0

बिटमेक्स रिसर्च: माइक्रोस्ट्रैटजी की बॉन्ड संरचना का खुलासा, इसे कब परिसमाप्त किया जाएगा?

मूल लेखक: बिटमेक्स

Abstract: This article will focus on the structure of MicroStrategy bonds and analyze whether MicroStrategy may be forced to sell Bitcoin to repay bondholders if bondholders demand cash redemption. Based on the current debt structure, we believe that the possibility of forced liquidation is extremely low. However, given the sharp fluctuations in Bitcoin prices, anything is possible.

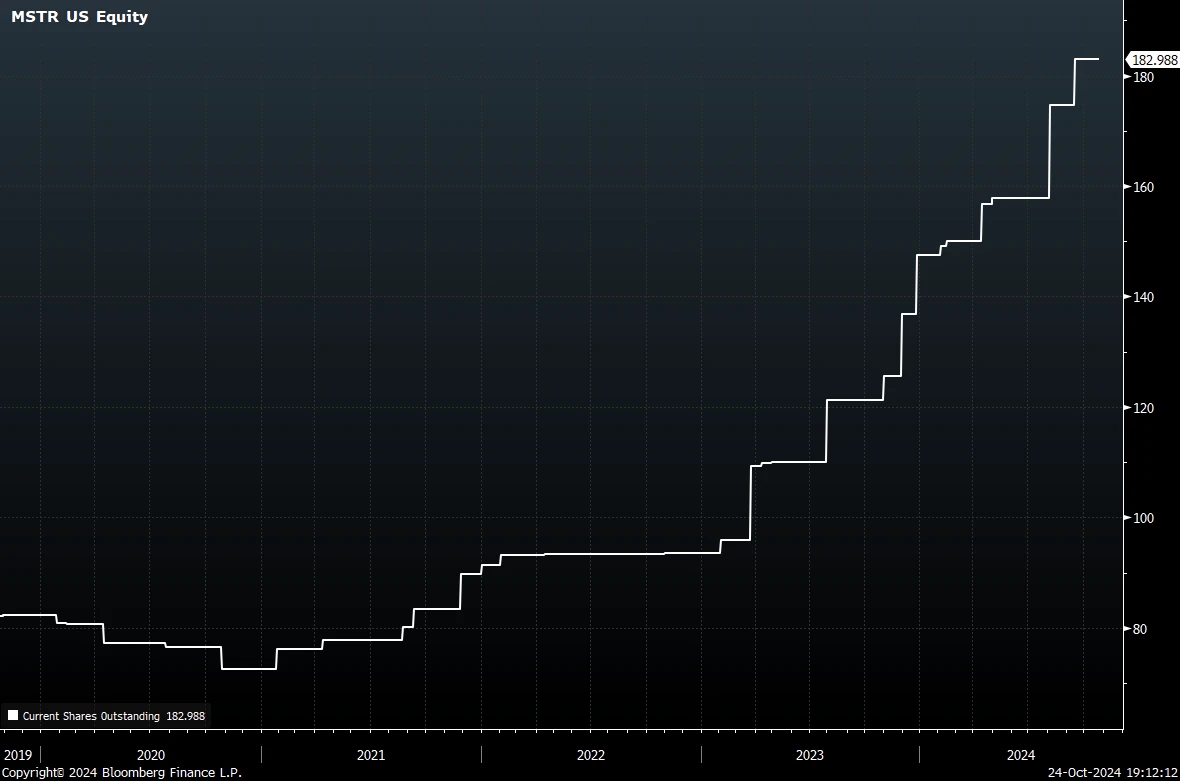

MicroStrategy holds more than 250,000 Bitcoins, and its stock price is at a significant premium to its net asset value (NAV). This is reminiscent of the similar high premium that Grayscale Bitcoin Trust (GBTC) experienced in the last cycle before it was converted to an ETF, which attracted a large influx of funds. However, we are puzzled and cannot give a reasonable explanation for why these two investment vehicles can trade at such a high premium. What is even more confusing is that MicroStrategy can even issue a large number of shares at a premium valuation to purchase more bitcoins, thereby pushing up the book value per share. This seemingly unlimited funds cycle operation is puzzling. Since launching its Bitcoin strategy, MicroStrategy has announced five equity issuances, raising a total of $4.4 billion.

MSTR shares outstanding (millions)

History seems to be repeating itself. MicroStrategy boss Michael Saylor is considered by many to be a “bad guy” in the Bitcoin space for some of his controversial positions. These include: his apparent hostility to supporting Bitcoin developers, his opposition to privacy technology, and his brief but outspoken opposition to self-custody. Similarly, Mr. Barry Silbert, who controls Grayscale, has been controversial for being the main organizer of the 2017 “New York Agreement”, which proposed a doomed proposal that the industry abandon Bitcoin in favor of an alternative coin “SegWit 2x” based on the flawed and vulnerable BTC 1 client.

As MicroStrategy has accumulated a large amount of Bitcoin, with a market value approaching $50 billion, concerns have begun to arise. In particular, some have asked whether MicroStrategys debt will force it to sell Bitcoin to the market, triggering a downward price spiral? Unfortunately, due to the complexity of the debt structure, there is no simple yes or no answer to this question. Nevertheless, we have reviewed the relevant documents and will do our best to answer this question in this article.

अस्वीकरण

We would like to add a disclaimer to this article by stating that we are not bond traders, bond market experts or lawyers. The corporate debt market can be complex and difficult for non-professionals to navigate. This article is likely to contain many errors. In addition, this article oversimplifies the product and does not comment on many conditions and complexities. Please do not rely on any information in this article and feel free to point out any errors.

MicroStrategy Bonds

As far as we know, MicroStrategy has issued seven publicly traded convertible bonds since announcing its Bitcoin strategy, as shown below.

The first thing to note is that two of the bonds have been redeemed in full and therefore have no relevance to outstanding debt. Therefore, MicroStrategy has five outstanding bonds with a principal value of $4.25 billion. Therefore, we will review these five bonds.

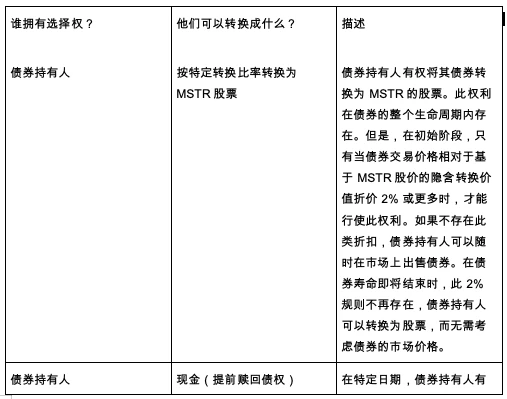

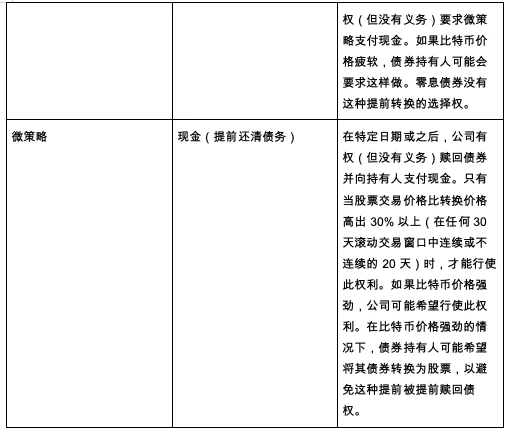

Redemption and conversion options

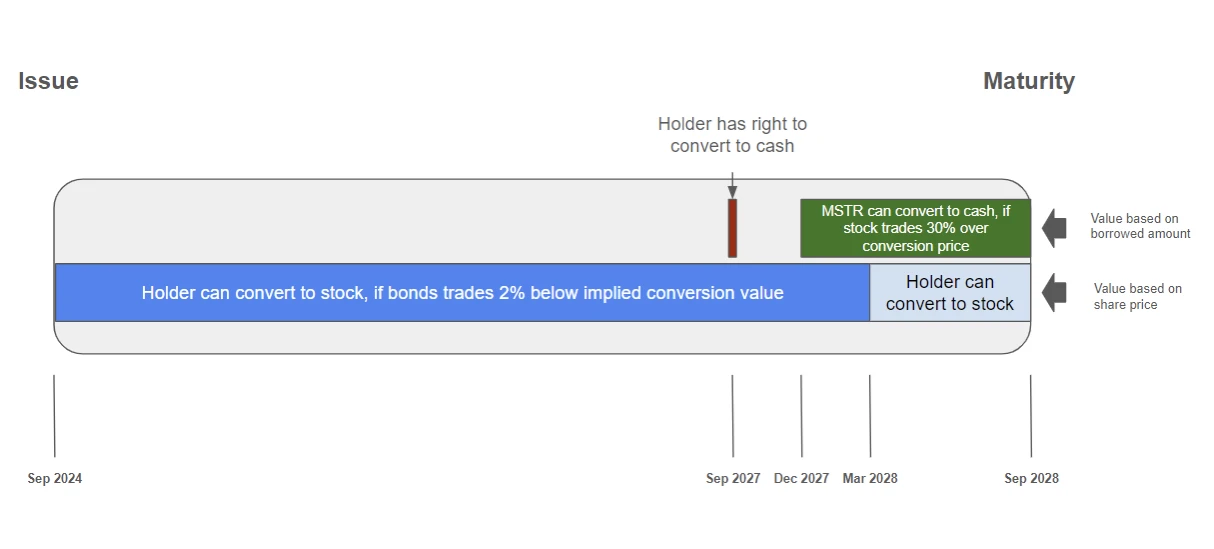

The structure of the bonds is relatively complex and, as far as we can tell, there are four different types of conversion options before maturity. The chart below summarizes these conversion options for the latest instrument (the bonds due in 2028).

MicroStrategy 0.625% 2028 Bond Schedule:

Sorting out convertible bond options:

As far as we know, except for the zero-coupon bond issued by MicroStrategy in September 2021, the remaining four convertible bonds have basically the same mechanism, only the price and date are different. The holders of the zero-coupon bonds do not have the right to redeem the cash before the maturity date unless there is a fundamental change in the business. This may be crucial if the price of Bitcoin falls.

The following table sets out the key dates relevant to the cash conversion options for the five bonds:

Source: Bond issuance documents

Note: *The stock must trade at least 30% above the conversion price within 20 consecutive or non-consecutive days in any 30-day rolling trading window

MicroStrategy’s Conversion Rights

It is important to note that for the zero coupon bond, MicroStrategy has already passed the cash option date in February 2024. The conversion price is $143.25, and a 30% premium to that is $186.23. MSTR stock is currently trading at $214, well above this price. However, it has only been above this price 11 of the past 30 trading days. Therefore, the option is about to become effective, but is not exercisable yet. Exercising this option would create value for MSTR shareholders, however, the bondholders will likely be able to prevent this from happening by exercising their conversion rights.

These complexities make bond valuation quite difficult because convertible bonds have multiple potential outcomes. However, many creditors are likely to be experienced professional bond investors who have models to perform these calculations.

Bond interest payments

Four of the five outstanding bonds carry interest payments. These coupons are cash liabilities, and MicroStrategy could theoretically be forced to sell Bitcoin to meet its payment obligations. However, given relatively low interest rates and the fact that its traditional software business generates ample free cash flow to cover interest costs, even a sharp drop in Bitcoin prices would not be enough to force the company to sell Bitcoin to pay the bond interest. In summary, we do not believe that interest costs will cause MicroStrategy to be forced to sell Bitcoin.

निष्कर्ष के तौर पर

MicroStrategy has $4.25 billion in debt, calculated based on its borrowed principal. Meanwhile, the company’s stock is currently valued at $43 billion, and its Bitcoin holdings are worth $17 billion. This shows that bonds do not account for a large proportion of MicroStrategy’s capital structure.

However, if the price of Bitcoin falls sharply, for example to around $15,000 per coin, and MicroStrategy is unable to raise further debt, analysts may need to consider the forced liquidation of Bitcoin. However, the timing of this potential forced liquidation will be concentrated on the expiration dates and option exercise dates mentioned in this article, which are scattered between 2027 and 2031, and the timing is very clear. Therefore, even if Bitcoin does fall to around $15,000, we believe that the probability of MicroStrategy being forced to sell Bitcoin to repay bonds is still low.

Although it is unlikely that MicroStrategy will be forced to sell Bitcoin, we think it is more likely that MicroStrategy will actively sell Bitcoin for the sake of maximizing shareholder interests. Currently, MicroStrategys stock price is at a huge premium to its net asset value. Once this premium disappears or even becomes a discount (which is almost inevitable), and the bonds are about to mature, selling Bitcoin to raise funds to repay the debt will become the best option in the interests of shareholders. However, as long as the stock price remains at a premium, MicroStrategy can use this to continue to do this kind of revolving loan operation, and there is no reason to sell Bitcoin. Of course, this huge premium state cannot last forever.

It is also important to note that if MicroStrategys stock price can continue to maintain a premium and the market demand for MSTR bonds remains strong, the company may issue more debt. This will cause its debt risk to rise and increase the possibility of forced selling when the price of Bitcoin plummets. But for now, MicroStrategys leverage ratio is low and the risk of liquidation is also at a low level.

This article is sourced from the internet: BitMEX Research: Uncovering the bond structure of MicroStrategy, when will it be liquidated?

संबंधित: OKX स्टार: उद्योग क्रिप्टो-फाइनेंस चरण में प्रवेश करने वाला है

10 अक्टूबर, 2024 को, OKX ने दुबई म्यूजियम ऑफ द फ्यूचर में आयोजित थीम इवेंट दुबईज न्यू चॉइस: OKX और ब्लॉकचेन इनोवेशन का भविष्य में आधिकारिक तौर पर घोषणा की कि यह यूएई में पूर्ण ऑपरेटिंग लाइसेंस प्राप्त करने वाला दुनिया का पहला क्रिप्टोकरेंसी ट्रेडिंग प्लेटफॉर्म बन गया है। यह मील का पत्थर न केवल वैश्विक अनुपालन प्रक्रिया में OKX की अग्रणी स्थिति को चिह्नित करता है, बल्कि क्रिप्टो उद्योग के अनुपालन विकास के लिए एक नया मानदंड भी स्थापित करता है, जो उद्योग के इतिहास में एक यादगार पृष्ठ बन गया है। इस उपलब्धि ने निस्संदेह वैश्विक क्रिप्टो बाजार के अनुपालन संचालन में नई जीवन शक्ति का संचार किया है, और भविष्य के क्रिप्टोकरेंसी उद्योग के अनुपालन पथ के लिए मूल्यवान अनुभव और प्रेरणा भी प्रदान की है। OKX के सीईओ स्टार ने OKX दुबई लॉन्च का जश्न मनाते हुए एक मुख्य भाषण दिया…

© 版权声明

Array

相关文章

0%

0%

0%

0%

0%

(0)

Bee.com दुनिया का सबसे बड़ा Web3 पोर्टल

बी नेटवर्क ऐप डाउनलोड करें और वेब3 यात्रा शुरू करें

© 2021—2025. All Rights Reserved.

गोपनीयता नीति

|

सेवाओं की शर्तें

© 2021—2025. All Rights Reserved.

गोपनीयता नीति |

सेवाओं की शर्तें