Task

Ranking

已登录

Bee登录

Twitter 授权

TG 授权

Discord 授权

去签到

下一页

关闭

获取登录状态

My XP

0

原作者: Charles Yu

原文翻譯:TechFlow

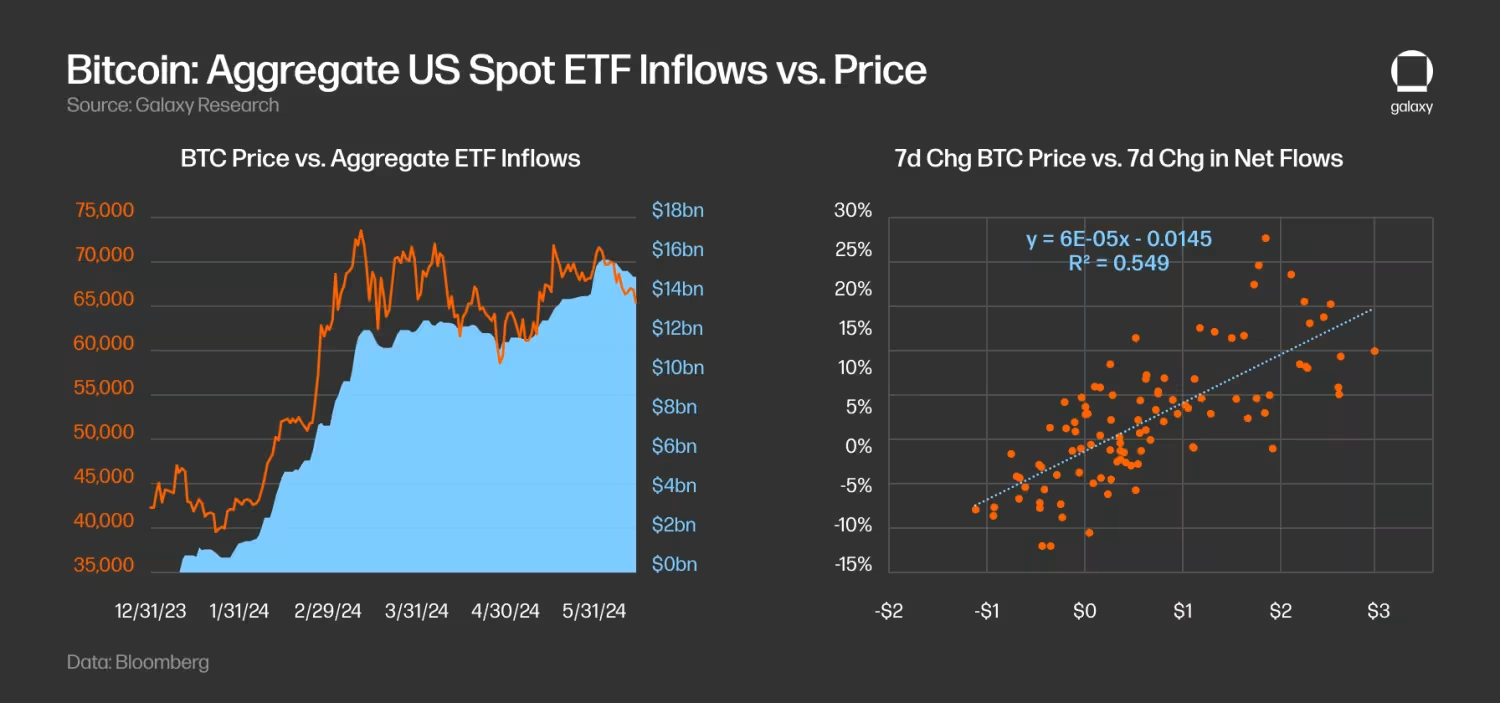

The Bitcoin ETF saw net inflows of $15.1 billion between its launch on January 11, 2024 and June 15, 2024.

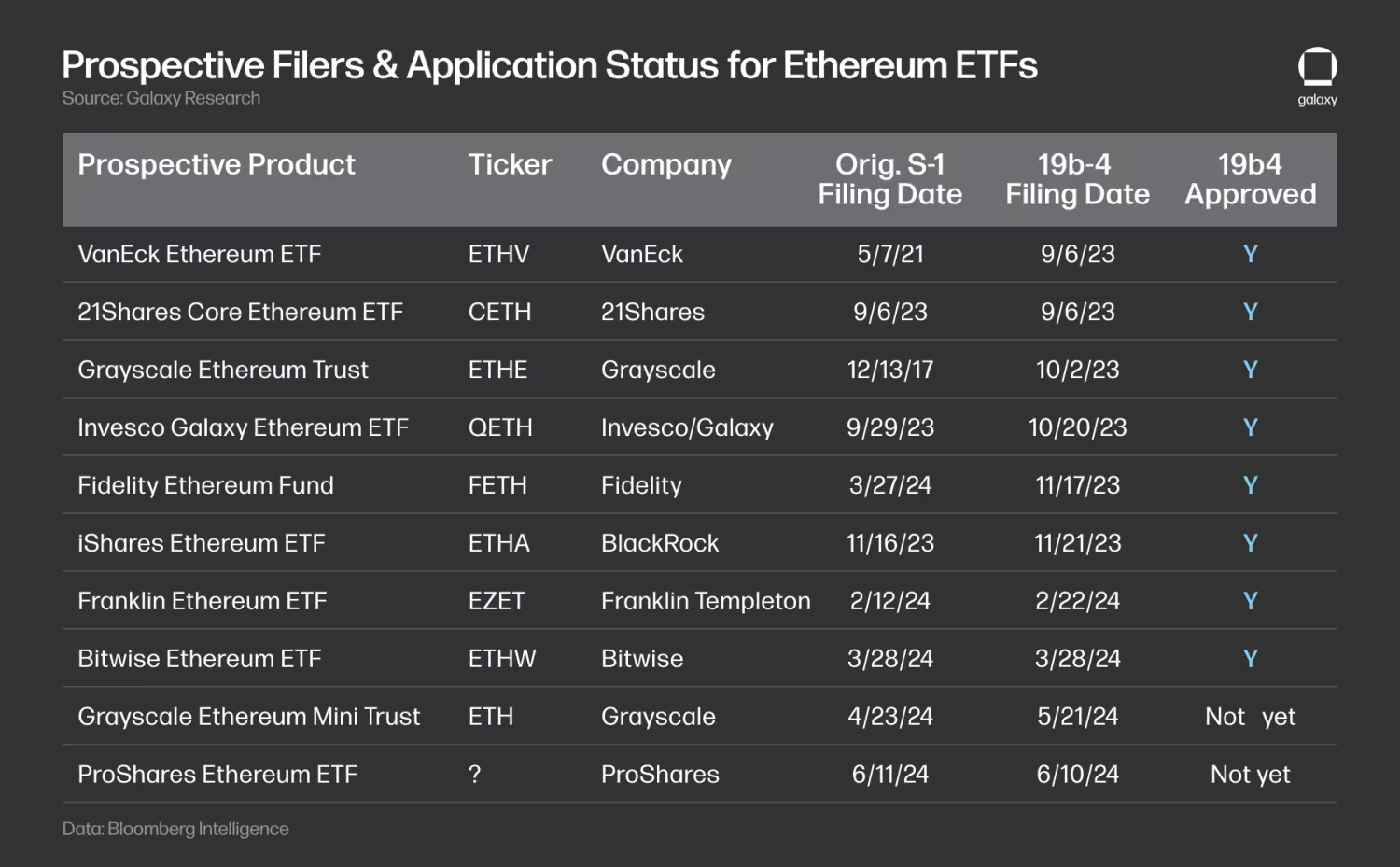

Nine issuers are vying to launch 10 Ethereum spot ETFs in the United States.

The SEC is expected to allow the instruments to begin trading in July 2024, after approving all 19b-4 filings on May 23.

As with the Bitcoin ETF, we believe the primary new accessible market is independent investment advisors, or those associated with banks or broker/dealers.

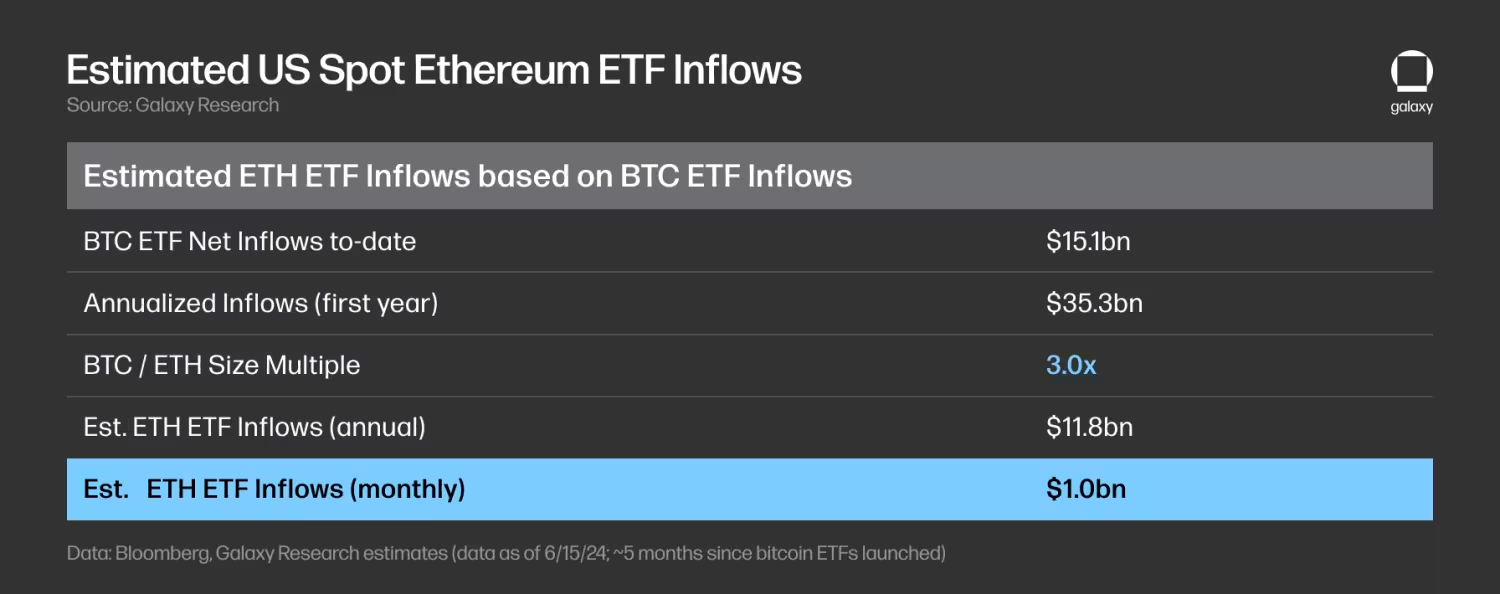

We expect ETH ETF net inflows to reach 20-50% of BTC ETF net inflows in the first five months, with a target of 30%, which would imply $1 billion in net inflows per month.

Overall, we believe ETHUSD is more price sensitive to ETF inflows than BTC due to the majority of ETH total supply being locked in staking, bridges, and smart contracts, and lower amounts on centralized exchanges.

For months, observers and analysts have been underestimating the chances that the Securities and Exchange Commission (SEC) would approve spot Ethereum exchange-traded products (ETPs). Pessimism stemmed from the SEC’s hesitation to explicitly state that Ethereum is a commodity, reports of a lack of engagement with potential issuers, and news of the SEC’s investigations and pending enforcement actions into the Ethereum ecosystem. Bloomberg analysts Eric Balchunas and James Seyffart put the odds of approval at 25% in May (when the first final approval/rejection deadlines for some potential issuers were approaching). However, on Monday, May 20, Bloomberg analysts suddenly raised the odds of approval to 75% after reporting that the SEC had contacted the exchanges. In fact, all applications for spot Ethereum ETPs were approved by the SEC later that week. While we are still waiting for these instruments to actually launch after the S-1 filing becomes effective—which we expect to happen sometime in the summer of 2024—this report draws lessons from the performance of Bitcoin spot ETPs to predict demand for Ethereum ETPs once they launch. We estimate that the spot Ethereum ETP will see ~$5 billion in net inflows in its first five months of trading (~30% of Bitcoin ETP net inflows).

There are currently nine issuers vying to launch exchange-traded products (ETPs) that hold spot ETH. In the past few weeks, several issuers have dropped out. ARK chose not to partner with 21 Shares to launch an Ethereum ETP, while Valkyrie, Hashdex, and WisdomTree withdrew their applications entirely. The following table shows the current status of applications sorted by 19 b-4 filing date:

Grayscale is looking to convert the Grayscale Ethereum Trust (ETHE) into an ETP, as the company did with the Grayscale Bitcoin Investment Trust (GBTC), but has also filed for a “mini” version of the product.

The SEC approved all 19 b-4 filings on May 23rd — these rule changes allow stock exchanges to finally list spot ETH ETPs — but now each individual issuer needs to go back and forth with the regulator on their registration statements. Until the SEC allows these S-1s (or S-3s in the case of ETHE) to go into effect, the products themselves can’t actually begin trading. Based on our research, as well as reporting from Bloomberg Intelligence, we think Ethereum spot ETPs could begin trading as early as the week of July 11, 2024.

Bitcoin ETFs have been online for less than 6 months and can serve as a useful basis for studying the possible acceptance of Ethereum spot ETFs.

資料來源:彭博社

Here are some observations from the first few months of Bitcoin spot ETP trading:

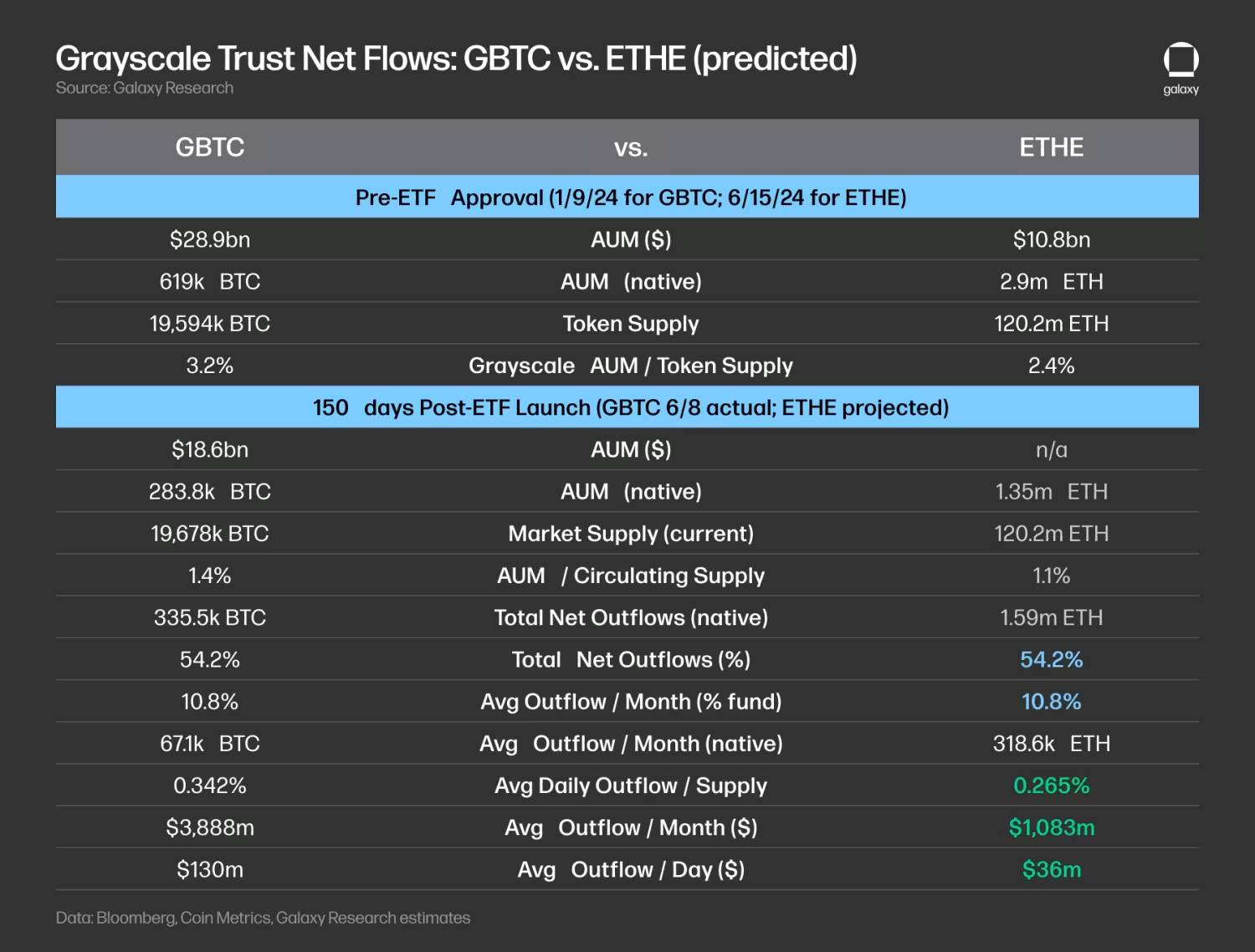

So far, inflows have exceeded expectations. As of June 15, U.S. spot Bitcoin ETFs have accumulated net inflows of more than $15.1 billion since launch, with an average net inflow of $136 million per day. The total amount of Bitcoin held by these ETFs is approximately 870,000 BTC, accounting for 4.4% of the current BTC supply. With BTC trading at around $66,000, the total assets under management of all U.S. spot ETFs are approximately $58 billion (note: before the ETF was launched, GBTC held approximately 619,000 BTC).

ETF inflows have partially driven the price of BTC higher. By regressing the one-week change in BTC price and ETF net inflows, we calculated an r-sq of 0.55, indicating that the two variables are highly correlated. Interestingly, we also found that price changes are a better leading indicator of inflows than inflows.

The unwinding of GBTC trading has taken a toll on overall ETF inflows. GBTC has experienced significant outflows in the first few months since converting the trust to an ETF. GBTC’s daily outflows peaked in mid-March, with $642 million in outflows on March 18th. Since then, outflows have moderated, and GBTC has even seen a few days of net inflows since May (there were 78 days of outflows before the first net inflow on May 3rd). As of June 15th, the BTC balance held by GBTC has decreased from 619k BTC to 278k BTC (a 55% decrease) since the launch of the ETF.

ETF demand is mainly driven by retail investors; institutional demand is increasing. 13 F filings show that as of March 31, more than 900 US investment companies held Bitcoin ETFs, with holdings of approximately $11 billion, accounting for approximately 20% of total Bitcoin ETF holdings, indicating that most demand comes from retail investors. The list of institutional buyers includes some well-known banks (such as JP Morgan, Morgan Stanley, Wells Fargo), hedge funds (such as Millennium, Point 72, Citadel) and even pension funds (such as the Wisconsin Investment Board).

Wealth management platforms have not yet begun offering access to Bitcoin ETFs. The largest wealth platforms have not yet allowed their brokers to recommend Bitcoin ETFs, although Morgan Stanley is reportedly exploring allowing its brokers to advise clients to buy. We wrote in our report, The Sizing of the Bitcoin ETF Market , that access to Bitcoin ETFs by wealth platforms (including broker-dealers, banks, and independent registered investment advisors) is expected to continue over the next few years. Sales-driven inflows from institutional platform access have been minimal so far, but in our view it will be a significant catalyst for Bitcoin adoption in the short to medium term.

Using the Bitcoin ETP as a reference, we can estimate the potential demand for similar Ethereum products.

To estimate the potential inflows into the ETH ETF, we applied a BTC/ETH multiple to estimate the inflows into the Bitcoin US spot ETF based on the relative asset sizes of BTC and ETH in multiple markets. As of May 31:

BTC的市值是ETH的2.9倍。

Across all exchanges, BTC’s futures market is about twice as large as ETH’s based on open interest and trading volume. Specifically on CME, BTC’s open interest is 8.4 times that of ETH, while its daily trading volume is 4.2 times that of ETH.

Total assets under management of various existing funds (broken down by Grayscale trust and products (e.g., futures, spot), and selected global markets) show that BTC funds are approximately 2.6x to 5.3x the size of ETH funds.

Based on the above data, we believe that the inflows into the Ethereum spot ETF will be about 3 times less than the inflows into the US spot Bitcoin ETF (consistent with the market cap multiple) , ranging from 2x to 5x. In other words, we believe that the inflows into the Ethereum spot ETF may be 33% of the inflows into the US spot Bitcoin ETF , ranging from 20% to 50%.

Applying this multiple to the $15.1 billion in Bitcoin spot ETF inflows as of June 15th implies monthly inflows of approximately $1 billion into Ethereum ETFs in the first five months following approval and launch (estimated range: $600 million to $1.5 billion per month).

Several estimates we have seen are lower than our forecasts due to several factors. Namely, our forecast of $14 billion in first-year Bitcoin ETF inflows in previous reports was based on the entry of wealth management platforms, but Bitcoin ETFs saw significant inflows prior to the arrival of these platforms. Therefore, we advise caution in predicting a lack of demand for Ethereum ETFs.

There are a number of structural/market differences between BTC and ETH that will impact ETF inflows:

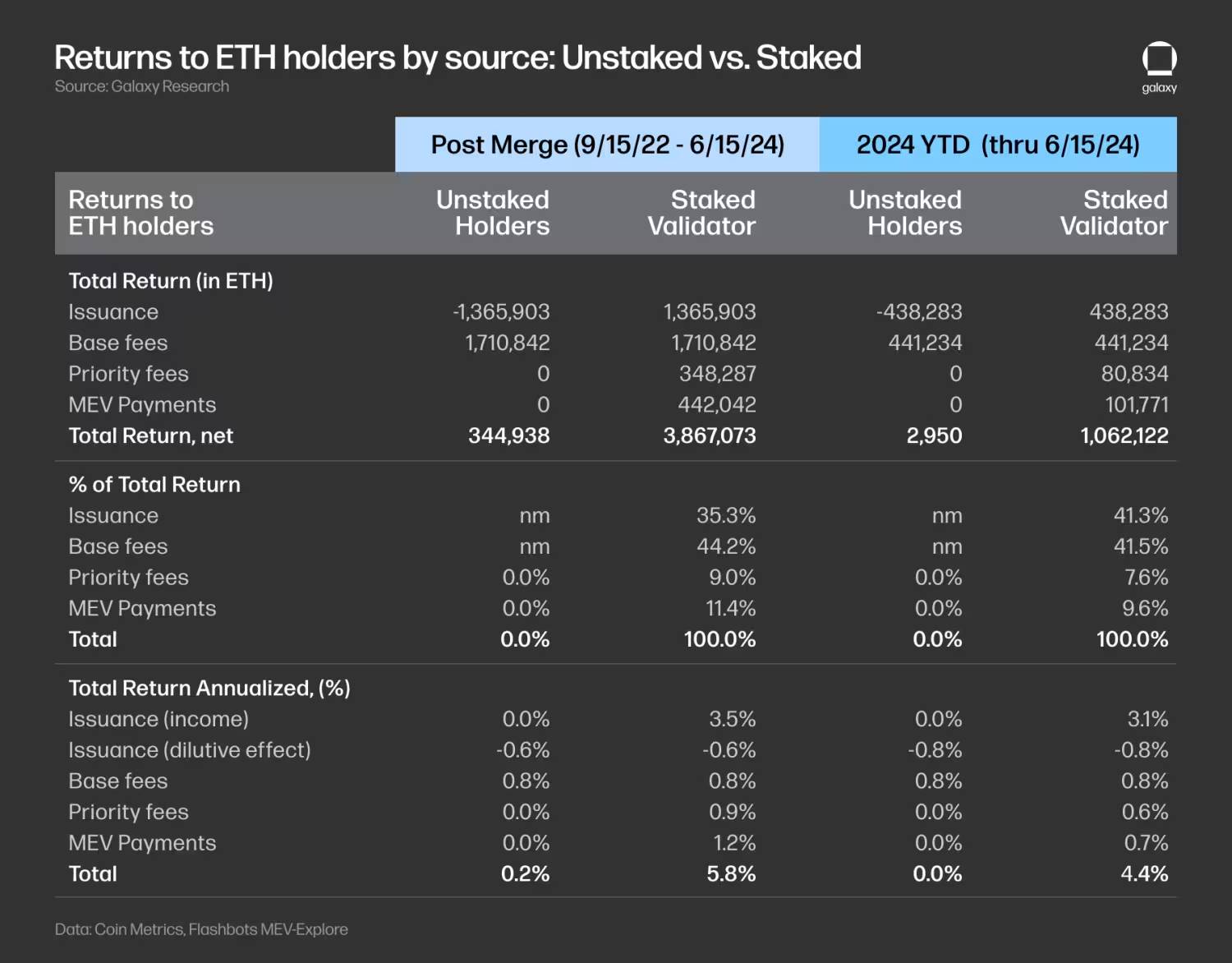

Due to the lack of staking rewards, the demand for spot Ethereum ETFs may be limited. Unstaked ETH forgoes the following opportunity costs:

(i) inflationary rewards paid to validators (which also has a negative dilution effect),

(ii) Priority fees paid to validators, and MEV revenue paid to validators via relayers. Using consolidated data (>September 15, 2022) through June 15, 2024, we estimate the annual opportunity cost of forgoing staking rewards to be 5.6ppt, a non-trivial difference for spot ETH holders (or 4.4ppt using year-to-date data). This would make a spot Ethereum ETF less attractive to potential buyers. Note that ETPs offered outside the US (e.g., Canada) offer holders additional yield via staking.

Grayscale 的 ETHE 可能會拖累以太坊 ETF 的流入。 Just as the GBTC Grayscale Trust experienced significant outflows when it converted to an ETF, the ETHE Grayscale Trust conversion to an ETF would similarly result in outflows. Assuming ETHE’s outflow rate matches that of GBTC in the first 150 days (i.e., 54.2% of the trust supply was withdrawn), we estimate ETHE’s monthly outflows to be around 319k ETH, which at current prices of around $3,400 would be $1.1 billion or an average daily outflow of $36 million. Note that the supply held by these trusts represents 3.2% of BTC supply and 2.4% of ETH supply, suggesting that the ETHE ETF conversion would be relatively less of a drag on ETH prices than the GBTC conversion. Additionally, unlike GBTC, ETHE does not face forced sellers due to bankruptcy (e.g., 3AC or Genesis), which would further support the view that the ETH-related Grayscale trusts would experience relatively less selling pressure.

Basis trading may have driven hedge fund demand for Bitcoin ETFs. Hedge funds want to arbitrage the difference between Bitcoin spot and futures prices, and basis trading is likely to drive hedge fund adoption of ETFs. As mentioned earlier, 13 F filings show that as of 3/31/24, more than 900 US investment companies hold Bitcoin ETFs, including some well-known hedge funds such as Millennium and Schonfeld. Throughout 2024, ETHs funding rate on exchanges averaged higher than BTC, indicating that: (i) there is relatively greater demand to go long ETH; and (ii) a spot Ethereum ETF has the potential to attract greater demand from hedge funds that want to enter basis trading.

Since our estimated market capitalization for Ethereum ETF inflows is roughly comparable to that of BTC inflows, we would expect the price impact to be roughly the same for Ethereum, all else being equal. However, there are some key differences in the supply and demand of the two assets that could make Ether more price sensitive to ETF flows:

Supply from exchanges : Currently, exchanges hold a higher percentage of BTC supply than ETH supply (11.7% vs. 10.3%), suggesting that ETH supply may be tighter, and assuming inflows are proportional to market cap, ETH’s price will be more sensitive (Note: this metric relies heavily on exchange address attribution, and data from different data providers vary greatly).

Inflation and Destruction : Following the latest halving on 4/20/24, Bitcoins annual inflation rate is about 0.8%. After the merger (> 9/15/22), Ethereums net issuance is negative (-0.19% annual issuance) because the new issuance paid to depositors (+0.63%) is more than offset by the base fee destroyed (-0.83%). In the past month, ETH base fees were relatively low (-0.34% annualized) and failed to offset new issuance (+0.76% annualized), resulting in an annualized net positive inflation rate of +0.42%.

Supply held in ETFs : Since launch, the net amount of BTC entering US spot ETFs to date (excluding GBTCs starting balance) has totaled 251k BTC, or 1.3% of current supply. If this rate is calculated annually, the ETF will absorb 583k BTC or 3.0% of BTCs current supply, which will far exceed the dilution of miner rewards (0.81% inflation rate).

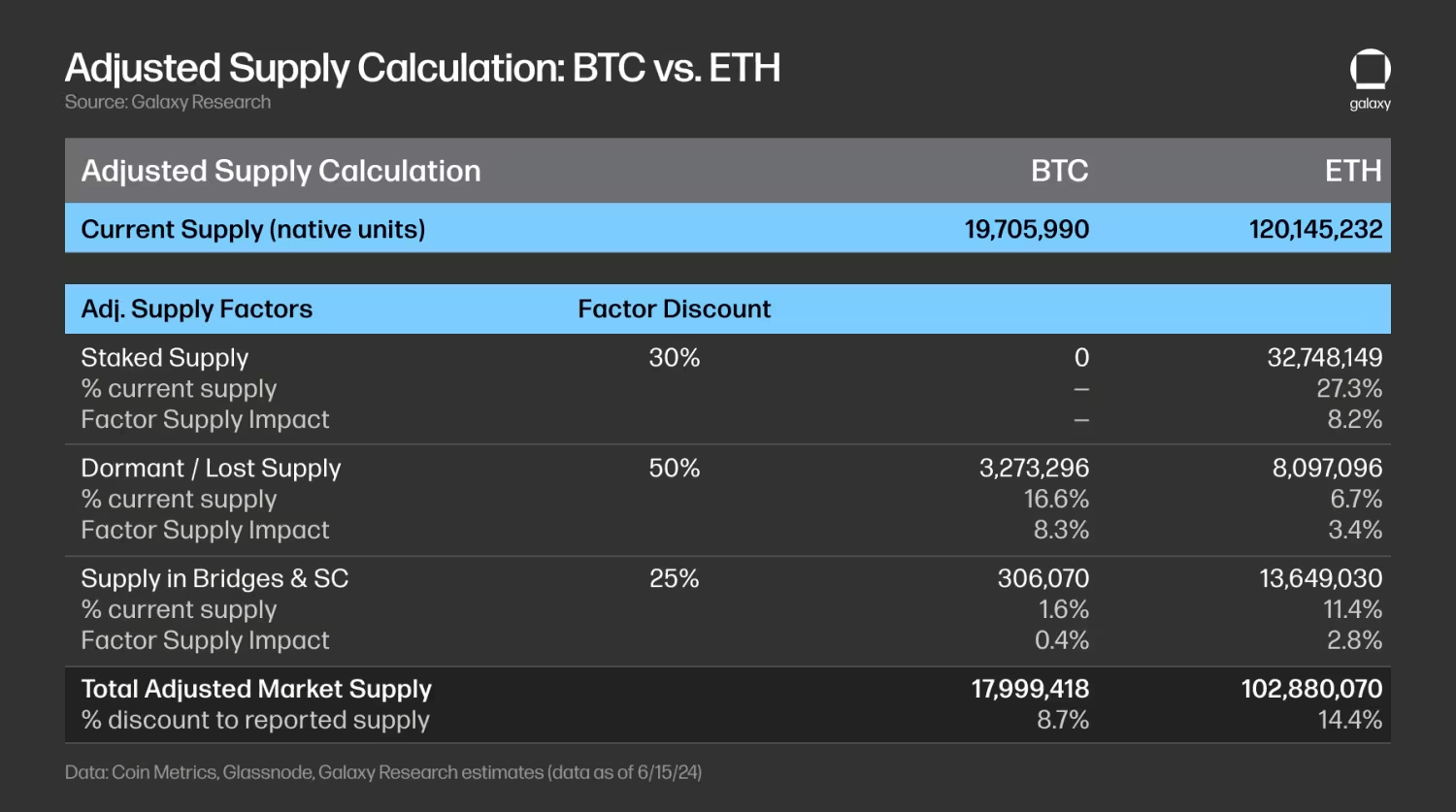

However, the actual market liquidity available for ETF purchases is far less than the reported current supply. We believe that to better reflect the available market supply of each asset in the ETF, adjustments must be made for various factors such as staked supply, dormant/lost supply, and supply held in bridges and smart contracts:

Staked Supply (Discount: 30%): Staked ETH reduces liquidity on the market. Currently, there is no staking option for BTC. Staked ETH is used to secure the network, but stakers can unstake some of the ETH for other purposes. Currently, staked ETH accounts for about 27% of the total supply, and we apply a 30% discount to estimate the supply available on the market, resulting in a supply discount of 8.2%.

Dormant/Lost Supply (Discount: 50%): Some BTC and ETH are considered irrecoverable (e.g. lost keys), which reduces the supply on the market; we use BTC that has not moved for more than 10 years and ETH that has been last active for more than 7 years, which account for 16.6% and 6.7% of the current supply respectively. We apply a 50% discount to these supplies because the supply in these assumed dormant addresses may come back online at any time.

Supply in bridges and smart contracts (discount: 25%): This supply is locked in bridges and smart contracts for productive purposes. For Bitcoin, there are ~153k BTC in BitGo-custodied wrapped BTC (wBTC), and we estimate that approximately the same amount of BTC is locked in other bridges, totaling ~1.6% of supply. ETH locked in smart contracts accounts for ~11.4% of current supply. We apply a 25% discount to these supplies because we believe these supplies are more liquid than staked supply (i.e., less likely to be subject to the same lockup requirements and withdrawal queues).

After applying the discounted weights of these factors to calculate the adjusted BTC and ETH supply, we estimate that the available supply of BTC and ETH is 8.7% and 14.4% less than the reported current supply, respectively.

全面的, ETH’s price sensitivity should be higher relative to BTC due to : (i) lower available market supply based on adjusted supply factors, (ii) lower proportion of supply on exchanges, and (iii) lower net issuance. Each of these factors should have a multiplicative effect on price sensitivity (rather than additive), as prices tend to be more responsive to changes in market supply and liquidity.

Looking ahead, we have several questions regarding adoption and secondary effects:

How should product managers and allocators think about BTC and ETH? Will existing holders move from Bitcoin ETFs to ETH? For allocators, some rebalancing is expected. Will a spot ether ETF attract new marginal buyers who havent bought BTC yet? What will be the proportion of potential buyers holding BTC only, ETH only, or a mix of both?

When (if ever) will staking be added? Will the absence of staking rewards impact the adoption of spot ether ETFs? Will the demand for investment in DeFi, tokenization, NFTs, and other crypto-related applications drive greater adoption of ether ETFs compared to Bitcoin given the lack of alternative investment products?

What is the potential impact on other alternatives? After Ethereum, are we more likely to see other alternative ETFs approved?

Overall, we believe the potential launch of a spot Ether ETF should have a positive impact on market adoption of Ethereum and the broader crypto market for two main reasons: (i) expanded accessibility across the wealth segment, and (ii) greater acceptance through formal recognition by regulators and trusted financial services brands. ETFs are able to provide greater coverage for both retail and institutions, provide broader allocations through more investment channels, and can support Ethers use in portfolios for more investment strategies. Additionally, greater understanding of Ethereum among financial professionals would ideally lead to accelerated investment and adoption of the technology.

This article is sourced from the internet: Galaxy Research Report: ETH ETF net inflows are expected to be $1 billion per month

相關:下週必看| Blast即將空投;季度選擇權交割可能影響短期市場(6月24日-6月3日)

下週亮點 io.net:IO Workers 每日區塊獎勵將於 6 月 25 日開始。爆料:6月26日開始空投; Blur 第 3 季將於 6 月 26 日進行 Blast 空投; Optimism將於6月27日推出OP治理第6季;下週五,本季選擇權結算:總計66.5億持股的BTC選擇權到期,總計35.6億持股的ETH選擇權到期; LayerZero CEO:最終女巫名單最晚將於下周公布。 6月24日至6月30日,業界更多值得關注的事件預覽如下。 6月24日 Upbit計劃於6月24日維護質押服務系統,預計將持續...