid staking protocol, represented by Jito, is basically the same as that of the Ethereum network. However, Solayers restaking is different from Eigenlayers restaking. In order to understand Solayers restaking, we need to first understand Soalnas swQoS mechanism.

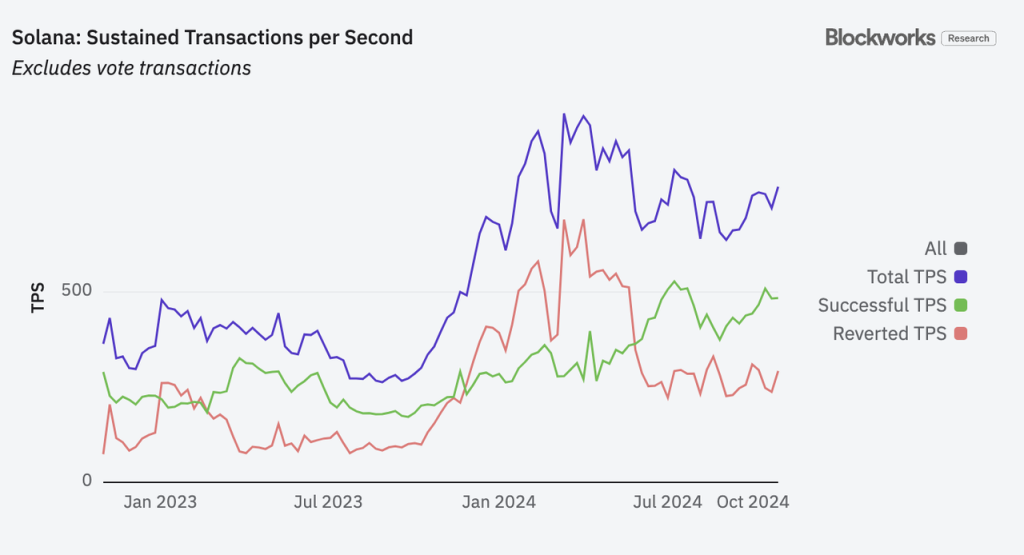

Solana’s swQoS ( stake-weighted Quality of Service) officially came into effect after a client version upgrade in April this year. The starting point of the swQoS mechanism is for the overall efficiency of the network, because the Solana network experienced a long period of network lag during the meme craze in March.

Simply put, after swQoS is enabled, block producers determine the priority of their transactions based on the staked amount of the stakers. A staker with x% of the entire network can submit up to x% of the transactions (for the specific mechanism of swQoS and its far-reaching impact on Solana, readers can read Heliuss article ). After swQoS is enabled, the transaction success rate of the Solana network has increased rapidly.

Solana network success and failure TPS Source:布洛克工程

swQoS floods the transactions of small-amount pledgers in the network, so that when network resources are limited, it prioritizes the rights and interests of larger-amount pledgers in the network, thereby avoiding malicious transactions from attacking the system. To some extent, the more the pledge ratio, the more network privileges you enjoy is in line with the logic of the PoS public chain: staking a larger proportion of the chains native tokens, the greater the contribution to the stability of the chain and the chains native tokens, and it is reasonable to enjoy more privileges. Of course, the centralization problem of this mechanism is also very obvious: larger pledgers can naturally obtain more priority trading rights, and priority trading rights will bring more pledgers, so that the advantages of the head pledgers can be self-reinforced, further tending to oligopoly and even forming a monopoly. This seems to run counter to the decentralization advocated by the blockchain, but this is not the focus of this article. We can also clearly see Solanas pragmatic attitude of performance first on the issue of decentralization from Solanas consistent development history.

In the context of swQoS, the target users of Solayers restaking are not oracles or bridges, but protocols that require transaction passability/reliability, such as DEX. Therefore, Solayer calls the AVS service provided by Eigenlayer exogenous AVS, because these systems served by Eigenlayer are usually located outside the Ethereum main chain. The services provided by itself are called endogenous AVS, because the service objects are located within the Solana main chain.

這 difference between Solayer and Eigenlayer

It can be seen that although both of them are to lease the pledged assets to other protocols with demand to achieve restaking, the core services provided by Solayers endogenous AVS and Eigenlayers exogenous AVS are different. Solayers endogenous AVS is essentially a transaction pass-through leasing platform, and its demanding users are platforms (or their users) that have demand for transaction pass-through, while Eigenlayer is a protocol security leasing platform. The core support of its endogenous AVS is Solanas swQoS mechanism. As Solayer said in its 文件 :

We did not fundamentally agree with EigenLayers technical architecture. So we re-architected, in a sense, restandardized restaking in the Solana ecosystem. Reusing stake as a way of securing network bandwidth for apps. We aim to become the de facto infrastructure for stake-weighted quality of service, and eventually, a core primitive of the Solana blockchain/consensus.

We fundamentally disagree with the technical architecture of EigenLayer. So in a sense, we rebuilt restaking in the Solana ecosystem. Reusing Stake as a way to protect APP network bandwidth. Our goal is to become the de facto infrastructure for swQoS and ultimately the core primitive of the Solana blockchain/consensus. ”

Of course, if there are other protocols on the Solana chain that have staking asset requirements, such as protocol security requirements, Solayer can also lease its SOL to these protocols. In fact, by definition, any leasing/reuse of staking assets can be called re-staking, not just limited to security requirements. Due to the existence of the Solana chain swQoS mechanism, the scope of restaking business on the Solana chain is wider than that on the Ethereum chain, and judging from Solana’s recent hot on-chain activity, the demand for transaction passability is more rigid than the demand for security.

Is Solayer’s restaking a good business?

The business process for users to participate in Solayer restaking is as follows:

-

Users deposit SOL directly into Solayer, and Solayer issues sSOL to users

-

Solayer will pledge the received SOL, so as to obtain basic staking income

-

At the same time, users can delegate sSOL to protocols that have demand for transaction approval rates, thereby obtaining fees paid by these protocols.

Current Solayer AVS 來源

It can be seen that Solayer is not only a restaking platform, but also a restaking platform that directly issues LST. From the perspective of business processes, it is like Lido, which supports native restaking on the Ethereum network.

As mentioned above, there are three sources of income for staking. On the Solana network, these three sources of income are as follows:

-

The underlying income of PoS is the SOL paid by Solana to maintain the network consensus. The annualized income of this part is about 6.5%, which is relatively stable.

-

Transaction sorting income refers to the fees that nodes can obtain in the process of transaction packaging and sorting, including the priority fee given by users for early transactions and the tips paid by MEV searchers. The two parts add up to about 1.5% per annum, but the fluctuations are large, depending on the level of activity on the chain.

-

The income from leasing pledged assets is to rent the users’ pledged assets to other protocols that have demand (transaction passability, protocol security or other). Currently, this part has not yet reached scale.

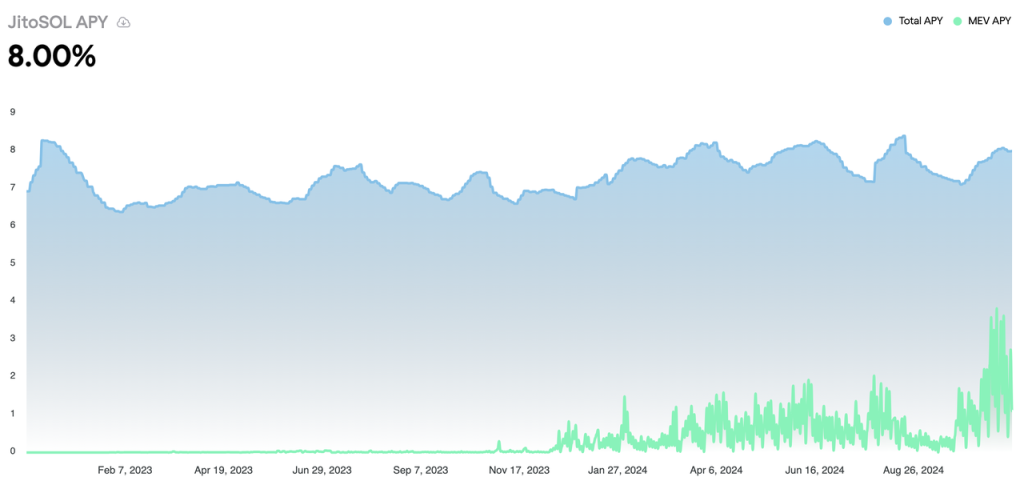

SOL liquid staking (taking JitoSOL as an example) Total APY income and MEV income 來源

If we carefully compare the above three benefits of Ethereum and Solana, we will find that although the market value of SOL is still only 1/4 of ETH, and the market value of staked SOL is only about 60% of the market value of staked ETH, the staking-related protocols of the Solana chain have a larger market and a larger potential market than the staking-related protocols of the Ethereum chain because:

1. In terms of the underlying income of PoS: the network issuance income that SOL is willing to pay has been higher than ETH since December 2023, and the gap between the two is still widening. Whether it is ETH or SOL staking, this accounts for more than 80% of its yield, which determines the income baseline of all staking-related protocols.

Ethereum and Solana token issuance rewards (i.e. the network’s underlying PoS revenue) Source:布洛克工程

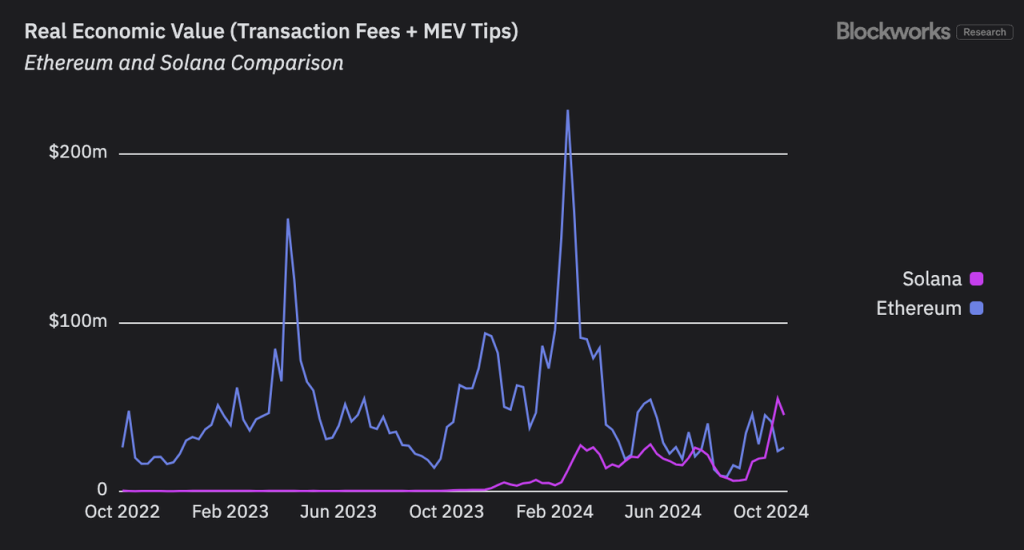

2. Transaction sorting revenue: Blockworks uses transaction fees and MEV tips to reflect the real economic value (REV) of a chain. This indicator can approximately reflect the maximum transaction sorting revenue that a chain can obtain. We can see that although the REV of the two chains fluctuates greatly, Ethereums REV has dropped rapidly after the Cancun upgrade, while Solanas REV has generally shown an upward trend and has recently surpassed Ethereum.

Solana and Ethereum’s REV Source:布洛克工程

3. In terms of the rental income of pledged assets, compared with the Ethereum network which currently only has security income, Solanas swQoS mechanism can bring additional transaction-passive leasing needs.

4. In addition, Solana’s staking-related protocols can expand their businesses according to business logic. Any liquid staking protocol can carry out restaking business, such as Jito we have seen; any restaking protocol can also issue LST, such as Solayer and Fragmetric .

5. More importantly, we currently do not see any possibility of a reversal in the above trend, which means that the advantages of the Solana staking protocol over the Ethereum staking protocol may continue to expand in the future.

From this perspective, although we still cannot say that Solana’s restaking has found PMF, it is clear that Solana’s staking and restaking are better businesses than those on Ethereum.

This article is sourced from the internet: Differences in the Staking Business Models of Ethereum and Solana: Starting from Lido and Solayer

相關:美國證券交易委員會與加密貨幣的鬥爭:爭議的結束,還是新爭議的開始?

原作者:恆興資本 原文翻譯:Vernacular Blockchain 近日,美國證券交易委員會向熱門 NFT 市場 OpenSea 發出威爾斯通知(正式指控的前奏)的消息,為困擾區塊鏈的法律傳奇增添了新的篇章行業多年。眾所周知,SEC 的歷史立場是「除了比特幣之外的一切都是證券」——根據 OpenSea 的通知,包括 NFT。關於加密資產是證券還是商品的爭論至關重要:它決定了 SEC 還是 CTFC 負責監管。從本質上講,這是一項司法實踐,旨在理解 1946 年定義的「安全」:因此,很難應用於現代技術,例如…