ایک مضمون ان خطرات کا جائزہ لیتا ہے جن پر فیڈ سود کی شرح میں کمی کے ابتدائی مرحلے میں توجہ دینے کی ضرورت ہے۔

اصل مصنف: Web3 Mario (https://x.com/web3_mario)

Abstract: On August 23, 2024, Federal Reserve Chairman Powell officially announced at the Jackson Hole Global Central Bank Annual Meeting that Now is the time for policy adjustments. The direction of progress is clear, and the timing and pace of interest rate cuts will depend on upcoming data, changing prospects, and the balance of risks. This also means that the Feds tightening cycle, which has lasted for nearly 3 years, has ushered in a turning point. If the macro data is not unexpected, the first interest rate cut will be ushered in at the interest rate meeting on September 19. However, at the beginning of the interest rate cut cycle, it does not mean that the surge is coming immediately. There are still some risks that deserve everyones vigilance. Therefore, the author summarizes some of the most important issues that need to be paid attention to here, hoping to help everyone avoid some risks. In general, in the early stage of interest rate cuts, we also need to pay attention to six core issues, including the risk of recession in the United States, the rhythm of interest rate cuts, the Feds QT (quantitative tightening) plan, the risk of renewed inflation, the efficiency of global central bank linkage, and US political risks.

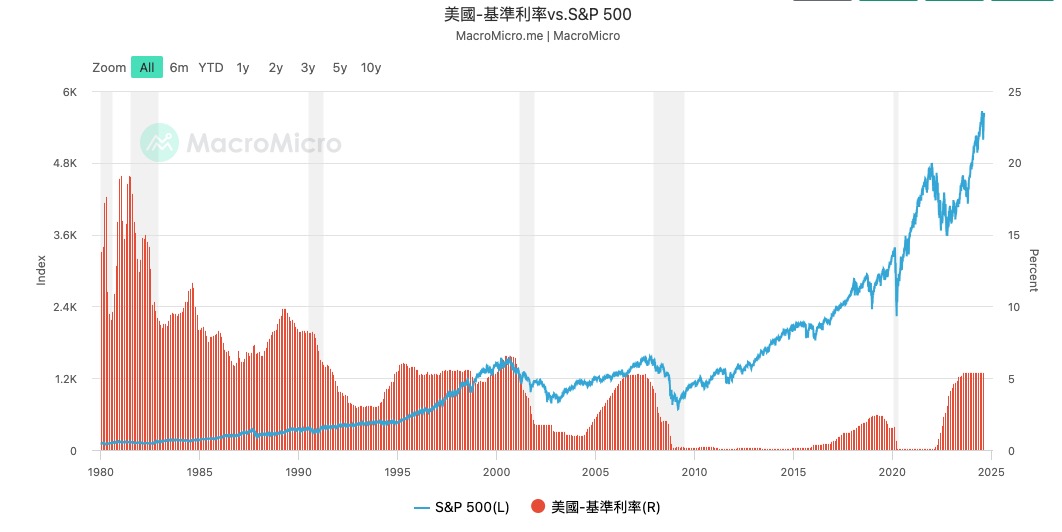

A rate cut does not necessarily mean an immediate rise in risk markets, on the contrary, it usually means a fall.

The Feds monetary policy adjustment has a profound impact on the global financial market. Especially in the early stage of interest rate cuts, although interest rate cuts are usually seen as measures to stimulate economic growth, they are also accompanied by a series of potential risks, which means that interest rate cuts do not necessarily mean an immediate rise in risk markets, but rather a decline in most cases. The reasons for this can usually be classified as follows:

1. Increased volatility in financial markets

Rate cuts are often viewed as a signal of support for the economy and markets, but in the early stages of a rate cut, markets may experience increased uncertainty and volatility. Investors tend to interpret the Feds actions differently, and some may believe that rate cuts reflect concerns about an economic slowdown. This uncertainty can lead to larger swings in the stock and bond markets. For example, during the 2001 and 2007-2008 financial crises, the stock market experienced significant declines even though the Fed began a rate cut cycle. This was because investors were concerned that the severity of the economic slowdown outweighed the positive effects of rate cuts.

2. Inflation risk

Lowering interest rates means lower borrowing costs, encouraging consumption and investment. However, if rate cuts are excessive or last too long, they can lead to rising inflationary pressures. When ample liquidity in the economy chases limited goods and services, price levels can rise quickly, especially when supply chains are constrained or the economy is close to full employment. Historically, such as in the late 1970s, the Feds rate cuts led to the risk of soaring inflation, which necessitated more aggressive rate hikes to control inflation, triggering a recession.

3. Capital outflow and currency depreciation

The Feds rate cuts usually reduce the interest rate advantage of the US dollar, causing capital to flow from the US market to higher-yielding assets in other countries. This capital outflow will put pressure on the US dollar exchange rate, causing the dollar to depreciate. Although the depreciation of the US dollar can stimulate exports to a certain extent, it may also bring the risk of imported inflation, especially when raw materials and energy prices are high. In addition, capital outflows may also lead to financial instability in emerging market countries, especially those that rely on US dollar financing.

4. Financial system instability

Interest rate cuts are often used to ease economic pressure and support the financial system, but they can also encourage excessive risk-taking. When borrowing costs are low, financial institutions and investors may seek riskier investments to earn higher returns, leading to the formation of asset price bubbles. For example, after the tech bubble burst in 2001, the Federal Reserve cut interest rates sharply to support economic recovery, but this policy to some extent fueled the subsequent real estate market bubble, which ultimately led to the outbreak of the 2008 financial crisis.

5. The effectiveness of policy tools is limited

In the early stages of rate cuts, if the economy is already close to zero interest rates or in a low interest rate environment, the Feds policy tools may be limited. Over-reliance on rate cuts may not effectively stimulate economic growth, especially when interest rates are close to zero, which requires more unconventional monetary policy tools, such as quantitative easing (QE). In 2008 and 2020, the Fed had to use other policy tools to respond to economic downturns after cutting interest rates close to zero, which shows that in extreme cases, the effect of rate cuts is limited.

Lets look at historical data. With the end of the Cold War between the United States and the Soviet Union in the 1990s, the world entered a globalized political landscape dominated by the United States. Until now, the monetary policy of the Federal Reserve has reflected a certain degree of lag. At present, the confrontation between China and the United States is in full swing. The shattering of the old order has undoubtedly exacerbated the risk of policy uncertainty.

Inventory of the main risk points in the current market

Next, let us take stock of the main risk points in the current market, focusing on the risk of recession in the United States, the pace of interest rate cuts, the Federal Reserve鈥檚 QT (quantitative tightening) plan, the risk of renewed inflation, and the efficiency of global central bank linkage.

Risk 1: Risk of US economic recession

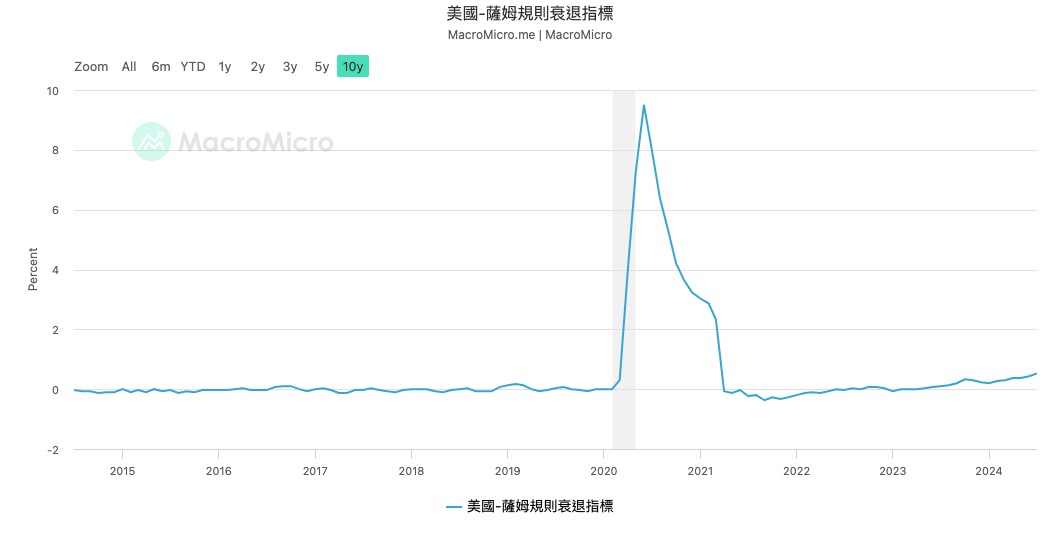

Many people call the potential rate cut in September a defensive rate cut by the Federal Reserve. The so-called defensive rate cut refers to the decision to cut interest rates to reduce the risk of potential economic recession when there is no obvious deterioration in economic data. In my previous article, I have analyzed that the US unemployment rate has officially set off the Sam Rule warning line for recession . Therefore, it is extremely important to observe whether the rate cut in September can curb the gradually rising unemployment rate and thus stabilize the economy and resist recession.

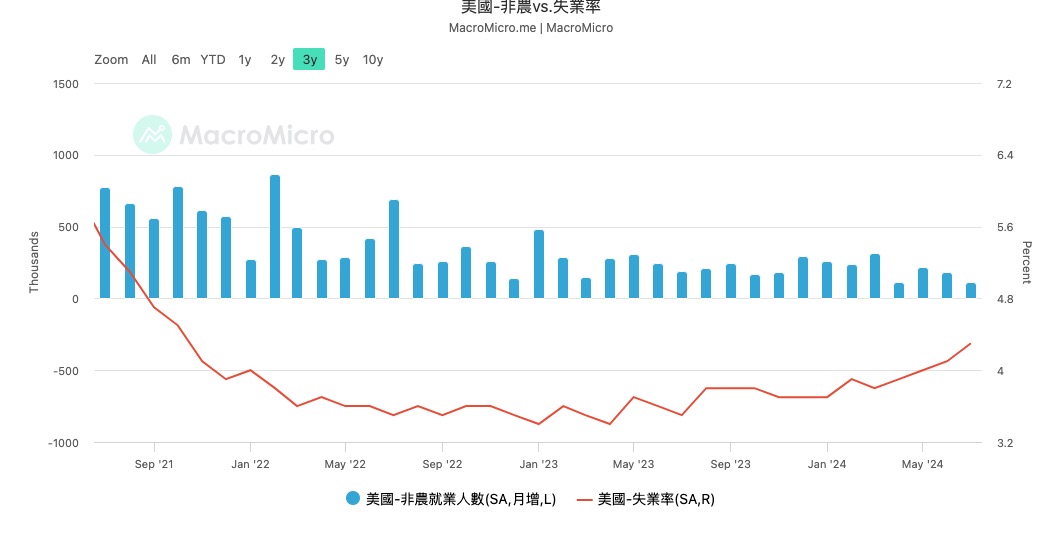

Lets take a look at what happened in the details of non-agricultural employment data. We can see that in the commodity production category, the number of manufacturing jobs has fluctuated for a long time with low volatility, and the construction industry has contributed more to the data. For the US economy, high-end manufacturing, as well as the technology and financial services industries that match it, are the main driving forces. That is to say, when the income of this part of the high-income elite class rises, consumption increases due to the wealth effect, which in turn benefits other low-end and medium-end service industries. Therefore, the employment situation of this part of the population can be used as a leading indicator of the overall employment situation in the United States. The weakness of manufacturing employment may show certain fuse risks. In addition, lets take a look at the US ISM Manufacturing Index (PMI). We can see that the PMI is in a rapid downward trend, which further proves the weakness of the US manufacturing industry.

Next, lets look at the service industry. The professional and technical industry and the retail industry both showed the same freezing situation. The main positive contributions to the index are education, medical care, leisure and entertainment. I think there are two main reasons. One is that the new crown has recurred recently, and due to the impact of hurricanes, there is a certain degree of shortage of related medical rescue personnel. The second is that most Americans are on vacation in July, which has driven the growth of leisure and entertainment industries such as tourism. When the vacation is over, this field is bound to receive a certain blow.

Therefore, in general, the current risk of recession in the United States still exists, so friends need to further observe the relevant risks through macro data, mainly including non-agricultural employment, initial unemployment claims, PMI, consumer confidence index CCI, housing price index, etc.

Risk 2: Pace of interest rate cuts

The second issue that needs attention is the pace of interest rate cuts. Although it has been confirmed that interest rate cuts have begun, the speed of interest rate cuts will affect the performance of risk asset markets. Historically, emergency interest rate cuts by the Federal Reserve are relatively rare, so economic fluctuations between interest rate meetings require the markets own interpretation to influence price trends. When certain economic data indicate that the Federal Reserve is raising interest rates too slowly, the market will be the first to react. Therefore, it is crucial to determine a suitable rate cut rhythm and guide the market to operate in accordance with the Federal Reserves goals through interest rate guidance.

The current market forecast for the September interest rate decision is that there is a nearly 75% probability of a 25 to 50 BP reduction, and a 25% probability of a 50 to 75 BP reduction. By paying close attention to the markets judgment, we can also more clearly judge market sentiment.

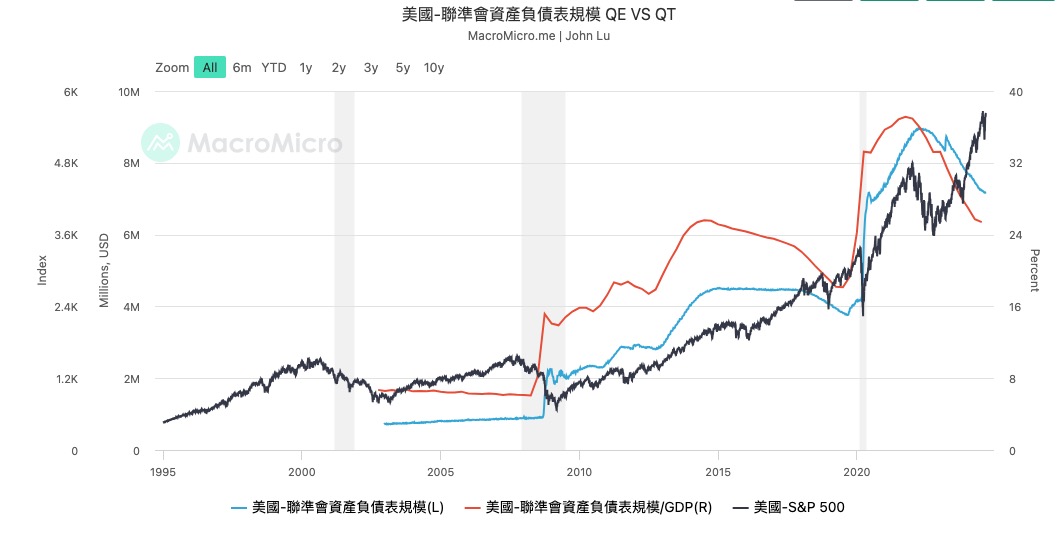

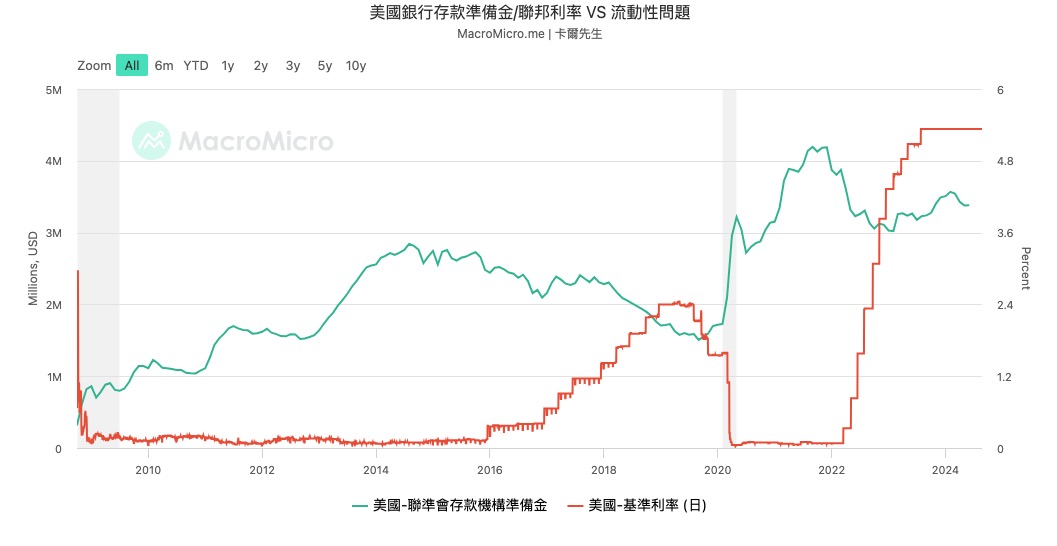

Risk 3: QT Plan

Since the financial crisis in 2008, the Federal Reserve has quickly lowered interest rates to 0, but it still has not been able to make the economy recover. At that time, monetary policy had failed because it could not continue to cut interest rates. In order to further inject liquidity into the market, the Federal Reserve created a quantitative easing (QE) tool to inject liquidity into the market by expanding the Federal Reserves balance sheet and increasing the size of the bank systems reserves. This method actually transfers market risks to the Federal Reserve. Therefore, in order to reduce systemic risks, the Federal Reserve needs to control the size of its balance sheet through quantitative tightening (QT). Avoid disorderly easing that leads to excessive risks.

Powells speech did not involve any judgment on the current QT plan and subsequent planning, so we still need to pay attention to the progress of QT and the changes in bank reserves caused by it.

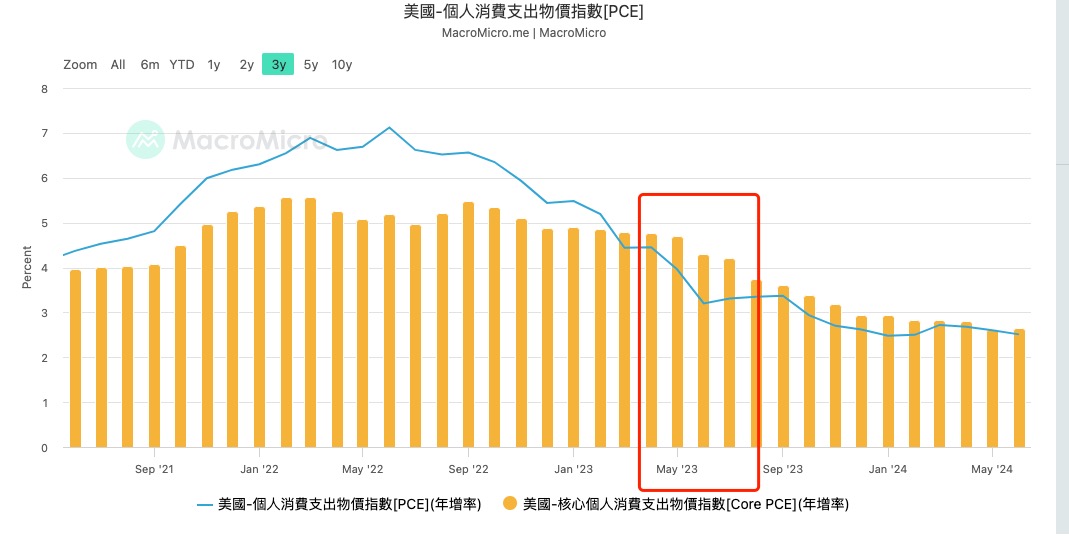

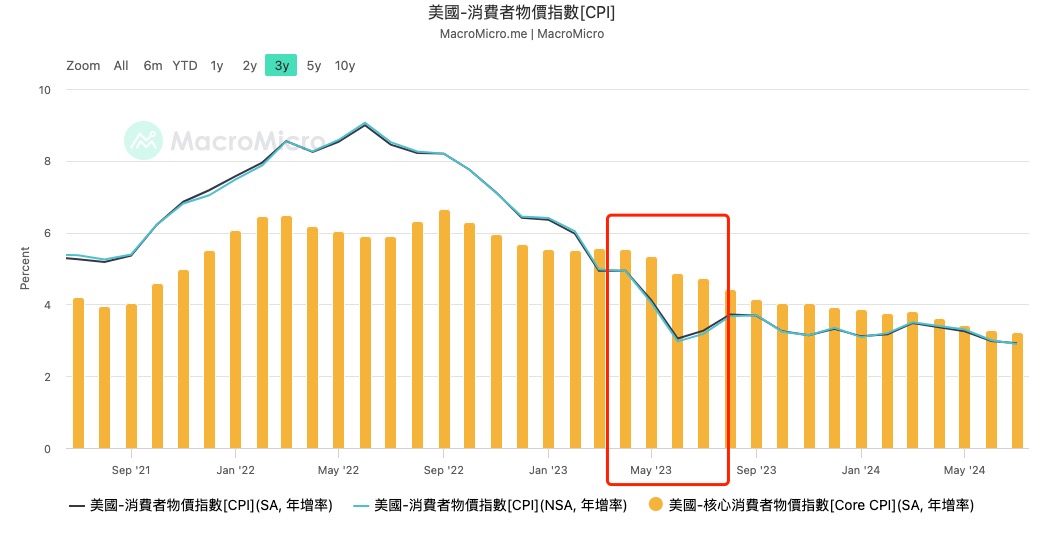

Risk 4: Renewed inflation risk

Powell remained optimistic about inflation risks at the meeting on Friday. Although it did not reach the expected 2%, he was confident in controlling inflation. Indeed, the data does reflect this judgment, and many economists have begun to talk about whether the target inflation rate is still set at 2% after the baptism of the epidemic.

But there are still some risks here:

-

First, from a macro perspective, the re-industrialization of the United States has not been smooth due to various factors, and it coincides with the anti-globalization policy of the United States in the context of the Sino-US confrontation. The supply-side problems have not been solved in essence. Any geopolitical risks will exacerbate the resurgence of inflation.

-

Secondly, considering that the US economy has not entered a substantial recession cycle during this round of interest rate hikes, as interest rate cuts continue, risk asset markets will recover. When the wealth effect reappears, service industry inflation will reignite as the demand side expands.

-

Finally, there is the issue of data statistics. We know that in order to avoid interference from seasonal factors, CPI and PCE data usually use annual growth rates, that is, year-on-year data to reflect the real situation. Starting from May this year, the high base period factors in 2023 will be exhausted. At that time, the performance of relevant data will be easily affected by growth.

Risk 5: Global central bank linkage efficiency

I think most of you still remember the risk of the Japan-US interest rate differential trade in early August. Although the Bank of Japan immediately came out to appease the market, we can still see its hawkish attitude from the congressional hearing of Kazuo Ueda two days ago. Moreover, during his speech, the yen also rose significantly and recovered after the officials re-appeasement after the hearing. Of course, in fact, the performance of macroeconomic data in Japan does require an interest rate hike, which has been analyzed in detail in my previous article , but as the core source of global leverage funds for a long time, any interest rate hike by the Bank of Japan will bring great uncertainty to the risk market. Therefore, it is necessary to pay close attention to its policies.

Risk 6: US election risk

Finally, I need to mention the risks of the US election. In my previous article, I have already made a detailed analysis of the economic policies of ٹرمپ اور حارث . As the election approaches, there will be more and more confrontations and uncertainties, so we need to keep an eye on matters related to the election.

This article is sourced from the internet: An article reviews the risks that need to be paid attention to in the early stage of the Feds interest rate cut

Related: The AI wave is coming again. An article reviews the holdings of Grayscale AI Fund

Original | Odaily Planet Daily ( @OdailyChina ) Author | Asher ( @Asher_0210 ) Recently, with the strong rise in Bitcoin prices, the altcoin market has ushered in a rare big rebound. Among them, the price performance of popular sectors such as Meme and AI is particularly outstanding. Last night, Grayscale announced the establishment of a new decentralized artificial intelligence fund – Grayscale Decentralized AI Fund LLC. The fund will focus on funding the following three key areas: artificial intelligence services, solving problems related to the use of centralized artificial intelligence, and developing infrastructure related to artificial intelligence. In addition, Grayscale announced some decentralized artificial intelligence projects that have been included in the fund, including TAO, FIL, LPT, NEAR and RNDR . After the news was released, the AI sector…