Task

Ranking

已登录

Bee登录

Twitter 授权

TG 授权

Discord 授权

去签到

下一页

关闭

获取登录状态

My XP

0

Orijinal yazar: Matthew Sigel, Patrick Bush

Original translation: Mars Finance, MK

Bitcoin (BTC) is expected to solidify its position as the world’s primary medium of exchange by 2050, eventually becoming one of the world’s reserve currencies. This prediction is based on the view that trust in current reserve assets may be eroded. Crucially, Bitcoin’s scalability issues have long hindered its widespread adoption, and emerging second-layer (L2) technology solutions are expected to completely solve this problem. Combined with Bitcoin’s immutable property rights and sound money principles, the enhanced capabilities provided by second-layer technology will build a global financial system that is more responsive to the needs of developing countries.

We predict that by 2050, the price of Bitcoin will reach $2.9 million. By then, Bitcoin will be used to settle 10% of international trade and 5% of domestic trade worldwide. This will result in central banks holding 2.5% of their assets in Bitcoin. Based on assumptions about global economic growth, investor demand for BTC and its trading volume, we calculated the potential price of Bitcoin through the money velocity equation to be approximately $2.9 million, corresponding to a total market value of $61 trillion. Using our valuation framework for Ethereum L2, the total value of Bitcoin L2 could reach $7.6 trillion, approximately 12% of BTCs total market value.

To accurately grasp Bitcoin’s potential role in the future financial architecture, it is necessary to analyze the current state of the International Monetary System (IMS) and how it is changing. This ongoing trend in the IMS, as economies gradually phase out the current reserve currencies, favors the rise of Bitcoin. We speculate that the main driver of this shift is the relative decline in the global GDP share of the current economic leaders (such as the United States, the European Union, the United Kingdom, and Japan). Unrestrained deficit spending and short-sighted geopolitical decisions by issuing countries will further erode people’s confidence in the current reserve currencies as a long-term store of value, thus accelerating this change. In addition, people are increasingly concerned about the property rights guaranteed by the Western monetary and financial system, especially the United States.

This overview includes:

Transformation of the international monetary system

Future Monetary System Trends

The IMS Problem and the Bitcoin Solution

Scaling Bitcoin with Second Layer Technologies

Predicting Bitcoins price in 2050

Trust is the cornerstone of the international monetary system

Trust is the backbone of the international monetary system

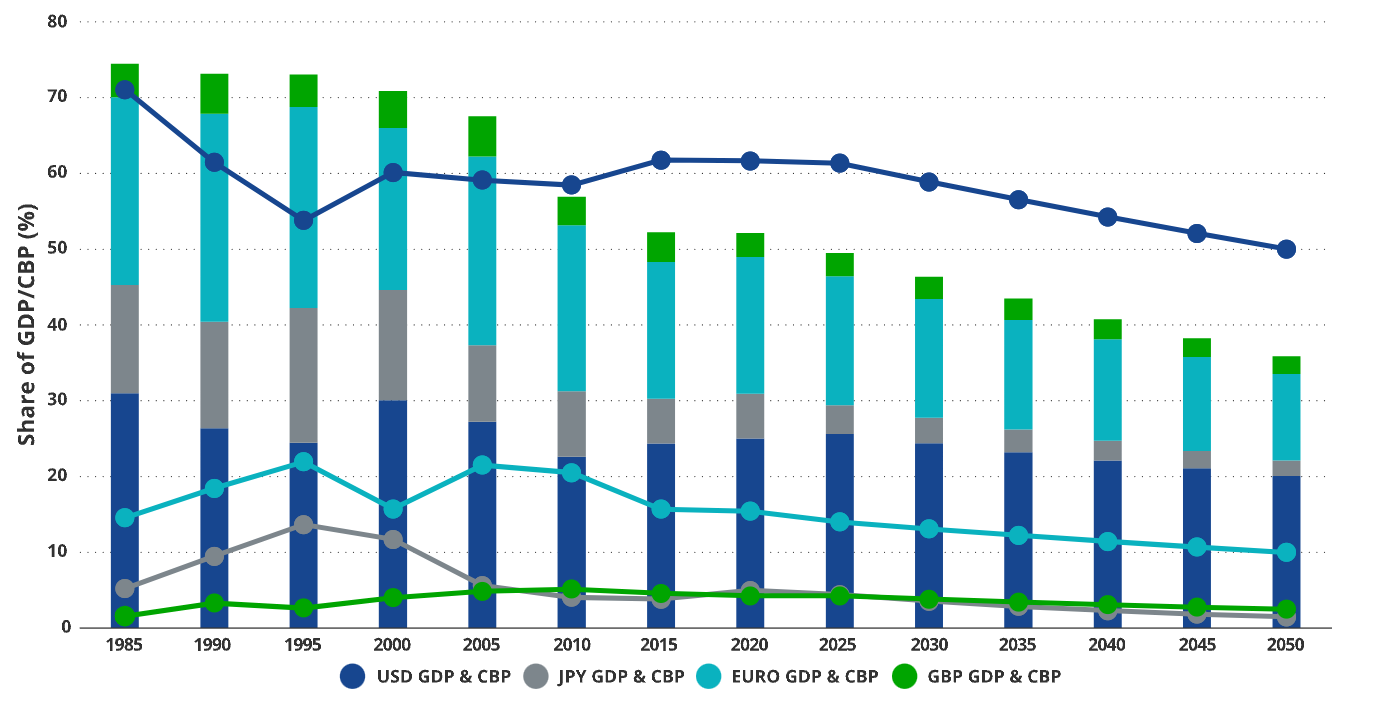

A currency’s position in the international monetary system is most directly reflected in its share of cross-border payments and central bank reserves. Currently, the international monetary system is dominated by a small number of currencies such as the US dollar, euro, pound sterling and yen. The use of a currency depends on its practicality, perceived value stability and trust in the fiscal discipline of its issuing country. The larger a country’s share of global GDP, the more widely its currency is used in international trade, forming a self-reinforcing feedback loop that consolidates its dominant position in international trade. Historically, changes in the international monetary system have tended to be slow, but we are at a critical turning point.

The gold standard dominated by the British pound in the early 20th century gradually shifted to a fiat dollar-backed system in the 1970s. Over the past 45 years, the dollars share of cross-border payments has been extremely stable. Except for a brief spike during the dollar rally in the early 1980s, the dollars share has remained largely stable at around 61%. This dollar-centric system is attributed to reliable fiscal policies, a consistently strong share of global GDP (25%), a dominant share of world defense spending (48%), and a strong domestic rule of law. The cumulative effect of these well-thought-out policies has made dollar holders trust in it as a globally recognized store of value for goods and services unwavering. Dollars can be used to purchase high-quality capital/consumer goods, invest in the worlds top companies, and even earn risk-free interest by lending to the US government. Most importantly, dollar holders believe that the rule of law ensures their currency status and can seek legal redress in the impartial US court system. However, this system is facing changes.

The EU’s share of global defense spending has fallen significantly between 1980 and 2023, from 25% to 14% of global spending (a 45% drop). Over the same time frame, the EU’s share of global GDP has also fallen, from 29% to 16% (a 43% drop). At the same time, the EU’s sovereign debt-to-GDP ratio has increased by about 34% since 1995, from 66% to 89% in 2023. Although Japan’s share of global military spending has remained relatively low at 2-3% due to its security agreement with the United States, its share of global GDP has also been declining. At the same time, its government debt-to-GDP ratio has also increased. Specifically, Japan’s share of global GDP has fallen from about 17% to just over 4% between 1995 and 2023—a 77% drop. From 1980 to 2023, Japan’s government debt as a percentage of GDP has surged 426%, from 47.8% to 251.8%. This series of events coincides with the decline in the use of the yen and the euro in global trade.

After regressing the major reserve currencies, we assess the relationship between changes in each country’s GDP share and changes in its share of cross-border payments (CBP). CBP refers to international transactions involving the transfer of funds across borders. These analyses show a highly significant correlation between GDP and CBP, with t-values greater than 4 for each test and R2 values between 0.3 and 0.5. This finding informs our predictions about the dominant currencies in the international monetary system in the future. Our model predicts that by 2050, the share of global productivity in Japan, the United Kingdom, and the European Union will drop from 27% in 2020 to less than 15%. We argue that this will lead to a corresponding decline in the use of their currencies, as demographic changes will inevitably affect the dominance of a currency.

The correlation between falling GDP and cross-border payments (CBP): Japan, UK and EU will lose FX share

Sources include VanEck Research, IMF and BIS, as of June 21, 2024. Forecasts shown are for informational purposes only, valid from the date of publication and subject to change without notice.

Our data analysis strongly suggests that existing reserve currencies are gradually losing their status as issuing countries become less economically important and less fiscally responsible. This trend is expected to continue and may accelerate. In particular, there is good reason to believe that the share of the US dollar, yen, euro, and pound sterling (the big four) in cross-border payments will continue to decline. Based on our forecasts of these currencies as a share of GDP, their share of cross-border payments is expected to fall from 86% in 2023 to 64% by 2050. In the intervening period when these currencies are declining in value, Bitcoin has ample opportunity to become an important alternative currency for international trade settlement.

Our analysis is based on a well-known fact: the populations of advanced economies are aging. By 2050, the share of older people in the four largest economies will increase by 20-40%. In Japan, for example, the share of people aged 65 and over will reach 39%, while those aged 75 and over will account for 25% of the total population. These demographic trends will force these countries to have lower productivity over time. Moreover, it is more difficult for advanced economies to significantly increase their economic growth rates than developing economies by simply investing in infrastructure, education, and technology. This interaction of demographic and economic realities leads the International Monetary Fund to predict that economic growth rates in developed countries will be much lower than in developing countries. As mentioned above, we forecast that the share of global GDP in the four largest economies will decline from 71% in 1984 to 36% in 2050.

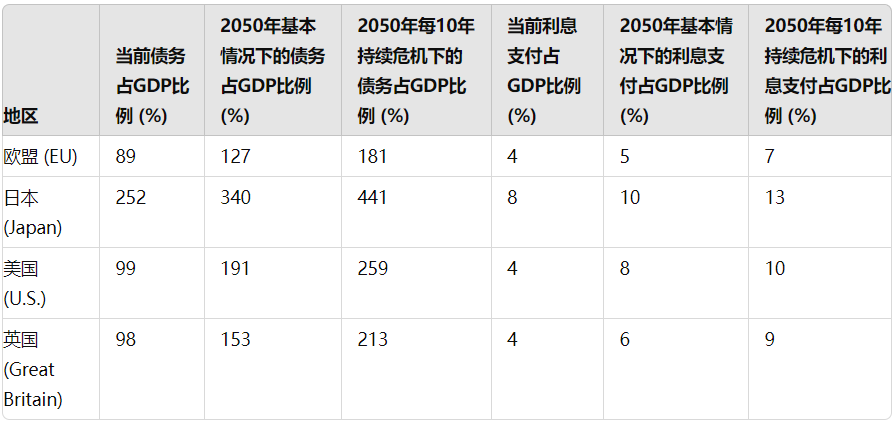

The reduction in the four major countries’ share of global GDP will be accompanied by a deterioration in each country’s fiscal position. The combined effect of population decline and low growth rates will cause these countries’ debt-to-GDP ratios to rise sharply. To assess the fiscal position of the four major countries in 2050, we refer to the IMF’s GDP growth estimates and population forecasts for these countries, and then combine the average debt maturity, inflation, deficit spending and GDP growth expectations. Our long-term forecasts are based on each administration’s long-term debt forecasts, adjusted appropriately for demographic trends.

Debt and interest rate scenario analysis to 2050

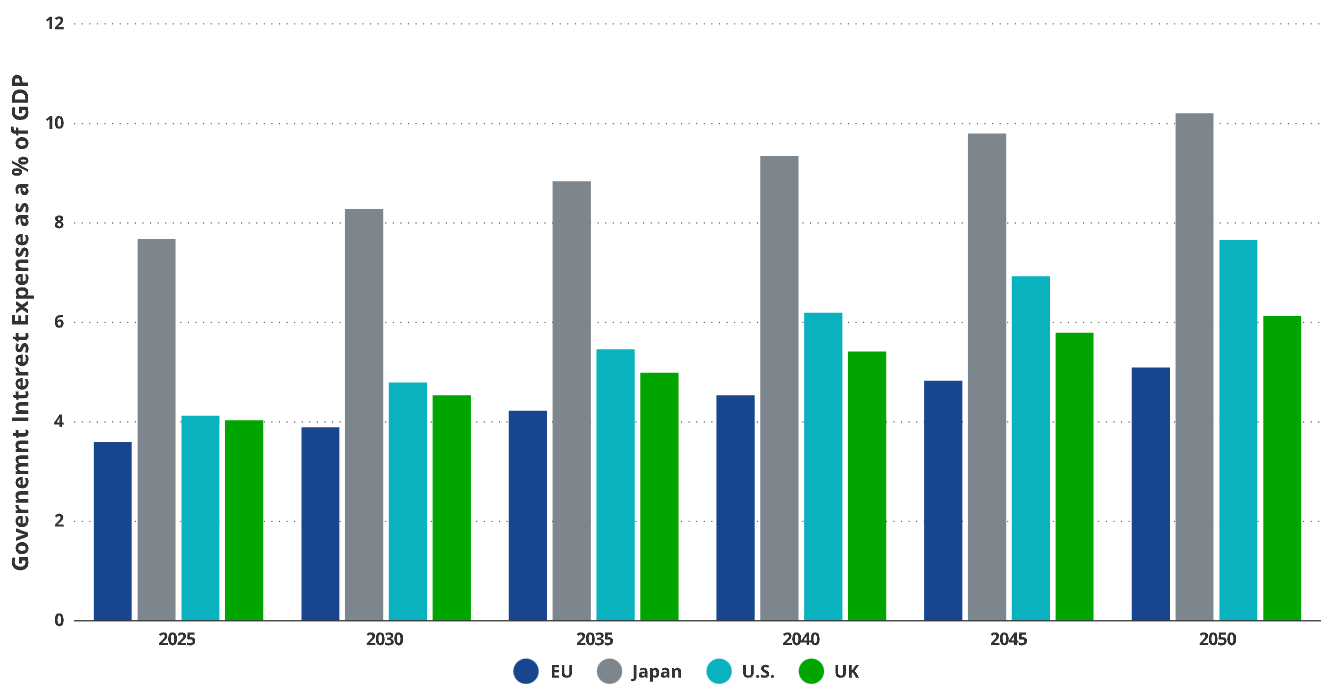

In our “baseline” scenario, we expect federal government debt payments to average more than 5% of GDP per year in the four major reserve currency countries. Specifically, for Japan and the United States, this ratio could reach 10% and 8%, respectively. It is important to note that these forecasts do not include major crisis scenarios such as the 2001 terrorist attacks, the 2008 financial crisis, or the 2020 pandemic, during which fiscal deficits in reserve currency countries increased significantly. Over the past 25 years, these major disasters have cumulatively increased the United States’ debt by 19%, 40%, and 26% of GDP. Given the frequency of these catastrophic events, we can almost certainly expect them to continue in the future. This successive crisis cycle will lead to upward revisions to our forecasts for the debt-to-GDP ratio and interest payments. Over the next 26 years, these three deficit spending shock scenarios are expected to increase interest payments by about 25% of GDP.

There are more factors that could make our “baseline” forecast for debt too optimistic. In the developed world, especially in the United States, fiscal indiscretions continue unabated as structural factors flourish. We have failed to factor in cost disease and the inefficiencies of some of the U.S. institutions that have led to the failure of billions of dollars in electric vehicle charging stations, subway lines that cost $4 billion per mile, high-speed rail that costs $36 billion per mile, and littoral combat ships that cost billions of dollars but cannot operate in coastal areas. Therefore, there is every reason to believe that government debt as a percentage of GDP will exceed our initial forecast. Most puzzling is that the fourth largest government deficit persists even during a period of strong economic growth. Clearly, governments in developed economies have realized that cutting spending is tantamount to political suicide. Under this logic, large deficits will persist until a dramatic reckoning forces change. Our forecast should be viewed as a conservative estimate because we also assume a relatively optimistic interest rate environment, averaging between 3-4%. As the cost of debt repayment increases, global bond investors are likely to demand higher rates.

We also need to note that the United States and its Western allies have increasingly favored solving expensive bureaucratic problems rather than seeking cost-effective solutions. The continued involvement of management and bureaucracy has led to ever-inflated costs to society, government, and the private sector, significantly increasing the cost of solutions. This interest-group-driven cost of management will continue in the fields of health care, higher education, and defense. While politicians can offer token positions to their preferred constituencies, employees within agencies view additional staff as a means to increase their salaries and positions. This practice creates an incentive structure for vested interests to continue to expand bureaucracy rather than streamline it. The result is not the solution of problems but the continued management of problems. The wars on drugs, homelessness, and terrorism have spawned multi-billion dollar industries that rely on the continued and long-term management of these problems rather than seeking cost-effective reductions and solutions. This is an incurable fiscal cancer that will continue to erode the long-term productivity and financial health of the four major agencies. The beneficiaries of administrative largesse are numerous, and there is no effective political force that can counter them.

Interest expenses at the four major banks are expected to surge

As a direct consequence, today’s reserve currencies, such as the dollar, pound, euro, and yen, will lose their role as a store of value and medium of exchange. The fiscal and economic problems that the four major countries are likely to face portend a gradual decline in the use of their currencies as reserve assets and in international trade. However, we believe that the strongest argument for a shift in the current international monetary system is the deterioration of property rights in countries and companies that trade and hold dollars, euros, yen, and pounds.

Today’s reserve currencies, such as the dollar, pound, euro, and yen, will gradually lose their function as a store of value and medium of exchange. The fiscal and economic problems that the four major countries are likely to face suggest that the use of their currencies as international trade and reserve assets will gradually decline. We believe that the strongest argument for a change in the current international monetary system is the gradual deterioration of property rights for countries and companies that hold and trade dollars, euros, yen, and pounds.

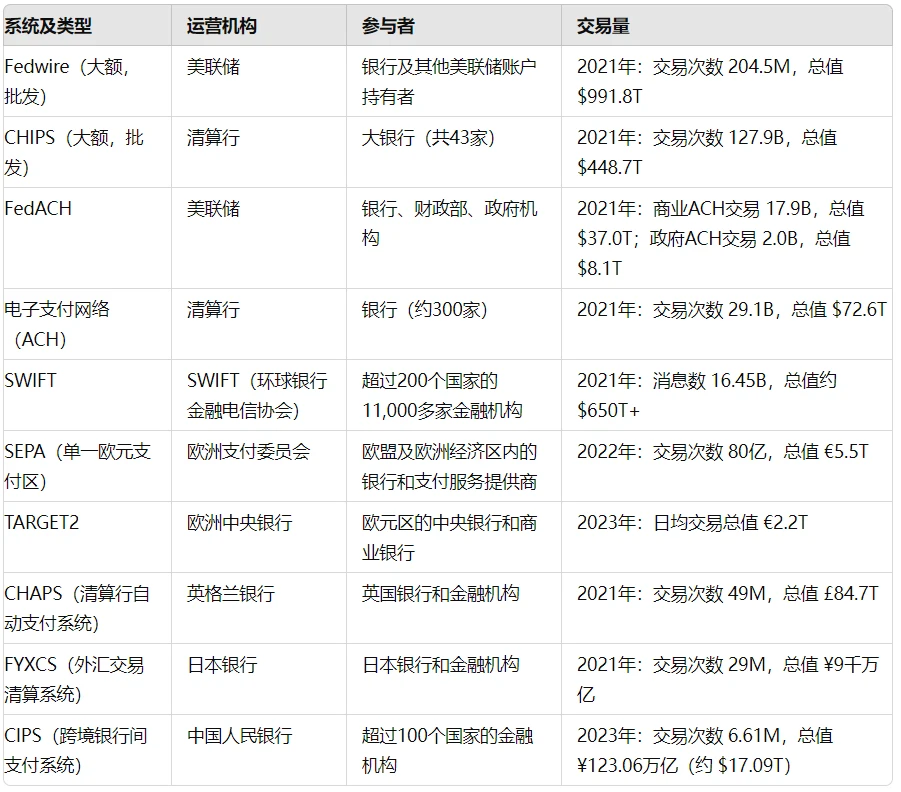

One of the most reliable ways to deprive a person or entity of their assets in the international monetary system is to place them on the US OFAC sanctions list. Sanctions are a policy tool that is used only when critical US national security interests are threatened. This tool is implemented in payment and settlement systems, such as the banking federations that run SWIFT (international), CHIP (US), TARGET 2 (EU), CHAP (UK), and FXYCS (Japan). Although these systems are controlled by many banks that are not directly regulated by the US, the threat of secondary sanctions forces all banks to agree to implement US policies. When the US announces sanctions, the banking systems of other major currencies tend to follow suit.

The number of entities subject to US sanctions has increased by 529% since 2009

Source: CNAS data as of June 21, 2024.

Over the past 25 years, the United States has increasingly used sanctions to advance its geopolitical strategy. Specifically, by 2022, the number of entities sanctioned by the United States reached 2,796, a 529% increase from 2009. Although part of this increase in 2022 was due to sanctions against Russia, this trend of increasing the use of sanctions shows that the United States has clearly chosen this policy direction since the September 11, 2001 terrorist attacks. In 2002, the year after the September 11 attacks, the official US report on sanctions was 17 pages. By 2021, 2022, and 2023, the number of pages of the same OFAC list had swelled to 247 pages, 825 pages, and 479 pages, respectively. Even before the Russian invasion, sanctions had become an increasingly important tool in US foreign policy.

In addition to the five countries that are subject to comprehensive sanctions by the U.S. Office of Foreign Assets Control, 17 other countries have been subject to sanctions to varying degrees. In addition, 13 countries are prohibited from using the U.S. dollar to purchase military equipment. Together, these 35 countries account for 31.6% of the world’s population and 22% of global GDP. Recent sanctions imposed by the United States and Europe on Russia, including freezing $300 billion of its foreign exchange reserves and other offshore assets, have further intensified the situation. As a result, many countries in the world are naturally concerned about the security of their assets in the current international monetary system. However, actions that undermine confidence in reserve currencies are not limited to the international arena; our analysis shows that the reputation of the U.S. dollar as an inviolable property right instrument is also being eroded.

Domestically, some government actions have raised widespread questions about the rule of law and the protection of property rights. Recently, a US judge cancelled a contractual obligation tied to a company’s performance targets because the rewards were deemed excessive. In another high-profile case, a company was fined heavily for allegations of business fraud, even though there was no injured party. In addition, factors such as national security, eminent domain, and civil asset forfeiture have also led to infringements on the rights of property owners. It is worth recalling historical precedents of property rights infringement during the New Deal era, including the confiscation of private gold stocks and the technically defaulted Fourth Liberty Loan. Logically, the precedent of seizing gold could also be used to fill fiscal gaps with other assets. Looking ahead, we see the rise of populism imposing new constraints on the US property rights system by restricting investment or confiscating unfair assets.

Overall, the institutional momentum to abolish property rights is growing in the United States. At the same time, property seizures for fiscal reasons are becoming a reality. How will holders of dollars and other proxy currencies respond to this environment of arbitrary seizures that are backed by law? An increasing number of countries are not only strongly protesting against actual and potential injustices, but are also beginning to move away from the existing pillars of the international monetary system.

A new international monetary system is emerging

Source: SWIFT data as of June 18, 2024.

The renminbi is becoming one of the beneficiaries of the changes in the global currency landscape. Recently, China has reached agreements with several countries, including Saudi Arabia, the Gulf countries, Bolivia, Ecuador and Brazil, to use the renminbi to settle bilateral trade. At present, the use of the renminbi in Chinas international trade settlement has surpassed the US dollar. Russia, an international currency pariah, recently stopped trading in the US dollar and the euro on its Moscow Stock Exchange. At the same time, its major commodity producer, Rosneft, issued two renminbi-denominated bonds, amounting to 10 billion yen and 15 billion yen respectively. Some Indian refiners have begun to use renminbi to pay for their oil purchases. As a result, as of April 2024, the renminbi accounted for 4.52% of all transactions conducted through the SWIFT system, almost double that of April 2023.

In addition to the RMB, more and more countries are beginning to use their own currencies for international transactions rather than relying on the four major currencies. For example, India has reached an agreement with Malaysia and other countries to use rupees to purchase oil and settle trade, and has established a local currency settlement system with nine other central banks. It is particularly noteworthy that Saudi Arabia announced in 2023 that it was willing to accept currencies other than the US dollar to price oil, and recently joined the China-led central bank digital currency project.

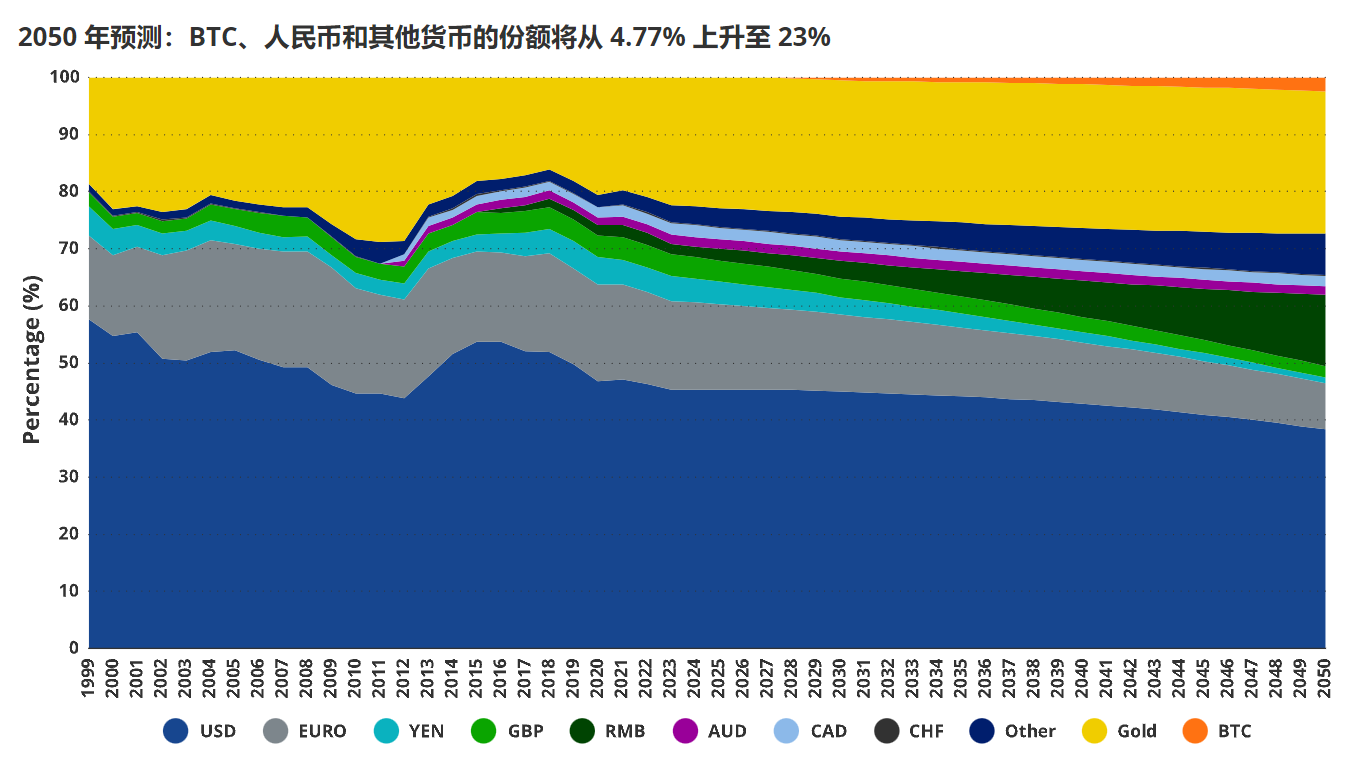

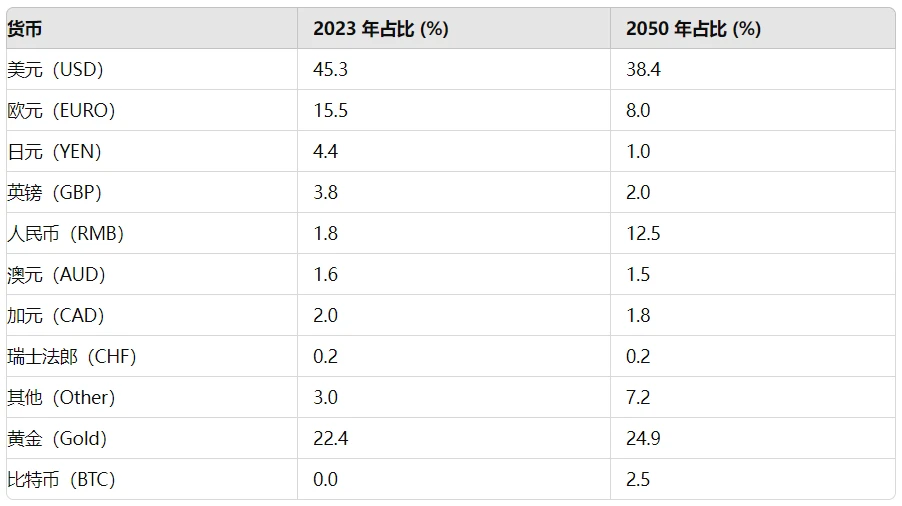

By 2050, the market share of BTC, RMB and other currencies is expected to rise from 4.77% to 23%.

It is expected that by 2050, multiple countries exploring alternatives to the existing international monetary system will face limited attractive options. By then, the number of bilateral trade agreements is expected to increase, and the use of the RMB will also increase. As a result, the use of emerging market currencies in transactions is expected to drive central bank reserves in the other category from 3% to 7.5%. At the same time, the share of the RMB in global reserves may also increase to about 12.5%. These changes may come at the expense of the four major currencies, while developed commodity producers such as Canada and Australia will lose less market share. It is worth noting that in the scenario we foresee, Bitcoin is expected to account for 2.5% of global reserves, and its share in domestic and international trade may rise to 5% and 10%, respectively.

This dynamic could unfold because of the challenges posed by other potential alternatives that could replace the current four major monetary systems. Although bilateral trade agreements and the rise of emerging market economies could promote the widespread adoption of emerging market currencies, trust issues could hinder their full acceptance. For example, the Latin American debt crisis in the 1980s and the Asian currency crisis in the 1990s both highlighted the risks and incentives of developing countries to meet international obligations or curb money printing.

Although the RMB has appreciated as Chinas GDP has grown relative to its own, widespread suspicion of China and its acceptance as a reserve currency may limit its use to a level comparable to that of the US dollar. In addition, the use of more domestic currencies in international trade implies a high degree of alignment of economic interests. However, the value of most developing countries main exports, such as commodities, is generally not competitive with the high-value manufactured goods of developed economies. This difference in trade value may force debtor countries to weaken their fiscal obligations through monetary expansion.

In short, the most challenging issues in adopting a new monetary system are about trust and issuance policies of potential alternative currencies. Frankly, only a few emerging market countries can inspire enough confidence to justify their inclusion in reserve currency status. Some countries may turn to China and other developing economies to hold reserve balances. However, many people are dissatisfied with poor reserve options and may increasingly turn to Bitcoin because it solves many of the problems faced by current reserve currency users.

Bitcoin provides its holders with:

Distrust

Neutrality

Unchanged monetary policy

Perfect property rights

Bitcoin is designed to replace fiat currencies, and its system replaces corrupt human authority with immutable logic. Holders do not need to worry about entities diluting the value of BTC, using Bitcoin for political purposes, or abusing its users. Bitcoin, through its innovative approach, eliminates biased government actions that could hinder the property rights of BTC holders. As a politically and economically neutral system, Bitcoin replaces biased actors with simple software algorithms.

Bitcoins framework enables anyone from national governments to local citizens to hold and trade BTC without going through intermediaries. This is very important for controlling foreign policy from a national sovereignty perspective. Considering the cost, Bitcoin also eliminates many of the financial expenses of transacting through the current international monetary system. Unlike fiat currencies, which are often subject to monetary inflation and have an average lifespan of only 35 years, Bitcoin has a fixed monetary policy that focuses on maintaining the value of BTC. Once the total supply of BTC reaches 21 million, the inflation strategy will peak and BTC holders can rest assured that the value of Bitcoin will not be arbitrarily diluted by central banks due to conflicts of interest. Bitcoins solid hard currency design is supported by a group of loyal users and core contributors who are committed to maintaining its economic principles. Therefore, Bitcoin can be regarded as the religion of sound money.

Bitcoin offers central banks, investors, and international trade participants a value proposition that no current fiat currency can offer. Every fiat currency is controlled by a political class whose ultimate goal is usually to print money. Constitutions are designed to set limits on government power and avoid the abuses that have been common throughout history. Bitcoin applies constitutional constraints to the monetary realm, embodying a system created by the people, for the people. Bitcoin is unique in the international monetary system in that it provides holders with unlimited property rights. The issuer of BTC is the Bitcoin software itself, and its protocol does not allow for the seizure of BTC, ensuring that only those who hold the private keys to an account can access their Bitcoin. Barring hacking and theft, Bitcoin holders do not need to worry about their assets being arbitrarily seized for communicating with the wrong people or participating in protests. Given concerns about asset confiscation in the United States or other major countries, we believe the inviolable property rights provided by Bitcoin are extremely valuable.

International Payment Systems

In order for Bitcoin to become an effective medium for international trade, it must undergo fundamental reforms. Bitcoin has the potential to bring tremendous value to users of the International Monetary System (IMS) by solving many of the problems in the current system. Despite this, Bitcoin has not yet been able to become a mainstream cross-border payment tool. This is mainly because Bitcoins processing power is insufficient to cope with the needs of the global financial system.

Currently, Bitcoin processes transactions at a rate of about 7 to 15 per second, depending on the metadata. A Bitcoin block is processed every 10 minutes, and a transaction usually requires 5 to 6 blocks to be confirmed. Therefore, Bitcoin can process about 576,000 transactions per day, about 4,000 transactions every 10 minutes. In comparison, the SWIFT system can process about 45 million messages per day, and the CHIP system about 350 million transactions per day.

In addition, the software that manages the Bitcoin network does not support complex smart contract languages. This means that on the Bitcoin network, users cannot create complex financial applications that are feasible on more advanced blockchain platforms such as Ethereum or Solana. Therefore, for functions such as banking, trade execution, and complex custodial services, Bitcoin users usually need to rely on centralized institutions. While this practice can expand the scale of Bitcoins use, it also weakens some of its core features in international trade.

The limited functionality of Bitcoin is a deliberate design choice. Bitcoins main developers believe that adding more features could introduce new security risks, increase centralization, and could weaken Bitcoins fundamental purpose. Historically, those who support more complex versions of Bitcoin with higher processing power and smart contract capabilities tend to choose to create new cryptocurrency projects.

However, attitudes in the Bitcoin community are changing rapidly as new solutions are developed and adopted that cater to both hard currency seekers and those who expect more from Bitcoin. These solutions are the result of many people thinking deeply about the long-term sustainability of Bitcoin.

By exploring why countries do not currently use gold for transactions, we can better understand the challenges facing Bitcoin as a medium of international trade. Historically, gold has been widely used as a reserve currency and medium of international trade. However, several key issues have led to its decline in this role.

Physical inconveniences and logistical issues In theory, gold can be traded by moving bars from one warehouse to another, but this is not practical on a large scale. The physical properties of gold make it cumbersome and costly to transport and safely store. Although electronic systems are available to record gold transactions, the physical movement of gold remains a challenge, especially when large volumes are involved.

Lack of flexibility Gold cannot meet the flexibility required by the modern financial system. Due to its physical properties, gold is difficult to be divided into smaller units for daily transactions and is not suitable for supporting complex financial instruments. Although digital gold exists, its practical application is still limited by the basic properties of gold as a physical asset.

Security Risks The holding and transportation of gold involves significant security risks, including theft and loss. Extensive security measures need to be implemented, which not only increases the cost and complexity of using gold as a medium of exchange. These risks are exacerbated in international transactions involving multiple parties and multiple jurisdictions.

Integration of technology and finance The modern economy is highly dependent on advanced financial systems, requiring fast, secure and flexible means of transaction. Even if gold is digitized, it is difficult to integrate seamlessly with these systems. In contrast, the transaction speed and efficiency of electronic legal tender far exceeds that of gold, making it more suitable for modern financial infrastructure.

While Bitcoin faces certain challenges, such as potential security risks, it has overcome many of the limitations of gold. Unlike gold, Bitcoin is inherently digital and therefore easier to transfer and divisible. Despite some current limitations, Bitcoins programmability provides it with greater flexibility and the potential for future improvements. In addition, through the protection of cryptographic technology, Bitcoin transactions are able to reduce certain security risks associated with physical gold. Although the use of a neutral currency such as Bitcoin (or gold) for trade payments seems unlikely in the current environment, it is conceivable that the need for a stable, secure and flexible medium of exchange in a changing geopolitical context may drive a significant shift in the future.

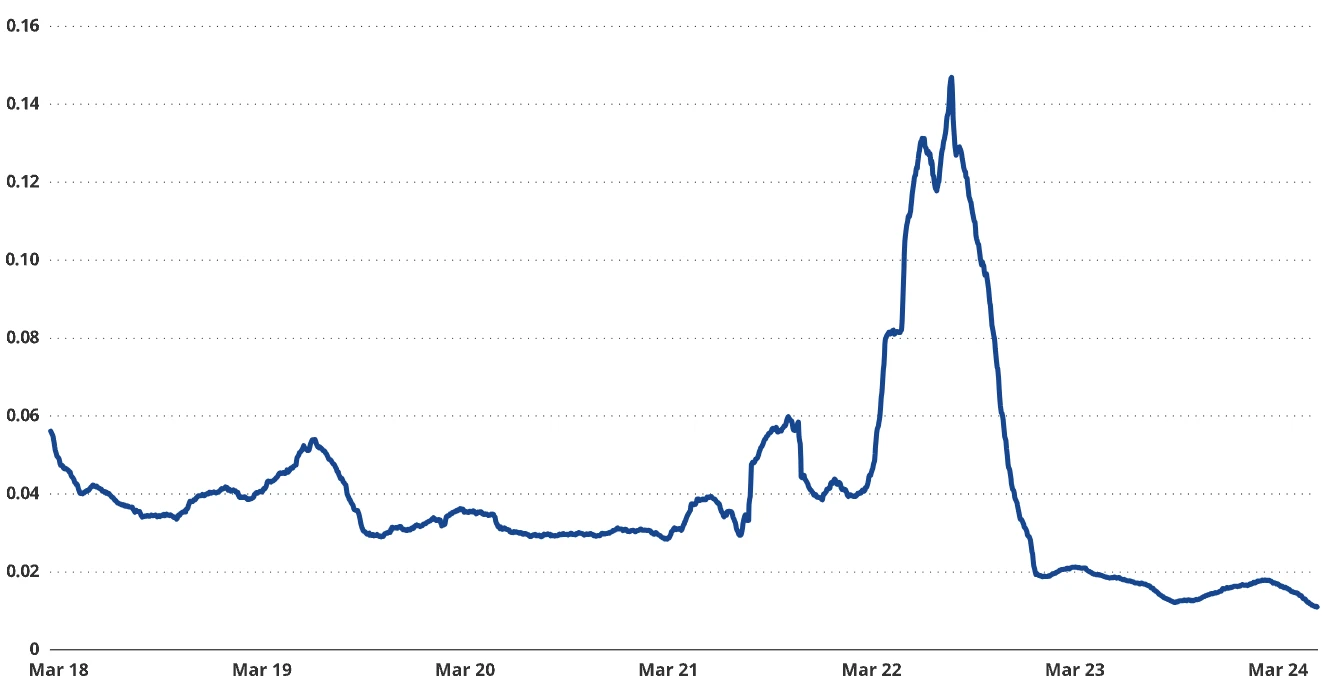

It is estimated that by 2024, the circulation speed of Bitcoin will be only 25% of that in 2018

Source: Glassnode, as of June 30, 2024.

Given that Bitcoin’s transaction throughput is limited by the economic principles that its community adheres to, many industry insiders have explored various technical means to expand the scale of its network. It is generally believed that Bitcoin must scale up to grow and even survive. The reason behind this is that the high fixed and variable costs are borne by miners, who are the guardians of the Bitcoin network. Since the inception of the Bitcoin network, miners’ main income (accounting for up to 94%) has come from the inflation of block rewards. Since Bitcoin’s inflation is limited, to cover miners’ costs, transaction fees on the network will become the main source of miners’ income to offset the decline in inflation. In the year before Bitcoin’s inflation halving on April 19, 2024, Bitcoin miners have earned nearly $13 billion through inflation, while revenue from transactions is $1.1 billion. In order for miners to be able to maintain operations in the long term, the price of Bitcoin must rise enough, or the number of transactions must increase to cover most of the costs.

Therefore, the Bitcoin community is actively promoting an increase in transaction volume in order to expand the scale of Bitcoin and provide basic income security for miners. In addition, subtle but critical changes to some core software are also part of this change. However, Bitcoins role as a store of value asset is somewhat contradictory to its need to be a medium of exchange – in theory, value stores should not be traded frequently. This is reflected in Bitcoins currency circulation velocity, which has dropped from 0.042 in 2018 to 0.014 in 2024. In any case, the need to expand the scale of Bitcoin has spawned a variety of solutions that can transfer the value of Bitcoin without directly using the Bitcoin chain, which are often referred to as second-layer solutions. Off-chain expansion mainly includes two forms: one is to create cryptographic tokens supporting Bitcoin on other blockchains through centralized entities; the other is to achieve the same purpose in a decentralized way.

In the centralized model, entities such as cryptocurrency exchanges, trading companies, or miners hold Bitcoin and issue certificates representing ownership of these Bitcoins. These certificates can be redeemed for Bitcoin on various blockchains and exchanges, and are usually created by minting crypto tokens. The most famous example is wBTC, known as wrapped Bitcoin. In this model, a centralized exchange called BitGo holds and locks Bitcoin, issuing a crypto asset called wBTC to users who provide Bitcoin. Since then, wBTC has circulated in ecosystems such as Ethereum, and its value is closely related to the price of Bitcoin. wBTC is widely used in DeFi applications on Ethereum and Tron, and approximately $10 billion worth of Bitcoin has been converted into wBTC.

The key point about these wrapped BTC products is that users must trust the issuing entity not to engage in fraud or re-hypothecate the underlying Bitcoin. The challenge with this system is that there is potential counterparty risk regardless of who is holding and wrapping the Bitcoin. One downside of centralized solutions like wBTC is that they do not add additional revenue to the Bitcoin network, as Bitcoin is locked up and not generating transaction revenue, which is the lifeblood of the Bitcoin ecosystem.

Bitcoin’s total locked value (TVL) is mainly dominated by wBTC, and other currencies are also gradually increasing

Source: Deflama, as of June 24, 2024.

Another class of “off-chain” scaling solutions are considered “trustless” because they do not rely on a centralized entity, but are based on decentralized solutions. This class of solutions involves various software that uses components of Bitcoin in conjunction with off-chain networks, such as other blockchains or similar trustless networks. At the heart of these solutions is often Bitcoin’s multi-signature scheme, which locks BTC in a Bitcoin account while minting tokens representing the Bitcoin on another blockchain. This range of off-chain scaling solutions allows users to transfer these representations, essentially certificates of ownership, corresponding to the BTC locked on the Bitcoin chain. Often, this is referred to as “bridging”, and these “bridging” Bitcoin off-chain solutions are collectively referred to as Bitcoin Layer 2 (L2). However, the concept of Bitcoin L2 encompasses a variety of different solutions compared to the more specific Ethereum L2 definition (see our article on Ethereum L2 for details). First, Bitcoin L2 is not a blockchain like most Ethereum L2s; second, Ethereum L2 relies on Ethereum to run its blockchain securely, while some Bitcoin L2s intend to use Bitcoin for security in the future, but many blockchains simply bridge BTC to their chain to allow transactions. The bottom line is that only some Bitcoin L2s are designed to increase the value of the network by creating value for miners.

A popular but limited second layer of Bitcoin is the Lightning Network, which allows users to create Bitcoin certificates off-chain and send Bitcoin through the created network (called a payment channel). In this setup, users can conduct any number of transactions off-chain, and when they decide to settle these transactions, they can close this payment channel. After that, the changes in BTC balances between different parties will be finalized as a single transaction on the Bitcoin chain. Payment channels are a subset of a broader set of scaling solutions (called state channels), which allow off-chain representations of Bitcoin to interact with off-chain dApps and settle transaction results at sporadic or predetermined time intervals.

The word state in state channels refers to the current state of balances and other relevant variables of all participants in a series of transactions. The main feature of state channels is that most of the transaction data is kept off-chain, which means that transactions are conducted privately between parties and are not immediately recorded on the blockchain. Only the final state or the result of multiple off-chain transactions is submitted to the blockchain. This approach can speed up transactions and reduce fees because only the final settlement is recorded on-chain. When a participant wishes to withdraw his balance, the final state of the off-chain data is reconciled and broadcast to the Bitcoin blockchain. Due to multiple shortcomings and potential security vulnerabilities of the Lightning Network, its usage is extremely low (TVL is $323 million, accounting for 0.026% of the Bitcoin supply).

Another widely used form of Bitcoin L2 is sidechains. They apply the concept of state channels to extend Bitcoin by minting Bitcoin representations off-chain, but completing off-chain transactions of BTC on a different blockchain from Bitcoin. Sidechains have a consensus mechanism that may (but not always) rely on Bitcoins consensus. They can be thought of as mini-economic zones pegged to Bitcoin via bridges. These bridges are protocols that use various combinations of complex mathematics, software, and economics to lock BTC on Bitcoins blockchain, allowing tokens to be created on the sidechain that represent locked BTC. When users trade bridged representations of BTC on the sidechain, they can redeem BTC on Bitcoin by settling the results of the transaction to receive the traded BTC.

These sidechains allow Bitcoin to be traded with BTC, thus achieving a much greater transaction throughput (in BTC) than the Bitcoin blockchain allows. This is because many transactions can be conducted off the bridged Bitcoin chain and then settled back to Bitcoin across multiple accounts in large batches if necessary. This is similar to the ACH batch processing system in the United States, where banks can record a database of interbank transfers and settle at the end of the day. An important distinction between sidechains is whether BTC is the native currency of the blockchain. If BTC is the primary currency, all transactions must be paid with BTC fees; if not, other currencies are accepted to pay transaction fees. Going back to the question of the value added to the Bitcoin network, most sidechains do not add value to the Bitcoin network because almost all BTC-valued transactions occur off-chain. However, mainly in the case where BTC is the native currency of the sidechain, they increase the value of Bitcoin by creating more demand for BTC.

Bitcoins sidechains L2 vary widely in how they operate. Some may be proof-of-stake networks like Ethereum, with validators running the chain and staked by various cryptocurrencies. Others, like Stacks, use BTC locked on Bitcoin to support validators running and protecting the chain. Another interesting consensus mechanism is called merged mining. Merged mining, used by Bitcoin L2 Rootstock and BOB, means that Bitcoin miners embed block hashes (compressed data) from the merged-mined chain somewhere inside a Bitcoin block. At almost no additional cost, any Bitcoin miner who chooses to merge-mine another blockchain will add a checkpoint of events on that blockchain to Bitcoin. In return, miners are compensated for this service in the form of transaction fees (in BTC) on those chains.

Advantages of Bitcoin Layer-2 Rollups

Source: VanEck Research, as of June 25, 2024.

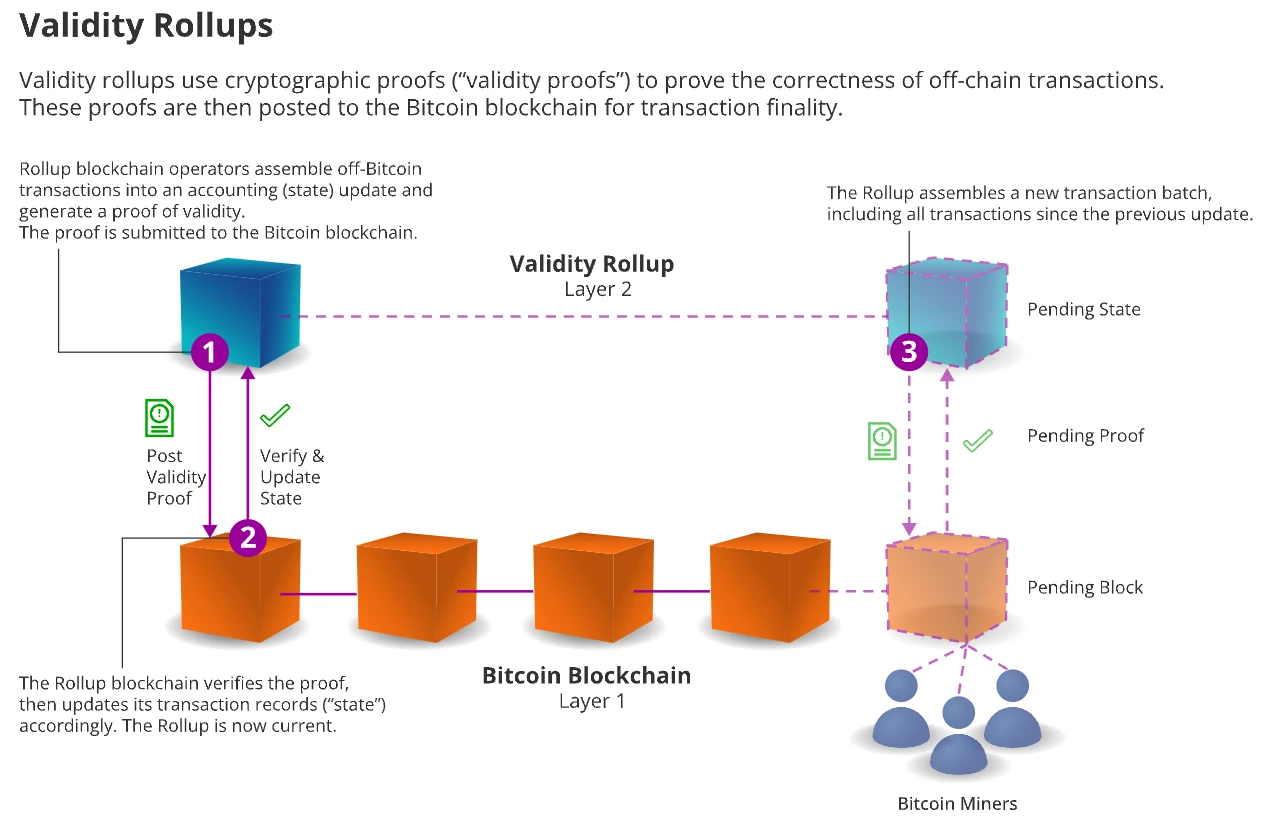

Hailed as the next generation of Bitcoins second-layer technology, Rollup aims to expand the Bitcoin network and spread the security properties of its blockchain to other blockchain platforms. Rollup technology works by publishing transaction data or verification information on a parent blockchain such as Bitcoin or Ethereum. Thanks to the publicly verifiable data on the parent blockchain, the security of the Rollup system relies on its parent blockchain. In a sovereign Rollup, the published data allows the outside world to verify the authenticity of the transaction; while a validity Rollup involves sending the transaction proof of Bitcoin L2 Rollup to Bitcoin and executing it.

The main difference between these two types of Rollup is the amount of data published and the software requirements. Sovereign Rollup publishes more data to the limited capacity of Bitcoin without modifying the Bitcoin core software. In contrast, the validity Rollup requires less data to be published, but it requires an update to the Bitcoin software, which is usually achieved through a soft fork. Rollups are seen as an ideal solution for Bitcoins expansion because they enhance off-chain scalability without compromising Bitcoins core principles – trustlessness and decentralization. In addition, they also bring more transaction revenue to Bitcoin miners because settlement proofs and data publication involve multiple transactions. Despite the bright prospects of Rollup, its implementation on Bitcoin still faces significant challenges that require changes to the core software.

Updates to the Bitcoin software brought the first wave of expansion improvements, which were significant but still limited. For example, the Segregated Witness (SegWit) and Taproot upgrades. SegWit greatly improved the efficiency of Bitcoin transactions by processing transaction signatures separately from transaction data, allowing each 1 MB Bitcoin block to accommodate up to 4 times the transaction volume. The Taproot upgrade optimized Bitcoins cryptographic infrastructure, making transactions more compact and faster. These two upgrades allow the Bitcoin core software to store more transactions and various types of data, as evidenced by the rise of NFTs and memecoin.

However, implementing sovereign rollups does not require changes to the Bitcoin software. While the amount of data published by these rollups is huge (even after compression), they still limit Bitcoin’s scaling potential. Ethereum rollups like Base and Arbitrum only have a transaction throughput of about 55 transactions per second at full load, despite having similar levels of compression. In order to achieve massive scaling, it will be necessary to significantly increase data compression or create multiple rollups to publish data simultaneously.

Validity rollup solves the problem of Bitcoins data capacity limitation, but requires verification to be performed through modifications to the Bitcoin core software. Some developers are working on an upgrade called BitVM to enable validity rollup on Bitcoin. BitVM introduces a challenge and response mechanism sent through Bitcoin transactions to verify fraud and validity proofs. This will not only expand Bitcoins capabilities, but also enable trustless bridging, replacing centralized BTC representatives such as wBTC. The development of BitVM is expected to be completed in about 18 months, and its implementation will require a soft fork by the Bitcoin community.

OP_CAT is a promising software update that may enable Bitcoin to scale to meet the needs of a global financial system. The introduction of OP_CAT adds a level of sophistication to Bitcoin programming, allowing for the use of primitive smart contracts called covenants on Bitcoin. Covenants allow software engineers to create the logic needed to support sovereign rollups and validity rollups on Bitcoin. Starknet, a second-layer blockchain on Ethereum, has pledged $1 million in funding to core developers working on OP_CAT. Starknet also plans to use OP_CAT to solve the problem of implementing proofs of validity on Bitcoin.

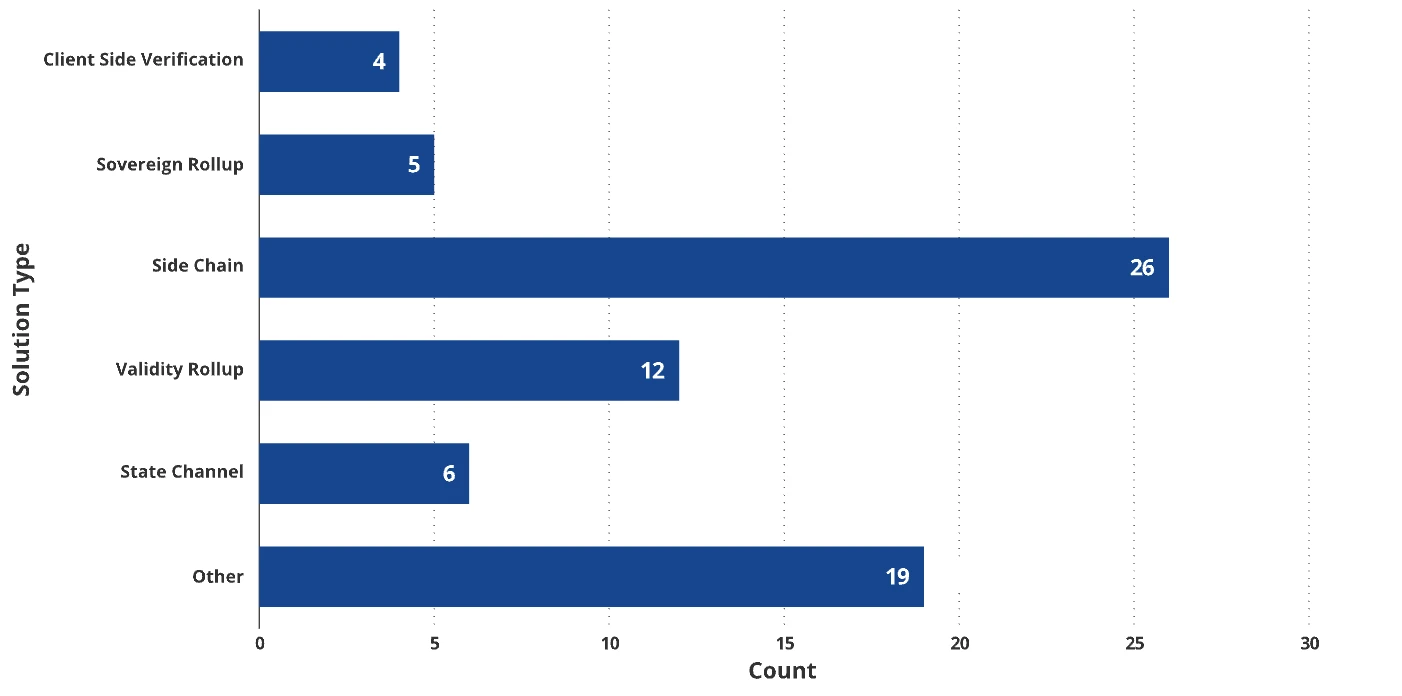

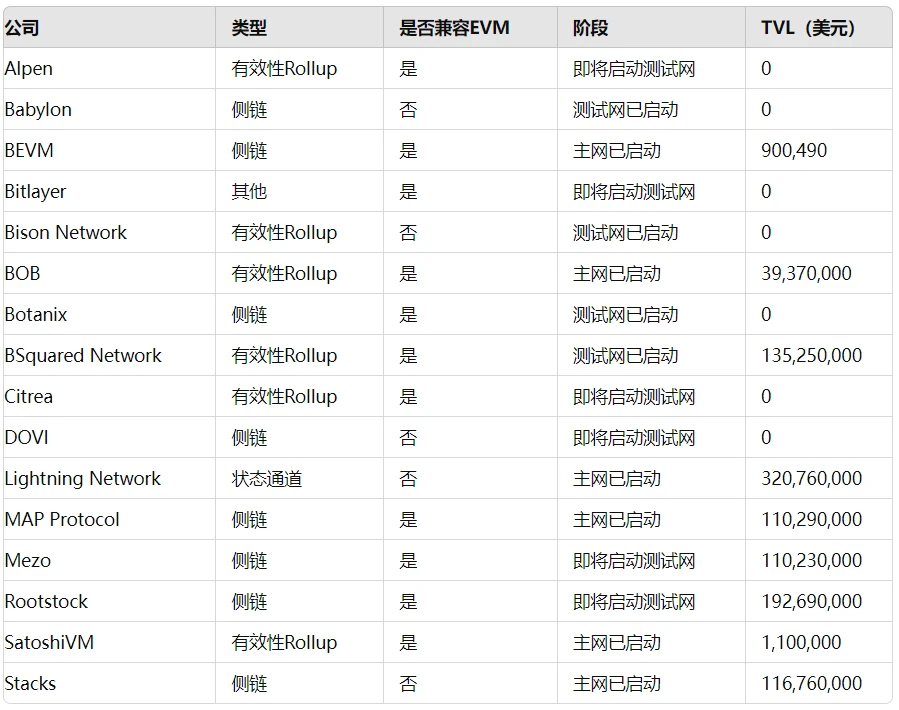

Bitcoin L2s Status

Source: BTC L2.INFO, as of June 24, 2024

Currently, more than 73 active projects are developing Bitcoin L2 solutions with a total locked value of more than $3.61 billion. Although these projects are still in the early stages, only 26 of them already have live mainnets running. Due to their early stages, most projects have not yet shown significant traction. Merlin Chain, as one of the early leaders, has an average daily transaction volume of only 50,000 to 80,000 transactions, despite being the largest Bitcoin L2 by total value (TVL) of BTC bridged to the chain, with a TVL of $1.33 billion. In terms of activity, it is on the same level as Cosmos Hub, Cardano, and Gnosis Chain. The reason why Merlin Chain lacks traction in the early days is that its most popular application, MerlinSwap, has a TVL of only $2.85 million.

The current competition for Bitcoin L2 is mainly focused on attracting TVL and developers. TVL mainly comes from large holders, such as independent whales, miners and investment funds. Private investment rounds offer investors discounts to introduce BTC to L2. Business development operations are mainly aimed at large BTC and other cryptocurrency holders to ensure the realization of TVL promises. Attracting developers is also another important strategic goal, and about 40 projects support EVM with the aim of recruiting Ethereum developers. Currently, there are about 312 developers working on BTC L2, while there are 960 developers on Ethereum L2 and 966 developers on Ethereum.

There are no clear winners in the Bitcoin L2 space, as many projects have yet to launch or conduct official marketing. As the space is still in its early stages, we focused on 16 projects that we believe have high potential to scale Bitcoin. We evaluated these projects based on the reputation of their builders, backers, and promised TVL (if any).

Bitcoin Layer 2 Has Huge Potential

To accurately estimate the value of Bitcoin in 2050, this analysis uses a simple equation based on the velocity of money, which covers three core factors:

Total domestic and international trade volume settled in Bitcoin (GDP);

The supply of Bitcoin (BTC) in active circulation;

BTC transaction speed.

A key assumption underlying our forecast for 2050 is that Bitcoin will enter the international monetary system and become a major force challenging the four major currencies. It is expected that BTC will be widely used in international trade as a major medium of exchange and a valuable store of wealth. This trend forms a positive feedback loop similar to Greshams Law: as the utility and value of BTC increase, central banks and long-term investors will tend to increase their holdings of BTC, thereby compressing the floating supply in the market.

First, we calculated using baseline data on global trade and world GDP for 2023 and their growth forecasts. We assume that trade growth will be lower than the average growth rate of global GDP – 2% vs. 3% due to populist movements and protectionist repatriation desires. Further, we forecast that Bitcoin will account for a certain proportion of cross-border payments, which is based on our outlook on the use of other currencies in international trade. Given the expected decline in the share of the four major currencies in international trade due to deteriorating economic and fiscal fundamentals and erosion of property rights, the market share is expected to decrease by 20%, with the RMB, BTC, emerging market currencies and gold taking over. Considered as a medium of exchange, we believe that BTC will account for 10% of cross-border payments and 5% of domestic trade.

In this base case, we expect 2.5% of central bank assets to be held in BTC. Given its importance as a store of value, we also foresee 85% of BTC being effectively removed from circulating supply as investors seek its store of value properties. Assuming a BTC velocity of about 1.5, the average velocity of U.S. currency since the global financial crisis, we calculate a value of $2.9 million for Bitcoin. Based on the global asset base, this valuation would represent 1.66% of all financial assets, compared to our estimate of just 0.1% today.

Bitcoin price scenarios in 2050: base case, bear case, bull case

We comprehensively evaluate the Bitcoin Layer 2 space by applying a valuation system for smart contract platforms (SCPs) based on end-market share projections to 2050. This valuation technique draws on our analysis of Solana, Ethereum, and their Layer 2 blockchains. Our forecasts consider the Total Address Market (TAM) revenue of enterprises that will adopt public SCPs such as Ethereum and Bitcoin L2 in the future. Based on this data, we estimate the activity rate that SCPs will charge from enterprises that deploy their services, similar to the platform fee model used by Apples App Store or Amazons online Pazar yeri.

Bitcoin is not only the core force driving the development of blockchain technology, but also the most critical blockchain platform. As a means of storing value, Bitcoin has demonstrated strong product-market fit. Currently, key members of the Bitcoin community are working hard to make Bitcoin a settlement system for smart contract platforms, a strategy similar to Ethereum. Given Bitcoins high brand influence and its more significant success than Ethereum, we foresee that Bitcoin L2 will occupy 50% of the market share in the smart contract platform market.

Assuming Bitcoin becomes a reserve asset, we expect its share of the smart contract platform market to reach about 50%. We foresee that the Bitcoin L2 space will cover thousands of L2 projects, including state channels, aggregation technologies, and new types of technologies that may emerge in the future. Assuming BTC becomes a major part of the international monetary system, in this case, financial institutions around the world will compete to establish their own L2 networks to support their BTC-related activities such as trading, exchange, and lending. Some of these solutions may be solutions that rely on centralized trust. Even so, we believe that unless Bitcoin L2 remains decentralized, its value proposition will be diluted.

We can even predict that a fractional reserve system similar to the early banking system before the emergence of fiat currency may emerge. In this case, most current blockchain technology may be converted to Bitcoin L2 to leverage the value of BTC as a strong asset. In any case, we have enough reason to believe that BTC has become one of the most important assets in the world, and Bitcoin L2 has great value-added potential by improving the practicality of Bitcoin. We predict that the valuation of the entire L2 ecosystem will reach 7.6 trillion US dollars, which is about 12.5% of the value of Bitcoin itself.

The valuation scenario for Bitcoin L2s unfolds like this:

Bitcoin has been around for over 15 years and has demonstrated remarkable resilience through multiple economic cycles. Despite being a key store of value asset, price predictions for Bitcoin over the next 25 years are based on the assumption that more and more people around the world will view Bitcoin as a medium of exchange. In fact, Bitcoins future value lies in its widespread recognition as an ideal form of money, and its potential for success lies in its unique position among monetary forms. The fragility of Bitcoins value stems from peoples subjective perceptions, which form the cornerstone of its existence. However, we believe that Bitcoins meme value as a sound currency is the most solid foundation for its survival.

The main risks to our Bitcoin thesis include:

Sustainability of Bitcoin Mining: While we take most of the premises and conclusions of “ESG” with a grain of salt, it is important to recognize the implied electricity demand required for future Bitcoin mining. This is particularly concerning from the perspective of the cost of maintaining network security. Since 2018, the Bitcoin network’s hash rate has grown at a compound annual growth rate of 71.7%, while the price has grown at a compound annual growth rate of 24%. Under our $2.9 million BTC scenario forecast, the hash rate has grown at a compound annual growth rate of 48%, and the hash rate is expected to grow from 600 M TH/s to 13.1 B TH/s. Assuming miner efficiency decreases power consumption per TH/s at a rate of 12% per year, the total power consumption of the Bitcoin network will reach 9.181 M GW/h, which is about 2.16 times the capacity of the US power grid in 2022 and equivalent to 15% of the world’s projected power generation in 2050. We predict that our Bitcoin theory may be difficult to achieve without new innovations in chip design and further breakthroughs in energy production costs.

Bitcoin consumption is expected to reach 15% of the worlds electricity supply by 2050

Failure of Miner Economics: Bitcoin is like a financial shark, requiring continuous purchases to balance miners sales, as miners face the dual pressure of fixed and variable costs. As Bitcoins inflation rate decreases, on-chain transactions must increase to support demand for BTC and cover miners expenses.

Failure to Scale: If Bitcoin fails to scale sufficiently to become a significant medium of exchange, our core argument for its rapid rise collapses.

Competition from other cryptocurrencies: We are currently in the early stages of the competition to create a more perfect, permissionless currency. While BTC is trusted for its potentially huge market cap of over $1 trillion, there are many ecosystems that are trying to carve up a piece of Bitcoins market share. These competing blockchains offer higher processing power and the ability to onboard more users into a network similar to the current financial system. While many blockchains do not promote their own currencies as money and could help promote BTC, it is very likely that many of them will try to create their own token as the perfect currency. Ethereum is one example of this, considering ETH as the currency in its ecosystem and inevitably competing with Bitcoin.

Community Split: We explored the challenges facing BTC and the costs it needs to pay to miners to maintain long-term stability. The BTC community is a group of outstanding individuals who believe in its long-term potential. However, there are significant differences among them on how to create a sustainable environment for Bitcoin. This dispute may cause the community to split again, triggering one or more Bitcoin hard forks, when the value of BTC will be divided in the new network.

Catastrophic changes in Bitcoins monetary policy: In order to maintain the long-term stability of BTC, it may be necessary to tax BTC holders. This is because the circulation velocity of BTC is extremely low, only 1/30 of the US dollar, which cannot meet the economic needs of Bitcoin miners. The possible consequence is to tax the fixed BTC through inflation and other means. Although this new type of taxation will not destroy BTC, it will undermine the inherent concept of permanent monetary policy. Changes in Bitcoin policy are like a historical scene of Caesar crossing the Rubicon. Many BTC holders may wonder whether sound monetary policy will continue to deviate from the established track.

Government Bans and Attacks: Many governments strongly believe that the monetary system should remain under federal control. If BTC becomes wildly successful, it is highly likely that countries around the world will coordinate actions to ban it. Since Bitcoins ledger is public and many wallets can be traced back to IP addresses, it is not difficult to ban Bitcoin. Given the authority of the United States in currency control, they can easily justify seizing domestic mining operations. Due to Bitcoin miners dependence on high prices, an organized attack, even if only verbally announced, would be enough to severely destabilize Bitcoin. While Bitcoin may be able to survive, organized government action will undoubtedly reduce its long-term development potential.

Controlled by Oligarchic Financial Entities: In January 2024, the approval of a Bitcoin spot ETF was celebrated by the cryptocurrency and Bitcoin community. As of the time of writing, BTC spot ETFs hold over 865,000 BTC, or about 4.1% of the total BTC supply. Over time, we believe that BTC held by large financial institutions will increase significantly. If BTC held by large financial institutions increases to a majority of the supply, many negative consequences could result. One of these could be that BTC becomes increasingly controlled by large financial institutions and governments. A more far-fetched possibility is that governments seize BTC from these centralized entities and dump it on the market to destroy the Bitcoin economic system. Another potential risk is a financial crisis caused by the rehypothecation of BTC through certain lending networks, where margin calls on BTC expose everyone to being swimming naked. At the same time, financial control of BTC by large investment firms could change the culture of BTC and lead to new policies that favor large holders and harm the interests of small holders.

Theft and Hacking: As permissionless bearer assets, assets like BTC belong to anyone who controls the private keys to move them. Hacking attacks on Bitcoin are frequent, mainly targeting centralized institutions that hold large amounts of BTC. As Bitcoin software is upgraded and second-layer solutions emerge, the surface area for hacking is expected to increase significantly. If theft by sanctioned state actors persists, it could provide more reasons for governments around the world to ban Bitcoin.

Financial Attacks: Excessive financialization has resulted in highly compensated financial practitioners who have the power to undermine poorly designed economic systems. Most famously, this dynamic has led to financial attacks on the monetary systems of G7 countries. The disruption of Bitcoin’s economic system could yield far more profits than undermining the Bank of England. Bitcoin’s economic security is directly tied to the amount of money spent to “secure” its network. With miner equity value hovering around 1.2 EV/S, this implies that the value of the enterprise to miners is about $21 billion (assuming 1.5x EV/S is generous). Meanwhile, BTC’s market cap is $1.2 trillion. A straightforward financial attack (an easy trick that BTC holders hate!) would be to buy all BTC miners, short hundreds of billions of dollars worth of BTC, and then shut down the miners. The resulting chaos could yield returns far greater than the cost of purchasing the miners. Currently, neither liquid nor secure counterparties have emerged to complete such a transaction, but that could change.

Core Software Failure: The simplicity of Bitcoin’s software strengthens its resistance to hacker attacks. The simpler the system code, the less likely it is that a vulnerability will appear that could destroy Bitcoin. Bitcoin will likely need at least two major software upgrades to remain viable. As mentioned earlier, Bitcoin must change its economic system to achieve long-term sustainability for miners. In addition, Bitcoin will also have to upgrade its encryption scheme to cope with the rise of quantum computing. Although a breakthrough in quantum computing may be years away, Bitcoin will eventually have to change key components of its system by introducing quantum cryptography. This is because quantum computing will make current encryption technology no longer secure and easy to crack. Regardless of how these major upgrades are carried out, when the Bitcoin core software is upgraded, new vulnerabilities may be introduced, threatening its long-term success.

This article is sourced from the internet: 10,000-word article: Bitcoin valuation scenarios in 2050

Related: From the hottest to the worst, the rise and fall of Friend.Tech

As the market goes up and down, the prices of some altcoins will never return to their original levels. Products and businesses may also be gone forever. In the daily question of What to play today, will anyone mention the name Friend.Tech? However, you didn鈥檛 say this a year ago: Friend.Tech is the new trend of SocialFi, the darling of Paradigm鈥檚 investment, the hot topic that all research reports are competing to write about, and the god of wealth that liberates the KOL fan economy… How come he has now become an abandoned pawn that even dogs dont play with? Attention is not eternal. The once popular encryption products have already fallen from the altar inadvertently. But the crypto market has memory, so let鈥檚 take a brief look back to…