My XP

0

Đăng nhập

Original author: Cosmo Jiang, Erik Lowe

Original translation: 0x js@Golden Finance

As we approach the mid-year mark, we wanted to take a moment to share our thoughts on the pace of the market so far this year. After a rapid rise at the beginning of the year, digital asset prices retreated in the second quarter. Every period of strong performance is followed by a period of consolidation. Inevitably, during this period, some people will throw in the towel and start calling for the end of the cycle, especially in an asset class that is more volatile than most. While digital asset prices have seen some recovery in July, we wanted to provide our thoughts on what happened and why we remain bullish on the future.

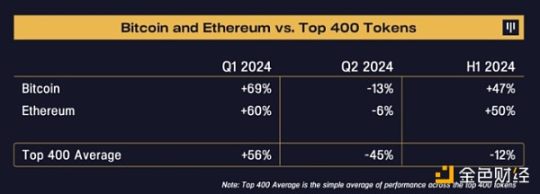

Following the broad market gains in Q1, the top 400 tokens lost an average of 45% in Q2 and were down 12% year-over-year as of June 30.

Below we point out several macro-related and crypto-specific reasons for this decline.

The main macro headwind in early April was that the market began to re-price a scenario of higher long-term interest rates, as the economy remained strong and inflation was high, in stark contrast to the previous view that rates would quickly move downward. In crypto, the market was dragged down mainly by concerns about excess supply. For Bitcoin, the German government began to liquidate its $3 billion position and the $9 billion Mt.Gox distribution schedule was confirmed. Long-tail tokens face supply resistance, which comes from both the increase in new token issuance, investor distraction and limited capital, as well as private investors who have continued to profit from newly issued tokens over the past year. In addition, the SECs investigation into Consensys and Uniswap has brought some uncertainty to certain protocols.

Overall, breadth has been narrow, with the crypto space as a whole significantly underperforming Bitcoin and Ethereum so far this year, similar to the dynamics of the stock market this year, with the big seven holdings holding up against the rest. To help illustrate this, we’ve included below the distribution of returns for the top 400 tokens by market cap this year.

It’s been a one-size-fits-all period for the long-tail tokens. We say this because the sell-off was widespread — nearly 95% of tokens underperformed Bitcoin and Ethereum, and nearly 75% of tokens underperformed this year. By subcategory, Q2 performance was largely the same — nearly every major subcategory was down 40-50%.

We believe altcoins have underperformed for the following reasons:

1) Attention is mainly focused on Bitcoin and Ethereum due to approval from key regulators

2) New token issuance this year has diluted available capital and attention

3) The market is more cautious about private investors unlocking large amounts of tokens, which may increase selling pressure for the rest of the year

As often happens in underperforming markets, we are seeing token commoditization and a failure to adequately differentiate between protocols with stronger and weaker fundamentals. As investors, it is important that we do not fall into the same trap and generalize. As prices and sentiment begin to rebound, this phenomenon presents a great opportunity for token selection. We believe that as diversification increases, tokens with strong fundamentals and promising growth prospects will outperform. We have already seen evidence of this in early July.

Price and fundamentals – If we only look at price action, especially for the long tail of tokens, the market appears weak, with many tokens underperforming this year. However, this is in stark contrast to improving fundamentals, such as on-chain users and activity, both of which have clearly accelerated from the bear market lows of the past two years.

In addition, many green shoots of innovation have emerged in this cycle, such as AI-related blockchain protocols, decentralized physical infrastructure networks (DePIN), and decentralized social.

We think everything is actually much cheaper now, in terms of price versus fundamentals, than at any time during the recovery.

Regulatory Shift – One of the biggest obstacles to the growth of the crypto industry has been the negative attitude of regulation in the U.S. We are now seeing a 180-degree shift in real time.

Trump turned in support of cryptocurrencies in early May, followed by legislative developments such as FIT 21 and the approval of an Ethereum ETF.

It is very good for our industry that prominent politicians are openly supporting cryptocurrencies. We believe they realize that supporting cryptocurrencies is the same as supporting innovation, and being against innovation does not win votes and may even be anti-American. Polls show that the likelihood of pro-cryptocurrency regulators and authorities increases after the November election.

As far as tokens go, we are optimistic that shifting political and regulatory stances towards cryptocurrencies will begin to drive positive change. To date, regulatory clarity has led to unfortunate volatility in the cryptocurrency space. Currently, a token is legal if it clearly has no value, but illegal if it creates value and attempts to return that value to token holders. This creates completely the wrong incentives, attracting bad actors and discouraging good actors. With regulatory clarity, we believe we are headed in the right direction to correct this, and tokens with real value pegged to strong fundamentals will stand out, while those without real value will not be rewarded. In fact, the FIT 21 bill recently passed by the House of Representatives begins to lay the foundation for this kind of sensible regulation.

We believe this paves the way for innovation and blockchain to flourish and continue to grow in the United States.

Position and Sentiment – The technical indicators we observe describe the current position as “very clean” i.e. “good entry point”.

A lot of leverage has been flushed out of the system, judging by futures open interest. Many altcoins are back to their lows of September 2023 before this rally began. The Crypto Fear and Greed Index as measured by CoinGlass just hit its lowest level since the depths of the bear market in December 2022, just after the FTX crash. The sentiment is just as fearful now as it was then.

Based on these indicators, we believe todays position and entry point are attractive.

Macro – Recent macroeconomic indicators show that inflation is finally cooling, which signals the Fed to start cutting interest rates. CPI deflation in June was -0.1% month-on-month, the first time since 2020. Although the unemployment rate rose slightly to 4.1%, it is still at a stable level.

The rhetoric from Powell and several of the more dovish Fed members suggests that rate cuts may be closer than most on Wall Street realize, and rate hikes may well be off the table. That’s a big deal.

The shift in Fed policy from restrictive to supportive rates is very favorable for high-growth early-stage technologies such as cryptocurrencies. There is a lot of capital on the sidelines. Money market fund assets reached $6 trillion, a record high. As interest rates are expected to fall later this year and money market fund yields fall, we believe capital will return to high-growth assets.

Our thesis is that protocol tokens with product-market fit and strong unit economics that generate real revenue and have strong unit economics will perform best in this cycle. We have previously described how these tokens outperformed other tokens in the second phase of the bull cycle when market breadth expanded from the major tokens.

Looking back, we observe that historically there are two distinct phases in bull cycles. The first phase is the early stages of the rally, where Bitcoin tends to outperform the rest of the market. The second phase is the late stages, where altcoins tend to outperform the rest of the market. The chart below highlights these phases, showing how Bitcoin grew relative to altcoins during each phase, and how altcoins performed throughout the bull cycle, with most of the gains occurring in the second phase.

We believe we are entering Phase 2. Historically, Bitcoin dominance has increased by 15-20 percentage points in the first phase of each previous cycle, and at this stage of the cycle, it has increased by 17 percentage points. We believe we are closer to the end of Bitcoin dominance than the beginning, and the next phase will be meaningful outperformance by fundamentally sound tokens.

This article is sourced from the internet: Pantera: We are entering the second phase of the bull market

Original author: @Web3 Mario (https://x.com/web3_mario) Abstract: I have been learning the relevant technologies for TON DApp development recently, and trying to think about some product design logic. As TON becomes more popular, some AMA, roundtable discussions and other activities have become more and more. I have also participated in some of them and found some interesting things that I hope to share with you. Let me first talk about the conclusion. In general, I found that the official ecological construction ideas of TON are different from traditional execution layer projects, that is, the so-called public chains. It seems to choose traffic-driven rather than asset-driven. This brings a new requirement to developers. If you want to get official endorsement, or more directly become a project that the official prefers, the core…