Task

Ranking

已登录

Bee登录

Twitter 授权

TG 授权

Discord 授权

去签到

下一页

关闭

获取登录状态

My XP

0

Оригинальный автор: Mason Nystrom

Оригинальный перевод: TechFlow

Update: August 19, corrected Orderflow data

Over the past 30 days, Ethereum has seen over $12 billion in order flow, with nearly half of that order flow coming from private or proprietary applications. Click here to read the full article .

Источник: Orderflow.art

But how did we get here, and where are we going?

In short, the reason we are here is foodcoins. A slightly more detailed explanation is that the DeFi summer gave rise to a large number of professional users and retail trading, which subsequently led to the birth of trading aggregators (such as 1inch) that provided users with better price execution through private order routing. Wallets (such as MetaMask) quickly followed suit, realizing that user convenience could be monetized by adding in-app exchange functions, proving that any application that controls the attention (and orders) of end users has a very valuable business model.

Источник: Дюна

Over the past two years, we’ve seen two additional categories of players enter the private order flow space – Telegram bots and solver networks. Telegram bots align with MetaMask’s “convenience fee” and provide users with an easy way to trade a long tail of crypto assets in group chats. As of July, Telegram bots account for ~17% of trades and 6% of volume , most of which are conducted through private mempools.

On the other hand, in the main part of the market, solver networks (such as Cowswap and UniswapX) have also emerged as core venues for trading highly liquid pairs (such as stablecoins and ETH/BTC). Solver networks change the order flow market structure by outsourcing the task of finding the best route for a given trade to solvers (market makers) competing in the market.

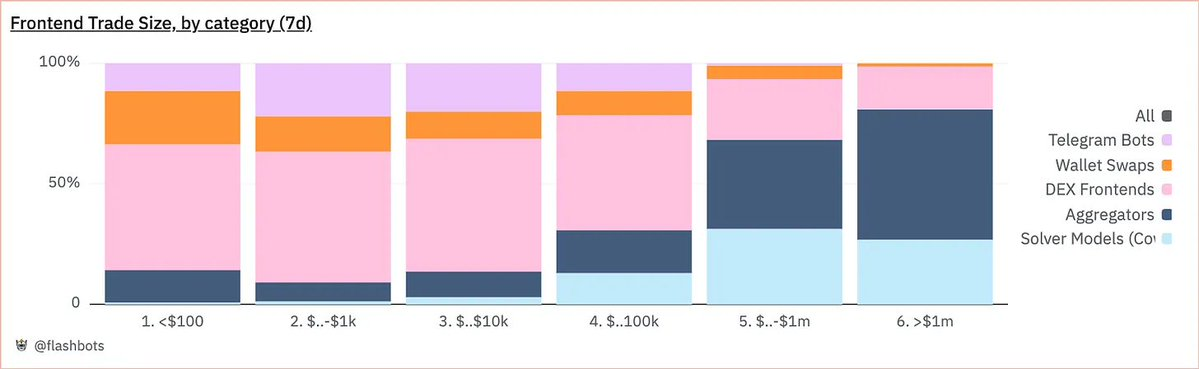

As a result, an initial bifurcation of trading venues has occurred, with convenient front-end tools (including TG bots, wallet exchanges, and Uniswap’s front end) primarily used for longer-tail, lower-value (less than $100k) trades, while aggregators and solver networks are the preferred venues for larger trades, which often involve stablecoins and major currencies (ETH/BTC).

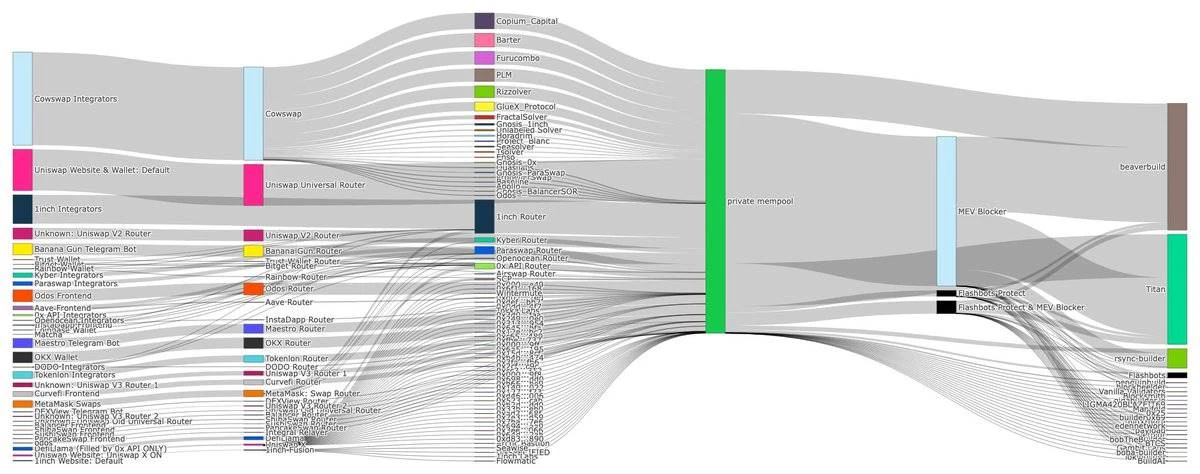

On a more detailed analysis, you’ll find that the majority of private order flow comes from aggregators (like 1inch) and front-end tools (TG bots, wallets, and front-ends).

The privatization of order flow becomes even more pronounced when we consider that only 30% of Ethereum transactions, by trade, go through private mempools, meaning that a small number of exchanges contribute a significant portion of private order flow.

Источник: Дюна

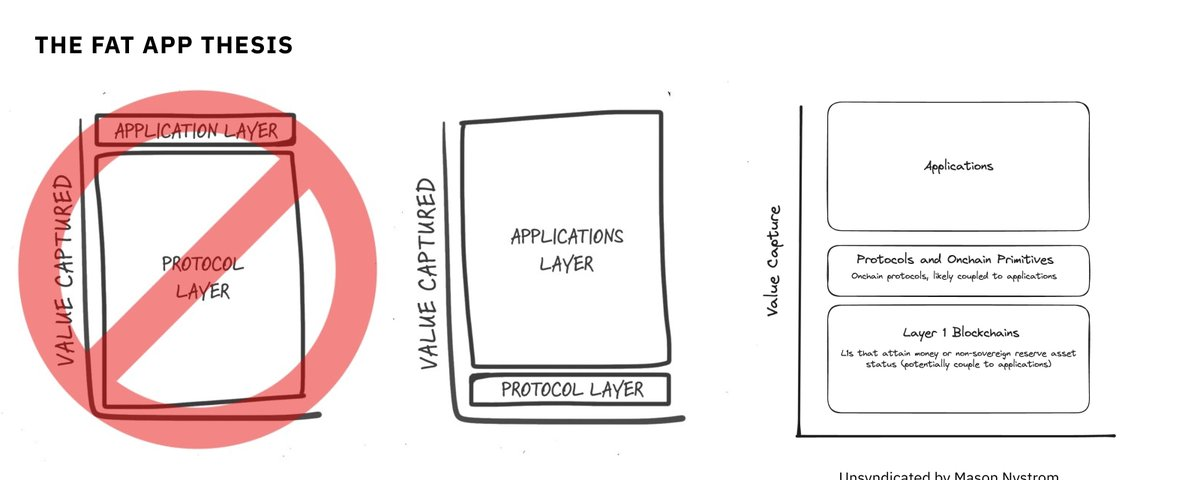

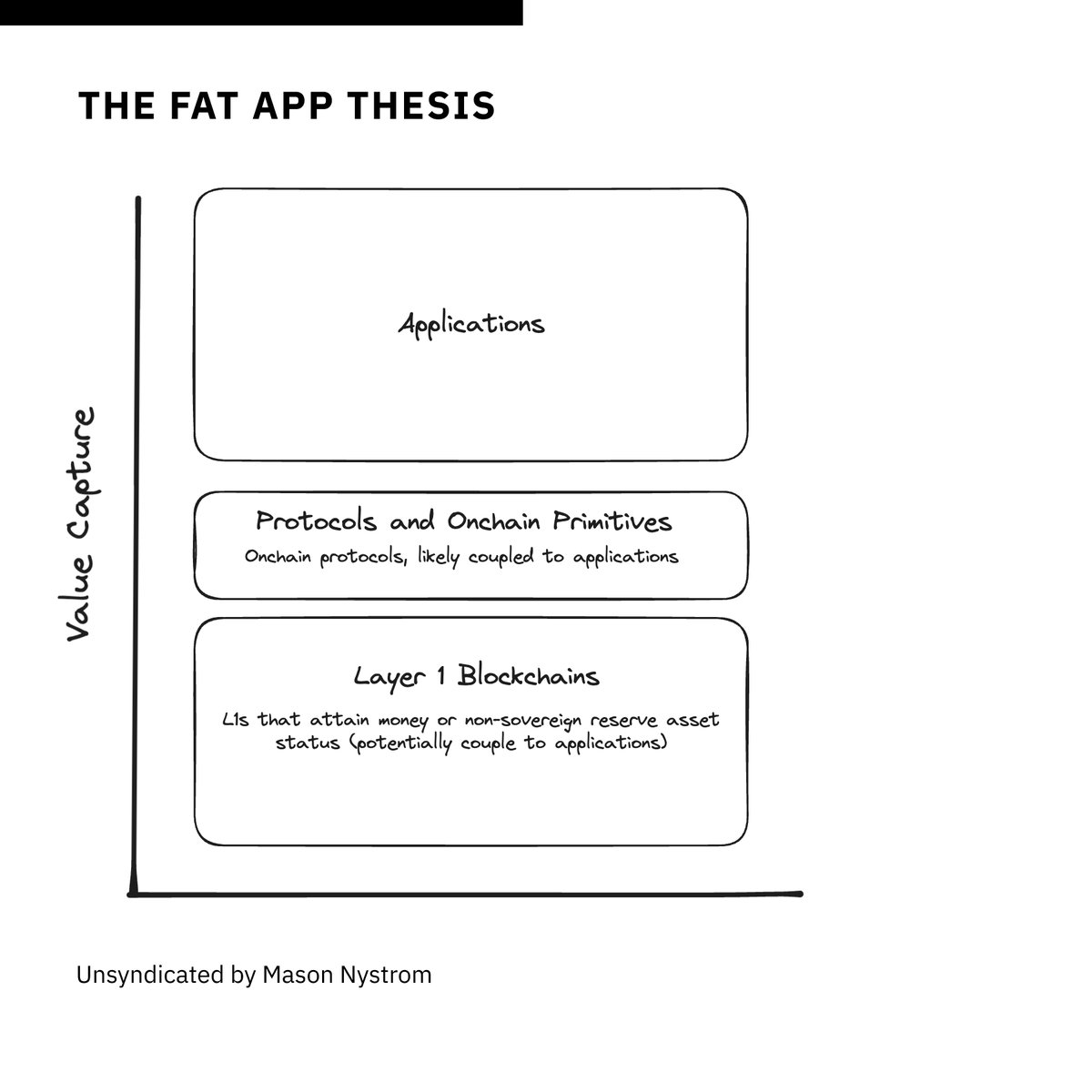

In other words, valuable order flow is more important than the quantity of order flow. The power law relationship between users and order flow leads to an inevitable conclusion – applications will accumulate the largest proportion of overall value. In other words, the theory of fat applications still exists.

Uniswap’s protocol clearly has value, but the more interesting story is happening at the application layer, as Uniswap works to become a consumer application — by vertically integrating key components of its technology stack, expanding the capabilities of its interface, mobile wallet, and aggregation layer. For example, Uniswap Labs’ application — Uniswap’s frontend, wallet, and aggregator, UniswapX — has generated about 16% of the $8 billion in private order flow in the past 30 days, and almost 18% of total order flow (private and public).

In the cryptocurrency space, applications like Worldcoin account for nearly 50% of Optimism mainnet activity, which has prompted them to launch their own application chain, further highlighting the power of fat application theory and control requirements (such as users and transactions).

Even top NFT projects with strong brands like Pudgy Penguins are building their own chains, with CEO Luca explaining that controlling the block space on which distribution depends is beneficial to the value accumulation of Pudgys brand and intellectual property.

Going forward, applications should look to create new types of order flow, whether by creating new assets (like Pump and memecoins), by building applications that provide new user utility like identity (e.g. Worldcoin, ENS), or by building better consumer experiences that are vertically integrated and support valuable transactions, like Farcaster and frames, Solana Blinks, Telegram and TG applications, or on-chain games.

It is worth noting that the fat app theory has been the focus of many crypto people since the end of the last cycle, as the application chain theory has developed as part of the consensus view.

My current take on the fat app theory is that we will see most value accrue to the application layer of the tech stack, where control of users and order flow puts applications in a privileged position. These applications will likely be coupled with on-chain protocols and primitives, similar to today’s UniswapX and Uniswap Protocol, Warpcast and Farcaster, Worldcoin and Worldchain. Ultimately, these protocols, especially those that are most on-chain (like MakerDAO), can still accrue significant value, but applications may capture more value due to their proximity to users and off-chain components, thus forming a more defensible moat.

Fat App Theory and Value Accumulation in Crypto Investment

In the end, I still believe that Layer 1 blockchains (like Bitcoin, Ethereum, Solana) can capture significant value as non-sovereign reserve assets where the underlying asset (like ETH) accrues tremendous value. Given enough time, applications may try to build their own L1s just as they build their own L2s, but launching a commodity L2 blockspace is very different than launching an L1 and turning the token into a commodity and collateral asset, so this may be a distant future.

The core takeaway is that as more and more consumer applications create and own valuable order flow, the crypto world will re-evaluate applications as people will come to the inevitable conclusion – fat applications are inevitable.

This article is sourced from the internet: Ethereum private order flow accounts for half of the total, and the fat application theory is gradually taking effect

Related: Banana Game: Rare banana worth $500, the next upstart in TG clicker games?

Original | Odaily Planet Daily ( @OdailyChina ) Author: Golem ( @веб3_golem ) After Notcoin broke the circle, similar click games on Telegram quickly gained attention. Later, Hamster Kombat became the leader in this field. However, due to the highly homogeneous gameplay and invitation incentive mechanism, as well as the undetermined airdrop time, click games on Telegram are no longer easy to gain the favor of players (PUA is no longer active). Even so, on July 26, Banana, an idle game that was once popular on the traditional game platform Steam, was moved to TON. Just three days after its launch, the number of registered users exceeded 1 million , the game connected to more than 580,000 social accounts, and the number of TG channel subscribers currently exceeded 560,000. So,…