My XP

0

Login

Original author: Will Awang

Investment and financing lawyer, Digital Assets Web3; independent researcher, tokenization RWA payment.

At the beginning of 2024, Cathie Wood, the most shining Wall Street investment manager of technology stocks, led her ARK team to release the Big Ideas 2024 report. The report aims to cover the field of disruptive innovation around the world, has extremely high gold content, and is an important reference for global technology entrepreneurs and investors.

This article extracts content related to cryptocurrency and blockchain from two research reports in 2023/4 and presents a way of looking at Crypto from the perspective of Wall Street funds.

Among them, we can see the changes that public blockchain can bring to currency, finance, and the Internet, the solutions that smart contracts/DeFi provide for the real world, and the value growth rate brought by digital wallets combining crypto/blockchain payment capabilities.

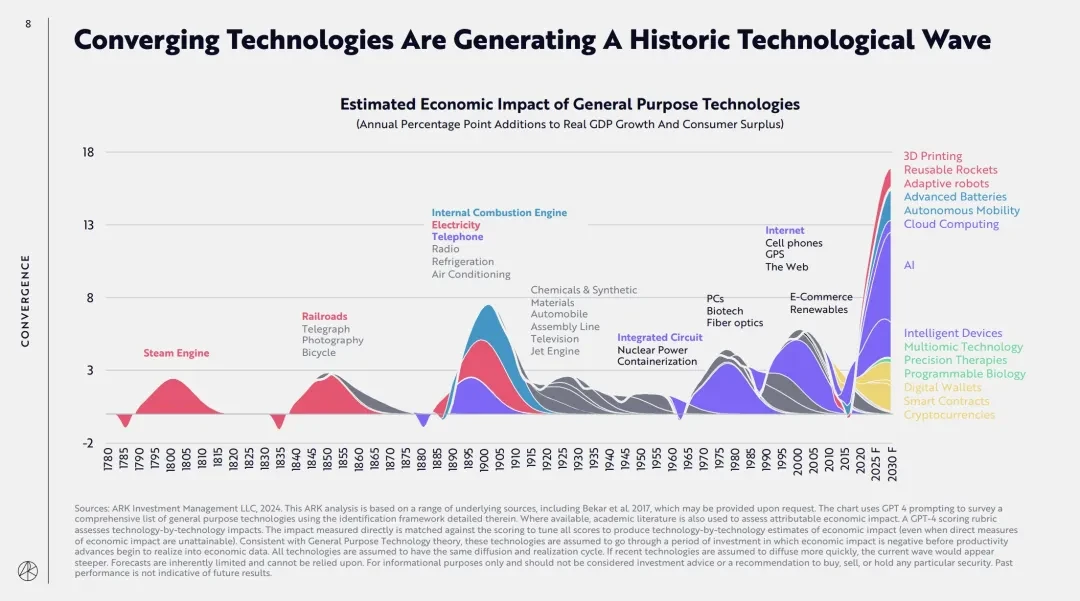

ARK research report believes that the integration of disruptive innovative technologies will define the development of the next decade, and the current technological integration may trigger more profound macroeconomic changes than the first and second industrial revolutions.

AI, public blockchain, multi-omics sequencing, energy storage and robotics, these five major technology platforms are converging with each other, which will change global economic activities, and the economic growth rate may accelerate from the average 3% in the past 125 years to 7% in the next 7 years.

The figure below shows the impact of previous technological revolutions such as steam engines, railways and telegraphs, and general technological revolutions such as electricity, telephones and radio on the economy. Today, with the integration of disruptive technologies such as AI, public blockchain, multi-omics sequencing, energy storage and robotics, the impact on the economy may exceed that of the past.

As one of the five major technologies, once mass adoption is achieved, all currencies and contracts will migrate to the public blockchain, supporting the verification of digital rights and proof of ownership. The financial ecosystem may be reconfigured to adapt to the rise of cryptocurrencies and smart contracts/decentralized finance (DeFi).

These technologies increase transparency, reduce the impact of capital and regulatory controls, and lower the cost of contract execution. In such a world, as more and more assets are monetized/tokenized, businesses and consumers gradually adapt to the new financial infrastructure. Digital wallets that carry these assets will become increasingly important. The governance structure of traditional companies will also be challenged.

2. Changes that public blockchain can bring

The proposal for public blockchain was mainly made in the 2023 research report. ARK stated that despite the major earthquake in the crypto industry in 2022, public blockchain continues to promote changes in currency, finance and the Internet. The long-term opportunities for Bitcoin, DeFi and Web3 are increasing. In the next decade, the market value of cryptocurrencies and smart contracts may reach 20 trillion US dollars and 5 trillion US dollars respectively.

Public blockchains can coordinate the transfer of value and ownership outside the top-down control of governments and centralized institutions, thereby promoting the transition of the monetary system from a centralized to a global, decentralized, and non-sovereign one.

Existing problems: The centralized monetary system can hardly provide strong guarantees for the global economy:

1) 4 billion people live under repressive regimes;

2) More than 2 billion people suffer from double-digit inflation;

3) More than 1 billion people cannot use traditional payment transfer applications;

4) More than 1 billion people rely on remittances.

The power of change comes mainly from cryptocurrencies represented by Bitcoin:

1) Bitcoin can ensure independent property rights, combining encryption technology and self-custody to ensure independent property rights;

2) Bitcoin is inflation-resistant. Its quantity is mathematically measured and predictable. Currently, the supply of Bitcoin is 19 million, with an upper limit of 21 million;

3) Bitcoin is censorship-resistant, and the threshold for transactions is very low. The only requirement is to have a private key;

4) Bitcoin is auditable and transparent.

Public blockchain can reconstruct a set of decentralized financial technology facilities (DeFi) outside the traditional financial system to meet many needs that the traditional financial system cannot meet and solve many problems that the traditional financial system is difficult to solve.

Existing Problems:

1) More than 2 billion people lack access to basic banking services, including account management and credit;

2) The opacity of the financial system has caused many financial crises;

3) The risks of traditional financial institutions acting as counterparties can easily lead to single point failures in the system, and centralized decision-making leads to rampant rent-seeking.

The power of change mainly comes from the newly constructed decentralized financial infrastructure (DeFi):

1) DeFi eliminates traditional intermediaries, and automatic smart contracts guarantee execution without the need for trusted entities;

2) DeFi is global, and financial services deployed on open protocols enable anyone with an internet connection to access custody, trading, and lending facilities;

3) DeFi is interoperable, and financial services are open source and interoperable, allowing for rapid innovation and experimentation;

4) DeFi is auditable and transparent. Users manage their own risks. Collateral and capital flows are stored in the ledger and open to scrutiny.

Public blockchains can help realize personal sovereignty over identity, reputation, and data outside of traditional groups and large technology companies, and achieve the transition of property rights from corporate sovereignty to personal sovereignty.

Existing Problems:

1) The development of current Internet technology giants depends on utilizing, owning and monetizing user data;

2) Digital identities and reputations between platforms are not interoperable;

3) Centralized decision makers determine the discovery of information and subjectively regulate content and communication.

The power of change mainly comes from the value economic system of Web3:

1) Web3 emphasizes personal sovereignty and introduces the concept of personal digital property rights;

2) Web3 relies on protocols, not platforms. Decentralized protocols support the management and open access to distributed data, limiting the control of central aggregators;

3) Web3 brings a new profit model, which embeds the economic system into the ecosystem, enabling users to monetize and participate in network development;

4) Web3 realizes the integration of consumption and investment. With the digitalization of the economy, consumer behavior is also changing, giving rise to new business models for purchasing, owning and using.

This public blockchain that combines Bitcoin/cryptocurrency network, DeFi, and Web3 will further redefine traditional assets and will be able to achieve a total market value of US$25 trillion by 2030 (including US$20 trillion in crypto asset value and US$5 trillion in smart contracts/DeFi protocol value).

3. Smart Contracts – Driving the Financial and Internet Revolution

In the wake of the catastrophic failures of 22/23 centralized crypto institutions, smart contracts deployed on public blockchains offer a global, automated, and auditable decentralized financial infrastructure (DeFi) alternative to the traditional financial system.

Decentralization has proven to be even more important to maintaining the original value proposition of public blockchain infrastructure.

According to ARKs research, as tokenized financial assets have gradually attracted attention (such as stablecoins, tokenized U.S. Treasury bonds, etc.), the size of their on-chain assets has achieved a significant growth. It is expected that the market value related to decentralized applications will grow at an annual rate of 32%, from US$775 billion in 2023 to US$5.2 trillion in 2030.

The following are the main points:

Still in its infancy, smart contracts are powering a new financial system native to the internet. Driven by Ethereum, the largest smart contract blockchain, multiple networks are supporting on-chain activity and competing for market share.

Given the rise in hyperinflation in emerging markets and global instability, the demand for stablecoins that provide digital access to the U.S. dollar is soaring. Over the past three years, the number of daily active stablecoin addresses worldwide has grown by 93% per year, from 171,000 to 1.2 million. In 2023, stablecoin transaction volume exceeded Mastercard.

Tokenization enables asset management on public blockchains, making it easier to verify, track, trade, and utilize funds than in traditional financial markets. In 2023, tokenized Treasury funds grew more than sevenfold to $850 million. Early funds were launched on the Stellar blockchain, but Ethereum became the largest tokenized Treasury market in 2023.

Faced with the 2022 crisis and its aftermath, core developers proposed a technical roadmap and protocol enhancements to support the next bull run. Ethereum successfully achieved Proof of Stake (PoS) consensus, and Solana also set a new record for continuous uptime.

Since the beginning of 2021, more than 20 Layer 2 projects have been launched, enabling Ethereum to quadruple the average daily transaction size with lower fees. Despite early success, most Layer 2s are centrally controlled. The proliferation of Layer 2s has created a mixed experience for users and developers.

As transaction costs have fallen, on-chain participation (measured by the ratio of daily active addresses (DAU) to monthly active addresses (MAU)) has increased.

There are trade-offs in the design of smart contract network functions. By prioritizing underlying decentralization, the Ethereum ecosystem becomes more complex as it scales. By prioritizing single-layer scalability, Solana maintains a simple architecture for users and application developers and has achieved phased success.

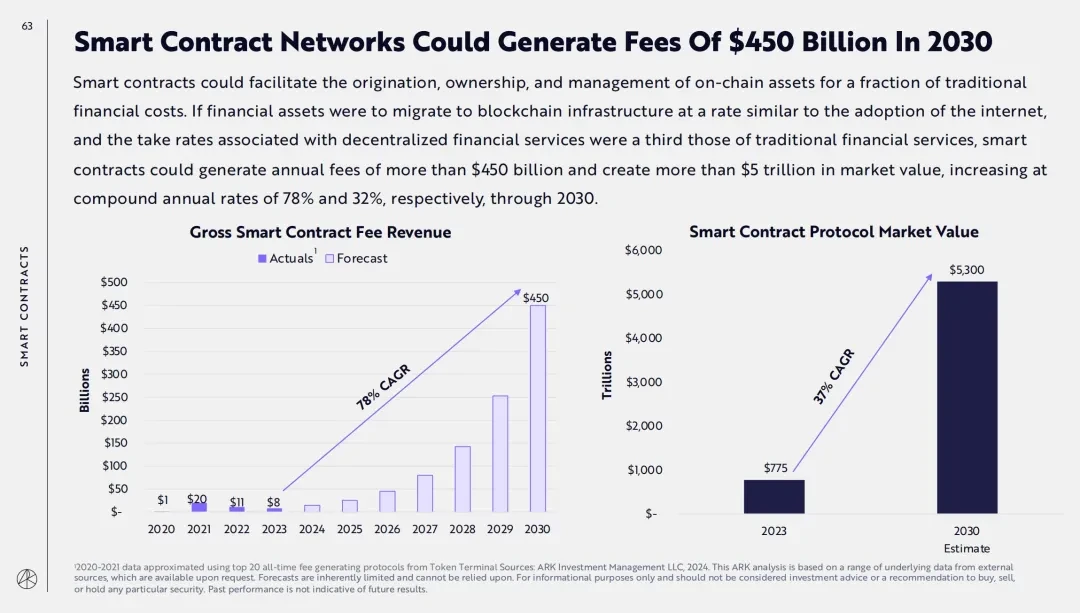

The value of global financial assets has surged from $140 trillion in 2000 to $510 trillion in 2020, a combination of global economic growth, increased financialization, and expanded equity multiples. The operating costs of the global financial system have increased as the value of financial assets has increased. The financial services industry has total annual revenues of $20 trillion, or 3.3% of the value of all financial assets. Smart contracts can significantly reduce this drag on the global economy.

Smart contracts can facilitate the creation, ownership, and management of on-chain assets at a cost far lower than traditional finance. If tokenized assets migrate to blockchain infrastructure at a speed similar to the adoption of the Internet, and the service fees associated with DeFi are one-third of those of traditional financial services, smart contracts can generate more than $450 billion in service fees and create more than $5 trillion in market value each year, growing at a compound annual growth rate of 78% and 32% respectively by 2030.

As ARK mentioned in its 2023 research report, public blockchain can transform the existing system at three levels: currency, finance, and the Internet. One of the solutions is smart contracts/DeFi. So who will carry these tokenized assets on the public blockchain? Digital wallets must be mentioned.

Interestingly, the digital wallets in ARK’s research report are not the same as the crypto wallets based on the public blockchain , although some of the improved growth points in the digital wallets mentioned below can be fully achieved through Crypto/Blockchain Payment.

From ARKs perspective, digital wallets use Blockchain to transform the traditional payment system (both internal and external) to achieve cost reduction and efficiency improvement (closed-loop payment ecosystem), and combine the huge consumer/merchant dividends that digital wallets have accumulated before, so that the value is reflected in the main company of the digital wallet.

Digital wallets have attracted billions of consumers and millions of merchants, and currently have 3.2 billion users, covering 40% of the worlds population. As consumers and merchants gradually adopt digital wallets, the use of traditional checking accounts, credit cards, debit cards and direct merchant accounts will decline.

Digital wallets can fundamentally change the nature of traditional payment transactions – eliminating financial intermediaries.

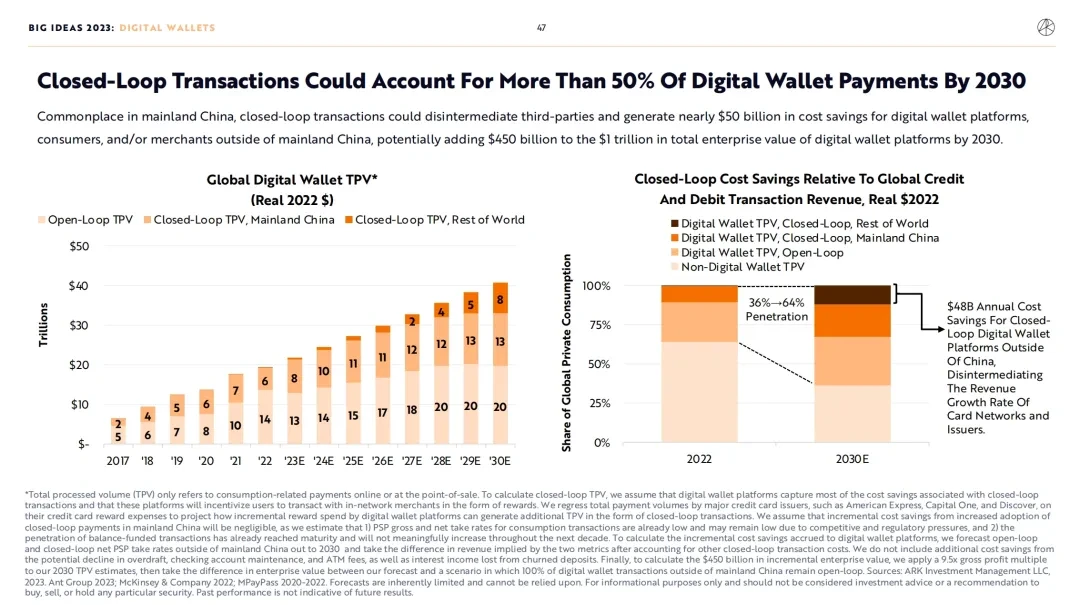

Digital wallets can provide a closed loop for more than 50% of payment transactions, which will save the market nearly $50 billion in costs. By 2030, the value of digital wallet companies may increase by an additional $450 billion from the current $1 trillion. ARK research shows that the number of digital wallet users will grow at an average annual rate of 8%, covering 65% of the worlds population by 2030.

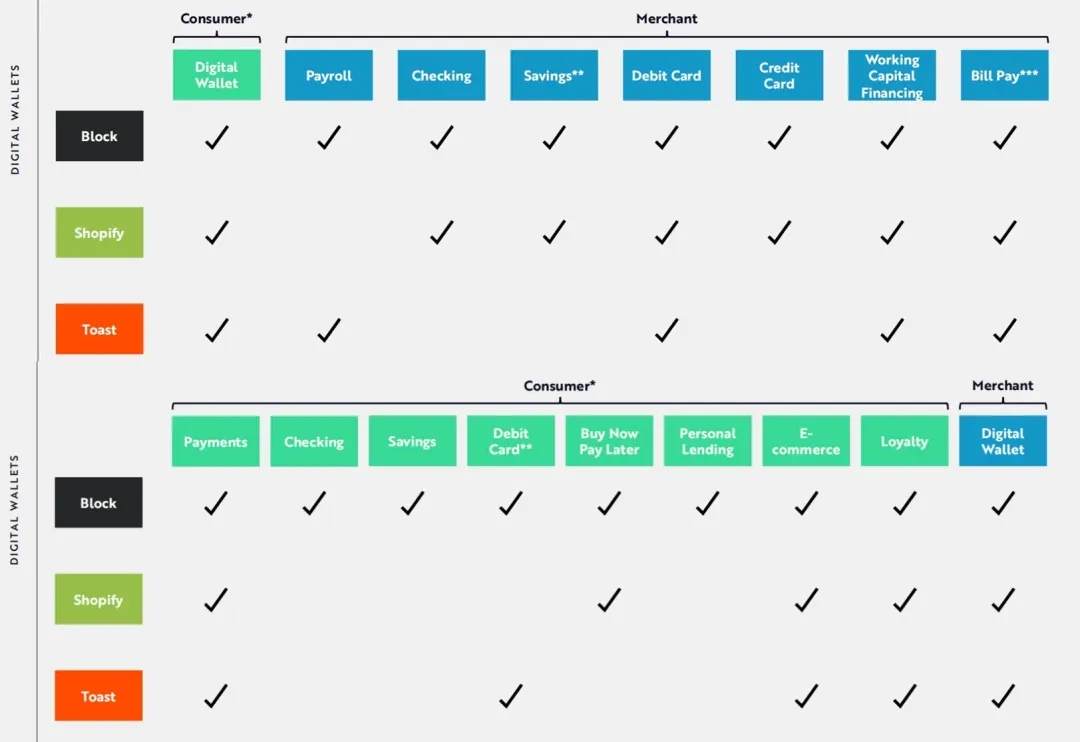

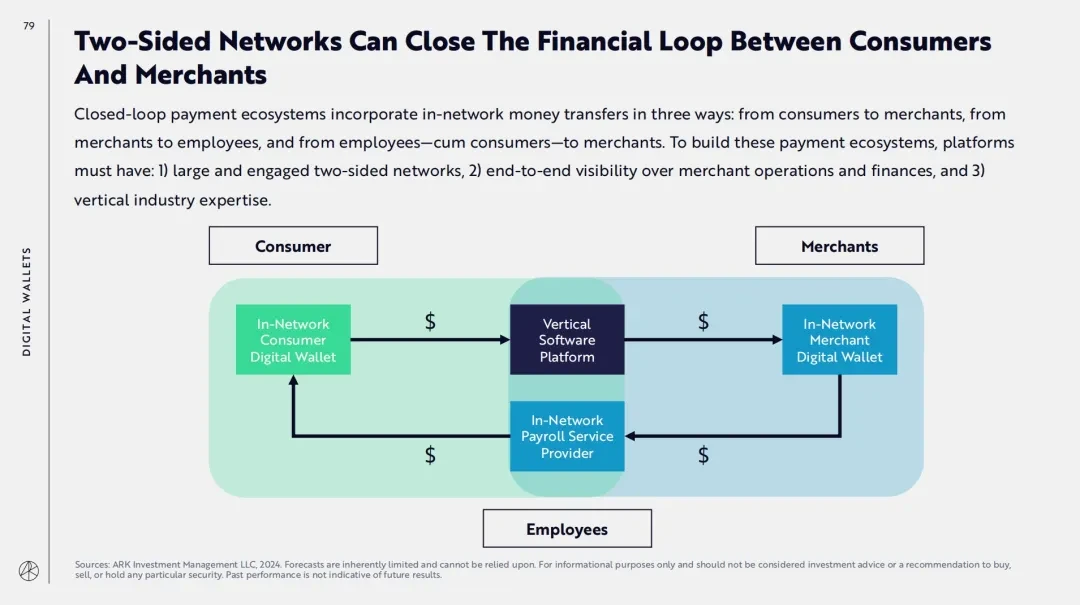

Vertical software applications are a set of solutions tailored to specific industry needs, such as Block, Shopify and Toast. The leading vertical software applications are rapidly expanding to financial services on both the consumer and merchant ends. Through a two-way network, this software can facilitate closed-loop transactions from consumers to merchants, merchants to employees, and employees to merchants.

ARK believes that digital wallets on these applications will enable a completely closed payment ecosystem. According to ARKs research, revenue from closed-loop consumer payments, commercial banking, and employee wages/payments will grow at an annual rate of 22%-33% over the next seven years, from $7 billion in 2023 to $27-50 billion in 2030.

The following are the main points:

Block, Shopify and Toast are all very attractive platforms that are likely to use digital wallets as the core of their ecosystems connecting consumers, merchants and employees. In addition to supporting core business operations, they use digital wallets as the core, work with partner banks and fintech companies, or activate their own banking licenses, thereby eliminating the inefficient traditional financial institutions in the interaction with countless merchants.

At the same time, vertical software applications can not only realize a huge back-end business network, but also build a front-end consumer network through digital wallets. By expanding both business and consumer networks at the same time, vertical software applications are closing the loop and becoming the operating system of these two-sided networks.

Closed-loop payment ecosystems combine the movement of funds within a network in three ways: from consumers to merchants, from merchants to employees, and from employees and consumers to merchants. To build these payment ecosystems, platforms must have: 1) a large and active two-sided network; 2) end-to-end visibility into merchant operations and finances; and 3) vertical industry expertise.

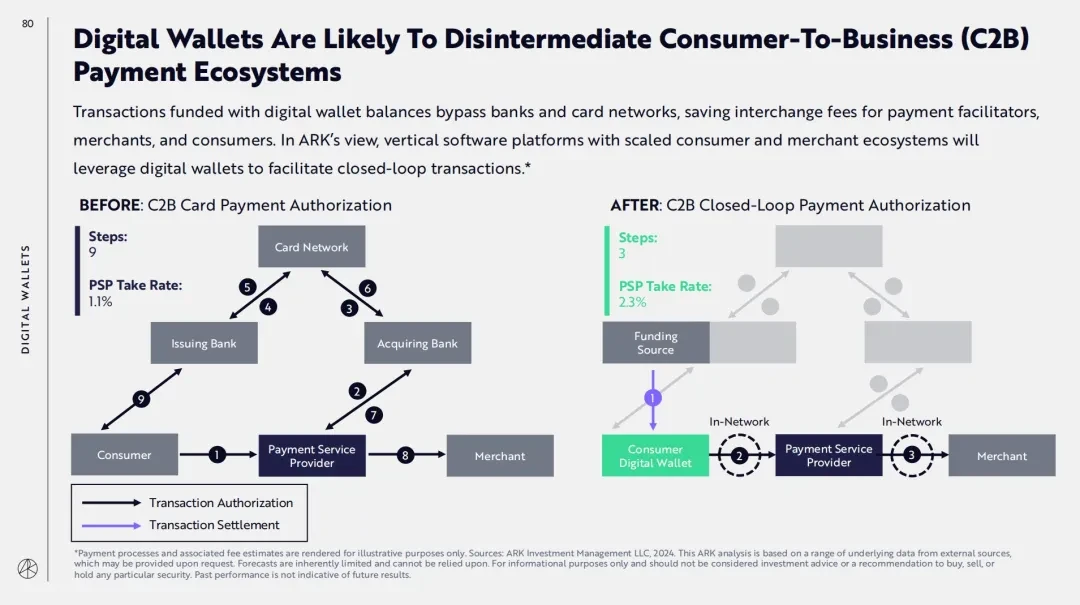

Transactions using digital wallet balances bypass banks and bank card networks, saving transaction fees for payment service providers, merchants, and consumers. In ARKs view, vertical software platforms with large-scale consumer and merchant ecosystems can better utilize digital wallets to facilitate closed-loop transactions and achieve maximum benefits.

Block paid about 60% of customer transaction fees to third parties for interchange, assessment, processing, and bank settlement fees in 2022. Block’s net fee rate could more than double if Cash App, Block’s front-end consumer app, enables users to use their balances to transact with Block merchants.

Closed-loop payment ecosystems are commonplace in mainland China, eliminating third-party intermediaries and saving digital wallet platforms, consumers and/or merchants outside of mainland China nearly $50 billion in costs. By 2030, the total enterprise value of digital wallet platforms may increase by $450 billion.

In addition, in the 2024 report, ARK specifically added financial services for merchants and salary/payment services for merchant employees to the closed-loop payment ecosystem.

According to ARK research, the core revenues of Block Square, Shopify, and Toast will grow 22% annually over the next seven years, from $7 billion in 2023 to $27 billion in 2030. By 2030, closed-loop payment businesses consisting of consumer payments, merchant financial services, and employee wages/payments will generate an additional $23 billion in revenue, increasing the annual revenue growth rate from 22% to 33%.

While the public blockchain industry will not have an “iPhone” moment like AI, its impact on transforming traditional architectures (especially traditional financial architectures) will be profound, although this is a long-term path for change.

This path will start with financial payments, and the most direct or most capable of capturing value is payment companies.

From the perspective of Wall Street funds, digital wallet companies that currently have huge consumer/merchant relationships on both ends, after combining the capabilities of crypto/blockchain payment, can transform the traditional payment system through stablecoins or internal settlement networks, which can bring huge value growth to the company and be reflected in the companys stock price.

This is the most direct way for Wall Street funds to capture value, and it is also the path for crypto to achieve Mass Adoption with the help of the off-chain world. This can be seen from Paypals strategy of launching stablecoins on Solana.

This article is sourced from the internet: Interpretation of ARK Big Ideas 2023/4 report: What does Wood think of Crypto?

Compiled edited by TechFlow Participants: Ahmed Shadid, Founder and CEO of io.net; Tory Green, Founder and COO of io.net; Aline Almeida, SVP of Engineering of io.net; Mahar Jilani, Chief Experience Officer of io.net; Gauvrav Sharma, CTO of io.net; Basen Oubah, Co-founder and CoS of io.net; Hashim Alnabulsi, Managing Partner of IO.VENTURES Guests: Avery Ching, Co-founder and CT of Aptos Labs; Toly Yakovenko, Co-founder of Solana; Lily Liu, Chairman of Solana Foundation; Hidde Hoogland, CEO of DCENT Podcast source: io.net Original title: IO Summit 2024 Keynote Air Date: June 4, 2024 Summary of key points At the 2024 IO Summit, io.net announced three major breakthroughs, launched the worlds largest AI computing network IOG (Internet of GPUs), and demonstrated cooperation with Aptos and Solana. These innovations will revolutionize the future of AI,…