My XP

0

Login

บทความต้นฉบับโดย: Gaurav Gandh

ต้นฉบับแปล: TechFlow

Exchanges are the foundation of capital markets and achieve their core purpose by facilitating the trading of assets between participants. The core goal of any exchange is to enable efficient (low transaction costs and slippage), fast, and secure trading between counterparties. Decentralized exchanges (DEXs) add a layer of trustlessness to this goal, aiming to eliminate the need for intermediaries and centralized control. DEXs let users retain control of their funds, allow for community participation, and promote open innovation. However, these benefits have historically often been accompanied by higher latency and lower liquidity due to the throughput and latency limitations of the underlying blockchain.

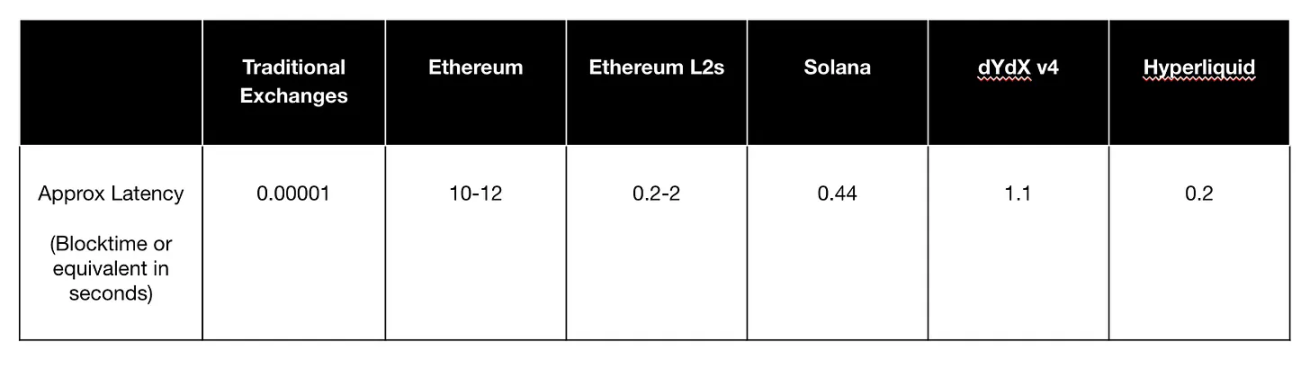

Source: Chainspect, select block explorers

Spot DEXs now account for 15-20% of total spot trading volume, while perpetual contracts account for only 5%. When it comes to perpetual contracts, centralized exchanges (CEXs) have two main advantages – a better user experience for ordinary investors and tighter spreads due to effective control by market makers. The collapse of FTX has further consolidated the industry, and now only a few CEXs dominate the market. This centralization poses a potential risk to the crypto ecosystem. The widespread popularity of decentralized exchanges can not only reduce this risk, but also support the long-term sustainable growth of the entire ecosystem.

Source: The Block

In this article, we took a deep dive into the existing perpetual DEX ecosystem and reviewed what the optimal design of a decentralized perpetual exchange might be. The rise of second-layer solutions and multi-chain environments provide a good foundation for innovation in liquidity acquisition and user experience. Based on research and knowledge from previous attempts, we believe we are now entering the golden age of DEX. Finally, we explored how perpetual DEXs might drive the adoption of cryptocurrencies among mainstream audiences, beyond the core function of facilitating efficient trading.

Perpetual contracts have found product-market fit (PMF) in the crypto ecosystem for both speculation and hedging.

Perpetual contracts are futures contracts with no expiration date, allowing traders to hold positions indefinitely. These contracts are similar to over-the-counter swaps that traditional financial institutions have offered for decades. However, by introducing the concept of funding rates, cryptocurrencies have democratized this product, which has historically been available only to qualified participants, and now opens it up to ordinary investors.

The perpetual market currently has over $120 billion in monthly trading volume, creating an efficient trading venue with a central limit order book, a clear user interface, and fast and secure trading through a vertically integrated clearing system. In addition, projects like Ethena have built on top of perpetual contracts, expanding the use of perpetual contracts beyond speculation.

Perpetual contracts have several advantages over traditional futures contracts:

Traders save on transaction fees and other costs of renewing futures contracts each time they expire.

Investors avoid high rolling costs due to more expensive forward contracts.

The settlement/funding mechanism provides continuous realized profit and loss, simplifying the back-end processes for contract holders and clearing systems.

Contracts provide a smoother price discovery process, avoiding the price jumps that occur when switching from one month’s contract to the next.

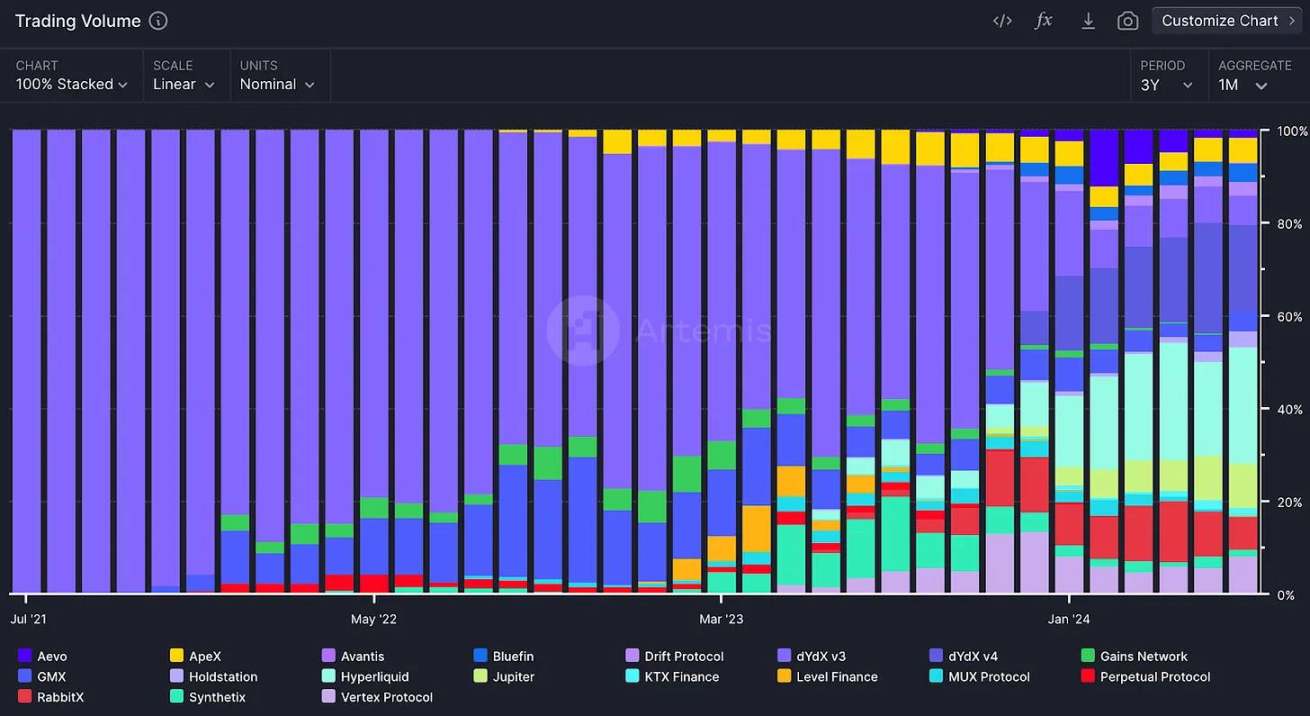

Source: Perpetual DEX Market Share – Artemis

Since BitMEX introduced the concept in 2016, the market has experienced a Cambrian explosion of perpetual DEXs, with over 100 implementations now in existence. While the market was initially dominated by dYdX, today we have a vibrant ecosystem across chains. Perpetual contracts are now an essential part of the crypto ecosystem – various lead-lag studies show that perpetual markets begin to facilitate price discovery when spot markets are inactive. Perpetual volume on DEXs has grown from $1 billion in July 2021 to $120 billion in July 2024, a CAGR of approximately 393%.

However, in order for the market to mature further, the fundamental challenges of high latency and low liquidity must be addressed to create a cheap and efficient trading environment. High liquidity reduces slippage and provides a smoother trading experience. Low latency helps market makers quote tighter, execute trades quickly, and improve active quote liquidity, forming a positive feedback loop.

In the pursuit of the “holy grail” of decentralized exchanges (DEX), a variety of implementations have emerged, from oracle models to virtual automated market makers (vAMMs) to “off-chain order books and on-chain settlement.”

The oracle model provides trades based on price data from high-volume leading exchanges. This approach eliminates the cost of closing the gap between DEX prices and market prices, but also carries a greater risk of oracle price manipulation. Platforms like GMX benefit from their liquidity depth, offer zero price impact trades and fixed fees, and demonstrate organic growth. By using protocols such as Chainlink to provide price data, GMX ensures price accuracy and integrity, promotes a price taker-friendly environment, and provides adequate rewards for price makers. However, the main challenge faced by these exchanges is that they act as price takers rather than facilitating price discovery.

Virtual AMMs (vAMMs) facilitate the trading of perpetual contracts without involving actual spot exchanges, and are inspired by Uniswaps spot market AMM. This model, adopted by platforms such as Perpetual Protocol and Drift Protocol, allows for decentralized, composable liquidity bootstrapping for new tokens. Despite the problems of high slippage and impermanent loss, vAMMs provide a transparent on-chain price discovery mechanism. By adjusting the virtual depth (K value), these exchanges balance the need for liquidity with the risk of excessive depth or high slippage, aiming to achieve a sustainable model.

To overcome the limitations of on-chain matching, some DEXs use off-chain order books and on-chain settlement. Trade matching occurs off-chain, while execution and asset custody remain on-chain. This approach maintains the self-custody advantages of DeFi while addressing performance and risk limitations such as miner extractable value (MEV). Notable examples include dYdX v3, Aevo, and Paradex, which utilize this hybrid approach to provide efficient trading while ensuring transparency and security through on-chain settlement.

Fully on-chain order books represent the best way to maintain transaction integrity, but face significant challenges due to blockchain latency and throughput limitations. These issues lead to vulnerabilities such as front-loaded trades and market manipulation. However, chains like Solana and Monad are rapidly attempting to solve this challenge at the infrastructure level. Projects like Hyperliquid, dYdX v4, Zeta Markets, LogX, and Kuru Labs are also pushing for high-performance fully on-chain systems, either leveraging existing chains or creating their own application chains.

The main trends in the perpetual DEX space right now are community-driven cross-chain active liquidity and simple user experience through gas-free transactions, session keys, and social login.

Historically, building liquidity on exchanges has been a cold start problem. Exchanges acquire liquidity through a combination of incentives, rewards, and market forces. Market forces are essentially traders looking to exploit arbitrage opportunities between different markets. However, with the proliferation of DEXs competing for users’ attention, it has been difficult for DEXs to attract enough traders to reach critical mass. In the perpetual DEX space, another popular approach is through liquidity pools with incentives and rewards. In this setup, liquidity providers (LPs) deposit their assets into a pool, which is then used to facilitate trades on the DEX. Some perpetual DEXs offer high annualized yields (APYs) in vaults or airdrops to attract liquidity providers. Recently, two main approaches have emerged to more effectively solve this cold start challenge – community-supported active liquidity vaults and cross-chain liquidity acquisition.

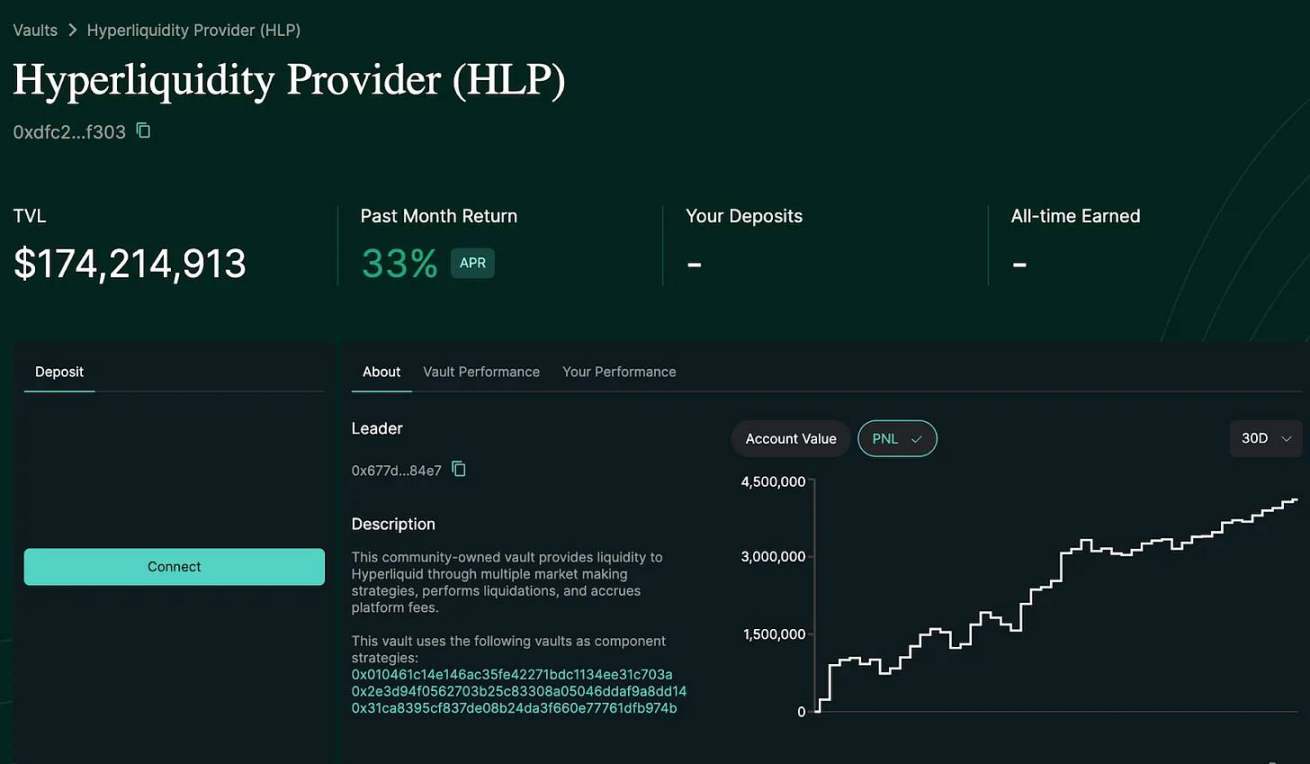

Hyperliquid has launched the HLP Treasury, which uses users funds to provide liquidity for the Hyperliquid exchange. The Treasury uses data from Hyperliquid and other exchanges to calculate fair prices and execute profitable liquidity strategies across a variety of assets. The profits and losses (PL) generated by these activities are distributed according to the participants shares in the Treasury. In addition to community-led liquidity, Hyperliquid also uses HyperBFT to improve the performance of DEX through optimistic execution and responsiveness. Optimistic execution means that transactions in a block can be executed before the block is finalized at the consensus level. This means that as soon as a block is proposed, validators begin executing transactions in the block in parallel with the consensus process. Optimistic responsiveness allows consensus to scale based on the number of validators that can establish consensus and network conditions. Currently, a major risk of Hyperliquid is the lack of open source and transparent infrastructure code. Similar to Hyperliquid, multiple projects are increasingly adopting an application chain-based approach to overcome some of the inherent limitations of the underlying blockchain.

Source: Hyperliquid

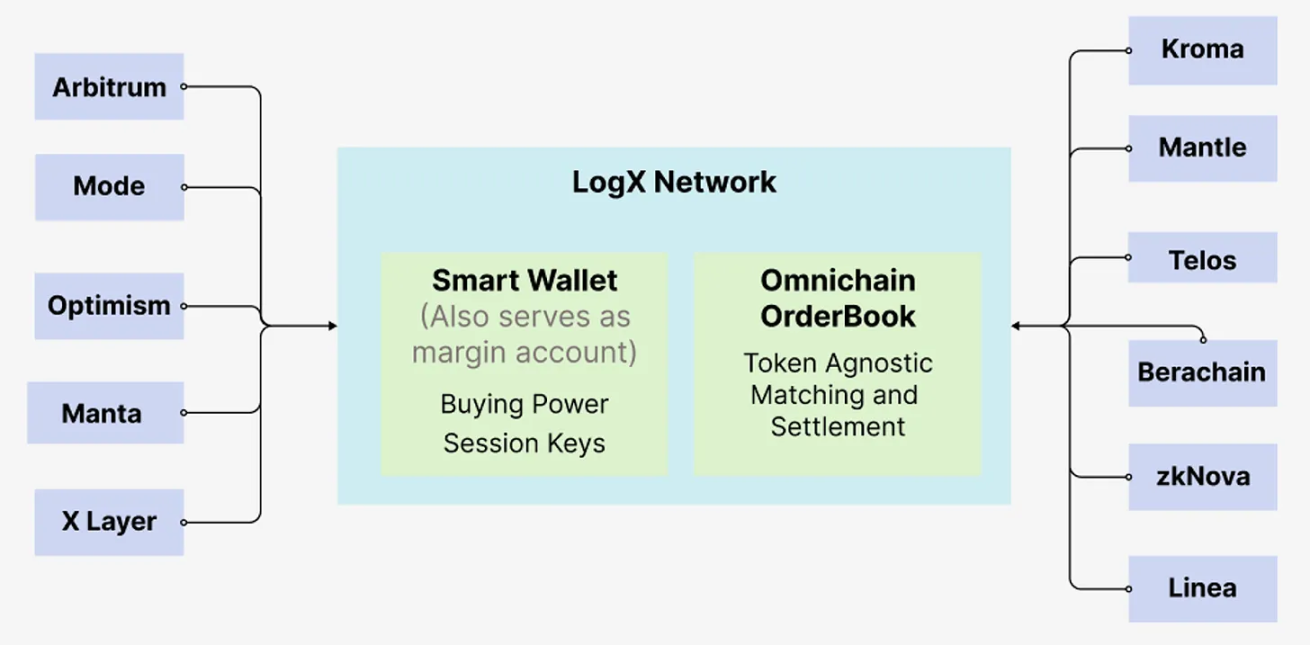

Another interesting approach is cross-chain liquidity acquisition by projects like Orderly Network and LogX Network. These networks allow the creation of front ends on any chain to trade perpetual contracts and tap into liquidity across all markets. By combining native liquidity on the chain, aggregated liquidity across other chains, and creating discrete asset, market neutral (DAMN) AMM pools, LogX can maintain liquidity during periods of high market volatility. These pools use stable assets like USDT, USDC, and wUSDM to enable traders to trade oracle-based perpetuals. While designed for trading, this infrastructure also creates options for building a variety of applications on top of it.

Source: LogX

As user interfaces become increasingly commoditized, DEXs are beginning to add features like gas-free trading, session keys, and social logins, leveraging wallet adapters to create a smooth user experience. Traditionally, centralized exchanges (CEXs) have integrated within the ecosystem – acting as onboarding and bridging services in addition to the core exchange, while DEXs typically remain isolated within their native ecosystems. These cross-chain DEXs are also revolutionizing the user experience by enabling seamless trading across multiple blockchain networks, and providing users with a wider selection of trading pairs, with tighter spreads on certain long-tail tokens.

DEX aggregators such as Vooi.io are also building integrated smart routing systems to find the most efficient trading paths or best venues to execute on various chains. This simplifies the trading process for users, who can manage complex trading routes in a single interface. These super aggregators combine the functionality of multiple DEXs and bridges to provide a smooth and user-friendly trading experience.

Telegram bots further simplify the trading experience for users, providing real-time trading alerts, executing trades, and managing portfolios, all from the convenience of the Telegram chat interface. This integration enhances accessibility and user engagement, making it easier for traders to stay informed and quickly act on market opportunities. The listing of the BANANA token on Binance is a big win for the emerging Telegram bot ecosystem. However, Telegram bots come with significant risks because users must share their private keys with the bot, exposing them to smart contract risks.

Perpetual decentralized exchanges (DEX) are constantly introducing new financial products or creating mechanisms to simplify the trading process of existing products to meet the ever-changing needs of traders.

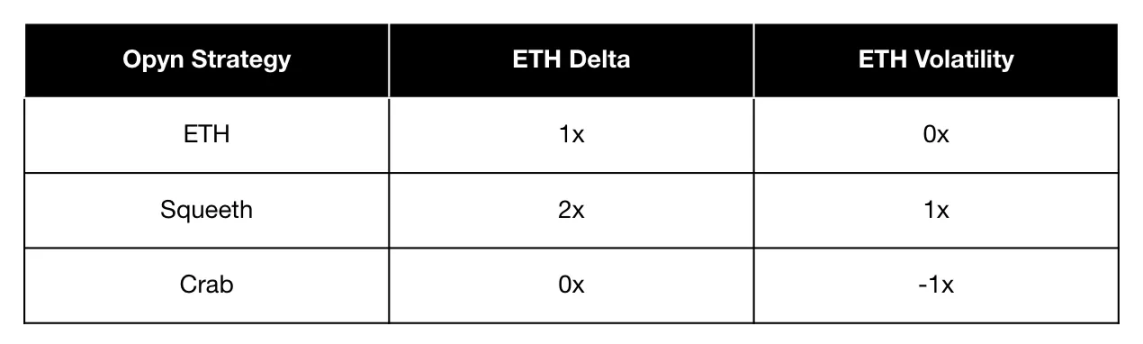

These innovative financial instruments allow traders to speculate on the volatility of an asset. In the highly volatile crypto market, this product provides a unique way to hedge risk or take advantage of market volatility. Opyn leverages existing markets to develop new types of perpetual contracts that can replicate complex strategies, hedge unique risks, and improve capital efficiency. Opyns perpetual products include Stable Perpetual Contracts (0-perps), Uniswap LP Perpetual Contracts (0.5-perps), Regular Perpetual Contracts (1-perps), and Square Perpetual Contracts (2-perps, also known as Squeeth). Each of these perpetual contracts serves a different purpose: Stable Perpetual Contracts provide a solid foundation for trading strategies, Uniswap LP Perpetual Contracts mirror returns without directly providing liquidity, Regular Perpetual Contracts provide simple long/short positions, and Square Perpetual Contracts amplify returns through secondary exposure. These perpetual contracts can be combined into more complex strategies. For example, the Crab strategy involves shorting 2-perps in the stable market while going long 1-perps to obtain funds. Another example is the Zen Bull strategy, which combines shorting 2-perps, longing 1-perps, and shorting 0-perps to earn money in a quiet market while maintaining long exposure.

Source: Opyn

Pre-launch token perpetual contracts allow traders to speculate on the future price of a digital asset before it is officially launched, acting as an on-chain gray market version of an IPO. These contracts enable investors to trade based on expected market value. Several perpetual DEXs such as Aevo, Helix, and Hyperliquid have created unique niches in the market using pre-launch futures. The main advantage of these pre-launch contracts is their ability to attract and retain users by providing access to exclusive assets that are not available elsewhere.

Perpetual swaps may become the primary way to list real world assets (RWAs). Listing a new asset as a perpetual swap is simpler than tokenizing it, requiring only liquidity and a data feed. Additionally, spot markets do not need to exist on-chain in order for a liquid perpetual market to exist on-chain, as perpetual swaps can exist independently. In this case, perpetual swaps become a springboard for spot tokenization once enough market interest/liquidity is established through perpetual swaps. The combination of spot and perpetual swaps on RWAs opens new avenues for predicting sentiment, event-based trading, and executing cross-asset arbitrage strategies. Companies like Ostium Labs and Sphinx Protocol are some of the emerging players in this space.

Perpetual contracts can also be used to create exchange-traded products that hold expiring futures contracts, such as ETFs that hold WTI light sweet crude oil futures (such as USO) and ETNs that hold VIX futures (such as VXX) to reduce fees and net asset value (NAV) depreciation. This eliminates the need to convert their baskets into long-term contracts when expiration approaches. Companies that need protection from long-term economic exposure but do not need physical delivery of commodities can reduce operating costs through perpetual contracts. Speculating or hedging risk on restricted foreign currencies usually involves non-deliverable 30-day or 90-day forward contracts, which are non-standard and traded over-the-counter. These can be replaced with perpetual contracts denominated in US dollars.

Perpetual DEX can revolutionize prediction markets by providing a flexible and continuous trading mechanism to accommodate non-periodic markets such as elections/irregular weather forecasts. Unlike traditional prediction markets that rely on real events or oracles, perpetual futures allow the creation of prediction markets based on the markets own constantly changing data. This design makes it possible to form sub-markets within long-term markets, providing users with short-term trading opportunities and instant gratification. The continuous settlement of perpetual futures ensures regularity in market activity, enhancing liquidity and user engagement. In addition, community-controlled perpetual futures markets can incentivize participation through reputation and token rewards, and ensure alignment of interests, creating a solid foundation for decentralized prediction markets. This approach democratizes market creation and provides scalable solutions for diverse prediction scenarios.

By providing a platform for building integrated iOS-like experiences, Perpetual DEX has the potential to usher in the next era of crypto adoption.

As the crypto-financial system evolves, the design of perpetual DEXs will continue to improve. The focus will likely shift from simply replicating the functionality of centralized exchanges (CEXs) to leveraging the unique benefits of decentralization — transparency, composability, and user empowerment. Building the best perpetual DEX design requires a careful balance between efficiency, speed, and security. Perpetual DEXs are also focused on fostering community engagement through presales and engaging developers in the ecosystem. This approach fosters a sense of belonging and loyalty among users. Community-led initiatives, such as market making through Hyperliquid bots, further democratize access to trading activity.

Creating iOS-like integrations and user-friendly experiences is critical to mass crypto adoption, which in turn requires developing more intuitive user interfaces and ensuring consistency in the user journey. These can make crypto trading more attractive to the average consumer who may not be crypto natives, ultimately leading them to other decentralized applications. Perpetual DEXs like Hyperliquid, LogX, and dYdX are also able to develop user-friendly and intuitive markets in various fields outside of finance, such as elections and sports, which in turn opens new channels for mass participation.

Source: LogX

The development of DeFi over the past decade has focused on DEXs and stablecoins. However, the next decade may see DeFi consumer applications intersecting with multiple fields such as news, politics, sports, etc. These applications may become the most valuable and widely used applications, further driving crypto adoption. We look forward to working with these participants in building the future of crypto.

This article is sourced from the internet: The evolution of perpetual DEX: from niche trading venue to driver of on-chain adoption

ต้นฉบับ | Odaily Planet Daily ( @OdailyChina ) ผู้เขียน: Azuma ( @azuma.eth ) 16,038.7 bitcoins ซึ่งมีมูลค่ารวมกว่า $900 ล้านดอลลาร์สหรัฐ เป็นจำนวน BTC ที่รัฐบาลเยอรมันโอนไปยังการแลกเปลี่ยนและผู้สร้างตลาด (ซึ่งบางส่วนถูกถอนออกไปแล้ว) ในหนึ่งวันเมื่อวานนี้ ตั้งแต่เริ่มขาย BTC เมื่อวันที่ 19 มิถุนายน รัฐบาลเยอรมันยังคง "ทิ้งตลาด" ต่อไปเป็นเวลาประมาณ 20 วัน เมื่อวานนี้เป็นจุดสูงสุดของการขายในแง่ของวัน โดยจำนวนการขายในหนึ่งวันเกินจำนวนรวมของเกือบ 20 วันก่อนหน้า ทำให้แนวโน้มการฟื้นตัวของตลาดถูกขัดจังหวะอย่างรุนแรง ในฐานะหนึ่งในสองปัจจัยเชิงลบที่เห็นได้ชัดที่สุดในตลาดปัจจุบัน (อีกปัจจัยหนึ่งคือ Mt.Gox เริ่มชำระเงินคืนเป็นมาตรฐานเหรียญ) ผู้อ่านจำนวนมาก…