My XP

0

Login

By Alex Thorn and Gabe Parker, Research Analysts, Galaxy Digital

Compiled by: Yangz, Techub News

Compared to the strong performance of Bitcoin and liquid cryptocurrencies in the first quarter, the market cooled slightly in the second quarter, but it still grew significantly compared to the same period last year. The rebound trend of cryptocurrency venture capital in the first quarter seems to be continuing. The performance of industry founders and investors in the second quarter means that the financing environment has become more active than in previous quarters. However, as of July 1, the data performance is slightly worse than the general market sentiment.

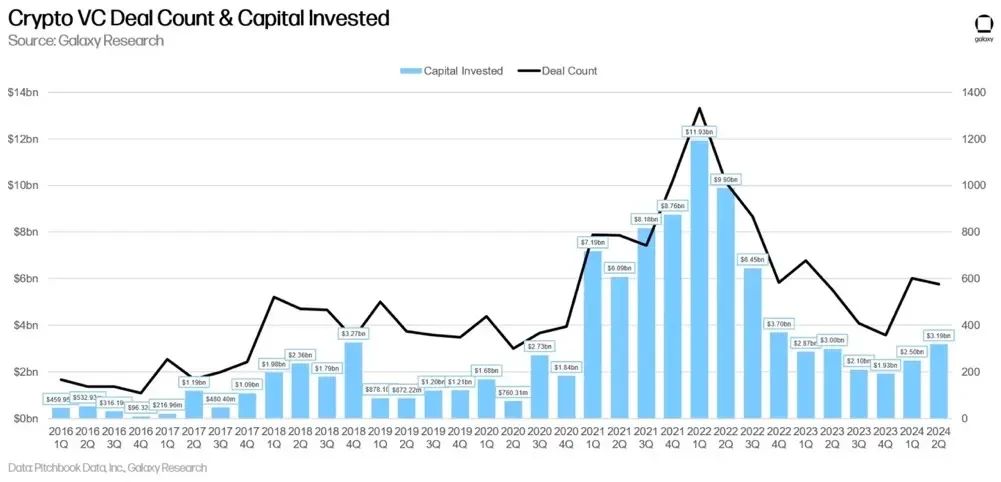

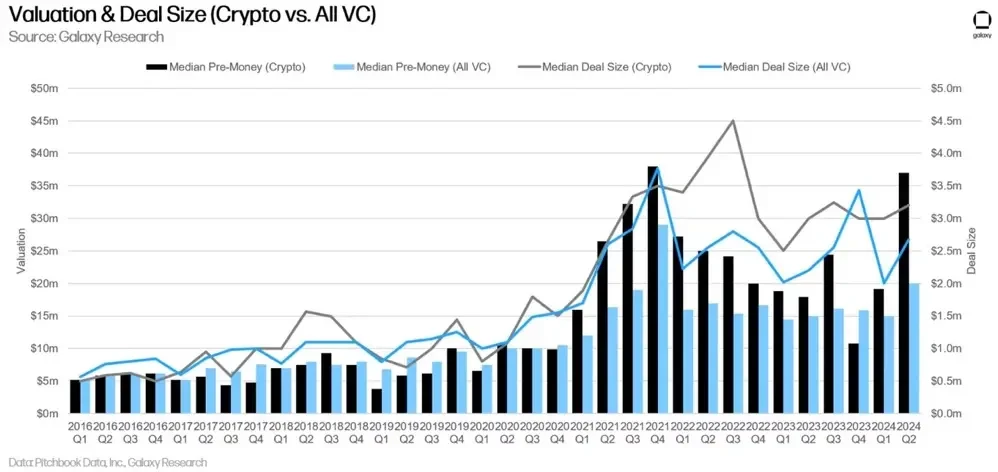

The number of industry VC deals in the second quarter fell slightly from 603 in the first quarter to 577 in the second quarter, while investment capital increased from $2.5 billion in the first quarter to $3.2 billion in the second quarter. The median deal size increased slightly from $3 million to $3.2 million, but the median pre-money valuation increased from $19 million to $37 million, close to the historical high. These data show that despite the lack of available investment capital compared to the previous peak, the recovery of the cryptocurrency market in the past few quarters has brought fierce competition and triggered their FOMO.

In the second quarter of 2024, venture capitalists invested $3.194 billion in cryptocurrency and blockchain companies (up 28% from the previous quarter) across 577 deals (down 4% from the previous quarter).

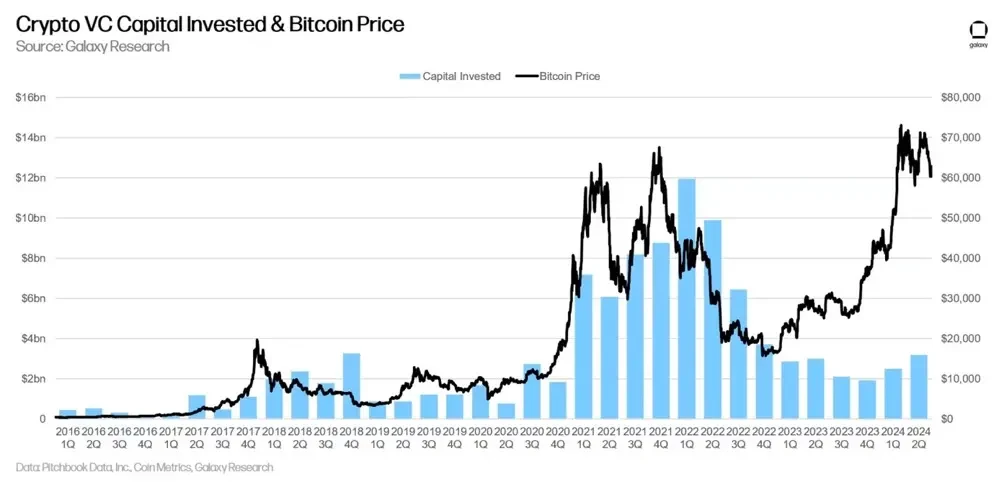

The multi-year correlation between Bitcoin price and capital invested in crypto startups has broken. Bitcoin has risen sharply since January 2023, while VC activity has not kept pace. While Bitcoin has risen sharply this year and invested capital has also risen, it is still far below the levels when Bitcoin broke through $60k in 2021-2022. Crypto native catalysts such as Bitcoin ETFs and emerging areas (such as re-staking, modular, Bitcoin L2), as well as pressure from crypto startup bankruptcies and regulatory challenges, combined with macroeconomic headwinds (interest rates), have led to this stark divergence. Now, as liquid crypto recovers, VCs are preparing to return and VC activity will increase in the second half of this year.

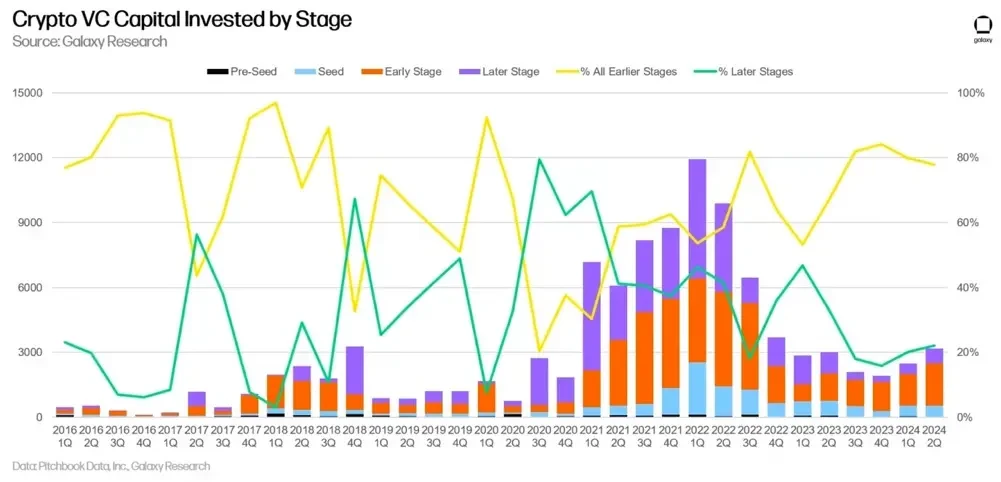

In the second quarter of 2024, 78% of funds were allocated to early-stage companies and 20% to late-stage companies. While early-stage VC funds focused on cryptocurrencies are active and have reserves left over from 2021 and 2022, large integrated VC firms appear to have exited the industry or significantly scaled back their activities, making it more difficult for late-stage startups to raise funds.

In terms of deal volume, the share of Pre-Seed deals has slightly decreased, but is still higher than in the previous market cycle.

Valuations of venture-backed crypto companies fell sharply in 2023, falling in Q4 to the lowest median pre-money valuation since Q4 2020. However, in Q1 2024, valuations of venture-backed crypto companies began to rebound, soaring to $37 million in Q2 (up 94% Q/Q), the highest level since Q4 2021. It is important to note that reporting delays and the lack of public valuation data will cause the above data to fluctuate significantly as more data becomes available. We strive to provide this information promptly after the end of the quarter, so the data may be revised, but this spike is still a signal. In addition, the median deal size increased slightly Q/Q (+7%) to $3.2 million, which is basically the same as the past five quarters. The increase in valuations is due to improved market sentiment; founders have captured the interest and competition of the existing investor base despite the lack of significant increase in investment capital.

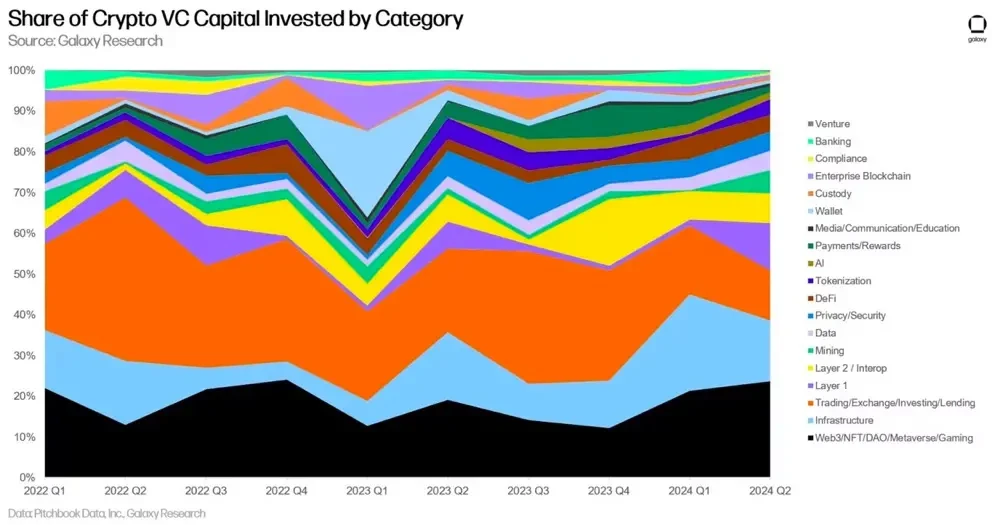

In the second quarter of 2024, cryptocurrency companies and projects in the Web3/NFT/DAO/Metaverse/Games category raised a total of $758 million in crypto VC funding, accounting for the largest share of all categories (24%). The two largest deals in this category were Farcaster and Zentry, which raised $150 million and $140 million, respectively.

Close behind are companies/projects related to infrastructure, transactions, and L1, with investments accounting for 15%, 12%, and 12%, respectively. It is worth noting that the market share of investment capital in the L1 category increased by more than 6 times, as Monad and Berachain raised $225 million and $100 million, respectively. In addition, Bitcoin L2 raised $94.6 million in Q2 2024, a month-on-month increase of 174% (from $34.7 million in Q1).

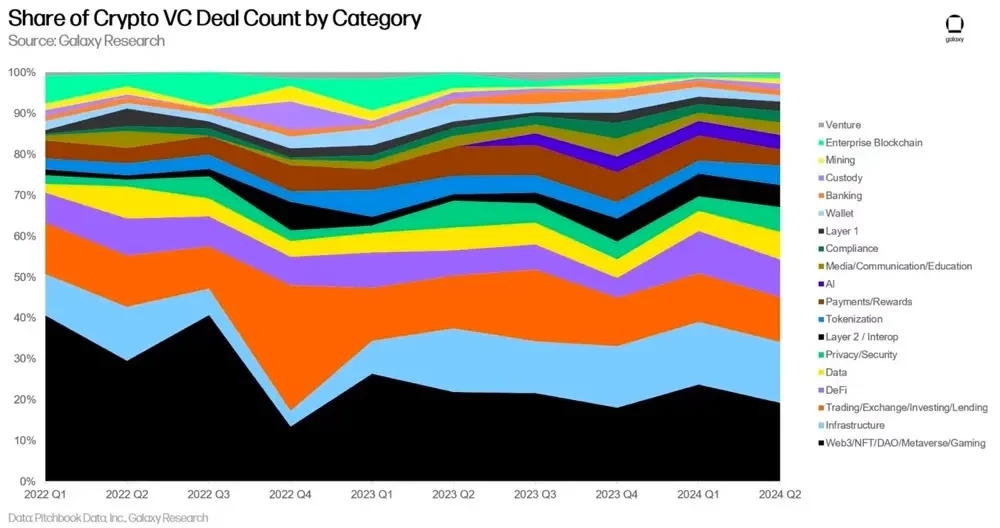

In terms of the number of transactions, the Web3/NFT/DAO/Metaverse/Game category leads the pack with 19%, thanks mainly to an increase in decentralized social media and gaming-related transactions. While the number of financings for crypto startups related to restaking declined in the second quarter of 2024, the number of transactions in the infrastructure category ranked second this quarter, accounting for 15%.

Closely following are cryptocurrency companies/projects related to trading and DeFi, accounting for 11% and 9% of the total number of completed transactions in Q2 2024, respectively.

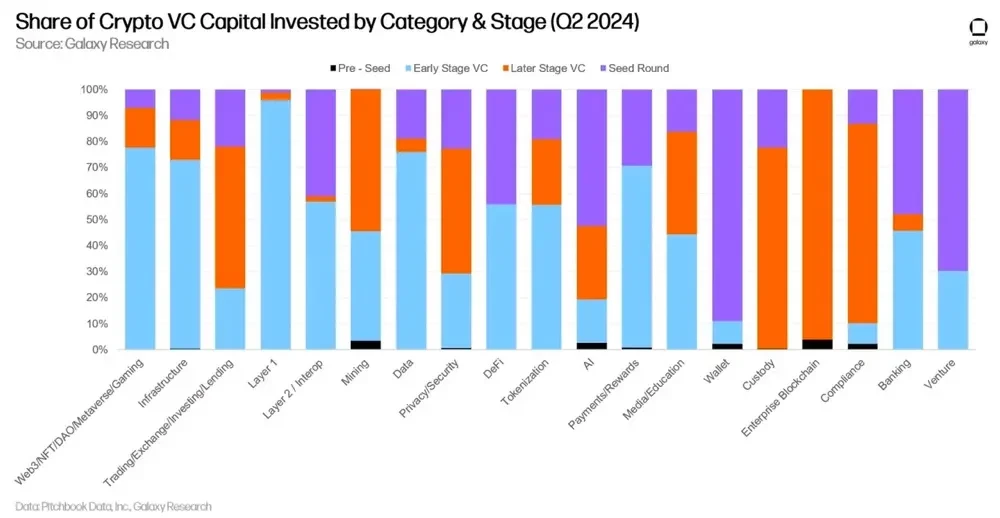

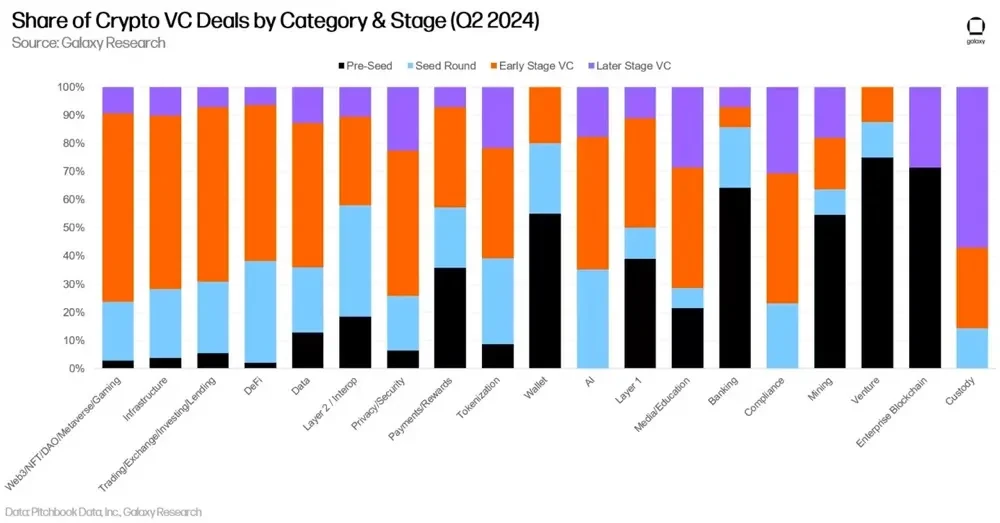

Breaking down investment capital and deal count by stage and category provides a clearer picture of what types of companies are raising funding in each category. In Q2 2024, the vast majority of funding in the Web3, L1, and Infrastructure categories went to early-stage companies and projects, while venture capital in the Deals category went more to companies in later stages of funding.

By studying the share of capital invested in each category at each stage, we can gain insight into the maturity of each category of investable capital.

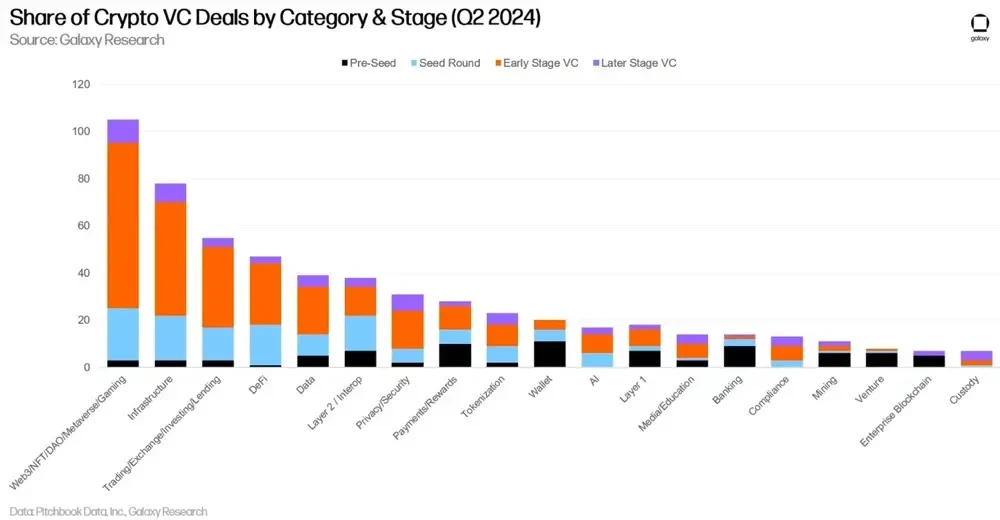

The number of deals tells a similar story, with a significant portion of completed deals in almost all categories involving early-stage companies and projects.

By examining the share of deals completed at each stage within each category, we can gain insight into the various stages within each investable category.

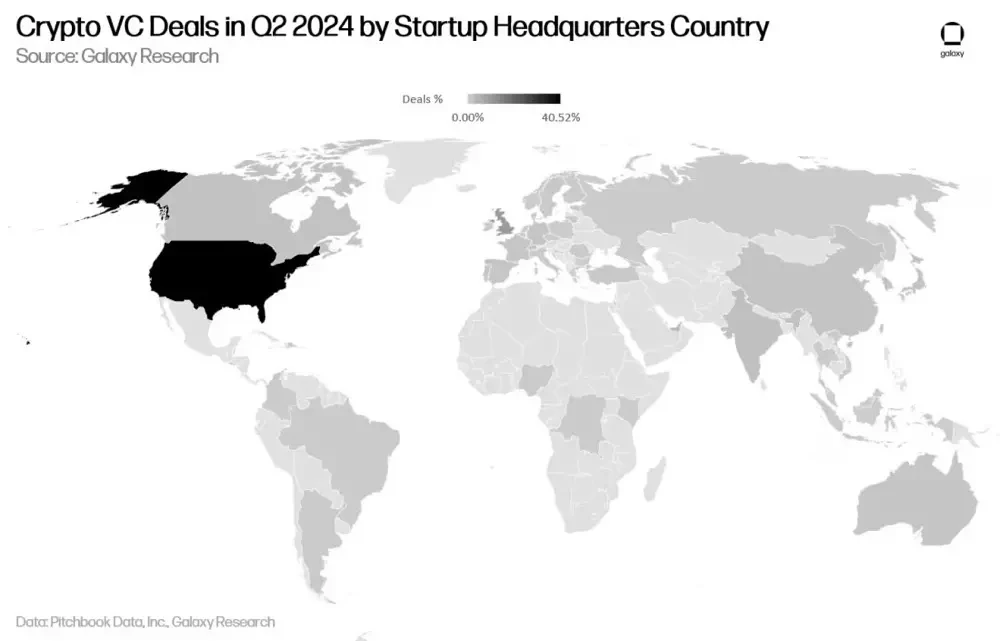

In terms of investment volume, more than 40% of venture capital went to companies headquartered in the United States in the second quarter of 2024. The United Kingdom accounted for 10%, Singapore accounted for 8.7%, the United Arab Emirates accounted for 3.13%, and Hong Kong accounted for 2.78%.

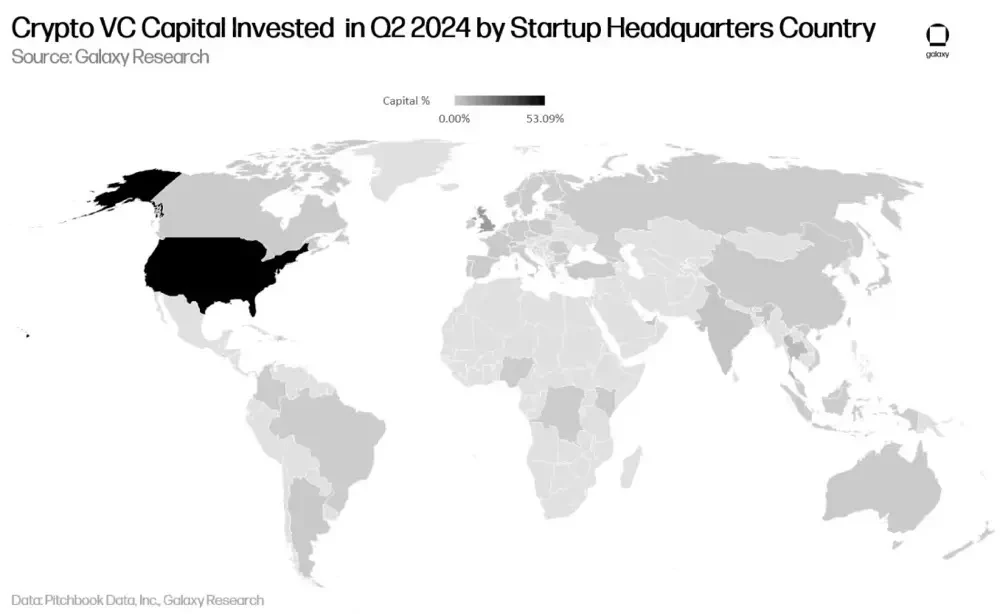

In terms of investment amount, companies headquartered in the United States attracted 53% of venture capital, an increase of 23.5% month-on-month. The United Kingdom accounted for 12.78%, Singapore accounted for 4.6%, and the United Arab Emirates accounted for 4.39%.

The vast majority of venture capital in the second quarter of 2024 went to companies founded between 2021 and 2023.

Crypto venture capital sentiment continues to improve, but levels remain significantly lower than the 2021-2022 bull run. With Bitcoin and Ethereum up about 50% this year, investment capital grew 28% month-over-month, while deal count remained roughly flat. If this growth rate continues through the end of the year, 2024 would rank third in investment capital and deal count, behind only 2021 and 2022.

Investments in the Web3 and L1 categories were notable. The Web3 category led the way with a total of approximately $750 million, driven by Farcaster ($150 million) and Zentry ($140 million). L1 ranked fourth with $371 million, driven by deals in Monad ($225 million) and Berachain ($100 million).

The median valuation of venture-backed cryptocurrency companies has soared to the highest level since the fourth quarter of 2021 (the peak of the previous bull market). Affected by the 2022 bear market and adverse macroeconomic factors, most general venture capital firms are still on the sidelines, while venture capital firms focusing on cryptocurrencies are in an increasingly competitive environment, providing project founders with more bargaining chips. It should be noted that the median is based on available data as of July 1, and as more transaction information in the second quarter increases, the median may be updated and may be adjusted downward.

Bitcoin L2 continues to receive a lot of investment, with related companies and projects raising a total of $94.6 million, a month-on-month increase of 174%. Investors are still enthusiastic about the emergence of more composable block spaces in the Bitcoin ecosystem and the return of models such as DeFi and NFT. Our internal research shows that at least 65 projects claim to be Bitcoin L2.

Early-stage deals dominated the second quarter, receiving nearly 80% of investment capital, with Pre-Seed rounds accounting for 13% of all deals. The continued focus on early-stage deals bodes well for the long-term health of the broader cryptocurrency ecosystem. While some late-stage companies struggle to raise capital, entrepreneurs are finding investors willing to invest in new and innovative ideas.

The United States continues to dominate the cryptocurrency startup ecosystem. While the United States maintains a clear lead in transactions and capital, regulatory headwinds may force more companies to move to other countries and regions. If the United States wants to remain a center of technological and financial innovation in the long term, policymakers need to be aware of how their actions or inactions will affect the cryptocurrency and blockchain ecosystem.

This article is sourced from the internet: Galaxy Digital Q2 Crypto Venture Capital Report: The rebound is still continuing, but there is still a gap with the previous bull market

Related: One-week token unlocking: ALT unlocks 6.9% of the circulating tokens

Next week, 9 projects will have token unlocking events. ALT will have 5% of its tokens unlocked, and other high-proportion unlocking projects include YGG, PORTAL, OP, etc., but the amounts are relatively small. The specific unlocking details are as follows: AltLayer Project Twitter: https://twitter.com/alt_layer Project official website: https://altlayer.io/ Number of tokens unlocked this time: 105 million Amount unlocked this time: Approximately 19.9 million US dollars AltLayer is an open, decentralized Rollups protocol that combines the concept of Restaked rollup. It takes existing rollups (derived from any rollup stack, such as OP Stack, Arbitrum Orbit, ZKStack, Polygon CDK, etc.) and provides them with enhanced security, decentralization, interoperability, and fast finality. In addition, AltLayer also provides temporary execution layer services. This round of unlocking is a regular linear unlocking of ALT. Since…