Look whos back?

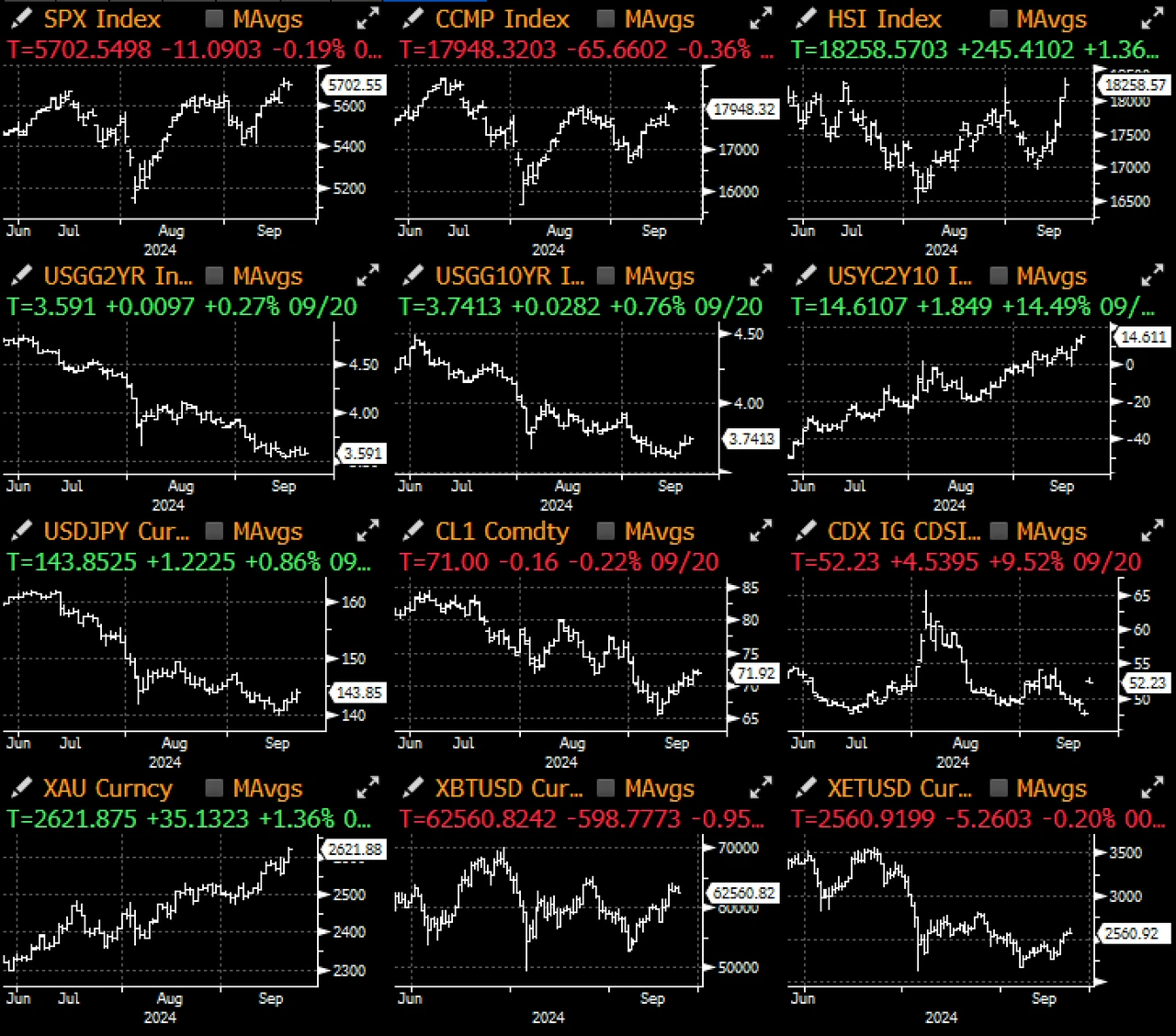

As we mentioned in the summary of last Thursdays FOMC meeting, Chairman Powell showed a confident dovish stance at last weeks FOMC meeting and took active actions, cutting interest rates by 50 basis points ahead of schedule while still advocating the view of a soft landing. The result is obvious. This is a significant dovish stimulus, marking the official start of a new round of easing cycle by the Federal Reserve. It took about 12 hours for the risk market to digest this information and then pushed the stock market to a new historical high. What about the recession?

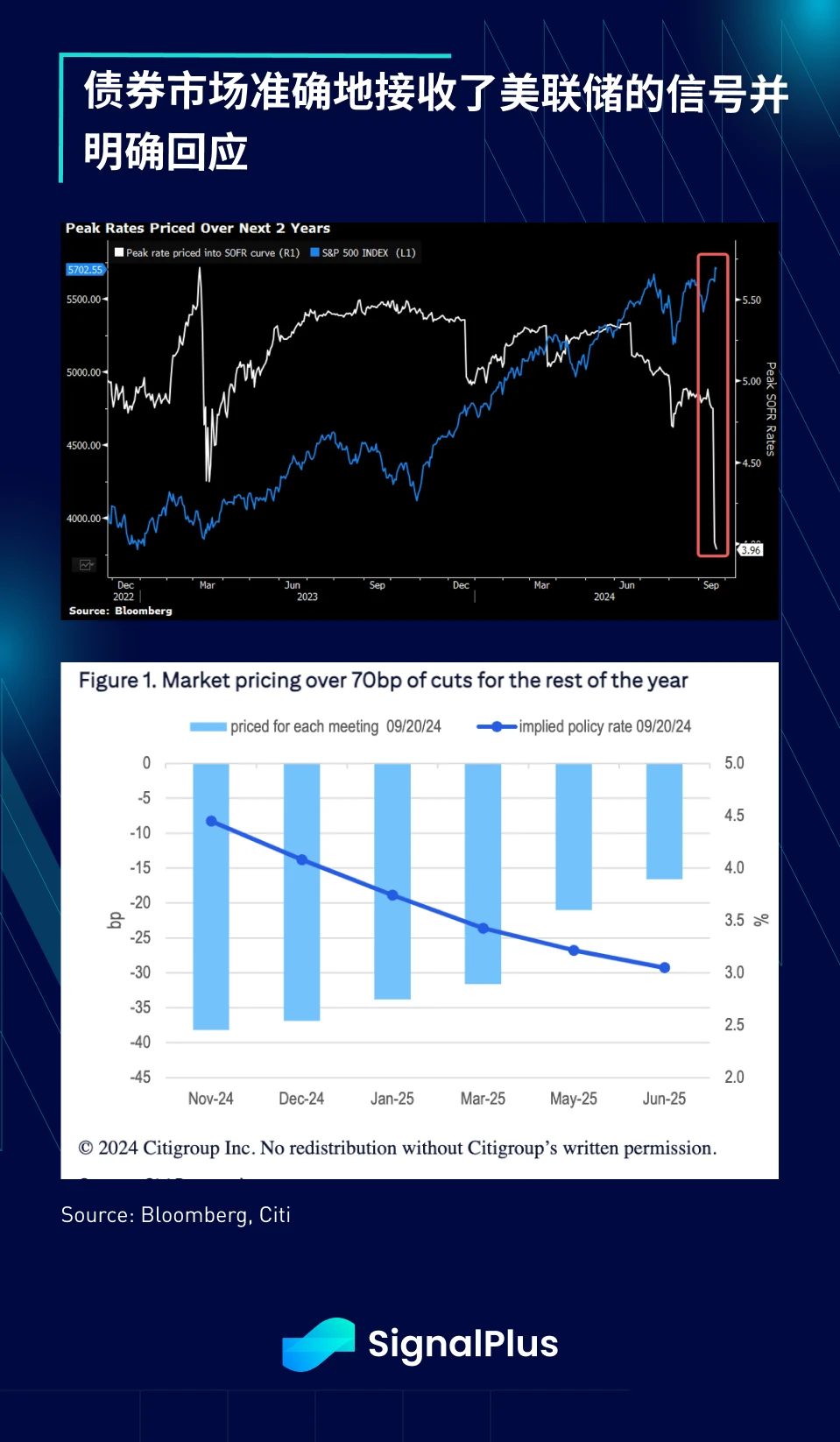

The performance of the fixed income market remains relatively calm, with relatively stable yields, but the trend of structural curve steepening has begun to emerge. The 2-5 year yields remained at the low point of the year after the rate cut, while the 10-30 year yields rose against the backdrop of improved risk sentiment and prevention of rising inflation. The important core PCE data will be released this Friday. Although others may have different views, we believe that based on economic fundamentals alone (the Atlanta Feds GDP growth forecast is still around 3%, the job market is still solid, and inflation is still above 2%), a 50 basis point rate cut at this time is unconventional operation, so the Feds actions should be regarded as a clear dovish signal, and the market has good reasons to respond to it in the short term.

So what could derail the rally? Ultimately it comes back to the hard data that the Fed has been hinting at. The key is still 1) the extent of the slowdown in the US job market and 2) the speed of the slowdown in CPI, both of which are still in the Feds favor for now, unless the economic situation can prove the market wrong, in other words, this rally will be presumed innocent until the economy slows significantly, which cannot be saved by the Feds loose policies.

For the US stock market, aggressive rate cuts in the context of a soft landing with no clear downside risk can only mean that the stock market will hit new all-time highs again, which is exactly what happened last week. The stock market has successfully coped with the negative seasonality in September, and even Trumps decline in the polls has not stopped the rebound in risk assets, and high-beta sectors (such as AI stocks) are expected to accelerate again. Similar to the situation in the bond market, economic data remains crucial and investors may maintain a buy-on-dip strategy in the last month before the election. Finally, technical indicators show that the SPX index has momentum for an upward breakout, which is worth watching in the short term.

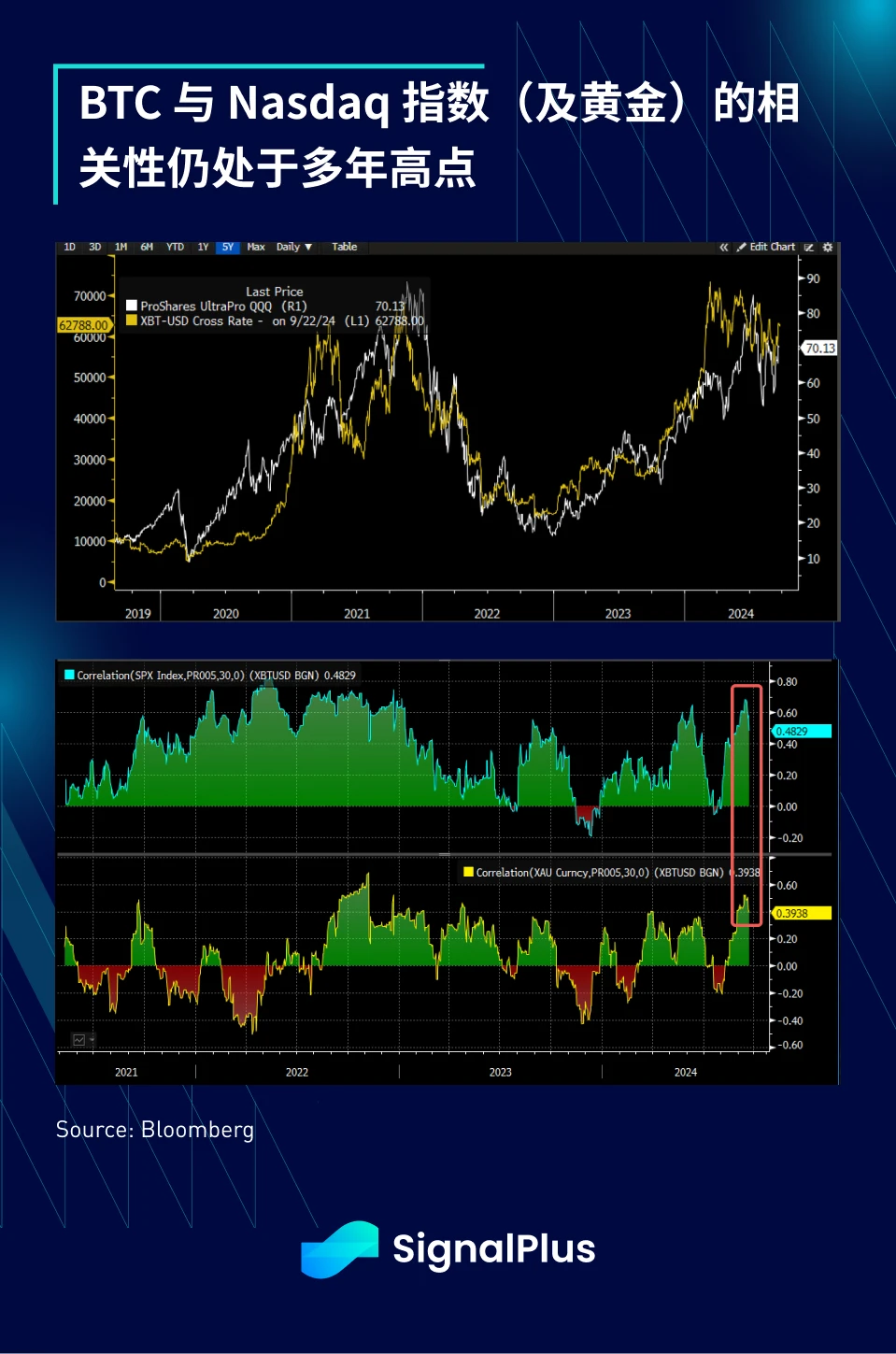

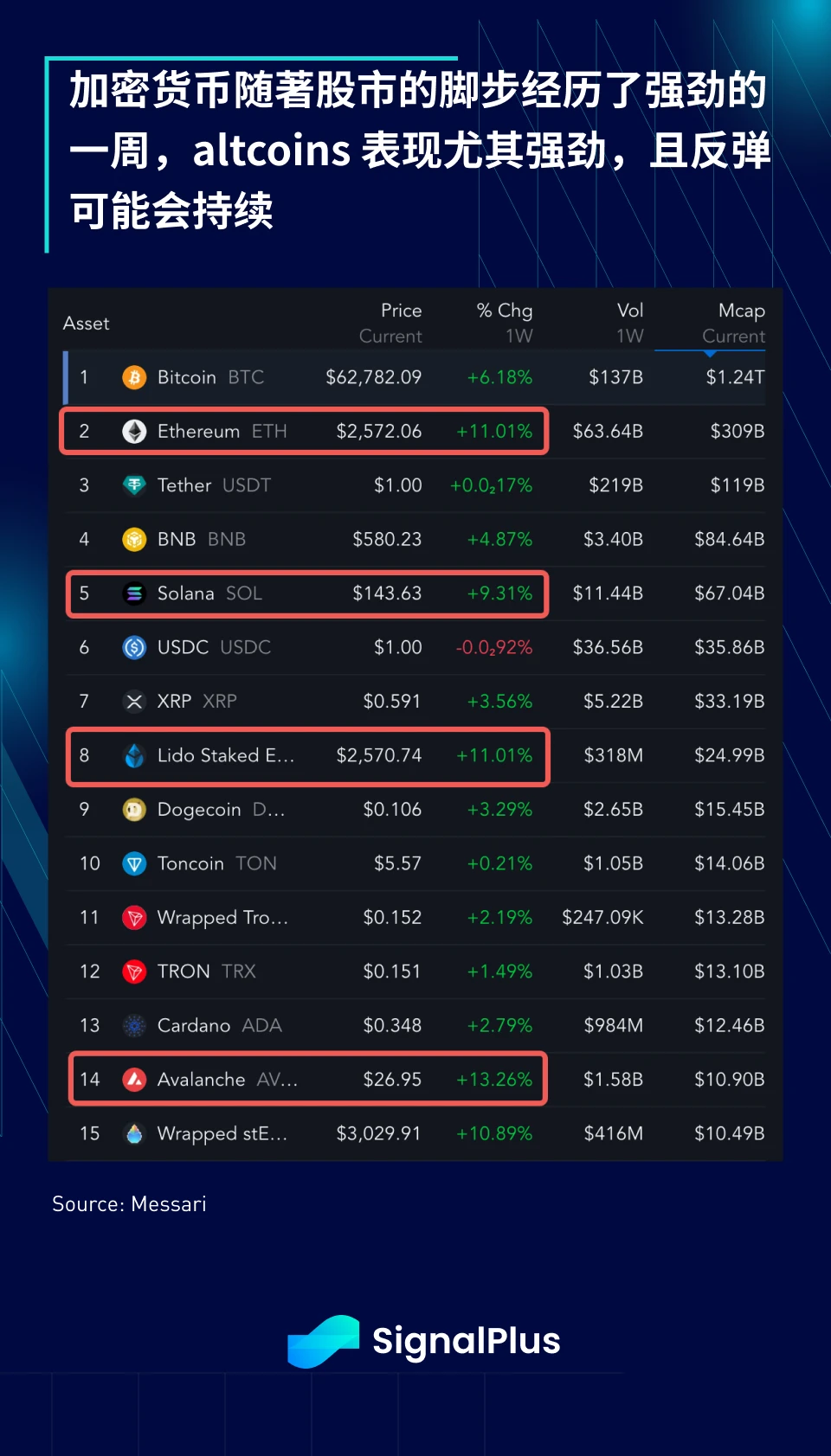

In terms of cryptocurrencies, BTC prices rebounded significantly last week, up 6%, as the correlation with stocks (and gold) returned to a two-year high. BTC and the 3x leveraged Nasdaq index have re-aligned, but cryptocurrencies have the opportunity to see more dramatic movements in the short term, especially altcoins, which performed very strongly last week. Even the much-criticized ETH managed to rise 11% in the past week without any new developments. We believe that this rebound may continue as the Feds dovish turn finally becomes the market consensus.

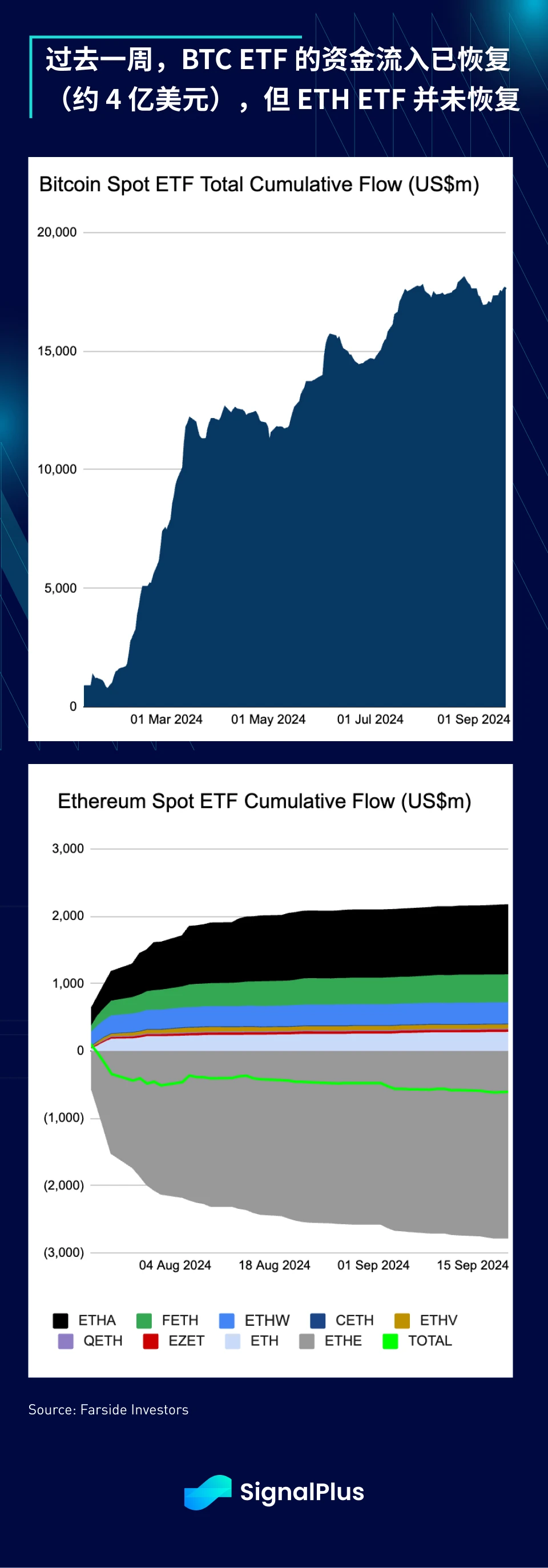

The strong rebound in Altcoins is an encouraging sign, and as long as stock market sentiment holds, there is a chance for more rebound momentum in the short term. Inflows to BTC spot ETFs have recovered over the past week and are expected to hit a cumulative high by the end of the month. Will this price rebound be able to save ETH ETF inflows? We think the answer will depend on whether the stock market can top out again before November, and the market has begun to benefit from the Feds dovish turn.

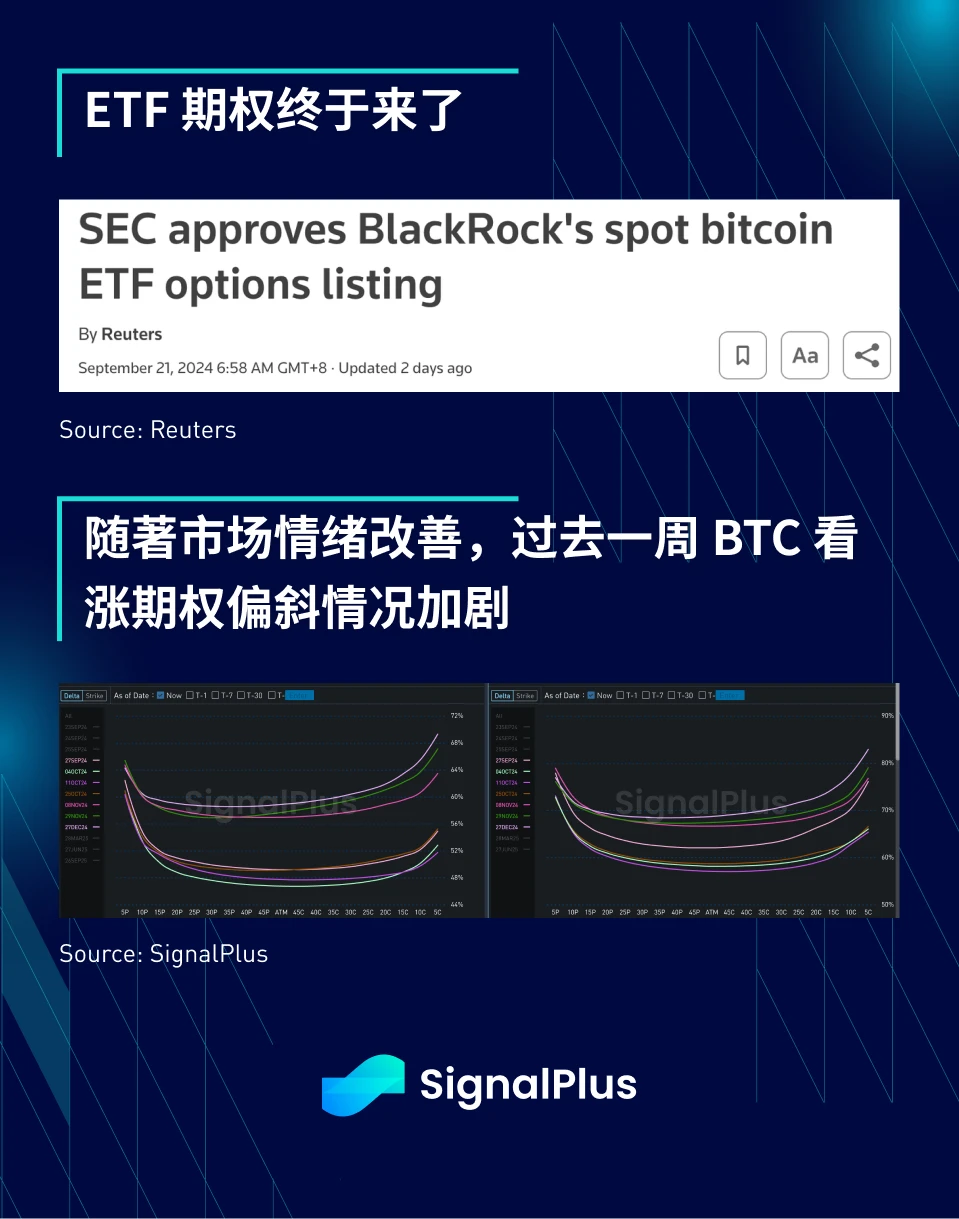

Another positive factor for ETF inflows may come from the US SEC鈥檚 approval of ETF options listing. As we have long emphasized, options are one of the mainstream asset classes in TradFi and are favored by many institutional investors. Therefore, it is only a matter of time before options enter the cryptocurrency market and are widely used in the future.

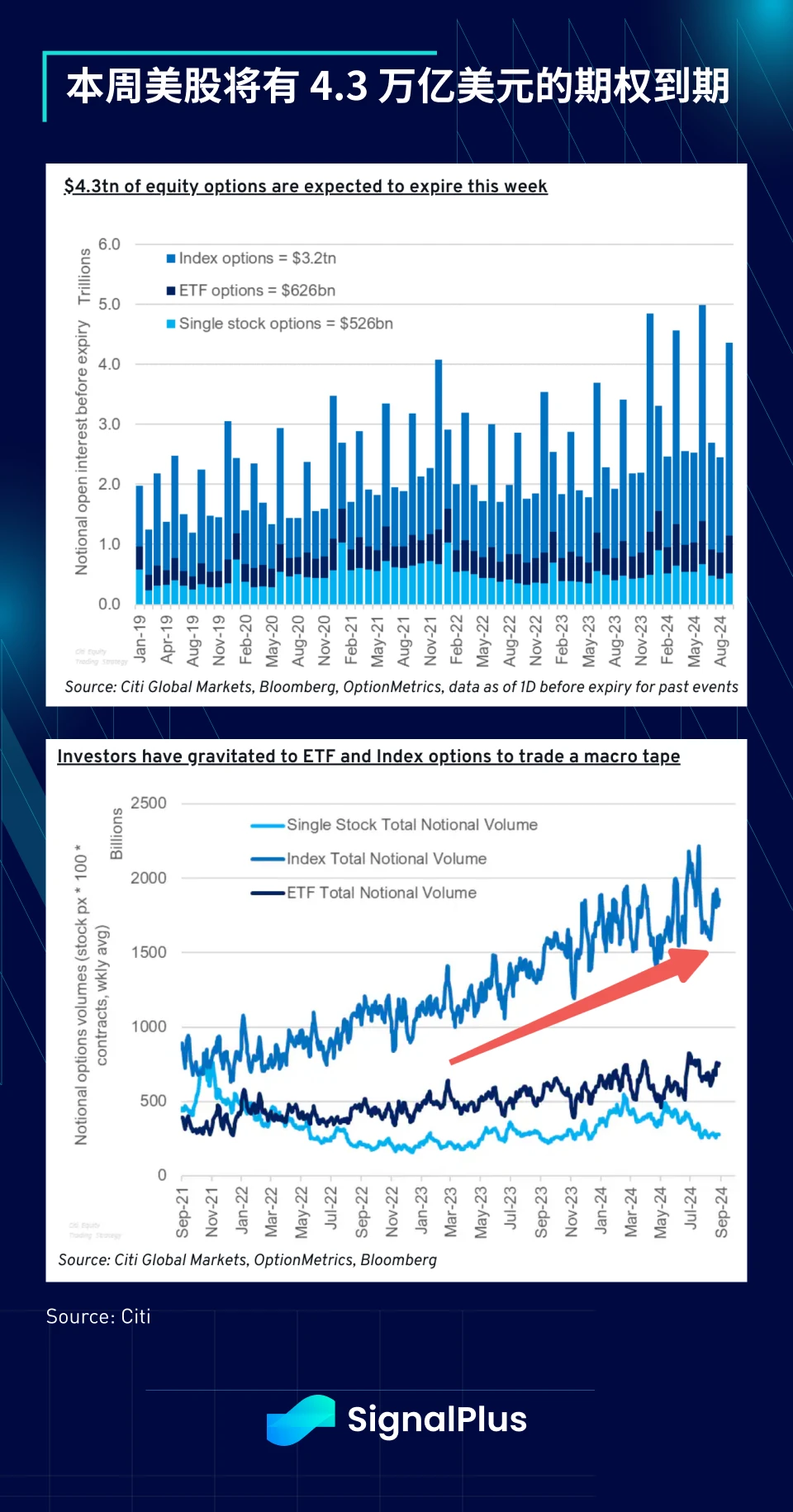

Speaking of the importance of options, the TradFi market will see over $4.3 trillion in US stock options expire this week, and index options activity is particularly active now that almost everyone is an index volatility trader. Will investors take more call options after the end of the month expiration? Is it time to buy some BTC out-of-the-money calls? Be sure to keep a close eye on this space.

Next, the market will focus on a series of Fed officials speaking, with 3 officials speaking on Monday, 6 (including Powell) on Thursday, and another 2 on Friday. The market will focus particularly on Powells speech on Thursday to assess his reaction to the significant easing of financial conditions, while the only noteworthy US economic data will be the PCE data on Friday.

Overall, the base case for the macro market is to continue to rise slowly, with risk premiums in the options market pricing low ahead of the release of the non-farm payrolls data on October 4. We do not expect Fed officials to rock the boat in their upcoming talks, and the most likely market move will still be to the upside.

I wish all readers smooth trading, but please be careful when going against the Federal Reserve!

t.signalplus.com에서 SignalPlus 트레이딩 베인 기능을 사용하면 더 많은 실시간 암호화폐 정보를 얻을 수 있습니다. 업데이트를 즉시 받으려면 Twitter 계정 @SignalPlusCN을 팔로우하거나 WeChat 그룹(WeChat 보조자 추가: SignalPlus 123), Telegram 그룹 및 Discord 커뮤니티에 가입하여 더 많은 친구들과 소통하고 상호 작용하세요.

시그널플러스 공식 홈페이지: https://www.signalplus.com

This article is sourced from the internet: SignalPlus Macro Analysis Special Edition: Dont Fight the Fed

Original author: Tang Han, founder of SeeDAO Crypto nihilism has been prevalent in the industry recently. But this is not surprising at all. For some experienced practitioners, as early as last year or even the year before, they had doubts about the current industry path. In my opinion, the biggest reason for the current crypto nihilism is that a large number of funds and builders have poured into a bunch of artificially conceived pseudo-demands. This pseudo-demand cannot bring real users, nor can it solve real problems. Instead, it has caused more and more smaller pseudo-problems, and has caused funds and people to run around in the split pseudo-problems. Because the problem is artificially constructed, the result is naturally nihilistic. Its like a person has created an enemy, and after a…