My XP

0

Login

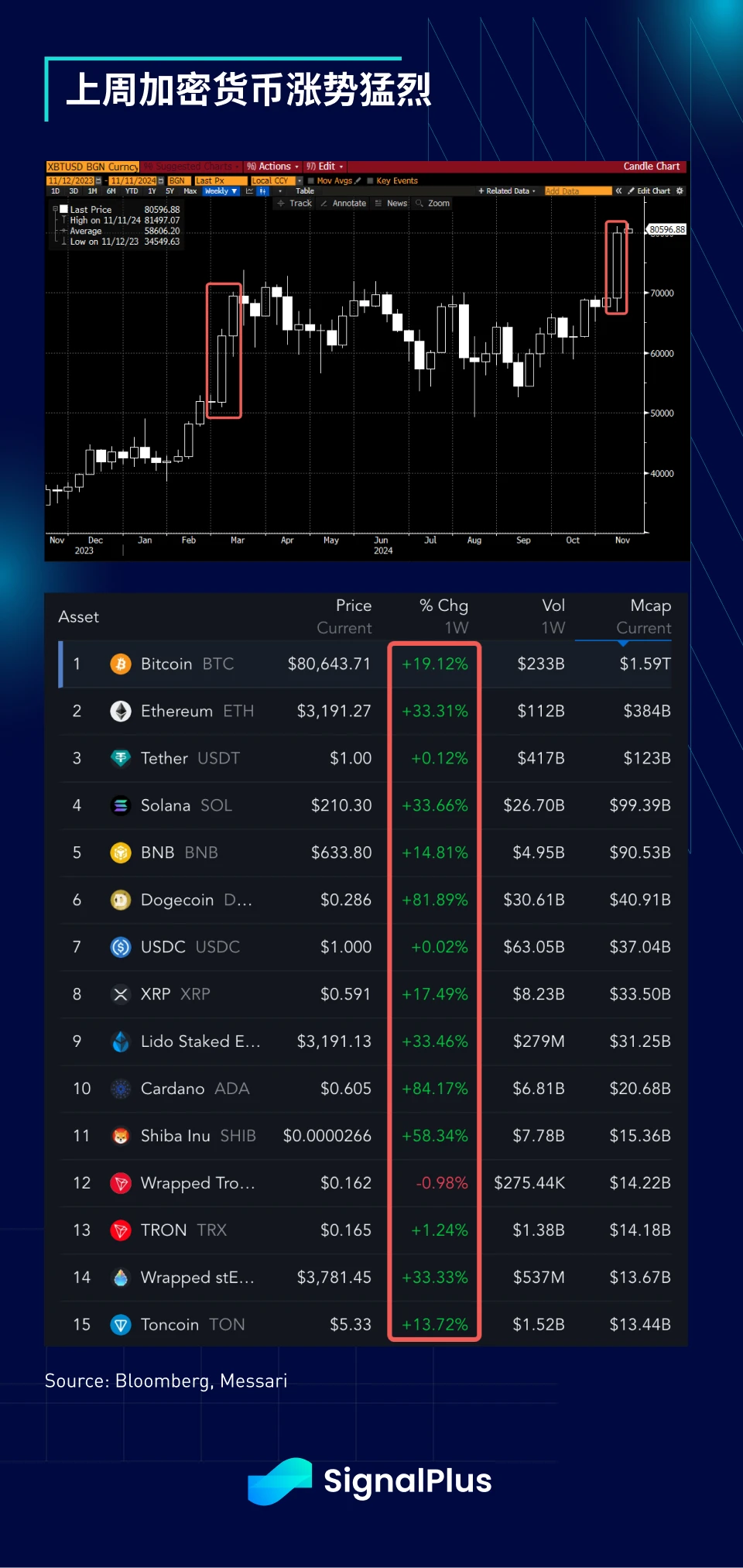

Although it will take Trump two months to officially take office after his election, the impact of his victory has been widely reflected in geopolitics and capital markets. Cryptocurrency has once again become the focus. While vote counting has not yet been completed in some parts of the United States, the price of BTC has exceeded $80,000, and Blackrocks BTC ETF (IBIT) set a record of $1.1 billion in single-day inflows last Thursday. Even the ETH ETF has seen the third-highest single-day inflow in its history.

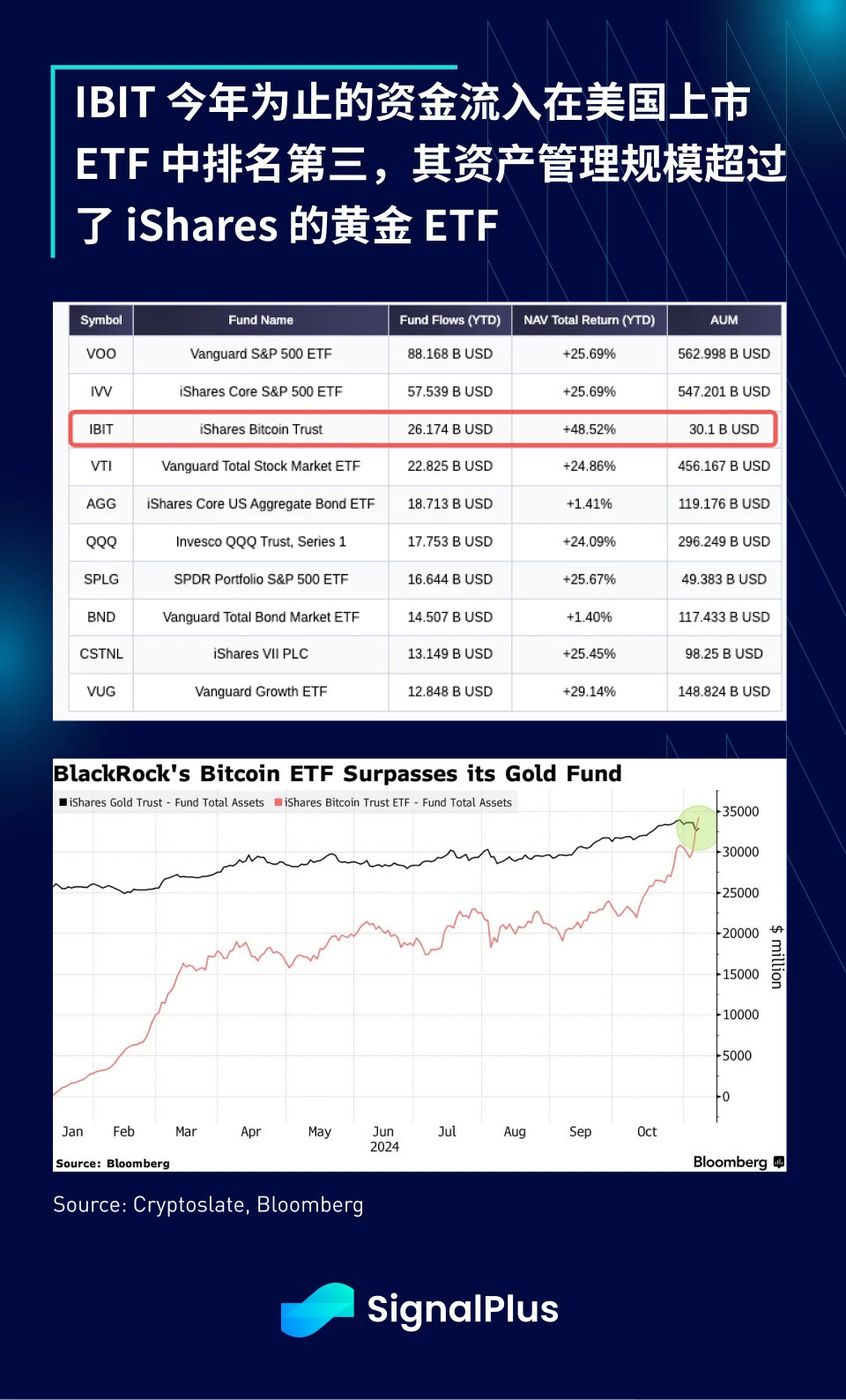

IBIT has the third highest inflow of all US-listed ETFs so far this year, and its assets under management have surpassed iShares own gold ETF, exceeding $33 billion. During this wave of gains, centralized exchanges (CEXs) liquidated more than $800 million in short futures positions in the past week, one of the largest short liquidations this year, while the funding rate of perpetual contracts soared to around 30% as leveraged funds returned in large quantities.

In addition, despite weak on-chain activity, inflows from traditional finance have become a stabilizing support factor. The market value of stablecoins has continued to recover steadily this year and has recovered to near its historical high in 2022. Further inflows of stablecoins should provide more margin funds, and leverage is expected to continue to be maintained as prices continue to rebound.

From a political perspective, given that the incoming government is more inclined to support 加密貨幣currency legislation, the industry is increasingly optimistic about the emergence of a more friendly cryptocurrency regulatory framework in the future.

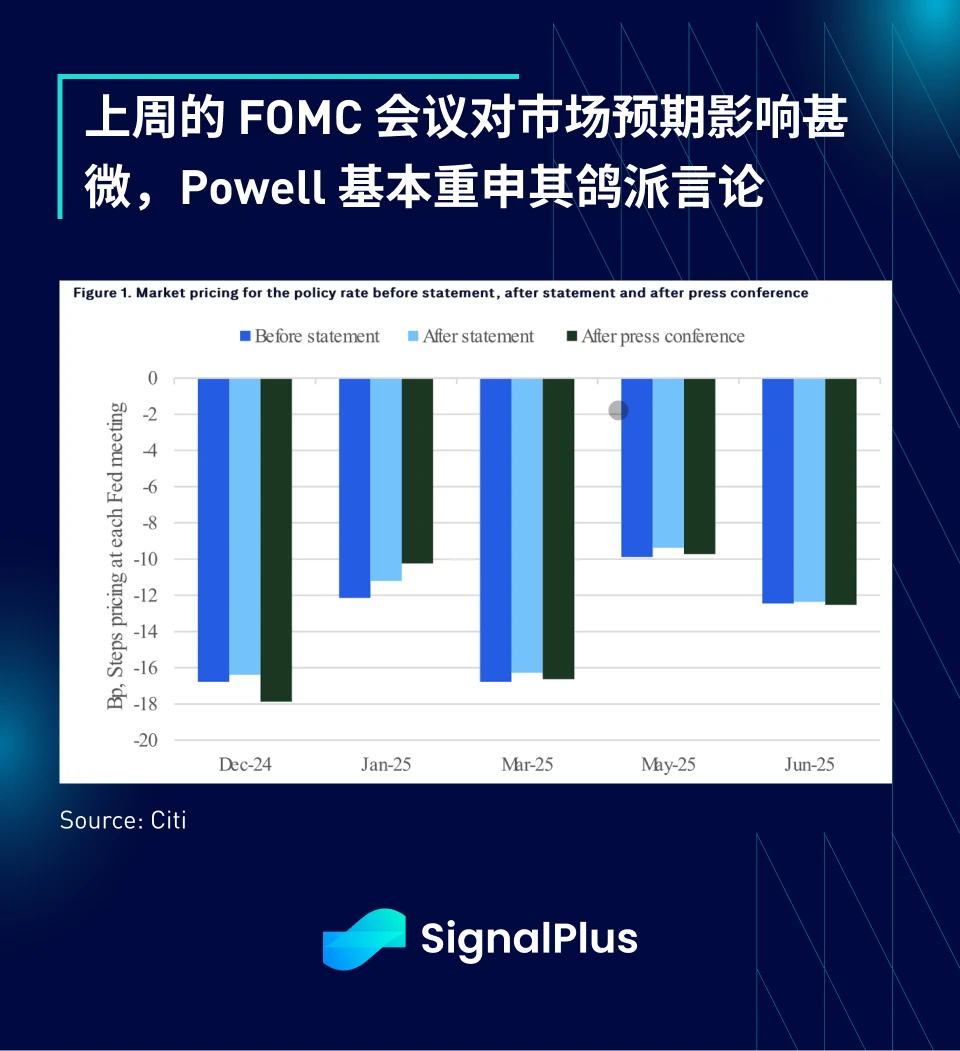

Back to the macro market, US stocks ignored the disappointment of Chinas stimulus policy and continued to hit new highs, while fixed income markets remained stable due to the dovish stance of the FOMC meeting last Thursday. In addition, as the market is expected to remain in risk-on mode until the end of the year, cross-asset volatility of macro assets has dropped significantly. On the other hand, as BTC broke through $80,000, the volatility of BTC and ETH rebounded slightly, and the $100,000 call option once again entered the market focus.

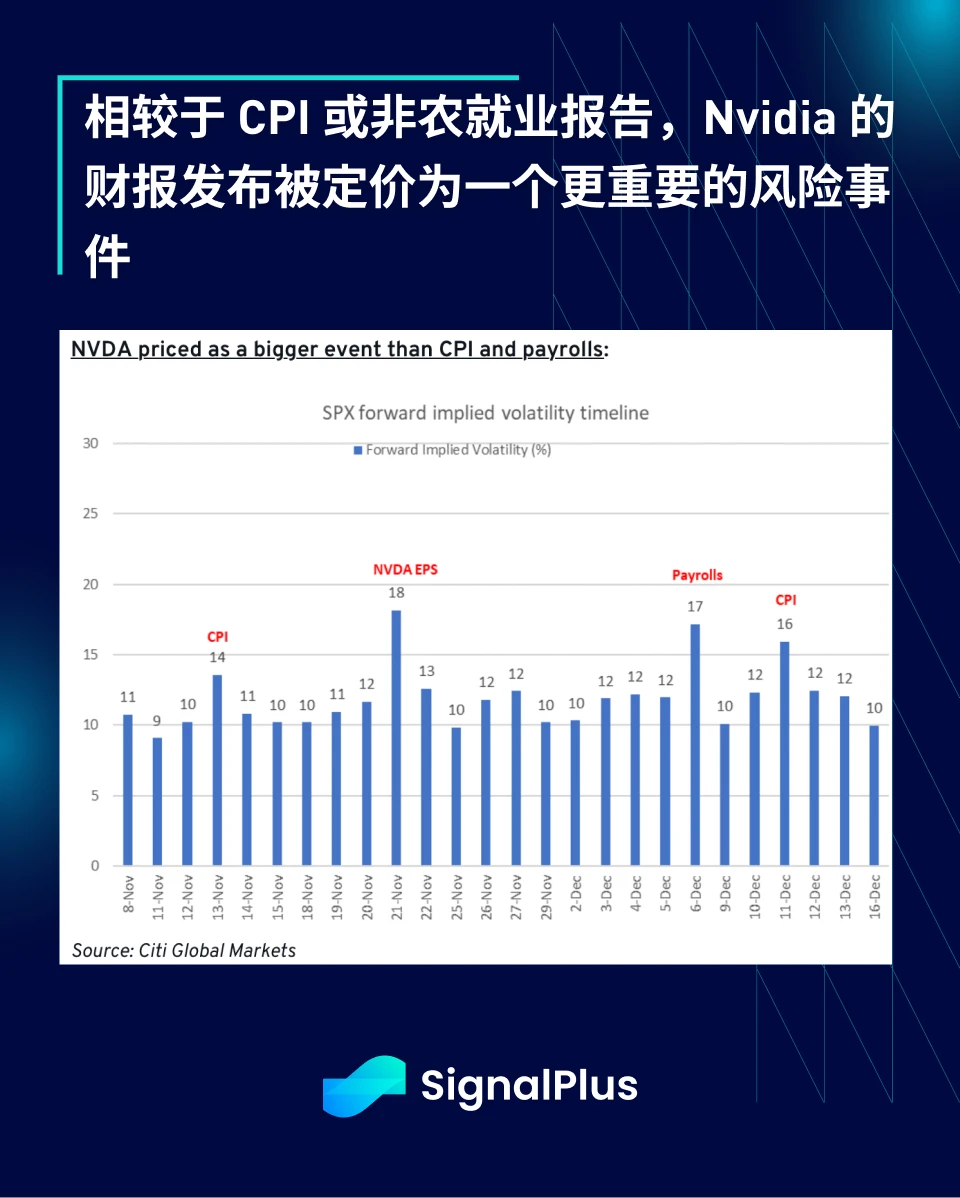

There is not much other important macroeconomic data this month, except for the CPI data release this week. Interestingly, the market pricing reflects that Nvidias earnings release is a more important risk event than CPI or non-farm payrolls, which shows that the market is more confident in the Feds stance and there are no obvious negative catalysts in the market environment.

So, enjoy the party while it lasts, but still maintain prudent risk management. Good luck everyone!

您可以使用 SignalPlus 交易風向標功能 t.signalplus.com 取得更多即時加密資訊。如果您想在第一時間收到我們的更新,請關注我們的推特帳號@SignalPlusCN,或加入我們的微信群(新增助手微信:SignalPlus 123)、Telegram 群和 Discord 社區,與更多朋友交流互動。

SignalPlus 官方網站: https://www.signalplus.com

This article is sourced from the internet: SignalPlus Macro Analysis Special Edition: 80K

相關:美國政治經濟面臨最動盪10天,BTC或到關鍵關頭(10.21~10.27)

Written by: Shang2046 The information, opinions and judgments on markets, projects, currencies, etc. mentioned in this report are for reference only and do not constitute any investment advice. Before November 6, the United States faced the disclosure of key data, the second interest rate cut meeting of the year, and the US election. Amid a series of uncertainties, BTC once again reached a breakthrough point of a historical high. 市場 Summary This week, BTC opened at 69014.87 and closed at 67943.19 USD, down 1.55% for the whole week, with an amplitude of 6.30% and a shrinking volume. This weeks BTC market can be understood as a technical confirmation of the decline of US stocks after a sharp rebound. What will happen to both US stocks and BTC in the next…