My XP

0

เข้าสู่ระบบ

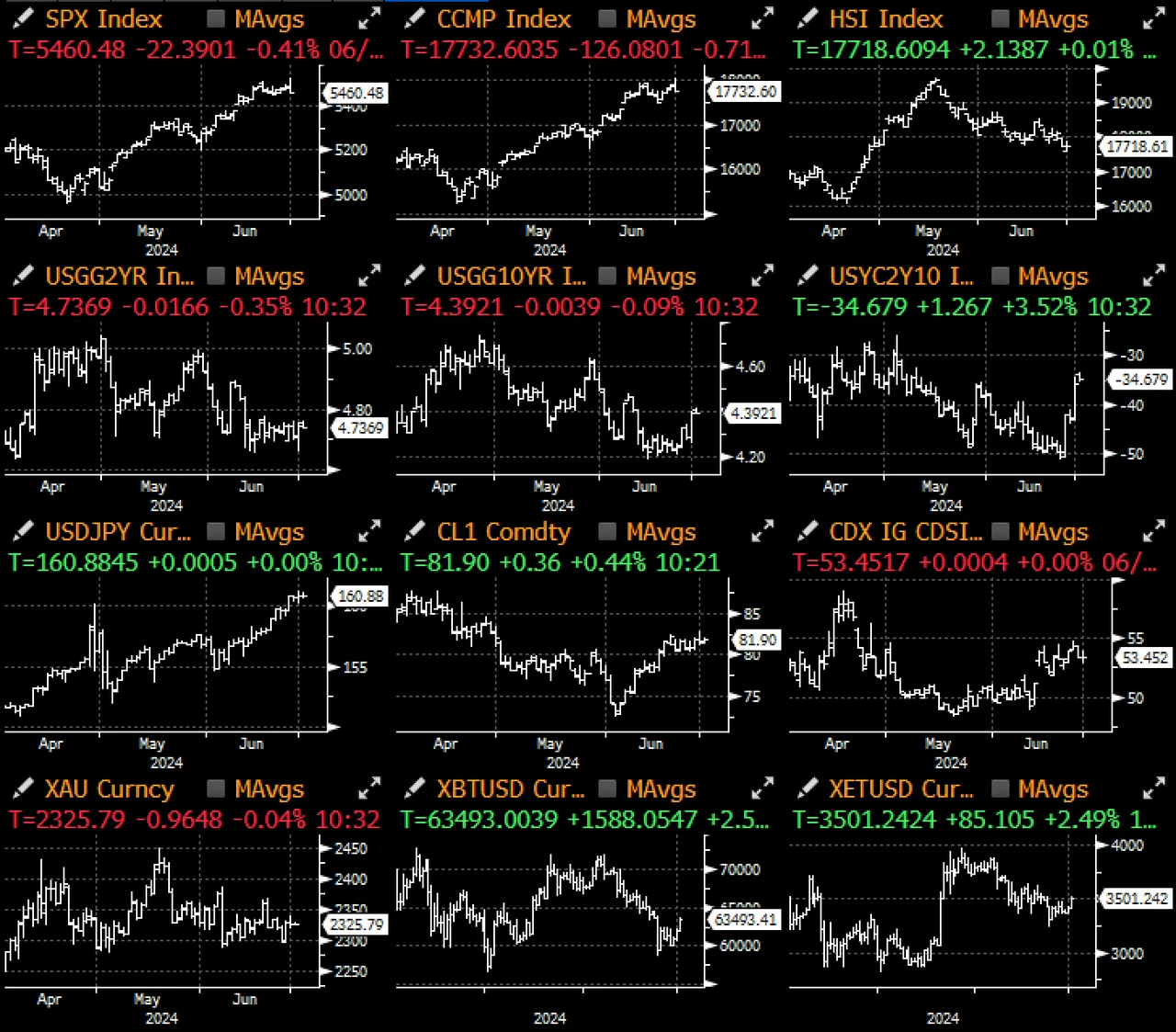

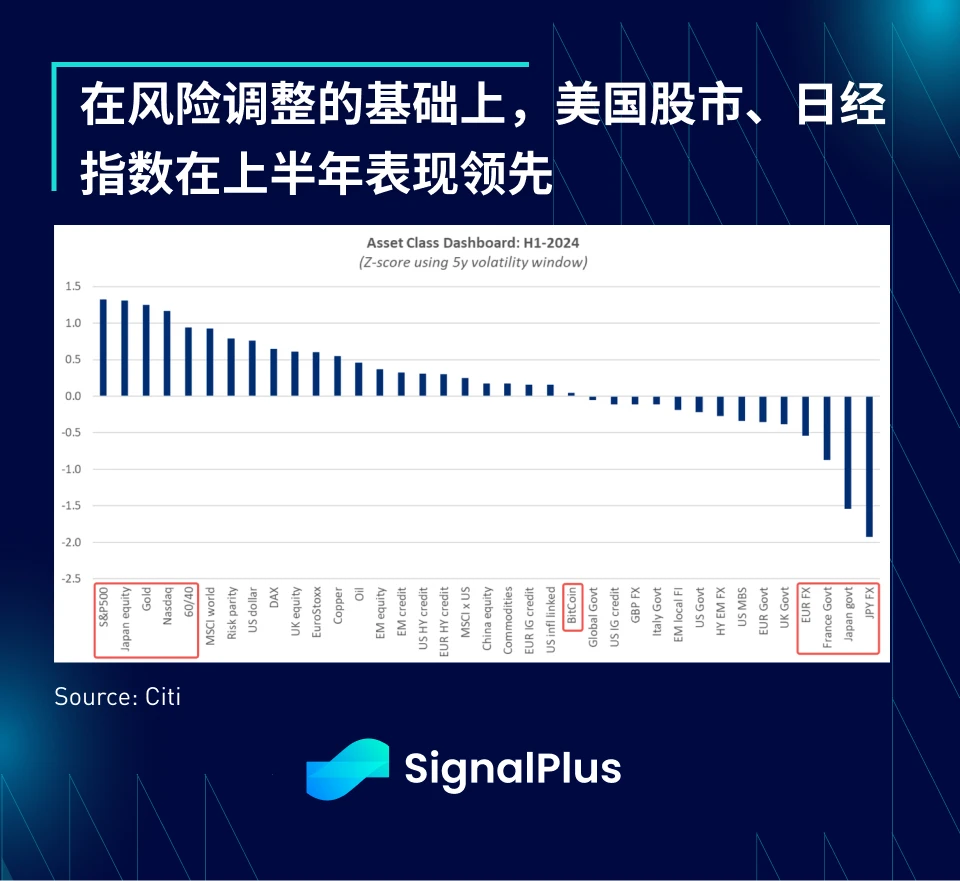

An unusually quiet first half of the year has come to an end, and a quick review of the first half of the year shows that the SPX, Nasdaq, Nikkei and gold prices have outperformed, while on the other hand, the Japanese yen, Japanese government bonds, the euro and most recently French government bonds (OATs) have lagged due to the continued zero interest rate policy of the Bank of Japan and Macrons political adventure of early elections.

Not to be outdone, the US dollar has also remained near its highest level in the past 30 years as AI continues to drive capital inflows, strong economic conditions and high benchmark interest rates. This year, the outstanding performance of the US capital market continues to exceed the expectations of most skeptics.

As capital continues to flow out of China, India has maintained its lead among emerging markets, with Indian markets up 30% (in US dollar terms) over the past 1.5 years, while Chinese stocks have fallen about 15%, a performance gap of 45%.

In the second half of the year, the US election will be the focus, and the market performance may still exceed expectations, although it may be different from the style of the first half of the year. We have long believed that the main axis of this election is about unsustainable US fiscal policy, which is reflected in the bond market, bringing higher yields and a steeper yield curve. However, in general, US customers believe that tariff policy is more important and that a stronger US dollar is a better choice. Although we basically agree with this view, we are not sure how much upside there is. After all, the US dollar index is only a few percentage points lower than its peak in the past 30 years.

Some clear themes that will emerge in the second half of the year:

U.S. economic momentum slows, although overall growth remains healthy

US recessions are rarer than unicorns

Inflation pressures are easing toward the Fed’s target, but not fast enough to justify a quick rate cut in the near term

Although there has been some rotation/correction in the US market, AI continues to drive overall sentiment

With the Fed passive and the economy on autopilot, the focus will turn to politics, with the US election, fiscal spending, new tariff policies and Treasury supply dominating the investment narrative

Judging from economic data, the US economy has slowed down from its highs in the past two years, the economic surprise index has fallen to a multi-year low, and high-frequency consumer data showed a sharp drop in savings during the epidemic and a worrying increase in consumer debt.

However, even at a lower level overall, economic activity is still relatively active compared to previous cycles, with non-farm payrolls expected to be around 190,000 this week, unemployment expected to be 4%, and average hourly earnings still having a chance to show a positive growth of 0.4%. At the current rate, the average job growth in 3 months is still 249,000, while the average before the epidemic in 2010-2019 was only 181,000.

On the inflation front, price pressures appear to be finally easing after several disappointments. PCE rose 0.08% in May, below market expectations, and “super core” PCE rose just 0.1%, helping to clarify the Fed’s plans for a possible rate cut in September.

On the political front, President Biden’s performance in the first presidential debate was below expectations, raising concerns about his age and health, while former President Trump’s performance was relatively stable (by his standards), and his post-debate reaction was swift and significant, with the difference in odds between Trump and Biden widening from +10 points before the debate to +22 points. Outside of the head-to-head matchup, Biden’s odds (35%) are now 7 points lower than the Democratic odds (42%), while Trump and the Republican odds are now well over 50%.

A landslide victory for Trump could have far-reaching implications for U.S.-China tariff policy, fiscal spending and extensions of tax breaks, monetary policy and the independence of the Federal Reserve, and potentially even the framework for cryptocurrencies.

Meanwhile, the first round of voting in the French election was won as expected by Le Pens National Rally, with the far-right party winning 34% of the vote, putting it on track for a majority.

This holiday-shortened week, with only 3.5 trading days, will see a slew of data releases on Wednesday, including ADP, jobless claims, the ISM services index and the FOMC, and Friday is expected to be very busy with the release of nonfarm payrolls immediately following Thursday’s holiday.

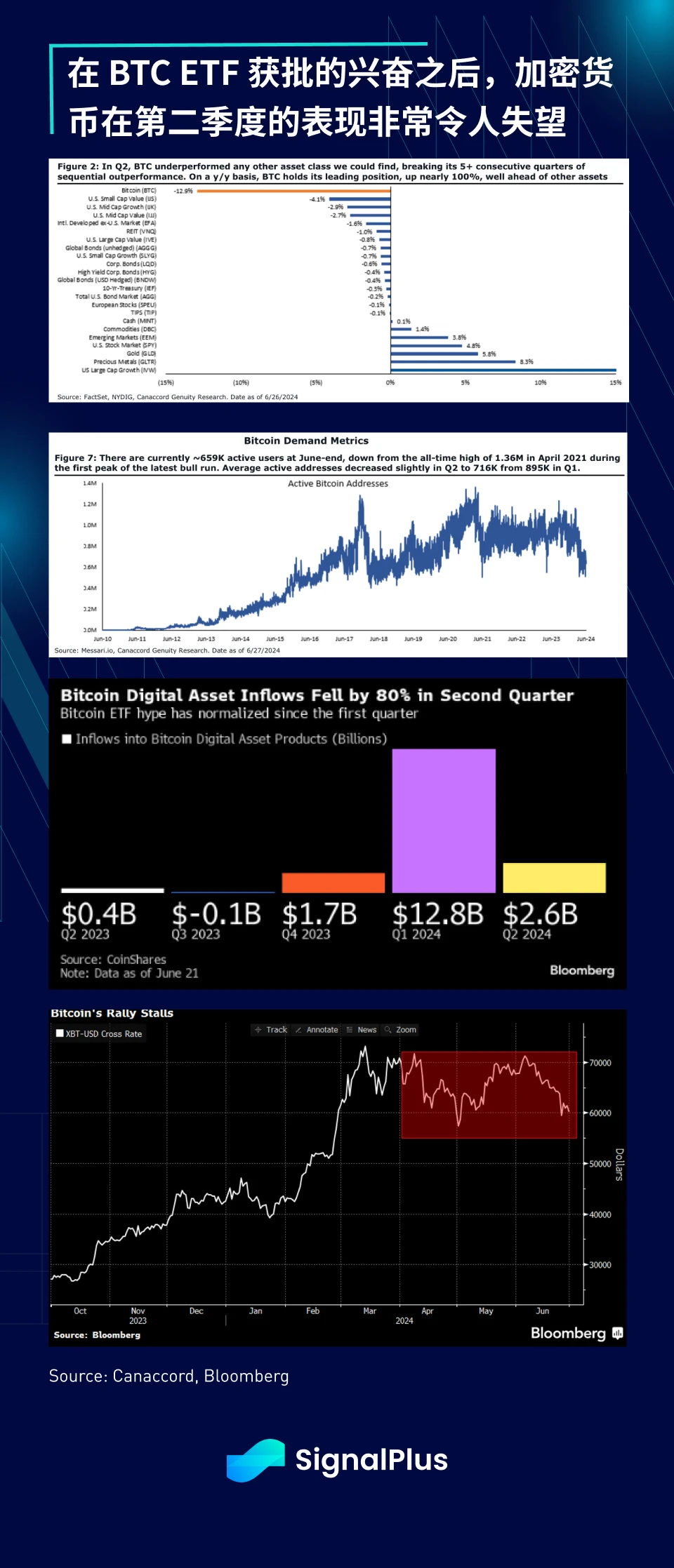

In terms of cryptocurrencies, a very disappointing quarter ended last Friday, with BTC falling 13% in the second quarter. Slowing capital inflows, a lack of substantial mainstream technological innovation, falling demand indicators, and supply-side concerns have all exacerbated the woes of cryptocurrencies, with BTC failing to break out of the 60-70k range.

Ethereum has also been disappointing, with expectations of ETF approval failing to generate excitement about the mainnet, and concerns about L2 offloads and reduced fees/increased supply (L1 fees fell to an all-time low last week), as the community continues to question the Ethereum Foundation over long-term structural issues.

Will the ETFs expected approval in the third quarter and the lawsuit victory against the SEC (regarding staking) change ETHs fortunes? Will Trumps victory solve the problem of mainstream application in the industry? Only time will tell…

คุณสามารถค้นหา SignalPlus ได้ใน Plugin Store ของ ChatGPT 4.0 เพื่อรับข้อมูลการเข้ารหัสแบบเรียลไทม์ หากคุณต้องการรับข้อมูลอัปเดตของเราทันที โปรดติดตามบัญชี Twitter ของเรา @SignalPlus_Web3 หรือเข้าร่วมกลุ่ม WeChat ของเรา (เพิ่มผู้ช่วย WeChat: SignalPlus 123) กลุ่ม Telegram และชุมชน Discord เพื่อสื่อสารและโต้ตอบกับเพื่อน ๆ มากขึ้น เว็บไซต์อย่างเป็นทางการของ SignalPlus: https://www.signalplus.com

This article is sourced from the internet: SignalPlus Macro Analysis Special Edition: Half Way Through

ที่เกี่ยวข้อง: Outlier Ventures: การเพิ่มขึ้นของเครือข่ายโซเชียลแบบกระจายอำนาจ

บทความต้นฉบับโดย: Lorenzo Sicilia หัวหน้าฝ่ายวิศวกรรมที่ Outlier Ventures แปลต้นฉบับ: xiaozou, Golden Finance Outlier Ventures สังเกตเห็นการเติบโตอย่างแข็งแรงในเครือข่ายโซเชียลแบบกระจายอำนาจบางเครือข่าย และ Farcaster และ Lens Protocol เริ่มได้รับความสนใจจากผู้ใช้จริง เมื่อพูดถึงผลิตภัณฑ์ในตลาดมวลชน สกุลเงินดิจิทัลกำลังกลายเป็นสิ่งที่ใช้งานได้จริงและมีประสิทธิภาพมากขึ้นเรื่อย ๆ จนถึงตอนนี้ การขาดการจัดการคีย์ส่วนตัวและประสบการณ์ที่เน้นอุปกรณ์พกพาเป็นอันดับแรกได้ขัดขวางการนำสกุลเงินดิจิทัลมาใช้ในผู้คน ในบทความนี้ เราจะเจาะลึกลงไปในโซเชียลมีเดียแบบกระจายอำนาจแบบเข้ารหัสหลัก ๆ หลายตัว รวมถึงคุณสมบัติ สถาปัตยกรรม และโอกาสที่ผู้ก่อตั้ง Web3 ให้ความสนใจในการสร้างโปรโตคอลกราฟโซเชียลแบบไม่ต้องขออนุญาตใหม่ 1. เครือข่ายสังคม หลังจากใช้ Instagram, Facebook, Twitter และแพลตฟอร์มอื่น ๆ มากว่าทศวรรษ ทุกคนก็รู้ว่าเครือข่ายสังคมออนไลน์ทำงานอย่างไร…