Weak US core PCE (and European CPI) data capped a risk-friendly week, with the US yield curve continuing its bullish steepness, while US and Chinese stock markets both hovered at cycle highs. On a 3-month moving average basis, annualized core inflation for CPI and PCE has fallen back to around 2%, moving towards the Feds 2% long-term target, allowing the Fed to continue to focus on its tasks in the job market. After the CPI was released, several investment banks reiterated their forecasts for a 50 basis point rate cut in December, while interest rate futures pricing in a 50 basis point rate cut in November returned to around 50%.

On the other hand, US consumer confidence jumped to a 5-month high on the back of the Feds aggressive easing and falling oil prices. Global beta trading has picked up, with Chinese and Hong Kong stocks having their best week in years (the CSI 300 rose 16%), thanks to Chinas heavy stimulus policy, and well-known investor David Tepper calling on market investors to buy everything China-related assets after the Peoples Bank of China announced its easing policy.

For example, iron ore has risen 20% since the end of September as China eased restrictions on home purchases, while a rapid surge in market trading activity also caused the Shanghai Stock Exchanges system to fail, while Chinese ETFs saw their highest daily inflows since 2021.

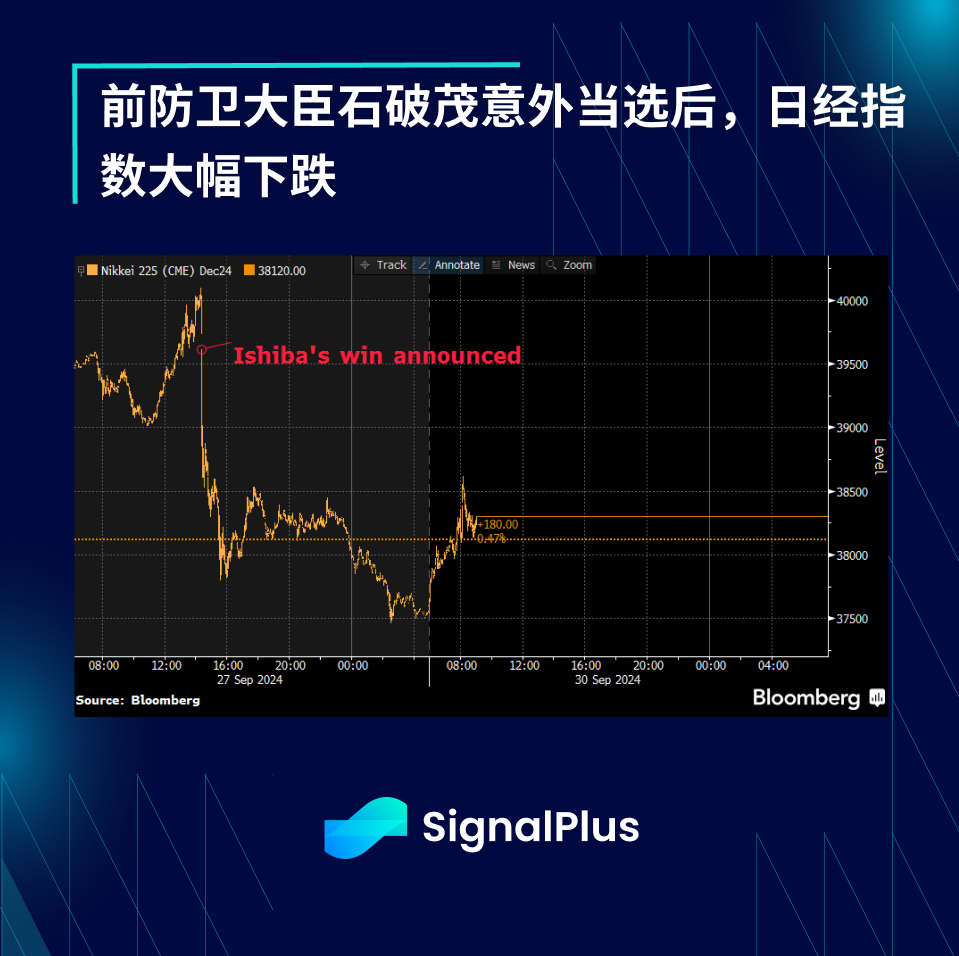

While the US and Chinese markets are strong, Japanese stocks are facing a new round of volatility following the unexpected election win by Shigeru Ishida. The former defense minister has publicly opposed Abenomics in the past and supports the normalization of the Bank of Japans policy. Japanese stock futures fell 6% and the yen rose to 142 as investors worried about further rate hikes by the Bank of Japan and a more aggressive geopolitical stance by the new prime minister. Next, the Bank of Japans speech this week will be the focus of the market.

Back in the US, this week will see a lot of important economic data, including JOLTS, ISM manufacturing and services indexes, and of course the non-farm payrolls report. In addition, there are multiple Fed officials speaking this week, and the market does not think that officials will try to stir up the market despite the fact that the US financial situation has eased to a cycle high. Powell will speak on the US economic outlook at the National Association for Business Economics meeting on Monday, and the market expects that his speech will not be far from the last FOMC meeting, especially considering that the recent inflation data trend is in his favor.

In addition, the United States will hold a televised debate for vice presidential candidates on Tuesday evening, but the market expects this to have little impact on the election, as current polls show a very tight race. China is on holiday during the Golden Week, so macro and cryptocurrency trading activity is expected to be relatively flat during the Asian session this week.

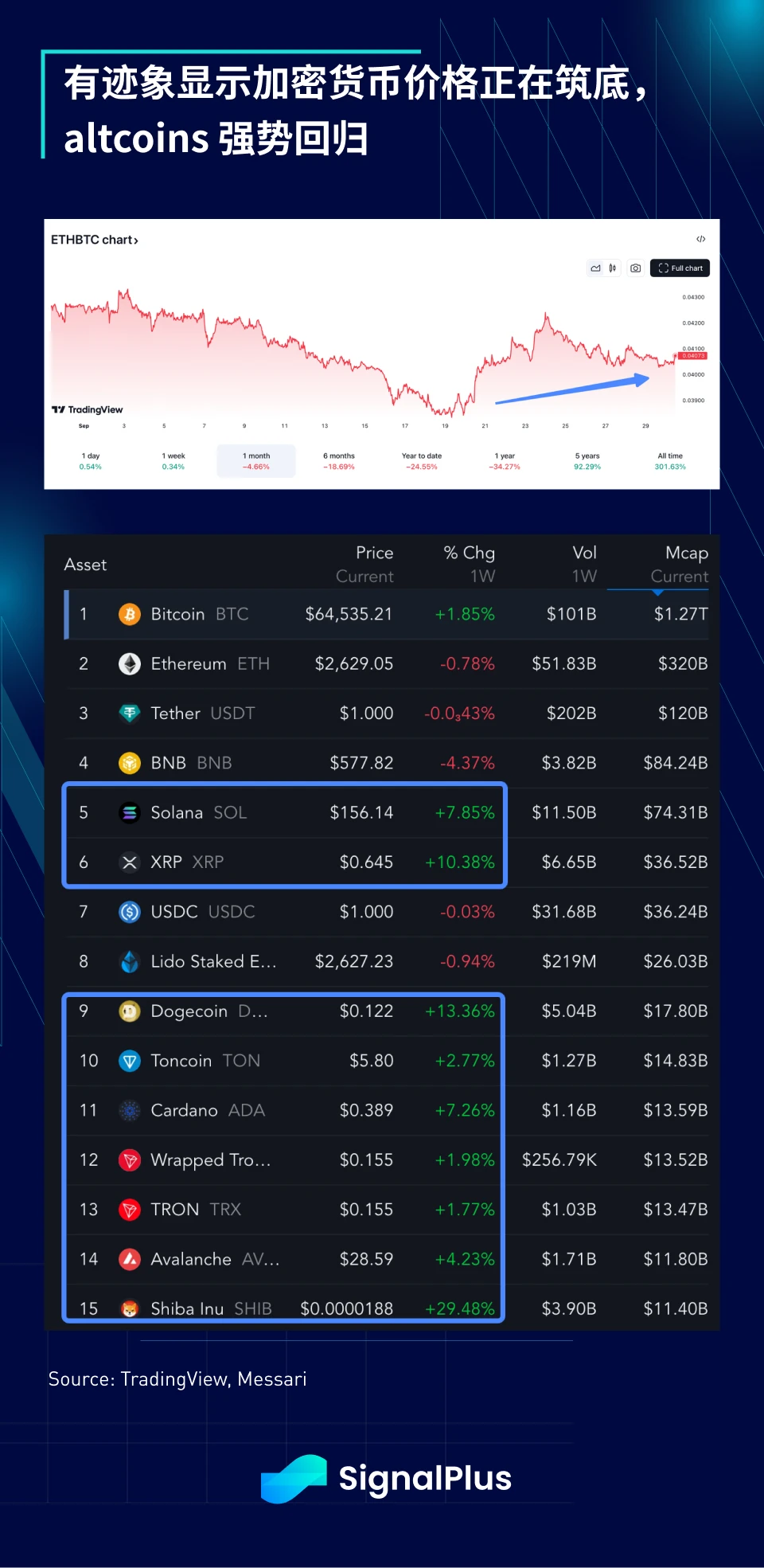

In terms of cryptocurrencies, BTC has performed well against the backdrop of loose liquidity, with strong economic growth, stable corporate earnings, and dovish central banks laying a solid foundation for BTCs rebound in the fourth quarter. Although ETF flows have been disappointing since July (ETH ETF outflows of $610 million and BTC ETF outflows of $330 million), ETH has performed well in the recent rebound, and altcoins have also returned strongly.

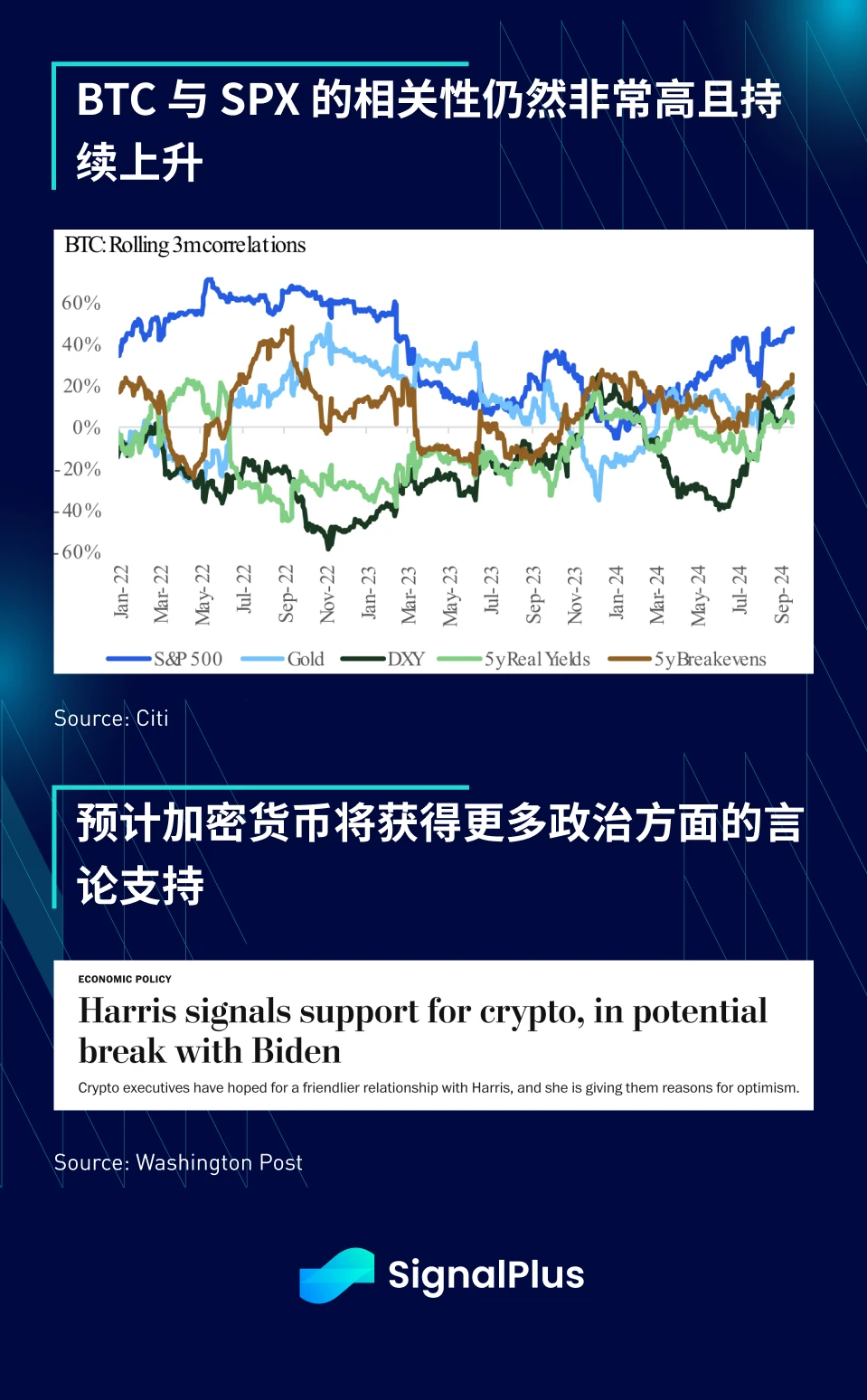

As cryptocurrencies remain highly correlated with macro assets, especially with the SPX index, we believe the friendly macro backdrop will continue to provide strong support for crypto prices in the fourth quarter. In addition, with Kamala Harris’s camp “endorsing” cryptocurrencies on the campaign trail, we remain bullish on near-term price action. As investors shift into “buy on dips” mode, we expect targeted short put option strategies to be popular. Wish you all good trading and a happy holiday!

t.signalplus.com の SignalPlus トレーディング ベーン機能を使用すると、よりリアルタイムの暗号通貨情報を入手できます。最新情報をすぐに受け取りたい場合は、Twitter アカウント @SignalPlusCN をフォローするか、WeChat グループ (アシスタント WeChat: SignalPlus 123 を追加)、Telegram グループ、Discord コミュニティに参加して、より多くの友人とコミュニケーションおよび交流してください。

シグナルプラス公式サイト: https://www.signalplus.com

This article is sourced from the internet: SignalPlus Macro Analysis Special Edition: Labour Week

As the market value of PayPal USD (PYUSD), the US dollar stablecoin launched by Paypal and issued by Paxos, has exceeded the $1 billion mark, the market value of this stablecoin supported by the giant PayPal has increased by 327% compared to the beginning of 2024. Such a huge increase has triggered extensive discussions in the community. The reason why PYUSD issuance has achieved such a rapid growth is mainly due to the high incentive strategy recently launched by PYUSD. According to the authors estimation based on the current TVL and APY of PYUSD on the chain, the interest paid to users by PYUSD incentive activities alone exceeds 6.5 million US dollars per month. As of the time of writing, the APY yield of PYUSD on the DeFi protocol on…