Task

Ranking

已登录

Bee登录

Twitter 授权

TG 授权

Discord 授权

去签到

下一页

关闭

获取登录状态

My XP

0

ผู้แต่งต้นฉบับ : YB

ต้นฉบับแปล: ลูฟี่, Foresight News

ในเดือนพฤษภาคม 2021 Byrne Hobart เขียนบทความอันยอดเยี่ยมชื่อว่า “ Stripe และเศรษฐกิจที่มั่นคง ” ซึ่งเขาได้แสดงความเห็นไว้ดังนี้:

รถยนต์ สเปรดชีต Excel คอมพิวเตอร์หลอดสุญญากาศ โปรแกรมเรียกซ้ำที่ใช้งานไม่ดี และความพยายามที่จะชนะเกมวางแผนแบบเรียลไทม์ ล้วนล้มเหลวด้วยเหตุผลเดียวกัน นั่นคือ มีชิ้นส่วนที่เคลื่อนไหวจำนวนมาก และยิ่งชิ้นส่วนที่เคลื่อนไหวมากเท่าไร ก็ยิ่งมีแนวโน้มที่จะพังมากขึ้นเท่านั้น

เขาสังเกตว่า Stripe เป็นบริษัทที่มีคุณค่าเนื่องจากสามารถผสมผสานฟังก์ชันธุรกิจต่างๆ ที่จำเป็นสำหรับการชำระเงินออนไลน์ได้อย่างลงตัว

อย่างไรก็ตาม ปัญหาคือ Stripe จำกัดอยู่แค่เพียงด้านอีคอมเมิร์ซ ซึ่งถูกจำกัดโดยสถาบันของระบบการเงินโลก

ปรากฏว่าจริงๆ แล้วไม่มีระบบการชำระเงินระดับโลก “ระบบเดียว” บางประเทศมีระบบการชำระเงินหลายระบบ โดยบางระบบอาจทับซ้อนกันในบางลักษณะ และการเข้าร่วมในระบบเหล่านี้ต้องได้รับการอนุมัติจากรัฐบาล อนุญาตจากธนาคาร พัฒนาเทคโนโลยี และต้องปฏิบัติตามข้อกำหนดและบำรุงรักษาอย่างต่อเนื่อง

กล่าวอีกนัยหนึ่ง การชำระเงินทั่วโลกเป็นเรื่องยากเนื่องจากผลกระทบของเครือข่ายระหว่างสกุลเงินไม่แข็งแกร่ง ผู้คนใน การเข้ารหัสลับวงการสกุลเงินรู้ไว้ว่า: นี่คือมูลค่าหลักของ DeFi

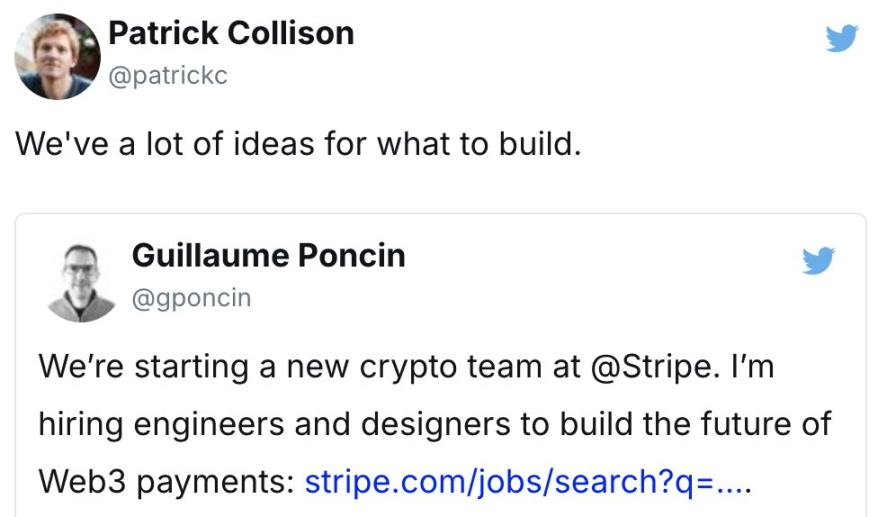

แล้วทำไมฉันถึงหยิบเรื่องนี้ขึ้นมาพูดล่ะ เพราะตอนนี้ Twitter กำลังตื่นเต้นกับข่าวการที่ Stripes เข้าซื้อกิจการ Bridge ด้วยมูลค่า 1,100 ล้านดอลลาร์

การเฉลิมฉลองถือเป็นเรื่องที่ถูกต้อง... นี่คือชัยชนะของสกุลเงินดิจิทัล! การเดิมพันของพี่น้องตระกูล Collison ในสกุลเงินดิจิทัลกำลังส่งสัญญาณไปยังผู้เล่นรายอื่นๆ ในอุตสาหกรรมเทคโนโลยีทางการเงิน

การซื้อกิจการครั้งนี้ถือเป็นการซื้อกิจการครั้งใหญ่ที่สุดในประวัติศาสตร์ของสกุลเงินดิจิทัล ตามมาด้วย Coinbase (การซื้อกิจการ Bison Trails มูลค่า $475 ล้านในปี 2021) และ Binance (การซื้อกิจการ Coinmarketcap มูลค่า $400 ล้านในปี 2020)

สิ่งที่ทำให้ฉันประหลาดใจเกี่ยวกับข่าวนี้ไม่ใช่การเข้าซื้อกิจการ แต่เป็นการที่ฉันไม่ได้ตระหนักเลยว่าระบบนิเวศของ Stablecoin นั้นมีขนาดใหญ่กว่าผู้ต้องสงสัยโดยทั่วไปอย่าง Circle (USDC) และ Bitfinex (USDT) มาก

โดยส่วนใหญ่ Bridge ไม่ได้อยู่ในเรดาร์ด้วยซ้ำ ในช่วง 2 ปีครึ่งที่ผ่านมา พวกเขาได้สำรวจพื้นที่ stablecoin อย่างเงียบๆ พยายามค้นหาว่าพวกเขาสามารถสร้างความแตกต่างได้ดีที่สุดที่ใด

ในที่สุดผู้ก่อตั้งร่วมของ Bridge อย่าง Zach และ Sean ก็พบว่า Stablecoin Orchestration คือคำตอบ ซึ่งเป็นเพียงวิธีที่แปลกใหม่ในการบอกว่าชุด API ของพวกเขาทำให้การแปลงระหว่าง stablecoin และสกุลเงินต่างประเทศเป็นเรื่องง่าย และในทางกลับกัน

เหตุใดการซื้อกิจการครั้งนี้จึงเหมาะกับ Stripe เป็นอย่างดี เนื่องจาก Bridge ช่วยให้ Stripe สามารถกำจัดส่วนที่เคลื่อนไหวมากเกินไปและรวมกระบวนการชำระเงินให้เป็นหนึ่งเดียวได้

แต่สิ่งนี้หมายถึงอะไร และการเข้าซื้อกิจการครั้งนี้มีผลกระทบต่อธุรกิจสตาร์ทอัพด้านการเงินและสกุลเงินดิจิทัลแบบดั้งเดิมอื่นๆ อย่างไร

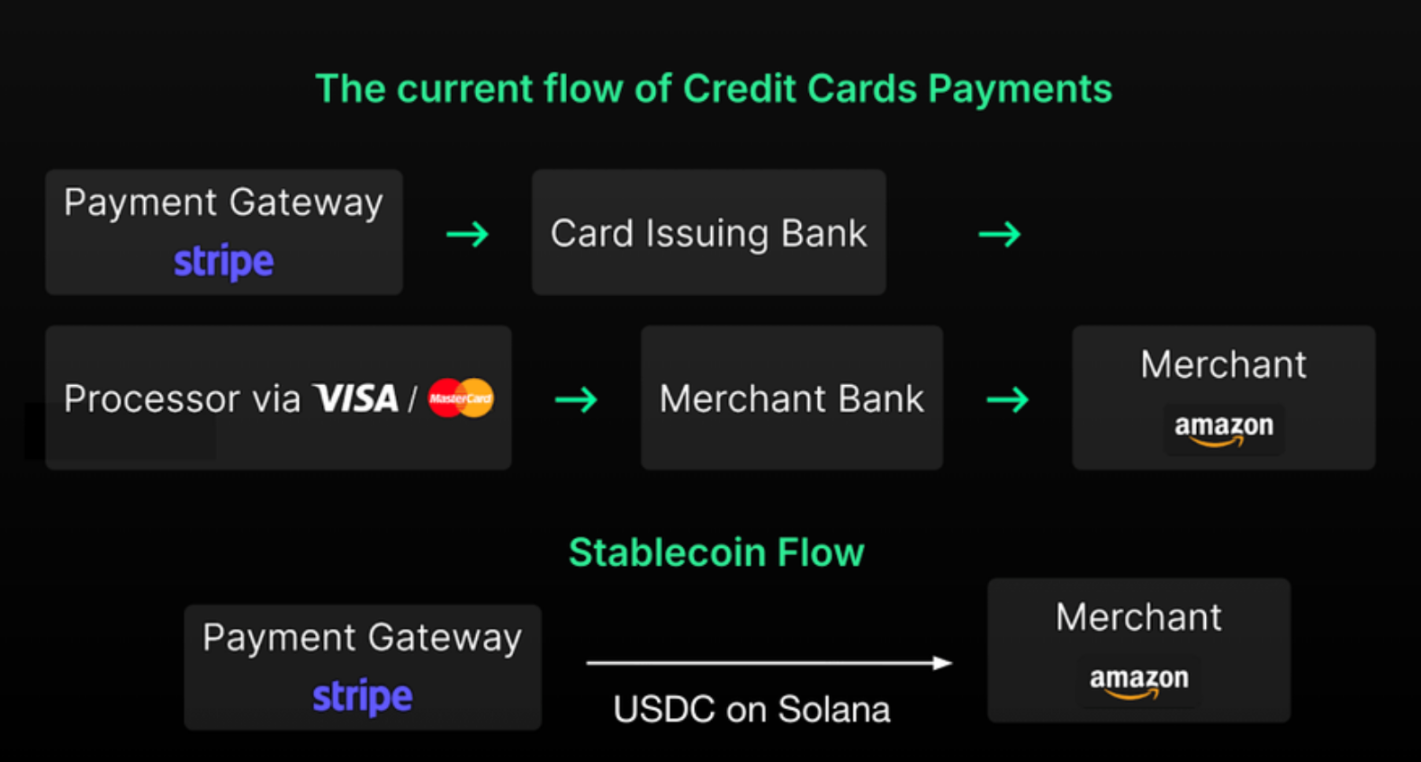

เมื่อใช้ Stripe คนส่วนใหญ่ไม่ทราบว่าผลิตภัณฑ์นี้จัดการกระบวนการระหว่างผู้ถือผลประโยชน์ต่างๆ เช่น ธนาคาร เครือข่ายการชำระเงิน และ SWIFT สำหรับการโอนเงินทั่วโลก เป็นต้น

แต่ตามที่ Byrne กล่าวไว้ Stripe ช่วยให้การชำระเงินออนไลน์เป็นไปได้

Stripe เป็นบริษัทในกลุ่มที่สร้างมูลค่าเพิ่มที่น่าสนใจ ซึ่งให้บริการที่ทำให้กระบวนการบางอย่างดำเนินไปตามที่คุณจินตนาการไว้ แม้ว่าคุณจะไม่เคยลองใช้มันมาก่อนก็ตาม

อย่างไรก็ตาม คนกลางเหล่านี้ไม่เพียงแต่เพิ่มความล่าช้าในการโอนและการชำระเงิน ซึ่งทำให้กระบวนการของ Stripes ไม่มีประสิทธิภาพ แต่ยังดึงค่าธรรมเนียมส่วนหนึ่งจากห่วงโซ่คุณค่าอีกด้วย

ปัญหานี้ไม่ได้เกิดขึ้นเฉพาะกับ Stripe เท่านั้น แต่ PayPal ก็ประสบปัญหาเดียวกัน ซึ่งน่าจะเป็นเหตุผลหลักที่ทำให้พวกเขาเปิดตัวสกุลเงินดิจิทัลที่มีเสถียรภาพอย่าง PYUSD เมื่อเดือนสิงหาคมปีที่แล้ว

ด้วยการบูรณาการ Stablecoin บริษัท FinTech เหล่านี้ก็ก้าวเข้าใกล้การครอบครองห่วงโซ่มูลค่าการชำระเงินออนไลน์ทั้งหมดอีกขั้นหนึ่ง

ดังที่ฉันได้กล่าวไปข้างต้น บริษัทชำระเงิน เช่น PayPal และ Stripe ทำงานร่วมกับธนาคารที่มีอยู่เพื่อถือเงินของผู้ใช้ แต่ด้วยการใช้ stablecoin พวกเขาจึงสามารถมีอำนาจตัดสินใจที่มากขึ้นในการจัดการมูลค่าของธุรกรรมบนเครือข่ายของพวกเขา

คำพูดนี้มาจากรายงานของ Delphi Digital เกี่ยวกับผลิตภัณฑ์ crypto ซึ่งอธิบายถึงแรงจูงใจทางการเงิน:

…ด้วยการให้ผู้ใช้ถือ pyUSD ผ่านระบบชำระเงินของ PayPal (เช่น Venmo) PayPal จึงกลายเป็นธนาคารอย่างแท้จริง จากนั้น PayPal สามารถนำเงินของผู้ใช้ไปฝากไว้ในคลังของตนและรับผลตอบแทน ซึ่งไม่เพียงแต่ช่วยให้ PayPal ลดค่าธรรมเนียมการชำระเงินให้เหลือศูนย์เท่านั้น แต่ยังสามารถจ่ายค่าตอบแทนแก่ผู้ใช้หรือรับรายได้บางส่วนจากยอดคงเหลือ pyUSD ที่ไม่ได้ใช้งานอีกด้วย ซึ่งถือเป็นข้อได้เปรียบเหนือคู่แข่งแอปชำระเงิน Web2 อื่นๆ

พวกเขาสร้างธนาคารขึ้นมาเอง ซึ่งเป็นแรงจูงใจหลักของยักษ์ใหญ่ด้านเทคโนโลยีทางการเงิน จากมุมมองทางธุรกิจ ประเด็นนี้อาจมีความสำคัญมากกว่าความเร็วของธุรกรรมและการชำระเงินที่เร็วขึ้น

สิ่งที่น่าสนใจที่ต้องชี้ให้เห็นคือ PayPal และ Stripe มีแนวทางที่แตกต่างกัน

การตัดสินใจของ PayPal ที่จะออก stablecoin ของตัวเองหมายความว่าพวกเขามุ่งเน้นไปที่การจัดการเงิน การเดิมพันของ Stripe ในเลเยอร์การแปลงแสดงให้เห็นว่าพวกเขามุ่งเน้นไปที่โครงสร้างพื้นฐานของ stablecoin พวกเขาเลือกเส้นทางของตนเองเพราะว่ามันเหมาะกับเทคโนโลยีปัจจุบันของพวกเขา

ในระดับสูง Stripe เป็นบริษัท API การชำระเงิน และ Bridge ก็สอดคล้องกับแนวคิดนั้น Stripe จำเป็นต้องรวม API ของ stablecoin ของ Bridge เข้ากับเอกสารสำหรับนักพัฒนาของตนเองเท่านั้น

PayPal เติบโตได้ดีจากฐานผู้ใช้ปลีกขนาดใหญ่ผ่านบริการฟรอนต์เอนด์อย่าง Venmo ดังนั้น ทีมงานด้านคริปโตจึงมุ่งเน้นไปที่การปรับปรุงวิธีการจัดการยอดคงเหลือของผู้ใช้และใช้ประโยชน์จากเงินทุนนี้ การออกสกุลเงินดิจิทัลที่มีเสถียรภาพของตนเองอย่าง PYUSD ช่วยให้ PayPal สามารถจัดการเงินได้อย่างมีประสิทธิภาพมากขึ้น

ในความเห็นของฉัน เป็นเรื่องหลีกเลี่ยงไม่ได้ที่ทั้งสองบริษัทจะต้องทำให้สแต็กของ stablecoin ทั้งหมดเป็นแนวตั้ง การจัดหาเครื่องมือภายในสำหรับการออก stablecoin การจัดการกองทุน บัตรเดบิต กระเป๋าเงินคริปโต ฯลฯ ถือเป็นสิ่งสำคัญ ดูเหมือนว่าจะไม่ต้องคิดมาก เพราะการมีสแต็กแบบเต็มรูปแบบภายในบริษัทจะทำให้บริษัทต่างๆ สามารถมอบประสบการณ์ผู้ใช้ที่ดีที่สุดและครองส่วนแบ่งในห่วงโซ่มูลค่าการชำระเงินได้มากขึ้น

กล่าวอีกนัยหนึ่งอย่าแปลกใจหากคุณเห็น Stripe เปิดตัวกระเป๋าเงินอัจฉริยะและบัตรเดบิตคริปโตของตัวเอง

นอกจากนี้ สิ่งที่น่าสังเกตก็คือ การออกโทเค็นถือเป็นแหล่งรายได้หลักของ stablecoin ตัวอย่างเช่น Tether สร้างกำไรได้มากกว่า BlackRock ในไตรมาสที่สี่ของปี 2022 ดังนั้น ในขณะที่ Stripe สำรวจแนวคิด stablecoin ที่หลากหลายกับผู้ใช้ พวกเขาจะเปิดตัว stablecoin ในที่สุดเพื่อช่วยให้ผู้ค้าเข้าร่วมได้อย่างรวดเร็ว และให้แรงจูงใจในการใช้ stablecoin ดั้งเดิมของระบบนิเวศของตน

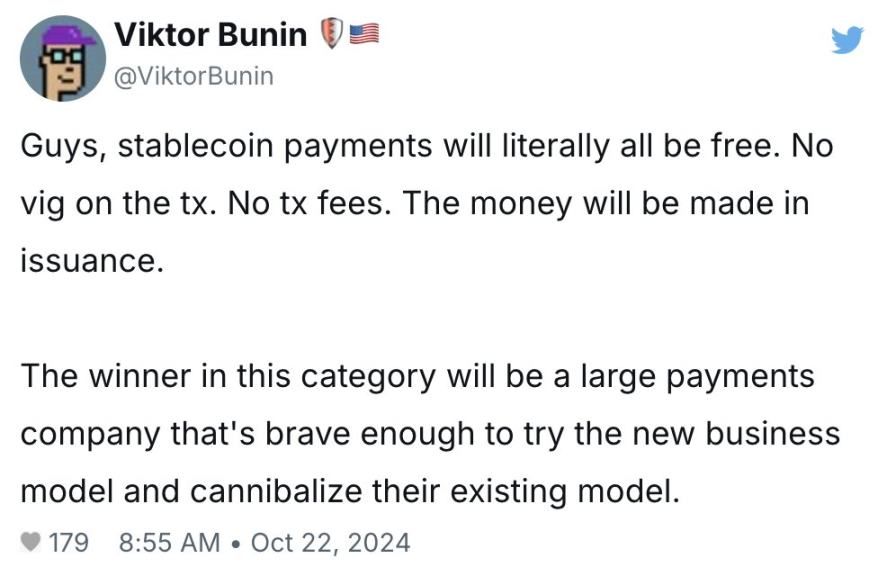

ทั้ง Stripe และ PayPal ต่างก็มีสถานะที่แข็งแกร่งทั่วโลกและจะพยายามเชื่อมต่อกับโครงสร้างพื้นฐานของ stablecoin ภายในเครือข่ายที่มีอยู่ ดังที่ Viktor ได้กล่าวไว้ข้างต้น ในช่วง 5 ปีข้างหน้า บริษัทต่างๆ ที่ “กินส่วนแบ่งตลาดแบบเดิม” ก่อนผู้เข้าร่วมตลาดรายอื่นจะได้รับประโยชน์อย่างมาก

ตอนนี้คุณอาจกำลังคิดว่า: หาก Stripe และ PayPal ทุ่มกลยุทธ์ stablecoin ทั้งหมด นั่นจะเป็นภัยคุกคามครั้งใหญ่ต่อเครือข่ายการชำระเงินอย่าง Visa และ Mastercard หรือไม่

แท้จริงแล้ว นั่นเป็นเหตุผลที่ Visa และ Mastercard เริ่มพัฒนาแผนการของตัวเองแล้ว เพื่อไม่ให้พลาดโอกาสของการปฏิวัติ stablecoin ตัวอย่างเช่น Visa กลายเป็นเครือข่ายการชำระเงินรายแรกที่ยอมรับ USDC ในปี 2020 ขณะที่ Mastercard เปิดตัวบริการบัตรเครดิต crypto ของตัวเอง

แต่ฉันสงสัยว่าการที่ Stripe เข้าซื้อ Bridge ได้เร่งดำเนินกลยุทธ์ stablecoin ของทีมงานด้านคริปโตในบริษัทการเงิน/ฟินเทคดั้งเดิมขนาดใหญ่เหล่านี้

ส่วนธนาคารล่ะ? พูดตรงๆ ว่าฉันไม่แน่ใจว่าพวกเขาจะมีกลยุทธ์ตอบสนองอย่างไร เห็นได้ชัดว่า Stablecoin ทำลายตำแหน่งของพวกเขาในฐานะผู้ให้บริการชำระเงินระหว่างประเทศและการเก็บรักษาเงินฝากของผู้ใช้ แต่ข้อดีของพวกเขาคือพวกเขาปฏิบัติตามกฎระเบียบของรัฐบาล และพวกเขาอาจโน้มเอียงไปทางการเพิ่มขึ้นของ CBDC?

ตัวอย่างเช่น ประเทศ BRICS เพิ่งประกาศว่ากำลังเปิดตัวสกุลเงินดิจิทัลของตนเองเพื่อลดการพึ่งพาเงินดอลลาร์สหรัฐฯ เป็นที่ชัดเจนว่าธนาคารต่างๆ จะคว้าโอกาสนี้ในการพัฒนากลยุทธ์ CBDC ของตนเองเพื่อแข่งขันชิงส่วนแบ่งตลาดใหม่นี้

ไม่ว่าคำตอบสำหรับผู้มีส่วนได้ส่วนเสียทางการเงินแบบดั้งเดิมเหล่านี้จะเป็นอย่างไร ธีมโดยรวมก็ยังคงสอดคล้องกัน: Stablecoin ได้เข้าสู่เวทีทางการเงินแล้ว

คำถามในตอนนี้ก็คือ สถาบันขนาดใหญ่ใดบ้างที่จะต้อนรับผู้เข้ามาใหม่ในระบบการเงินด้วยอ้อมแขนที่เปิดกว้างและกลายมาเป็นมิตรกับ Stablecoin อย่างรวดเร็ว

ในทางหนึ่ง ผู้เล่นหลายรายในระบบการเงินแบบดั้งเดิมเริ่มมีหน้าตาคล้ายคลึงกันมาก เนื่องจากพวกเขาทั้งหมดต่างมองหาการใช้ Stablecoin เพื่อให้บริการทางการเงินแบบครบวงจร (การชำระเงิน ธนาคาร บริการบัตร ฯลฯ)

จนถึงตอนนี้ เราได้อธิบายผลกระทบของ Stablecoin ต่อผู้เล่น Fintech ทั้งหมดแล้ว แต่จะเกิดอะไรขึ้นกับ Stablecoin ที่เป็นสกุลเงินดิจิทัลที่เพิ่งเกิดใหม่?

จากการวิจัยครั้งก่อนของฉัน ผู้ก่อตั้งในกลุ่ม Stablecoin จำเป็นต้องเลือกผู้ที่พวกเขาจะให้บริการ:

บริษัทการเงินแบบดั้งเดิม/เทคโนโลยี Web3

ผู้ใช้สกุลเงินดิจิทัลแบบออนเชน

ประการแรกคือเป้าหมายที่ชัดเจนของการซื้อกิจการ Bridge ของ Stripe ส่วนประการที่สองเป็นการชี้ให้เห็นถึงอนาคตอันยาวไกลของโครงสร้างพื้นฐาน Stablecoin ดั้งเดิมของ DeFi ที่กำลังจะมาถึง แต่ความแตกต่างระหว่างทั้งสองคืออะไรกันแน่?

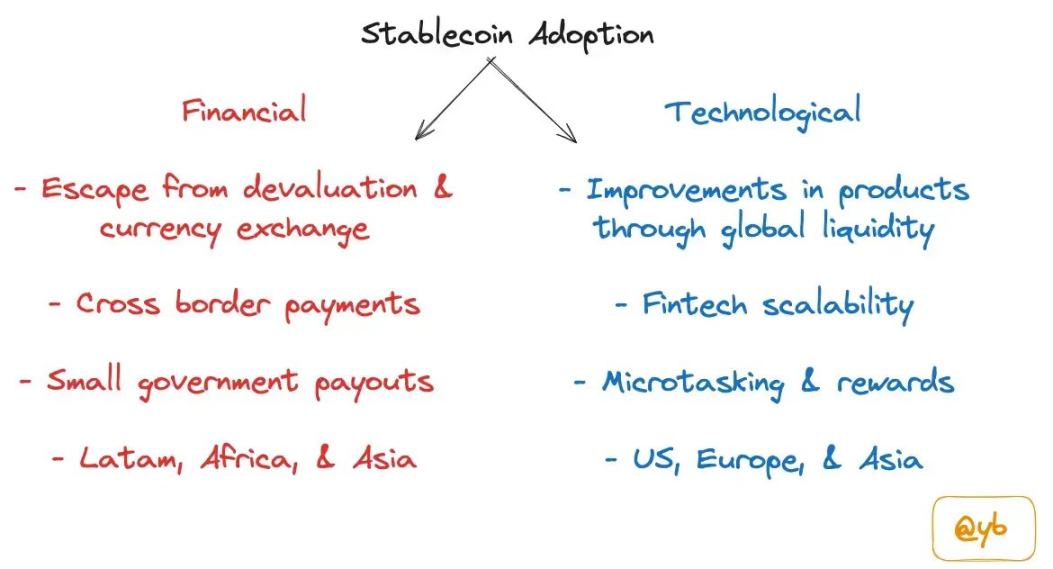

ขนาดของระบบนิเวศ stablecoin นั้นยิ่งใหญ่เกินกว่าการแทนที่บริการการชำระเงินของ fintech อย่างที่ฉันได้กล่าวไว้ใน บทความของฉัน การนำ stablecoin มาใช้มีแนวทางสองทาง หนึ่งคือพยายามปรับปรุงระบบการเงินที่มีอยู่ และอีกทางหนึ่งคือใช้ stablecoin เพื่อปรับปรุงผลิตภัณฑ์ crypto เช่น Polymarket, Bountycaster, Uniswap, Aave เป็นต้น

กลุ่มสตาร์ทอัพประเภทหนึ่งหวังที่จะกลายเป็นปลั๊กอินสำหรับผู้เล่นทางการเงินแบบดั้งเดิม เนื่องจากพวกเขาต้องการหาพันธมิตรที่แข็งแกร่งยิ่งขึ้น รวมถึง Paxos, Ondo Finance, Brale, Agora, Coinflow และ Sphere

สตาร์ทอัพประเภทอื่น ๆ ให้ความสำคัญกับโครงสร้างพื้นฐานของสกุลเงินดิจิทัลที่กระจายอำนาจอย่างสมบูรณ์ เช่น Prerna, Gnosis Pay, Based App และ Picnic บริษัทเหล่านี้หวังว่าจะสามารถแข่งขันกับผลิตภัณฑ์อย่าง Stripe และ PayPal ได้โดยตรง โดยมุ่งเป้าไปที่กลุ่มลูกค้าที่ชื่นชอบสกุลเงินดิจิทัล และช่วยปรับปรุงประสบการณ์บนเครือข่ายผ่านแอปพลิเคชันที่รองรับสกุลเงินดิจิทัล

เมื่อกล่าวเช่นนั้น ฉันคิดว่าผู้ก่อตั้งควรพิจารณากลยุทธ์แบบบาร์เบลล์สำหรับสกุลเงินดิจิทัลที่มีเสถียรภาพ เรากำลังให้บริการแก่บริษัทการเงินแบบดั้งเดิมที่ต้องการเข้าสู่พื้นที่สกุลเงินดิจิทัลที่มีเสถียรภาพอย่างหลีกเลี่ยงไม่ได้หรือไม่ หรือเรากำลังสร้างโครงสร้างพื้นฐานของสกุลเงินดิจิทัลที่มีเสถียรภาพสำหรับแอปพลิเคชัน DeFi และกำลังทดลองการทดลองใหม่ ๆ ที่ไม่สมเหตุสมผลสำหรับ Stripe และ PayPal หรือไม่

ในมุมมองของฉัน บริษัทที่พยายามตรวจสอบซ้ำจะต้องพ่ายแพ้ต่อผู้เล่นทางการเงินแบบดั้งเดิมที่มีช่องทางการจัดจำหน่าย หรือพ่ายแพ้ต่อผู้เล่น DeFi ที่ปรับแต่งผลิตภัณฑ์ให้มีฟังก์ชันบนเชนที่ไม่ซ้ำใคร

โพสต์ของวันนี้คือการแบ่งปันความคิดเริ่มแรกของฉันหลังจากที่ได้ยินข่าวการเข้าซื้อ Bridge แต่ฉันยังไม่พบคำตอบที่เป็นความหมายสำหรับคำถามต่อไปนี้:

คูน้ำในสแต็กของ Stablecoin อยู่ที่ไหน?

ผู้เล่น Web2 Fintech รายอื่นจะเข้าร่วมได้อย่างไร?

หากมีการซื้อกิจการอีกครั้ง จะเป็นของใคร?

ในอีกไม่กี่เดือนข้างหน้า การพัฒนาในพื้นที่ Stablecoin จะมีความน่าสนใจเพิ่มมากขึ้น

บทความนี้มีที่มาจากอินเทอร์เน็ต: สตาร์ทอัพ Stablecoin แยกทางกัน: TradFi หรือ DeFi?