My XP

0

Login

Original author: David Han

原文翻訳: TechFlow

The multiple roles categorized for ETH raise questions about its place in a portfolio, and this article will clarify some of these narratives, as well as potential tailwinds for the asset in the coming months.

Despite ETH’s poor performance year-to-date, we believe its market positioning remains strong in the long term.

We believe that ETH has the potential to deliver unexpected gains in the late cycle. We also believe that ETH has the strongest sustained demand momentum in the crypto market and maintains its unique expansion roadmap advantages.

ETH’s historical trading patterns suggest that it benefits from the dual narratives of “store of value” and “tech token”.

The approval of a BTC spot ETF in the US strengthens BTC’s store of value narrative and its position as a macro asset. On the other hand, there are still unanswered questions around ETH’s fundamental positioning in the crypto space. Competing layer-1 networks such as Solana have weakened ETH’s position as the preferred network for decentralized application (dApp) deployment. ETH’s L2 expansion and the reduction of ETH burns also seem to affect the asset’s value accumulation mechanism at a high level.

Nonetheless, we continue to believe that ETHs long-term positioning remains strong, with important advantages that other smart contract networks do not possess. These advantages include the maturity of the Solidity developer ecosystem, the popularity of its EVM platform, the utility of ETH as DeFi collateral, and the decentralization and security of its mainnet. In addition, we believe that advances in tokenization may have a more positive impact on ETH relative to other layer-1 networks in the short term.

We find that ETHs ability to capture the store of value and tech token narratives is reflected in its historical trading patterns. ETH has a high correlation with BTC, showing behavior consistent with BTCs store of value model. At the same time, it also decouples from BTC during long-term BTC price increases, behaving more like a technology-oriented cryptocurrency like other altcoins. We believe that ETH will continue to play these roles and is expected to outperform in the second half of 2024 despite its poor performance year-to-date.

ETH has been categorized in many ways, from being considered an “ultrasonic currency” named for its supply reduction mechanism to being called an “internet bond” for the non-inflationary nature of its staking returns, and with the development of second-layer networks (L2s) and the addition of re-staking functions, new descriptions such as “settlement layer assets” or more complex “general objective work tokens” have emerged. However, we believe that these descriptions do not fully capture the vitality of Ethereum. In fact, as Ethereum’s application scenarios continue to enrich and complicate, it has become increasingly difficult to fully assess its value through a single value metric. More importantly, these different descriptions may conflict with each other, which can have a negative effect because they may offset each other – distracting market participants from the positive drivers of the token.

Spot ETFs are extremely important for BTC as they provide regulatory clarity and a path for new capital inflows. These ETFs structurally change the industry and challenge the previous model of capital circulation, which was capital moving from BTC to ETH to higher beta altcoins. There is a barrier between the capital allocated to ETFs and that allocated to centralized exchanges (CEXs), which only have access to the broader crypto asset space. The potential approval of a spot ETH ETF would remove this barrier and allow ETH to access the same pool of capital currently only enjoyed by BTC. In our view, this may be the biggest unanswered question for ETH in the near term, especially given the current challenging regulatory environment.

While the SEC’s silence on issuers makes timely approval uncertain, we believe the existence of a US spot ETH ETF is a matter of when, not if. In fact, the main rationale for approving a spot BTC ETF applies equally to a spot ETH ETF. That is, the correlation between the CME futures product and the spot rate is high enough that “CME’s surveillance can reasonably be expected to detect improper behavior in the spot market.” The correlation study period in the spot BTC approval notice began in March 2021, one month after the launch of CME ETH futures. We believe this evaluation period was deliberately chosen in order to apply similar logic to the ETH market. In fact, previous analysis presented by Coinbase and Grayscale suggests that the spot and futures correlations in the ETH market are similar to those of BTC.

Assuming this correlation analysis holds, the remaining possible reasons for disapproval may stem from fundamental differences between ETH and BTC. In the past , we have discussed some differences in the size and depth of the ETH and BTC futures markets, which may have been a factor in the SECs decision. But among other fundamental differences between ETH and BTC, we believe the most relevant approval issue is ETHs Proof of Stake (PoS) mechanism.

In the absence of clear regulatory guidance on the treatment of staking of the asset, we believe it is unlikely that a spot ETH ETF that supports staking will be approved in the near term. Potentially ambiguous fee structures from third-party staking providers, differences between validator clients, complexity of slashing conditions, and liquidity risks (and exit queue congestion) of unstaking are materially different from BTC. (It is worth noting that some European ETH ETFs include staking, but generally, European exchange-traded products differ from those offered in the United States.) Nonetheless, we believe this should not affect the status of unstaked ETH.

We think this decision could be a surprise. Polymarket predicts a 16% chance of approval on May 31, 2024, and Grayscale Ethereum Trust (ETHE) is trading at a 24% discount to net asset value (NAV). We think the odds of approval are closer to 30-40%. As crypto becomes an election issue, we are also unsure if the SEC is willing to invest the necessary political capital to support a decision to reject crypto. Even if the first deadline of May 23, 2024 is rejected, we think the chances of overturning the decision through litigation are high. It is worth noting that not all applications for spot ETH ETFs must be approved at the same time. In fact, Commissioner Uyedas approval statement on the spot BTC ETF criticized the disguised motivation to accelerate the approval of applications to prevent a first-mover advantage.

At the adoption level, highly scalable integration links, especially Solana, appear to be eroding ETHs market share. High throughput and low-fee transactions have shifted the center of trading activity away from the ETH mainnet. Notably, Solanas ecosystem has grown from accounting for only 2% of decentralized exchange (DEX) trading volume to 21% today over the past year.

We believe that alternative L1s now also offer more meaningful differentiation than during the last bull run. The move away from the ETH Virtual Machine (EVM) and the redesign of dApps from the ground up have resulted in unique user experiences (UX) in different ecosystems. In addition, the integrated/monolithic approach to scaling enhances cross-application composability, avoiding the issues of bridging UX and liquidity fragmentation.

While these value propositions are important, we believe it is premature to use incentivized activity metrics as confirmation of success. For example, the number of transacting users on some ETH L2s has dropped by over 80% from the peak of the airdrop. Meanwhile, Solana’s share of total DEX volume grew from 6% to 17% between Jupiter’s airdrop announcement on November 16, 2023, and the first claim date on January 31, 2024. (Jupiter is the leading DEX aggregator on Solana.) Jupiter has three more airdrops to go, so we expect activity on the Solana DEX to continue for some time. In the interim, assumptions about long-term activity retention remain speculative.

That being said, trading activity on leading ETH L2s like Arbitrum, Optimism, and Base now accounts for 17% of total DEX volume (combined with ETH’s 33%). This may provide a more appropriate comparison for ETH demand drivers vs. alternative L1 solutions, as ETH is used as the native fuel token for these three L2s. Other additional demand drivers for ETH are untapped in these networks, which provides room for future demand catalysts. We believe this is a more equivalent comparison of integrated vs. modular scaling approaches in terms of DEX activity.

Another, more “sticky” measure of adoption is stablecoin supply. Stablecoin distribution tends to change more slowly due to frictions in bridging and issuance/redemption. (See Exhibit 2. The color scheme and arrangement are the same as in Exhibit 1, with Thorchain replaced by Tron.) Activity, as measured by stablecoin issuance, is still dominated by ETH. In our view, this is because the trust assumptions and reliability of many new chains are not yet strong enough to support large amounts of capital, especially capital locked in smart contracts. Large capital holders are generally indifferent to ETH’s higher transaction costs (relative to scale) and prefer to reduce risk by reducing liquidity pause times and minimizing bridging trust assumptions.

Even so, among high-throughput chains, ETH L2s are growing their stablecoin supply faster than Solana. Arbitrum’s stablecoin supply has surpassed Solana’s at the start of 2024 ($3.6 billion vs. $3.2 billion currently), while Base’s stablecoin supply has grown from $160 million at the start of the year to $2.4 billion. While the final verdict on the scaling debate is unclear, early signs of stablecoin growth may actually favor ETH L2s over alternative L1s.

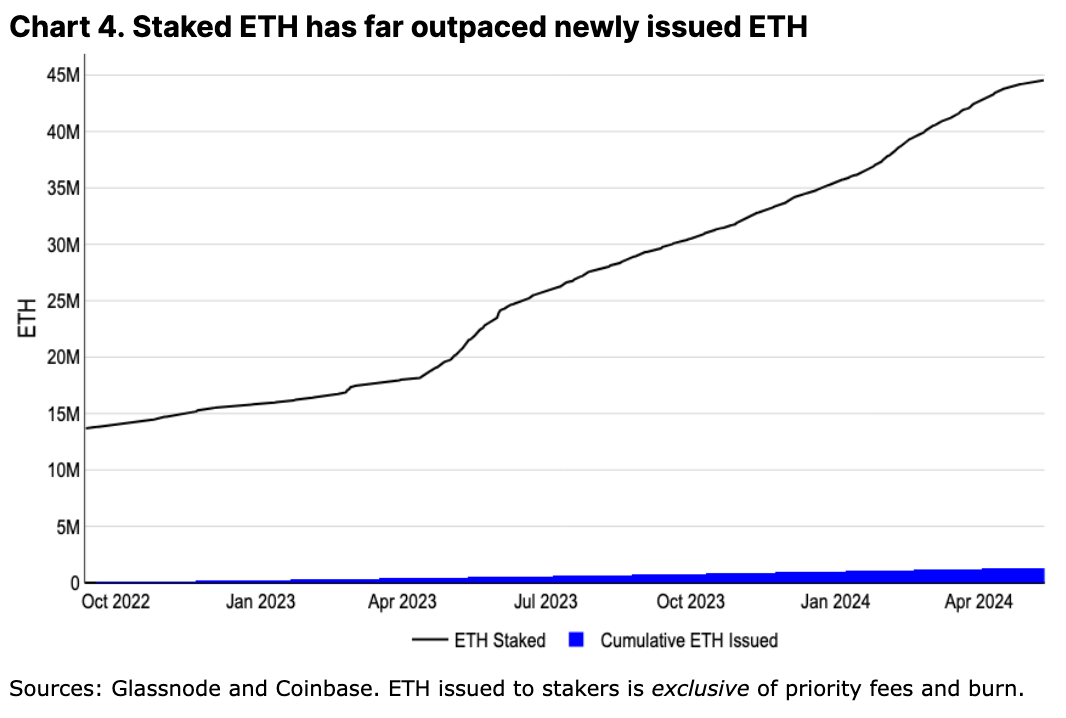

The growth of L2s has raised concerns about the actual threat they may pose to ETH – they reduce the demand for L1 block space (and therefore reduce transaction fee burns) and may support non-ETH gas tokens in their ecosystems (further reducing ETH burns). In fact, ETH has seen its highest annualized inflation rate since the switch to a proof-of-stake (PoS) mechanism in 2022. While inflation is often understood as a structurally important component of BTC supply, we do not believe this applies to ETH. All ETH issuance is owned by stakers, and since the merger, stakers collective balance far exceeds cumulative ETH issuance (see Figure 4). This is in stark contrast to BTCs proof-of-work (PoW) miner economics, where the competitive hashrate environment means miners need to sell a large portion of newly issued BTC to fund operations. While miners BTC holdings are tracked across cycles to account for their inevitable selling, ETH has the lowest staking operating costs, meaning stakers can continue to increase their holdings. In fact, staking has become a gathering point for ETH liquidity — the growth of ETH in stake has exceeded ETH issuance (even excluding destruction) by 20x.

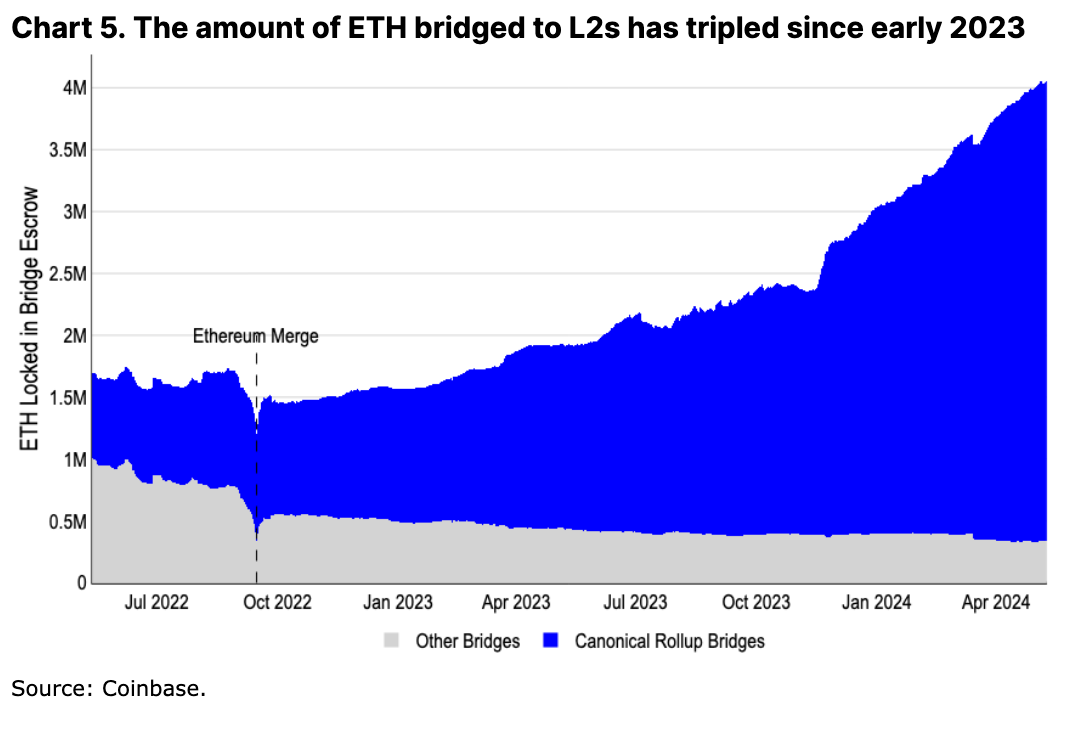

L2s themselves are also a significant demand driver for ETH. Over 3.5 million ETH has been moved to the L2 ecosystem, becoming another liquidity aggregation point for ETH. In addition, even if the ETH transferred to L2s is not directly destroyed, the remaining balance of native tokens held by new wallets to pay transaction fees also constitutes a soft lock-up of an increasing portion of ETH tokens.

Furthermore, we believe that some core activity will always remain on the ETH mainnet, even as their L2s scale. Things like EigenLayer’s restaking activity or governance actions of major protocols like Aave, Maker, and Uniswap remain firmly rooted in L1. Users with the highest security concerns (typically those with the largest capital) may also keep funds on L1 until fully decentralized sorters and permissionless fraud proofs are deployed and tested — a process that could take years. Even as L2s innovate in different directions, ETH will always be a component of their treasury (used to pay L1 “rent”) and native unit of account. We firmly believe that the growth of L2s is not only good for the ETH ecosystem, but also for ETH as an asset.

In addition to the commonly covered metric-based narratives, we believe ETH has other, harder to quantify but equally important strengths. These may not be short-term tradable narratives, but rather represent a set of long-term strengths that could sustain its current dominance.

One of the most important uses of ETH in DeFi is as collateral. ETH can be leveraged with minimal counterparty risk in the ETH and its L2 ecosystem. It acts as a collateral in money markets like Maker and Aave, and is also the base trading unit for many on-chain DEX pairings. The expansion of DeFi on ETH and its L2s has led to additional liquidity aggregation for ETH.

While BTC remains the primary store of value asset more broadly, using wrapped BTC on ETH introduces cross-chain bridges and trust assumptions. We do not believe WBTC will replace ETH for DeFi-based ETH usage — WBTC supply has remained flat for over a year and is over 40% below its previous high. Instead, ETH can benefit from the diversity of its L2 ecosystem.

An often-overlooked component of the ETH community is its ability to continue to innovate even as it decentralizes. ETH has been criticized for its extended release timeline and development delays, but few acknowledge the complexity of balancing the goals and objectives of diverse stakeholders to achieve technological progress. Developers of more than five execution clients and more than four consensus clients need to coordinate designing, testing, and deploying changes without causing disruption to mainnet execution.

Since BTC’s last major Taproot upgrade in November 2021, ETH has enabled dynamic transaction burning (August 2021), transitioned to PoS (September 2022), enabled staking withdrawals (March 2023), and created blob storage for L2 scaling (March 2024), among a host of other ETH Improvement Proposals (EIPs). While many other L1s appear to be able to develop faster, their single clients make them more fragile and centralized. The path toward decentralization inevitably leads to a degree of rigidity, and it is unclear whether other ecosystems are capable of creating similarly effective development processes if and when they begin this process.

This is not to say that ETH is innovating slower than other ecosystems. On the contrary, we believe that ETH’s innovation around execution environments and developer tooling is actually outpacing its competitors. ETH benefits from the rapid, centralized development of L2s, all of which pay settlement fees to L1. The ability to create diverse platforms with different execution environments (such as Web Assembly, Move, or the Solana virtual machine) or other features (such as privacy or enhanced staking rewards) means that the slow development timeline of L1 does not prevent ETH from gaining acceptance in more technologically comprehensive use cases.

Meanwhile, the ETH community’s efforts to define different trust assumptions and definitions around sidechains, Validium, Rollup, etc. have led to greater transparency in the space. For example, similar efforts in the BTC L2 ecosystem (such as L2ビート ) have yet to emerge, where trust assumptions for L2 vary widely and are generally not well communicated or understood by the broader community.

Innovation around the new execution environment does not mean that Solidity and EVM will become obsolete in the near future. On the contrary, EVM has been widely popularized to other chains. For example, many BTC L2s have adopted the research results of ETH L2. Some defects of Solidity (such as the easy introduction of reentrancy vulnerabilities) now have static tool checkers to prevent basic vulnerabilities. In addition, the popularity of the language has also created a mature audit sector, a large number of open source code samples, and detailed best practice guides. All of these are essential to building a large development talent pool.

Although the use of the EVM does not directly lead to the demand for ETH, changes to the EVM are rooted in the development process of ETH. These changes are then adopted by other chains to maintain compatibility with the EVM. We believe that it is likely that core innovations in the EVM will remain rooted in ETH – or quickly preempted by L2 – which will focus developer attention and thus breed new protocols within the ETH ecosystem.

The push for tokenized projects and increased global regulatory clarity may also benefit ETH (among public blockchains) first. In our view, financial products are often more focused on technical risk mitigation than optimization and feature richness, and ETH has the advantage of being the longest-running smart contract platform. We believe that higher transaction fees (dollars instead of cents) and longer confirmation times (seconds instead of milliseconds) are secondary issues for many large tokenized projects.

Additionally, for more traditional companies looking to expand their business on-chain, recruiting enough developer talent becomes a key factor. Here, Solidity becomes the obvious choice as it constitutes the largest subset of smart contract developers, which also echoes the previous point about the popularity of EVM. Blackrocks BUIDL fund on ETH and JPMs proposed ERC-20 compatible Onyx Digital Assets Fungible Asset Contract (ODA-FACT) token standard are early signs of the importance of this talent pool.

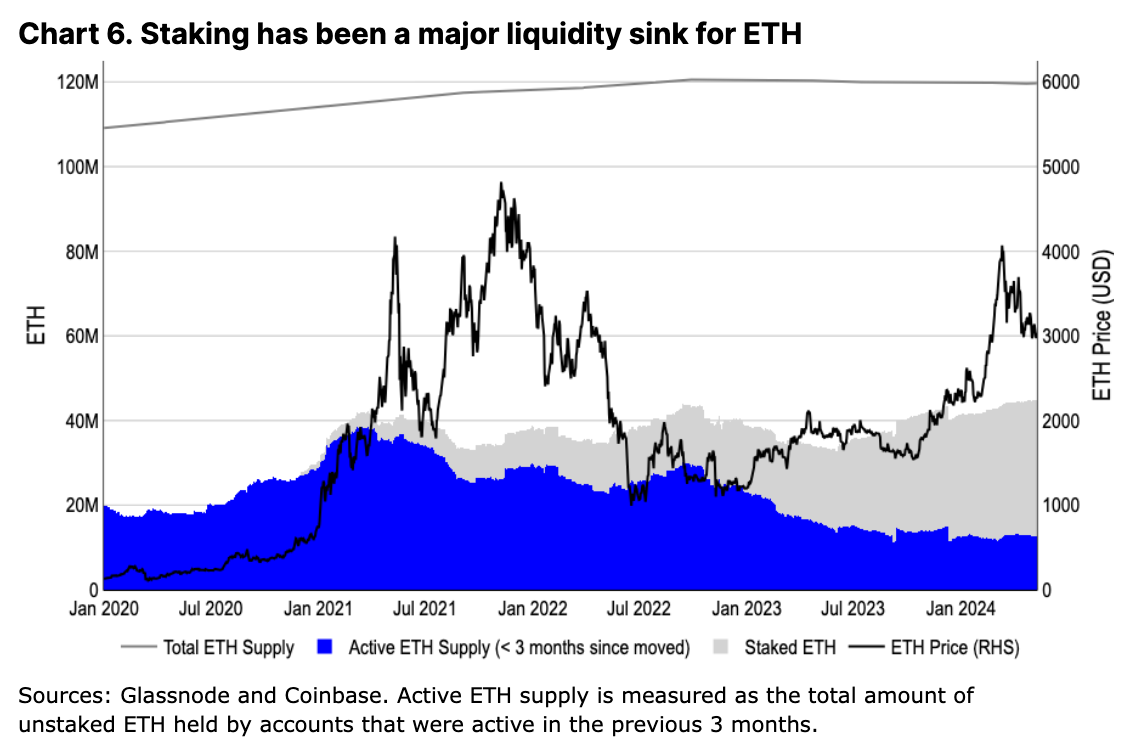

The evolution of active ETH supply differs significantly from BTC. Despite price increases since Q4 2023, ETH’s three-month circulating supply has not increased significantly. In contrast, we observe a nearly 75% increase in active BTC supply over the same timeframe. Unlike seen in the 2021/22 cycle when ETH was still running using Proof-of-Work (PoW), long-term ETH holders are not causing an increase in circulating supply, but rather a growing ETH supply is being staked. This reaffirms our view that staking is a key liquidity convergence point for ETH, minimizing structural sell-side pressure on the asset.

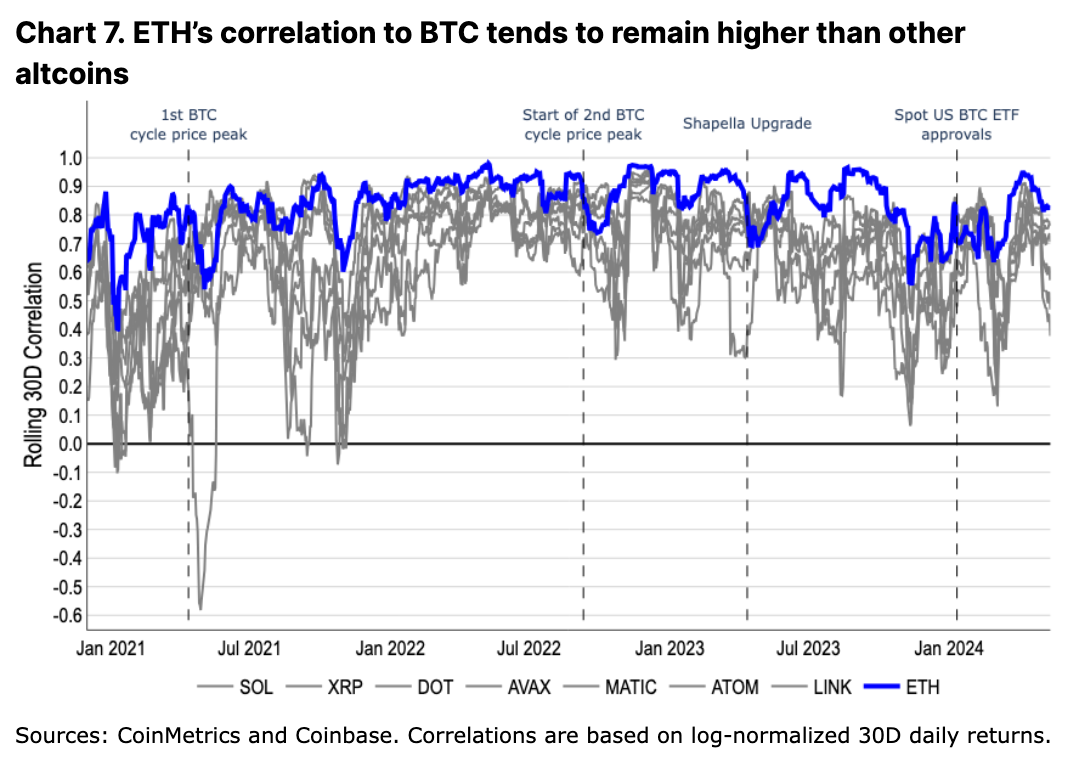

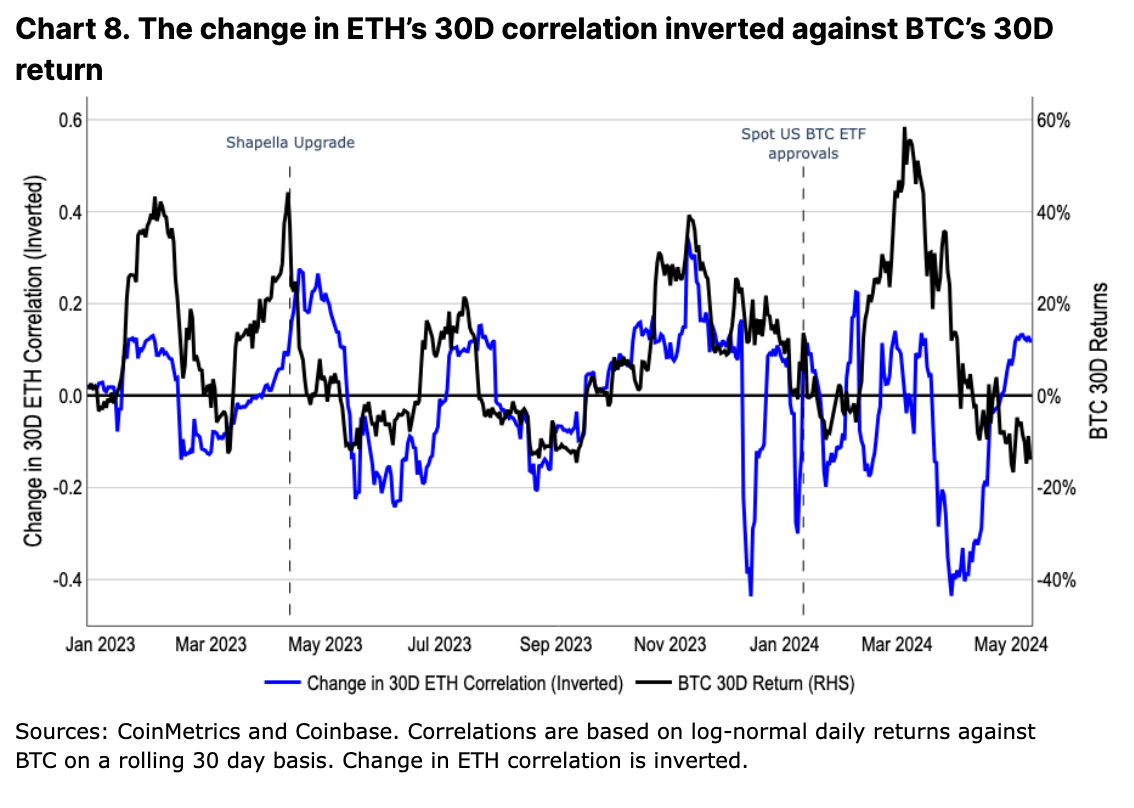

Historically, ETH has traded more in line with BTC than any other altcoin. At the same time, it has also decoupled from BTC during bull market peaks or specific ecosystem events – a similar pattern observed in other altcoins, albeit to a lesser extent. We believe that this trading behavior reflects the markets relative valuation of ETH as a store of value token and a technical utility token.

In 2023, ETHs correlation with BTC is inversely related to changes in BTCs price. That is, as BTCs value increases, ETHs correlation with it decreases, and vice versa. In fact, changes in BTCs price appear to be a leading indicator of changes in ETHs correlation. We believe this is a reflection of market enthusiasm led by BTCs price in altcoins, which in turn drives their speculative performance in bull markets (i.e. altcoins trade differently in bull markets than they do in bear markets relative to BTC).

However, this trend has weakened following the approval of the US spot BTC ETF. We believe this highlights the structural impact of ETF-based inflows, where an entirely new capital base has only exposure to BTC. New markets, such as registered investment advisors (RIAs), wealth management advisors, and securities firms, may view BTC differently in a portfolio than many crypto-native or retail traders. While BTC is the least volatile asset in a pure crypto portfolio, it is often viewed as a small diversifier in more traditional fixed income and equity portfolios. We believe this shift in BTC’s utility has impacted its trading patterns relative to ETH, and that ETH could see a similar shift (and a recalibration of trading patterns) if a US spot ETH ETF is approved.

We believe that ETH may still have upside potential in the coming months. ETH does not appear to have significant supply-side pressures such as token unlocking or miner selling pressure. Instead, staking and L2 growth have proven to be meaningful and growing convergence points for ETH liquidity. We believe that ETHs position as the center of DeFi is unlikely to be replaced due to the widespread adoption of EVM and its L2 innovations.

Additionally, the importance of a potential US spot ETH ETF cannot be ignored. We believe the market may be underestimating the timing and likelihood of a potential approval, which provides upside. In the meantime, we believe ETH’s structural demand drivers and technological innovation within its ecosystem will allow it to continue to juggle multiple narratives.

This article is sourced from the internet: Coinbase Monthly Outlook: ETH still has potential to rise in the coming months

関連: 2024年4月にビットコイン(BTC)を上回ると予測される強気のアルトコイン3つ

要約 4月のアルトコインはビットコインを上回る可能性を示しており、ALGOは「ゴールデンクロス」形成を示し、新たな強気相場を示唆しています。GTは勢いを増し、過去1か月で98.10%増加し、CAKEは2022年5月以来の最高値を目指しています。ALGO、GT、CAKEはEMAシグナルに支えられた強気トレンドを示しており、4月にさらなる成長の可能性を示しています。4月のアルトコインは、ビットコイン(BTC)を大幅に上回ると予測される潜在的な市場の激変の舞台を整えています。これらの中で、ALGOは4時間の価格チャートで最近「ゴールデンクロス」を形成しており、新たな強気相場の始まりを告げる指標となる可能性があります。さらに、GTは過去1か月で98.10%という印象的な成長を見せ、注目を集めています。その価格軌道は、この上昇傾向が4月に強まる可能性があることを示唆しています。一方、…