My XP

0

Login

原作者: Matthew Sigel Patrick Bush

原文翻訳: TechFlow

Please note that VanEck may hold the digital assets described below.

Before we get into our outlook for 2025, let’s take a look at how our predictions for 2024 performed. Out of the 15 predictions made at the end of 2023, our self-rated score was 8.5/15. While 56.6% accuracy isn’t perfect, it’s good enough to keep us “in the game.” With Bitcoin (BTC) breaking $100,000 and Ethereum (ETH) breaking $4,000, 2024 will be a memorable year in 暗号currency history, even if some predictions didn’t quite pan out.

In our 2024 forecast, we successfully bet on several key trends, including:

First launch of Bitcoin spot ETP

Bitcoin halving completed successfully

Ethereum still ranks second, behind Bitcoin

Bitcoin hits all-time high in Q4 2024

L2 dominates Ethereum activity (but L2 TVL is still lower than Ethereum)

Stablecoin market capitalization hits all-time high

Decentralized exchange trading volume reaches new record

Solana (SOL) Outperforms Ethereum (ETH)

DePIN Network Adoption Growth

Although some of the predictions were not fully realized, the overall trend still verifies our analysis direction.

Crypto bull market to reach interim highs in Q1 and new highs by year end

The United States further embraces Bitcoin through strategic reserves and policy support

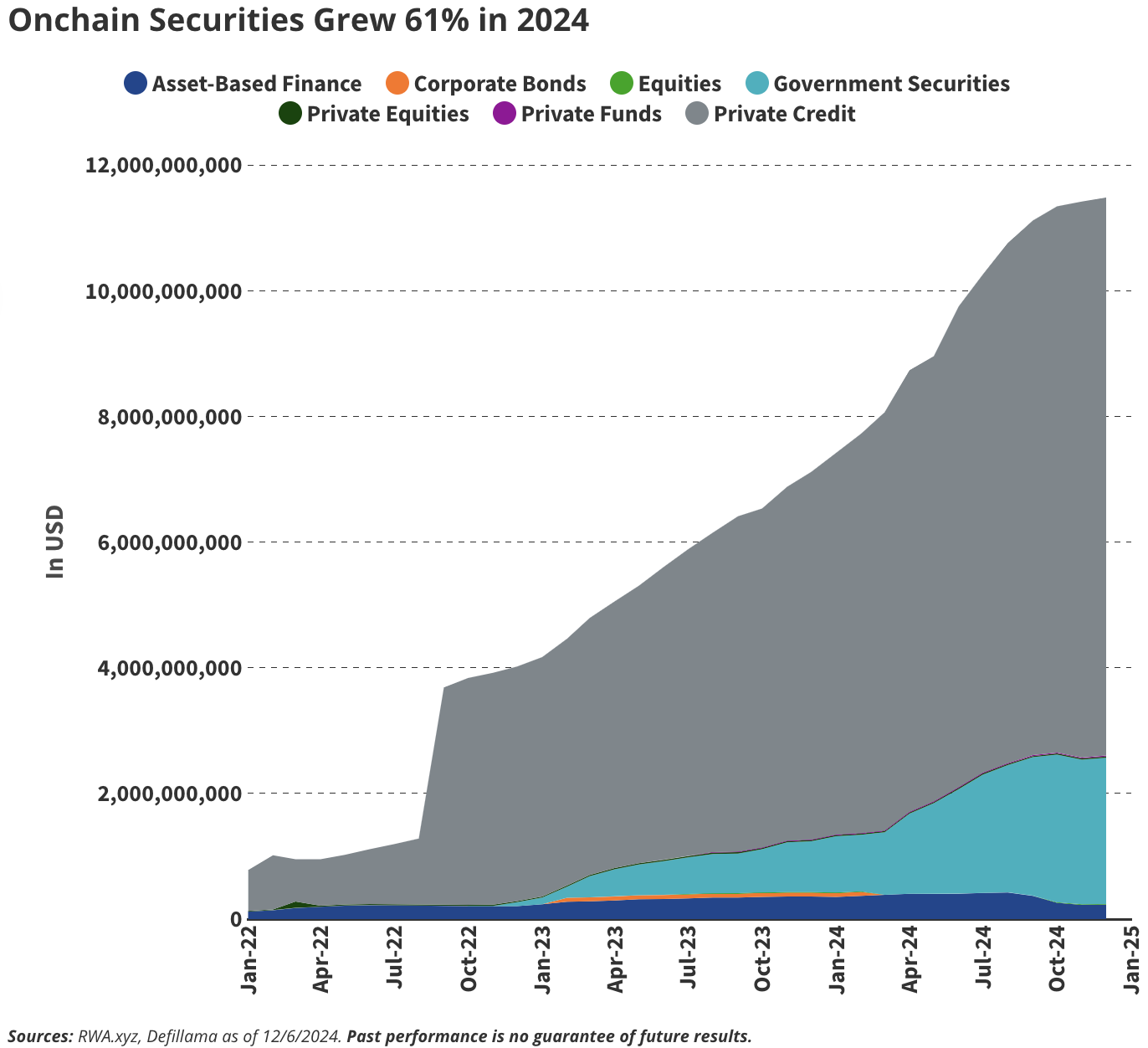

Total value of tokenized securities exceeds $50 billion

Stablecoin daily transaction settlement volume reaches $300 billion

AI agent on-chain activity exceeds 1 million

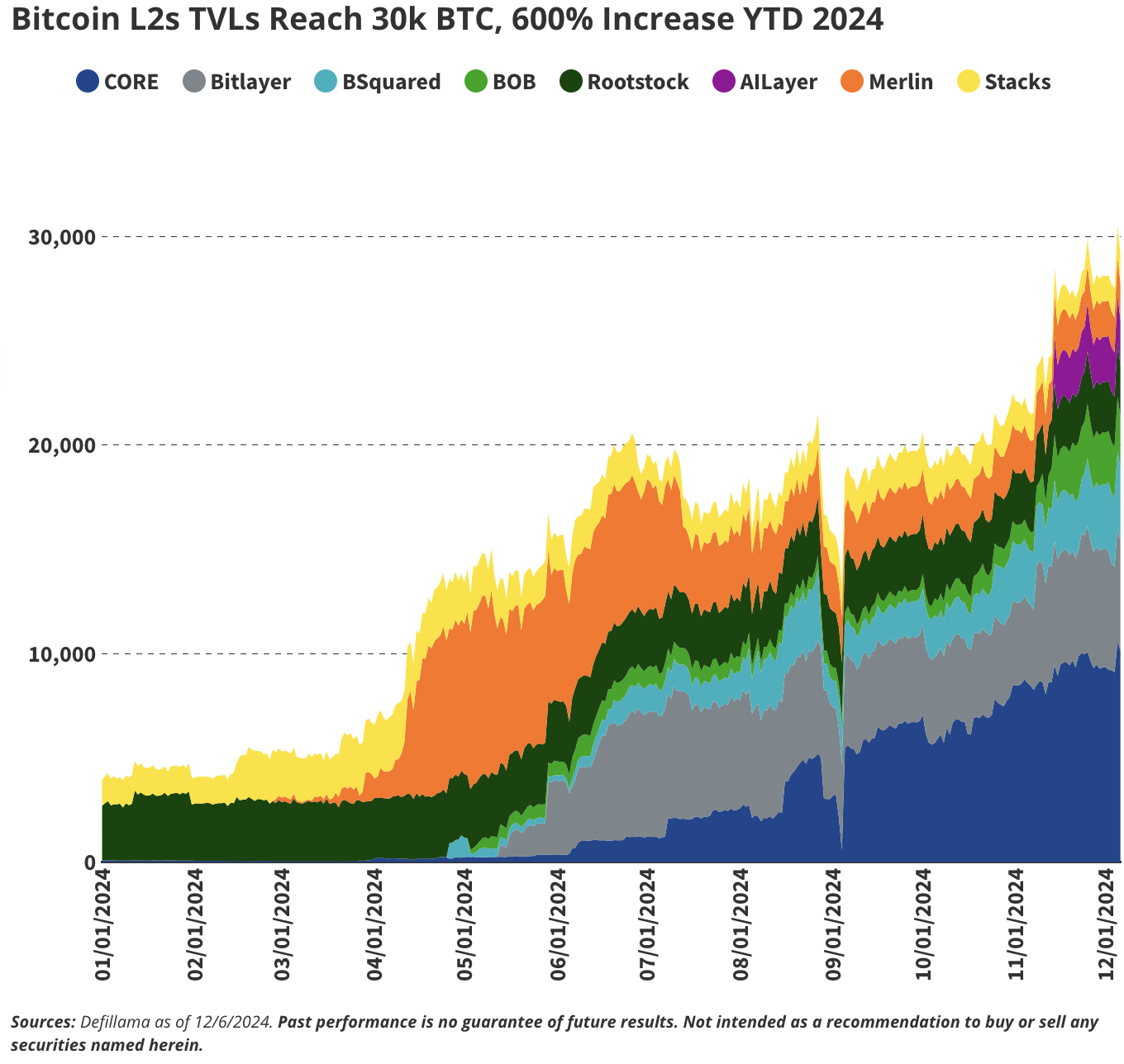

The total locked value (TVL) of the second layer of Bitcoin network has reached 100,000 BTC

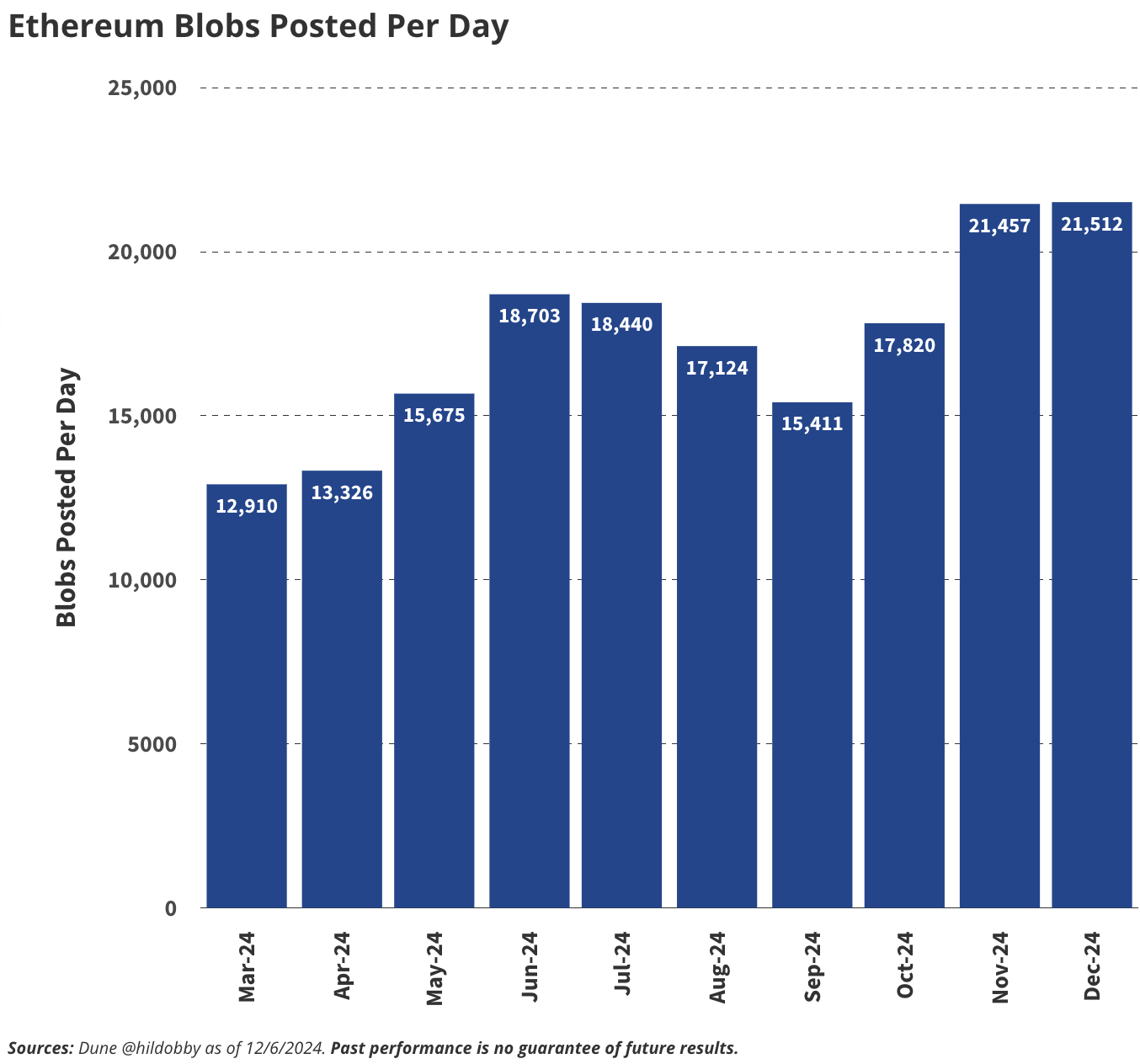

Ethereums Blob Space Fee Revenue Reaches $1 Billion

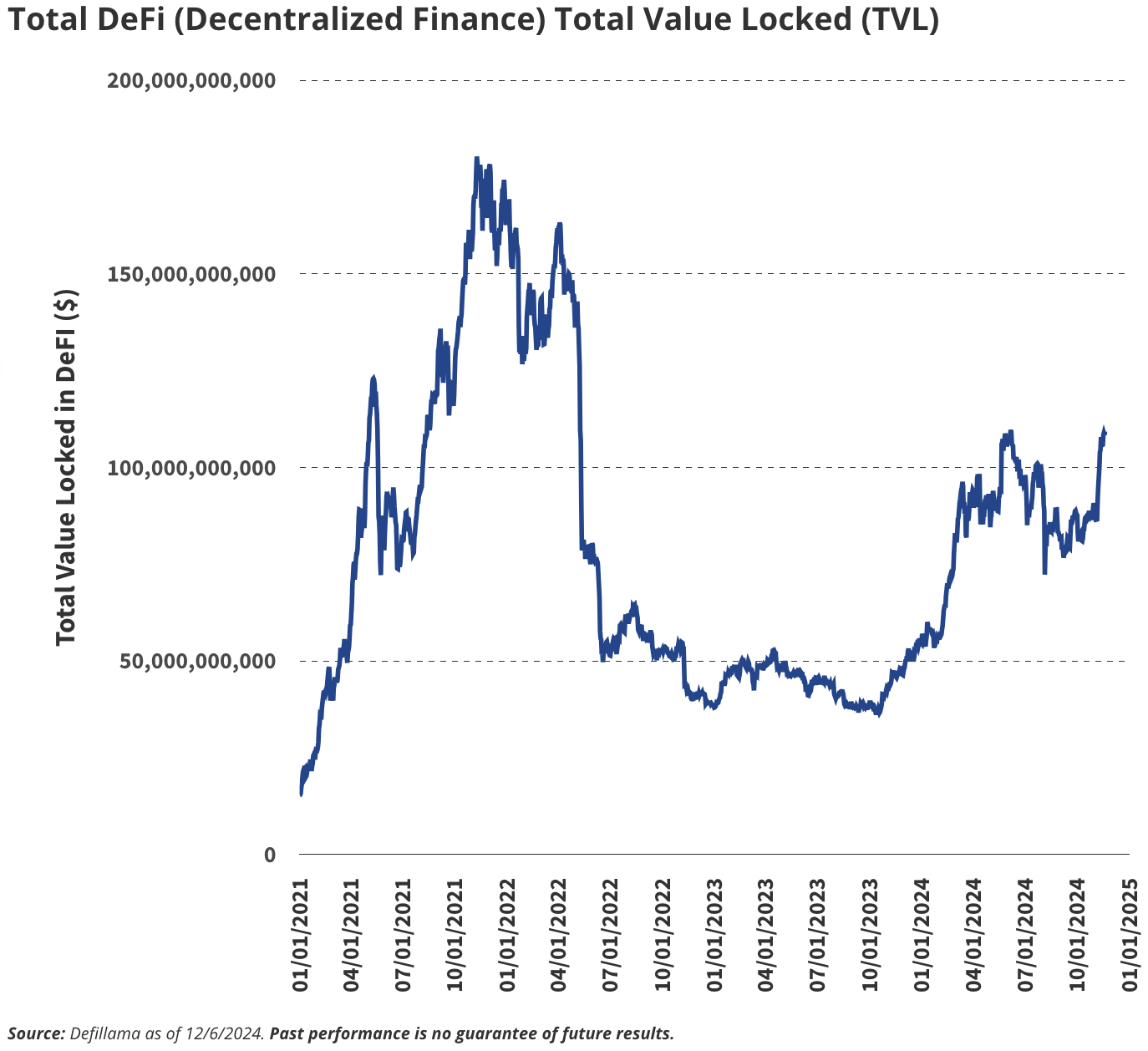

DeFi transaction volume hits a new high of $4 trillion, and the total locked value reaches $200 billion

NFT market recovers, with annual transaction volume reaching $30 billion

The performance of decentralized application (DApp) tokens is gradually catching up with mainstream public chain tokens

Next, we will delve into the background and logic of some of these key predictions.

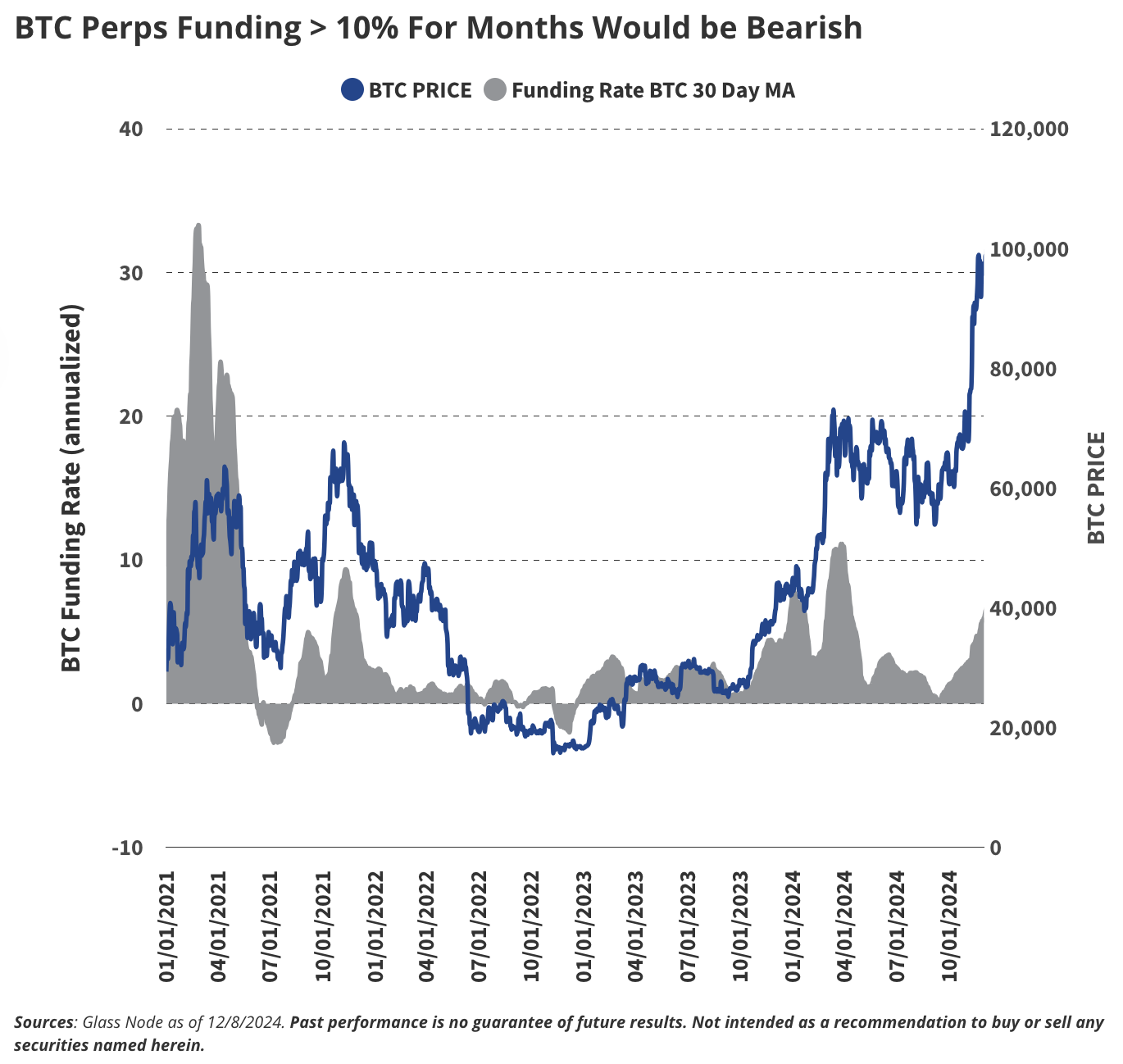

We believe that the 2025 cryptocurrency bull run will continue to develop and reach its first peak in the first quarter. At the apex of this cycle, we expect the price of Bitcoin (BTC) to reach about $180,000, while the price of Ethereum (ETH) will exceed $6,000. Other well-known projects such as Solana (SOL) and Sui (SUI) may exceed $500 and $10, respectively.

After the first high, we expect BTC to pull back 30%, while altcoins could see a bigger drop of 60%, reflecting the markets consolidation during the summer. However, a recovery could occur in the fall, with major coins regaining momentum and breaking out of all-time highs again before the end of the year. To determine when the market is nearing a top, we will be watching for the following key signals:

Sustained high funding rates: When traders borrow money to bet on rising BTC prices, they are willing to pay funding rates of more than 10% for three months or more, indicating speculative overheating.

Excessive unrealized profits: If a large percentage of investors holding BTC are in a state of significant paper gains (profit-to-cost ratio of 70% or more), this indicates that the market is in a frenzy.

Overvaluation of market capitalization relative to realized value: When the MVRV (market capitalization to realized value ratio) score exceeds 5, it means that the BTC price is far higher than the average purchase price, which usually indicates an overheated market.

Declining Bitcoin dominance: If Bitcoin’s share of the total crypto market falls below 40%, it means speculative funds are turning to higher-risk altcoins, which is typical late-cycle behavior.

Mainstream speculation: When a large number of non-crypto friends begin to inquire about suspicious projects, it is usually a reliable signal that the market is close to a top.

These indicators have historically been reliable signals of market manias and will ガイド us in developing our outlook for the market cycle through 2025.

The election of Donald Trump has injected significant momentum into the crypto market, with his administration appointing several pro-cryptocurrency leaders to key positions, including Vice President JD Vance, National Security Advisor Michael Waltz, Commerce Secretary Howard Lutnick, Treasury Secretary Mary Bessent, Securities and 交換 Commission (SEC) Chairman Paul Atkins, Federal Deposit Insurance Corporation (FDIC) Chairman Jelena McWilliams, and Health and Human Services Secretary RFK Jr. These appointments not only mark the end of anti-crypto policies (such as the systematic debanking of crypto companies), but also herald the beginning of a policy framework that positions Bitcoin as a strategic asset.

New SEC leadership (or potentially the Commodity Futures Trading Commission) will approve multiple new spot crypto exchange-traded products (ETPs) in the U.S., including VanEck’s Solana product. Ethereum ETP functionality will expand to include staking, further enhancing its utility to holders, while both Ethereum and Bitcoin ETPs will support physical creation/redemption. The repeal of SEC Rule SAB 121 (either by the SEC or Congress) will pave the way for banks and brokers to custody spot crypto, further integrating digital assets into traditional financial infrastructure.

We predict that by 2025, the U.S. federal government or at least one state (likely Pennsylvania, Florida, or Texas) will have established a Bitcoin reserve. At the federal level, this is more likely to be achieved through executive order using the Treasury’s Exchange Stabilization Fund (ESF), although bipartisan legislation remains an unknown. Meanwhile, state governments may act independently, looking to Bitcoin as a hedge against fiscal uncertainty or a means to attract crypto investment and innovation.

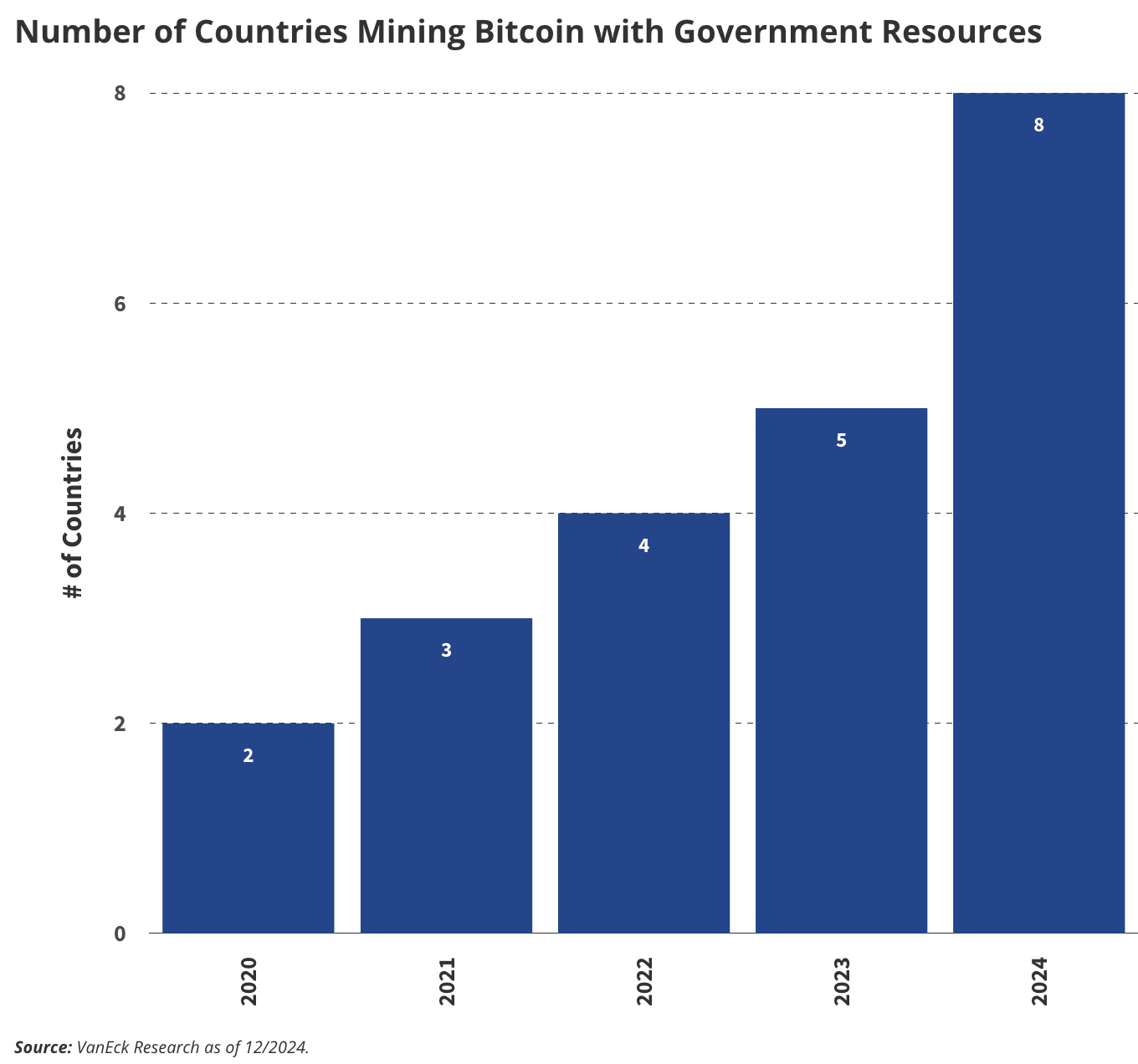

In terms of Bitcoin mining, the number of countries using government resources to mine is expected to reach double digits (currently seven), thanks to the growing adoption of cryptocurrencies in the BRICS countries. This trend is driven by Russias statement that it plans to use cryptocurrencies to settle international trade, further highlighting the global influence of Bitcoin.

We expect this pro-Bitcoin stance to ripple through the broader U.S. crypto ecosystem. The U.S. will rise from 19% to 25% of global crypto developers as regulatory clarity and incentives attract talent and companies back. At the same time, U.S. Bitcoin mining will boom, with the U.S. share of global mining power increasing from 28% in 2024 to 35% by the end of 2025, thanks to cheap energy and potential tax incentives. Together, these trends will solidify the U.S.’ leadership in the global Bitcoin economy.

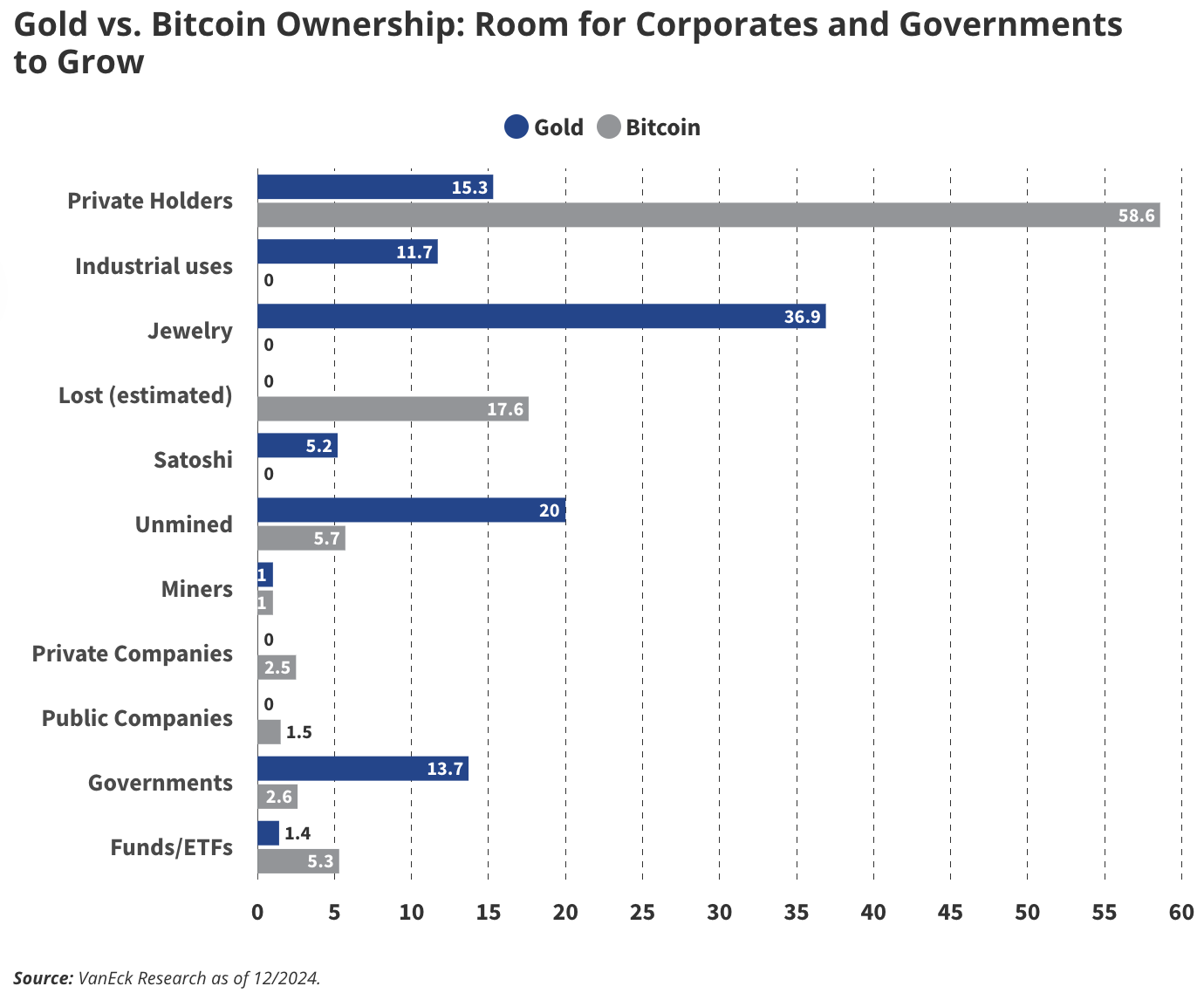

In terms of enterprise adoption, we expect companies to continue to accumulate Bitcoin from retail investors. Currently, 68 public companies hold Bitcoin on their balance sheets, and we expect this number to reach 100 by 2025. Notably, we boldly predict that the total amount of Bitcoin held by private and public companies (currently 765,000 BTC) will exceed Satoshi’s 1.1 million BTC next year. This represents a significant 43% increase in corporate Bitcoin holdings over the next year.

Cryptocurrency infrastructure promises to improve the financial system through increased efficiency, decentralization, and greater transparency. We believe 2025 will be the year tokenized securities break out. Currently, there are approximately $12 billion in tokenized securities on blockchains, the majority of which ($9.5 billion) are tokenized private credit securities on Figure’s semi-permissioned blockchain, Provenance.

In the future, we see great potential for tokenized securities to be launched on public blockchains. We believe that there are many motivations for investors to push for tokenized equity or debt securities to be issued entirely on-chain. We predict that entities like the DTCC will support the seamless transition of tokenized assets between public blockchains and private closed infrastructures in the coming year. This dynamic will lead to the establishment of AML/KYC standards for on-chain investors. As a bold prediction, we expect Coinbase to take the unprecedented step of tokenizing and deploying its COIN shares on its BASE blockchain.

Source: Artemis XYZ, data as of December 6, 2024.

Past performance is no guarantee of future results.

Stablecoins will move from a niche role in cryptocurrency trading to a core component of global commerce. By the end of 2025, we expect stablecoins to settle $300 billion per day, equivalent to 5% of current DTCC trading volume, and around $100 billion per day in November 2024. With adoption by major technology companies (such as Apple and Google) and payment networks (Visa and Mastercard), stablecoins will reデフィne payment economics.

In addition to transactional uses, the remittance market will also see explosive growth. For example, stablecoin transfers between the United States and Mexico could grow fivefold from $80 million per month to $400 million. The reasons are speed, cost savings, and the fact that more and more people view stablecoins as a utility rather than an experimental technology. Although blockchain adoption is still under discussion, stablecoins are actually a Trojan horse for blockchain technology.

Source: Dune @jdhpyer, data as of December 6, 2024.

Past performance is no guarantee of future results.

We believe AI Agents are one of the most compelling trends that will gain significant traction in 2025. AI Agents are specialized AI bots that help users achieve goals, such as “maximize revenue” or “increase engagement on X/Twitter”. These agents autonomously adjust their strategies to optimize results. AI agents are typically fed data and trained to focus on a specific domain. Currently, protocols like Virtuals provide tools for anyone to create on-chain AI agents. Virtuals allows non-technical people to access decentralized AI contributors (such as fine-tuning experts, dataset providers, and model developers), allowing ordinary users to create their own agents. This model will lead to the emergence of a large number of agents whose creators can rent out the agents to generate income.

Currently, the construction of agents is mainly concentrated in the DeFi field, but we believe that AI agents will go beyond financial activities. For example, these agents can be used as influencers on social media, virtual players in games, and interactive assistants or partners in consumer applications. Agents like Bixby そして Terminal of Truths have become important X/Twitter influencers with 92,000 and 197,000 followers respectively. As a result, we expect that more than 1 million new agents will be born in 2025.

Source: Deflama, data as of December 6, 2024.

Past performance is no guarantee of future results. Mention of securities in this article does not constitute a recommendation to buy or sell.

We are closely watching the rise of Bitcoins second layer (L2) blockchains, which have great potential to transform the Bitcoin ecosystem. By extending Bitcoins functionality, these L2 solutions can achieve lower latency and higher transaction throughput, thereby addressing the limitations of the Bitcoin main chain. In addition, Bitcoin L2 also enhances Bitcoins capabilities by introducing smart contract functions, providing support for the decentralized finance (DeFi) ecosystem built around Bitcoin.

Currently, Bitcoin can be transferred to smart contract platforms by bridging or wrapping BTC, but these methods rely on third-party systems and are vulnerable to hacking and security vulnerabilities. The Bitcoin L2 solution aims to address these risks through a framework that integrates directly with the Bitcoin main chain, thereby reducing reliance on centralized intermediaries. Although liquidity limitations and adoption barriers remain, Bitcoin L2 is expected to improve security and decentralization, providing BTC holders with greater confidence to participate more actively in the decentralized ecosystem.

As shown in the figure, Bitcoin L2 solutions have experienced explosive growth in 2024, with the total locked value (TVL) exceeding 30,000 BTC, a year-on-year increase of 600%, equivalent to approximately $3 billion. Currently, there are more than 75 Bitcoin L2 projects in development, but only a few are likely to achieve significant adoption in the long term.

This rapid growth reflects the strong demand from BTC holders for yield generation and broader use of the asset. As chain abstraction technology and Bitcoin L2 mature into products available to end users, Bitcoin will become an important part of DeFi. For example, the Ika platform on Sui or the Infinex chain abstraction technology used by Near demonstrate how innovative multi-chain solutions can enhance Bitcoins interoperability with other ecosystems.

By supporting secure and efficient on-chain lending, borrowing, and other permissionless DeFi solutions, Bitcoin L2 and abstraction technologies will transform Bitcoin from a passive store of value to an active participant in the decentralized ecosystem. As adoption scales, these technologies will unlock the huge potential of on-chain liquidity, cross-chain innovation, and a more integrated financial future.

Source: Dune @hildobby, data as of December 6, 2024.

Past performance is no guarantee of future results.

The Ethereum community is actively discussing whether its Layer-2 (L2) network can bring enough value to the Ethereum mainnet through Blob space. Blob space is a key component in Ethereums expansion roadmap. As a specialized data layer, L2 can submit a compressed version of its transaction history to Ethereum and pay ETH fees per Blob. Although this architecture supports Ethereums scalability, L2 currently pays less value to the mainnet, with a gross margin of about 90%. This has raised concerns that Ethereums economic value may be excessively transferred to L2, resulting in a decline in the utilization of the mainnet.

Despite the recent slowdown in the growth of Blobspace, we expect its usage to increase significantly by 2025, driven by three main factors:

Explosive adoption of L2: Ethereum L2 transaction volume has grown at an annualized rate of more than 300%, and users have migrated to a low-cost, high-throughput environment for DeFi, games, and social applications. As more consumer-oriented dApps emerge on L2, more transactions will flow back to Ethereum for final settlement, significantly increasing the demand for Blob space.

Rollup technology optimization: Advances in Rollup technology (such as improved data compression and reduced costs of submitting data to Blob space) will encourage L2 to store more transaction data on Ethereum, unlocking higher throughput without sacrificing decentralization.

Introduction of high-fee use cases: The rise of enterprise applications, zk-rollup-based financial solutions, and tokenized real-world assets will drive high-value transactions that prioritize security and immutability and are therefore willing to pay for blob space.

By the end of 2025, we expect Blobspace fees to exceed $1 billion, up from almost negligible amounts today. This growth will solidify Ethereum’s role as the final settlement layer for decentralized applications, while enhancing its ability to capture value from the rapidly expanding L2 ecosystem. Blobspace will not only scale the network, but will also become an important source of revenue for Ethereum, balancing the economic relationship between the mainnet and L2.

Source: Deflama, data as of December 6, 2024.

Past performance is no guarantee of future results.

Despite record volumes on decentralized exchanges (DEXs) and relative to centralized exchanges (CEXs), DeFi’s total value locked (TVL) remains 24% below its all-time peak. We expect DEX volumes to exceed $4 trillion in 2025, accounting for 20% of CEX spot volume, driven by the popularity of AI-related tokens and the emergence of new consumer-facing dApps.

In addition, the influx of tokenized securities and high-value assets will serve as a catalyst for DeFi growth, bringing new liquidity and wider use to the ecosystem. As a result, we expect DeFi’s total locked value (TVL) to rebound to over $200 billion by the end of the year.

This growth not only reflects the resurgence of decentralized finance, but also marks its rising status in the global financial system. By introducing more user-friendly dApps and innovative financial tools, DeFi will attract new capital inflows and consolidate its position as an alternative to traditional finance.

Source: Data as of December 6, 2024.

Past performance is no guarantee of future results. Mention of securities in this article does not constitute a recommendation to buy or sell.

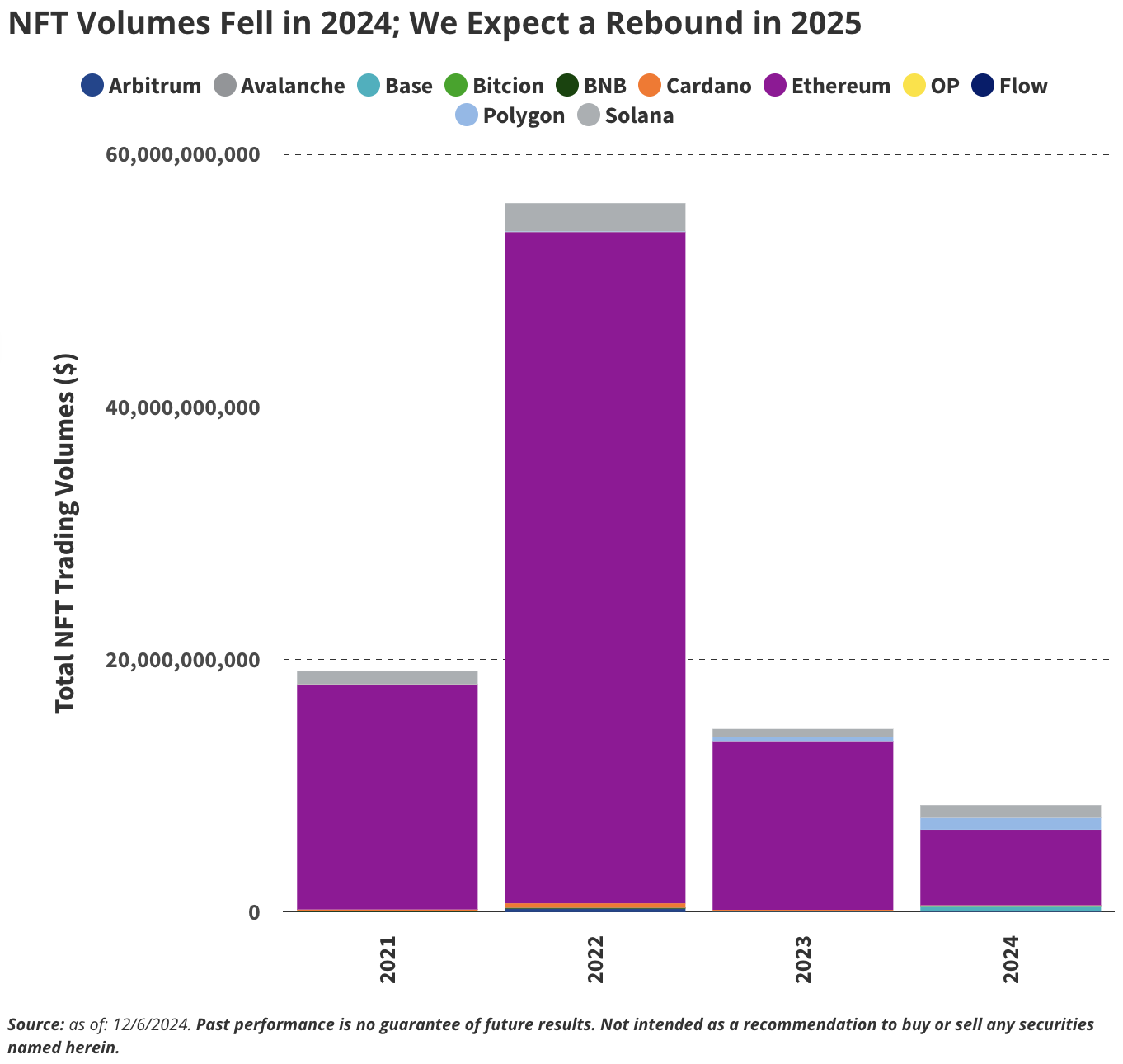

The 2022-2023 bear market hit the NFT space hard, with trading volumes down 39% since 2023 and plunging 84% from 2022. While fungible token prices began to recover in 2024, most NFTs continued to lag behind, not turning the corner until November following weak prices and low activity. Despite these challenges, some projects with strong community ties have bucked the trend by transcending speculative value.

For example, Pudgy Penguins successfully transitioned from collectible toys to a consumer brand, while Miladys gained cultural influence in the satirical internet culture space. Likewise, Bored Ape Yacht Club (BAYC) continues to grow as a dominant cultural force, attracting widespread attention from brands, celebrities, and mainstream media.

As crypto wealth recovers, we expect newly wealthy users to diversify into NFTs, not just as speculative investments, but also as assets of lasting cultural and historical significance. Established series like CryptoPunks and Bored Ape Yacht Club (BAYC) will benefit from this shift due to their strong cultural influence and relevance. While BAYC and CryptoPunks are still trading 90% and 66% below their all-time peaks (in ETH), other projects like Pudgy Penguins and Miladys have surpassed their previous highs.

Ethereum continues to dominate the NFT space, hosting the majority of significant collections. In 2024, Ethereum accounted for 71% of NFT transactions, and we expect this to rise to 85% in 2025. This dominance is also reflected in the market capitalization rankings, with NFTs on the Ethereum chain occupying all of the top 10 positions and 16 of the top 20 positions, highlighting Ethereum’s central role in the NFT ecosystem.

While NFT trading volumes may not return to the frenetic highs of previous cycles, we believe $30 billion in annualized volume is feasible, roughly 55% of the 2021 peak. The market is shifting from speculative hype to sustainability and cultural relevance.

ソース: 市場 Vectors, data as of December 8, 2024.

Past performance is no guarantee of future results. The MVSCLE index tracks the smart contract platform, and the MVIALE index tracks the infrastructure application token.

A persistent theme of the 2024 bull run is the significant excess returns of Layer-1 (L1) blockchain tokens relative to decentralized application (dApp) tokens. For example, the MVSCLE index, which tracks smart contract platforms, is up 80% year-to-date, while the MVIALE index of application tokens is up only 35% over the same period.

However, we expect this dynamic to change later in 2024 as a wave of new dApps launch with innovative and useful products, creating value for their associated tokens. Among the key thematic trends, we see artificial intelligence (AI) as a prominent category in dApp innovation. In addition, decentralized physical infrastructure network (DePIN) projects also have great potential to attract investor and user interest, thereby promoting a broader rebalancing of performance between L1 tokens and dApp tokens.

The shift highlights the importance of utility and product-market fit in determining the success of utility tokens in the evolving cryptocurrency landscape.

This article is sourced from the internet: VanEcks top ten predictions for 2025: The United States adopts BTC strategic reserves, and the bull market will reach a new high by the end of next year

Related: Roam: How many steps are there to decentralize the telecommunications industry?

Currently, the telecommunications industry is facing the dilemma of weak revenue growth and rising costs. The revenue growth rate of traditional telecommunications services, especially B2C services, has stagnated amid the increasingly fierce price war among peers. As traditional core telecommunications services have shifted from voice to VoIP, from SMS to chat, and from IPTV to video streaming, tariffs have also decreased. Restricted by the industrys existing complex systems and processes, traditional telecommunications companies find it difficult to provide truly customer-centric services and experiences. The simple and stereotyped customer packages they provide are increasingly unable to meet customer needs in the context of todays social development. At the same time, because the deployment of 5G networks requires large-scale fiber coverage and the construction of all-fiber fixed broadband networks, global telecom companies…