My XP

0

Login

मूल शीर्षक: क्या सोलाना की मुद्रास्फीति बहुत अधिक है?

मूल लेखक: लॉस्टिन

मूल अनुवाद: झोउझोउ, ब्लॉकबीट्स

संपादक का नोट: सोलाना के मुद्रास्फीति मुद्दे ने हाल के वर्षों में व्यापक चर्चा को जन्म दिया है। वर्तमान में, सोलाना नेटवर्क की मुद्रास्फीति दर लगभग 5.07% है, और नेटवर्क स्टेकिंग दर 65% तक पहुँच गई है। मुद्रास्फीति मॉडल में, उपयोगकर्ता नोड्स को मान्य करके पुरस्कार प्राप्त करते हैं, और टोकन का प्रचलन समय के साथ धीरे-धीरे कम होता जाता है। हालाँकि सोलाना की स्टेकिंग रिटर्न दर आकर्षक है, फिर भी टोकन की कीमतों पर इसकी मुद्रास्फीति के दीर्घकालिक प्रभाव के बारे में अनिश्चितता है। मुद्रास्फीति योजना में भविष्य के समायोजन जारी करने को कम करके या मुद्रास्फीति तंत्र को बदलकर नेटवर्क की स्थिरता और आर्थिक मॉडल को और प्रभावित कर सकते हैं।

मूल अनुवाद निम्नलिखित है:

इस लेख के पुराने संस्करणों की समीक्षा के लिए 0x के इचिगो और लेन | स्टेकविज़ के माइकल को तथा कुछ डेटा उपलब्ध कराने के लिए शिनोबी सिस्टम्स के ज़ांतेत्सु को हार्दिक धन्यवाद।

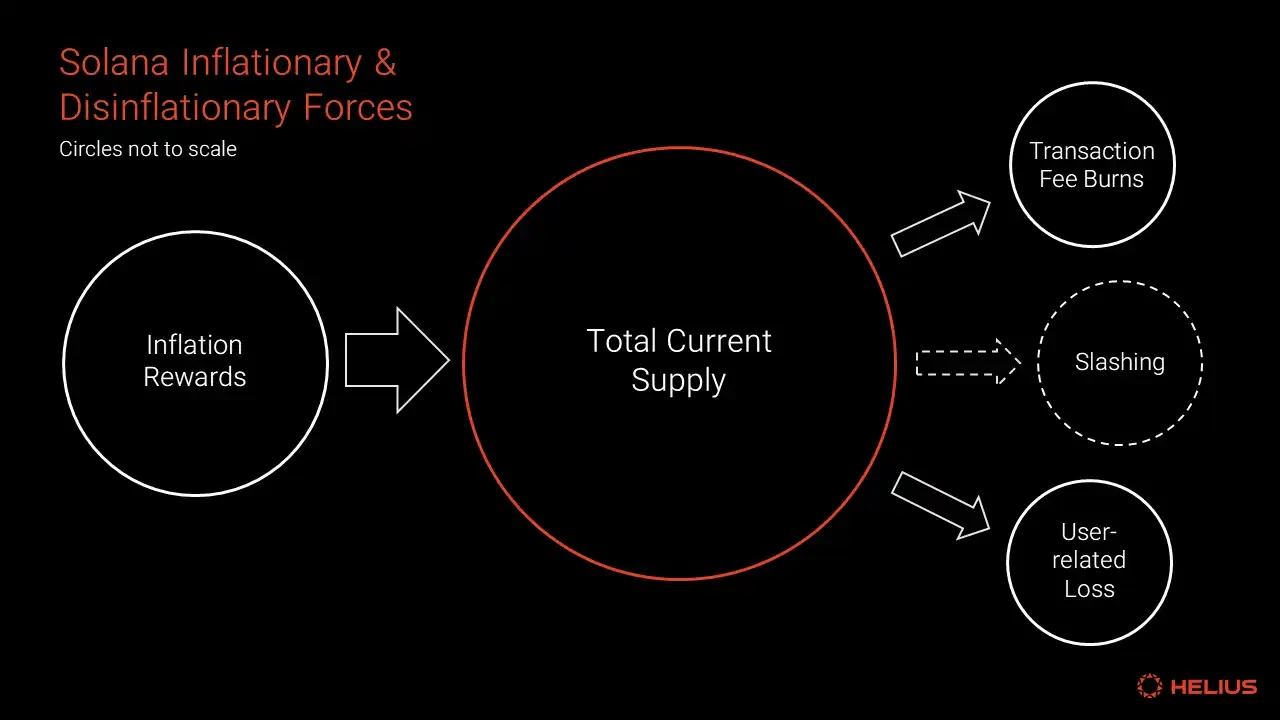

सभी SOL टोकन दो जगहों से आते हैं: उत्पत्ति ब्लॉक या प्रोटोकॉल मुद्रास्फीति (जिसे स्टेकिंग रिवॉर्ड भी कहा जाता है)। इसके विपरीत, लेनदेन शुल्क विनाश एकमात्र प्रोटोकॉल तंत्र है जो SOL टोकन को प्रचलन से हटा सकता है।

टोकन जारी करने को मुद्रास्फीति अनुसूची के तीन प्रमुख मापदंडों द्वारा वर्णित किया जाता है: प्रारंभिक मुद्रास्फीति दर (8%), अपस्फीति दर (-15%), और दीर्घकालिक मुद्रास्फीति दर (1.5%)। सोलाना मेननेट पर मुद्रास्फीति आधिकारिक तौर पर 10 फरवरी, 2021 को युग 150 पर शुरू हुई। वर्तमान मुद्रास्फीति दर 5.07% है।

प्रूफ ऑफ स्टेक मुद्रास्फीति के कारण गैर-स्टेकर्स को स्टेकर्स की तुलना में नेटवर्क का एक छोटा हिस्सा खोना पड़ता है, और यह कमजोर प्रभाव प्रभावी रूप से गैर-स्टेकर्स से स्टेकर्स को धन हस्तांतरित करता है।

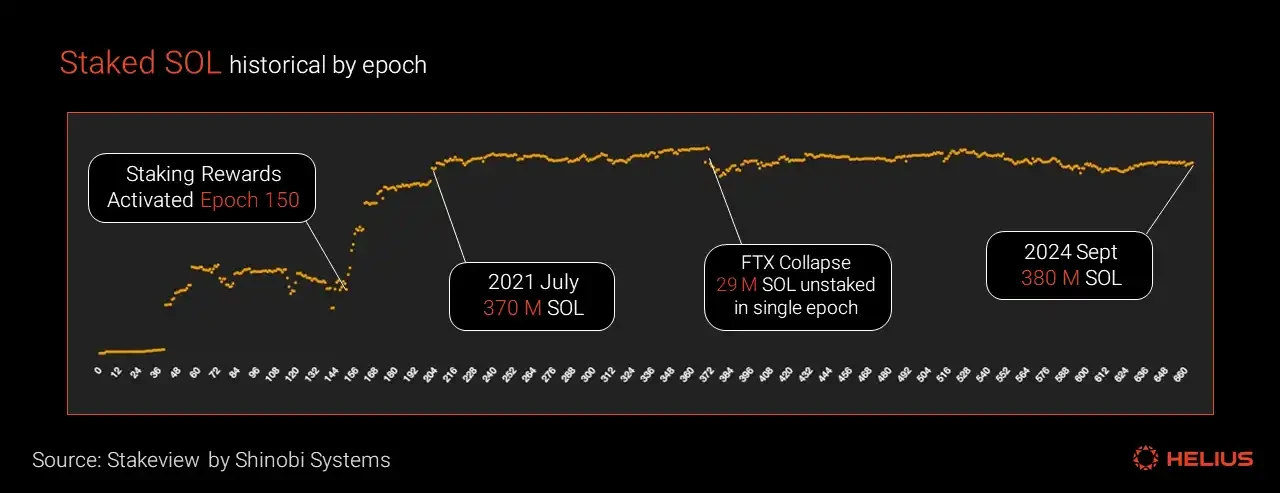

सोलाना की स्टेकिंग दर 65% है, जो उद्योग में अन्य नेटवर्क की तुलना में अपेक्षाकृत अधिक है। कुल स्टेक की गई राशि वर्तमान में 380 मिलियन SOL है, जो जुलाई 2021 में 202वें युग के बाद से अपेक्षाकृत स्थिर बनी हुई है। अधिकांश युगों में, सात अंकों वाले SOL स्टेक किए गए और अनस्टेक किए गए होते हैं।

स्टेकिंग यील्ड की गणना करते समय मुख्य चर मुद्रास्फीति दर और स्टेक किए गए SOL का प्रतिशत हैं। नाममात्र स्टेकिंग यील्ड (NSY) की गणना निम्न सूत्र द्वारा की जा सकती है: NSY = मुद्रास्फीति दर * सत्यापनकर्ता अपटाइम * (1 - सत्यापनकर्ता कमीशन) * (1 / SOL स्टेक किया गया प्रतिशत)।

14 दिसंबर, 2023 को, स्टेकिंग रिवॉर्ड के प्रतिशत के रूप में कुल बर्न फीस पहली बार 1% से अधिक हो गई, और मार्च में 7.8% पर पहुंच गई। पिछले 100 युगों में, फीस बर्न औसतन कुल स्टेकिंग रिवॉर्ड का 3.2% रहा है। SIMD-96 के कार्यान्वयन के बाद, टोकन बर्न करने से होने वाला अपस्फीति दबाव नगण्य हो जाएगा।

दुनिया भर के कई न्यायक्षेत्रों में, अतिरिक्त टोकन के रूप में मुद्रास्फीति पुरस्कार प्राप्त करना एक कर योग्य घटना माना जाता है, जिससे कर दायित्वों के कारण बिक्री दबाव बढ़ सकता है। इस प्रभाव को मापना मुश्किल है।

प्रूफ-ऑफ-स्टेक (PoS) मुद्रास्फीति से दीर्घकालिक और निरंतर मूल्य दबाव बढ़ता है, बाजार मूल्य संकेत विकृत होते हैं और उचित मूल्य तुलना में बाधा उत्पन्न होती है।

दीर्घ-पूंछ वाले स्वतंत्र सत्यापनकर्ता और पारिस्थितिकी तंत्र टीम सत्यापनकर्ता, अन्य सत्यापनकर्ता समूहों (एक्सचेंजों और संस्थागत सत्यापनकर्ताओं सहित) की तुलना में कम स्टेकिंग पुरस्कार कमीशन दर प्रदर्शित करते हैं और मुद्रास्फीति कमीशन पर कम निर्भर करते हैं।

दिसंबर 2023 से, MEV कमीशन और ब्लॉक रिवॉर्ड सहित सत्यापनकर्ताओं के लिए आय के वैकल्पिक स्रोतों में उल्लेखनीय वृद्धि हुई है। यह वृद्धि भविष्य में एक स्थायी सत्यापनकर्ता समूह के लिए परिचालन व्यय के लिए मुद्रास्फीति आयोगों पर कम निर्भर होने का संभावित मार्ग प्रदान करती है। हालाँकि, यह देखा जाना बाकी है कि क्या आय के ये वैकल्पिक स्रोत लंबी अवधि में ऊंचे बने रह सकते हैं।

यह रिपोर्ट डेटा और तथ्यों के आधार पर एक व्यापक विश्लेषण प्रदान करती है, जिसका उद्देश्य सोलानास मुद्रास्फीति योजना के बारे में संदेह (FUD) और गलत सूचना को दूर करना है। विश्लेषण को तीन भागों में विभाजित किया गया है: अतीत, वर्तमान और भविष्य।

अतीत: मुद्रास्फीति से पहले सोलाना के टोकन अर्थशास्त्र की समीक्षा, टोकन बिक्री, अनलॉक और प्रारंभिक टोकन बर्न सहित प्रमुख घटनाओं का विवरण।

अब: वर्तमान मुद्रास्फीति अनुसूची और अवस्फीति कारकों का मात्रात्मक मूल्यांकन करें, जिसमें लेनदेन शुल्क बर्निंग, जुर्माना स्लैशिंग, उपयोगकर्ता-संबंधित नुकसान और किराया शामिल हैं। आगामी SIMD-96 प्रोटोकॉल अपडेट के संभावित प्रभाव पर भी चर्चा करें।

भविष्य: सोलाना की वर्तमान प्रूफ-ऑफ-स्टेक (PoS) मुद्रास्फीति दर के पक्ष और विपक्ष में तर्कों का अन्वेषण करता है तथा मौजूदा मुद्रास्फीति अनुसूची में संभावित समायोजन पर विचार करता है।

सबसे पहले, हम औपचारिक रूप से कई महत्वपूर्ण शब्दों को परिभाषित करेंगे जिनका उपयोग इस रिपोर्ट में किया जाएगा। जो पाठक पहले से ही सोलाना-विशिष्ट परिभाषाओं से परिचित हैं, वे इस अनुभाग को छोड़ सकते हैं।

कुल वर्तमान आपूर्ति: लॉक और अनलॉक टोकन सहित अस्तित्व में मौजूद SOL टोकन की कुल संख्या। अधिक तकनीकी रूप से, कुल वर्तमान आपूर्ति उत्पन्न टोकन की कुल संख्या में से नष्ट किए गए टोकन की कुल संख्या को घटाने के बराबर है। लेखन के समय, वर्तमान कुल आपूर्ति 583 मिलियन है।

परिसंचारी आपूर्ति: एक्सचेंजों, ऑन-चेन प्रोटोकॉल और उपयोगकर्ता वॉलेट में परिसंचारी SOL टोकन की कुल मात्रा, जिसमें स्टेक्ड और अनस्टेक्ड दोनों SOL शामिल हैं। परिसंचारी आपूर्ति 466 मिलियन है। अधिक औपचारिक रूप से:

परिसंचारी आपूर्ति = वर्तमान कुल आपूर्ति – गैर-परिसंचारी आपूर्ति

नॉन-सर्कुलेटिंग सप्लाई: नॉन-सर्कुलेटिंग सप्लाई में दो मुख्य रूप होते हैं: स्टेकिंग खातों में लॉक किए गए SOL टोकन, और सोलाना लैब्स या सोलाना फाउंडेशन द्वारा रखे गए अनलॉक किए गए स्टेकिंग खातों में SOL टोकन। स्टेकिंग खातों में SOL आमतौर पर सोलाना फाउंडेशन द्वारा दिए गए SOL निवेश या अनुदान के कारण होते हैं। प्रत्येक स्टेकिंग खाते में वेस्टिंग व्यवस्था के अनुसार एक अनलॉक तिथि निर्धारित होती है। दूसरा, एसओएल टोकन सीधे स्वामित्व में हैं सोलाना लैब्स या सोलाना फाउंडेशन, जो अनलॉक स्टेकिंग खातों में रखे जाते हैं। फाउंडेशन वर्तमान में इसका एक बड़ा हिस्सा उपयोग करता है (वर्तमान में 51 मिलियन एसओएल ) अपने प्रतिनिधिमंडल कार्यक्रम के लिए। इस लेख को लिखते समय, गैर-परिसंचारी आपूर्ति 117 मिलियन है।

लॉक किए गए टोकन: लॉक किए गए टोकन स्टेकिंग खातों में रखे गए वे टोकन होते हैं, जिनमें ऐसी शर्तें होती हैं कि उन्हें पूर्व निर्धारित तिथि से पहले वापस नहीं लिया जा सकता। ये लॉकिंग पैरामीटर एक विशिष्ट UNIX टाइमस्टैम्प या युग पर आधारित होते हैं, और खाता बनाते समय नामित संरक्षक द्वारा निर्धारित किए जाते हैं। लॉक किए गए स्टेकिंग खातों को अनडेलीगेट किया जा सकता है, छोटे खातों में विभाजित किया जा सकता है, और अन्य सत्यापनकर्ताओं को फिर से सौंपा जा सकता है। हालाँकि, इन टोकन को तब तक वापस नहीं लिया जा सकता या दूसरे पतों पर स्थानांतरित नहीं किया जा सकता जब तक कि लॉक-अप अवधि समाप्त न हो जाए। जबकि कोई भी उपयोगकर्ता लॉक किए गए स्टेकिंग खाते बना सकता है, इस अभ्यास का उपयोग मुख्य रूप से सोलाना फाउंडेशन द्वारा टोकन और अनुदान वितरित करने के लिए किया जाता है, और ये आवंटन अक्सर विशिष्ट प्रदर्शन आवश्यकताओं या समय लॉक के साथ आते हैं।

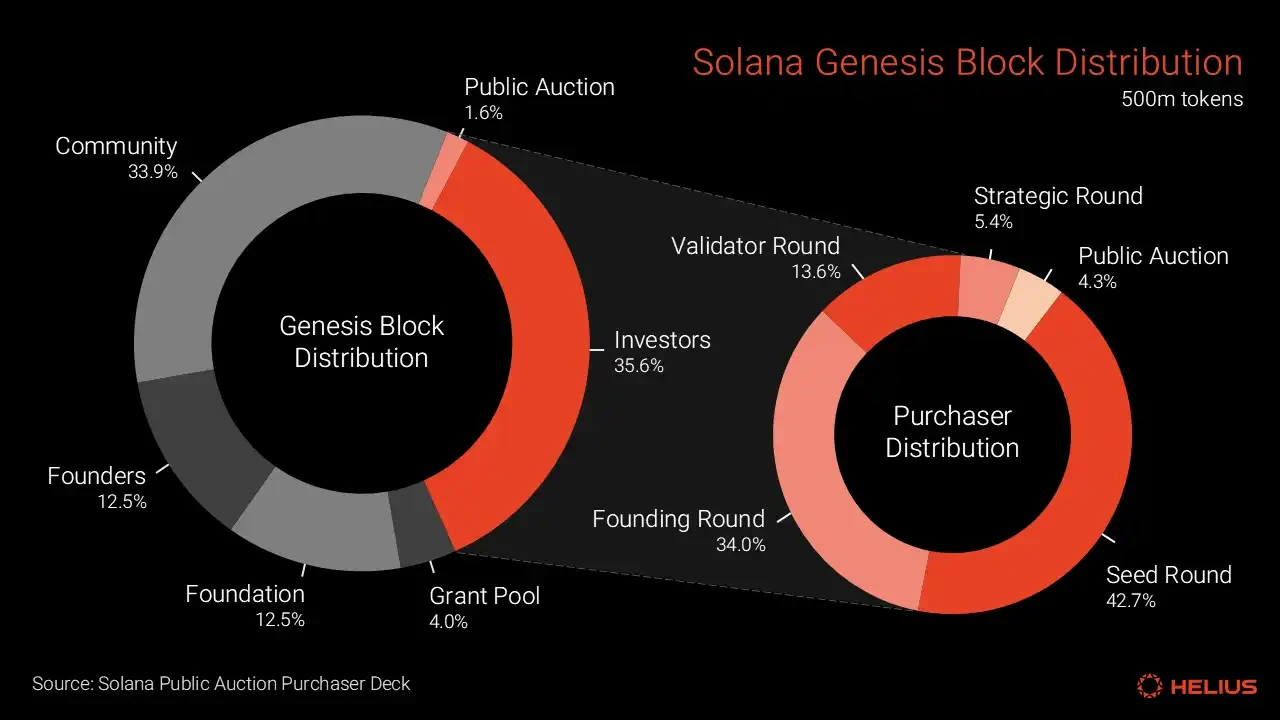

16 मार्च 2020 को 500 मिलियन SOL टोकन बनाए गए उत्पत्ति ब्लॉक सोलाना मेननेट बीटा क्लस्टर का। अपने संचालन के पहले वर्ष के दौरान, सोलाना के पास कोई मुद्रास्फीति संबंधी स्टेकिंग पुरस्कार नहीं था। 24 मार्च, 2020 को, 8 मिलियन SOL टोकन गैर-अमेरिकी खरीदारों को बेचे गए कॉइनलिस्ट पर एक डच नीलामी नीलामी से मात्र ₹ 1,000 जुटाए गए $1.76 मिलियन , जिसका अंतिम परिसमापन मूल्य $0.22 प्रति टोकन है। इस सार्वजनिक नीलामी से टोकन, प्लस कम संख्या बिनेंस पर एयरड्रॉप की एक श्रृंखला के माध्यम से वितरित टोकन, सोलाना की प्रारंभिक परिसंचारी आपूर्ति बनाते हैं।

सोलाना जेनेसिस ब्लॉक डिस्ट्रीब्यूशन, मूल से निकाला गया सार्वजनिक नीलामी क्रेता

इस अवधि के दौरान, सोलाना को उद्योग में अपने कई साथियों की तुलना में पूंजी जुटाने में महत्वपूर्ण चुनौतियों का सामना करना पड़ा है। उदाहरण के लिए, एल्गोरैंड ने सफलतापूर्वक $60 मिलियन जुटाए गए छह महीने पहले इसी तरह की कॉइनलिस्ट नीलामी के माध्यम से, जबकि हेडेरा हैशग्राफ ने 1टीपी10टी100 मिलियन अठारह महीने पहले संस्थागत और उच्च निवल मूल्य वाले व्यक्तिगत निवेशकों से।

"हमने 2020 में लॉन्च करने से पहले और अधिक ब्रिज फंडिंग जुटाने की कोशिश की, लेकिन यह कारगर नहीं हुआ। हमें फंडिंग का उपयोग करने के लिए समय बढ़ाने के लिए टीम के एक तिहाई लोगों को नौकरी से निकालना पड़ा। हमने मार्च में जितनी जल्दी हो सके लॉन्च किया, और दबाव बहुत अधिक था... हमने नीलामी की घोषणा की, और दो दिन बाद, 16 मार्च, 2020 को, सभी बाजार ढह गए। दुनिया अराजकता में थी, और हमारे पास केवल छह या सात महीने की फंडिंग बची थी।"

नकदी की कमी के इस दौर ने कई महत्वपूर्ण प्रारंभिक निर्णय लिए।

"इसने मुझे एक विशिष्ट रणनीति अपनाने के लिए मजबूर किया, जो पीछे मुड़कर देखने पर सही साबित हुई... अगर हमारे पास हमारे प्रतिस्पर्धियों जितना पैसा होता, तो मैं शायद उनके नेतृत्व का अनुसरण करता और ईवीएम का समर्थन करता; हमें ईवीएम का समर्थन करना ही था... यह पता चला कि सबसे अच्छा निर्णय जो हम कर सकते थे, वह एक ऐसा रनटाइम बनाना था जो पूरी तरह से प्रदर्शन के लिए अनुकूलित था।"

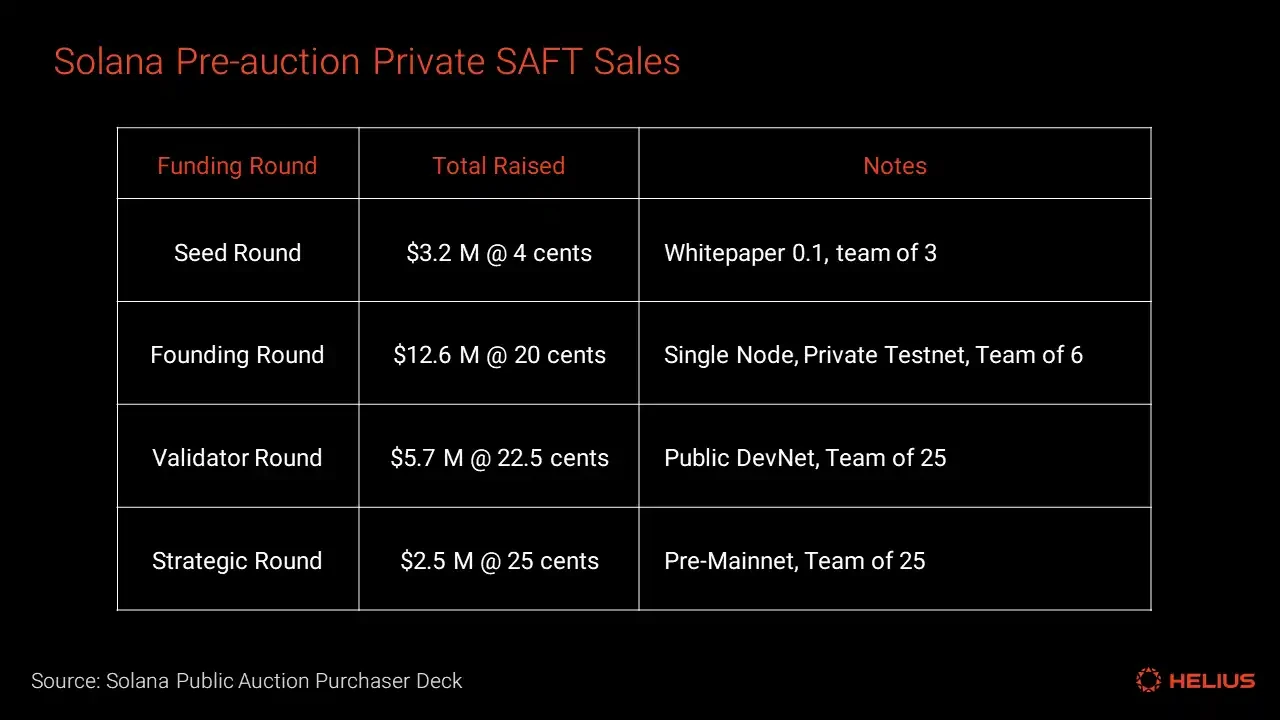

नीलामी से पहले निजी SAFT बिक्री ( स्रोत )

नीलामी के लगभग नौ महीने बाद, नीलामी से पहले निजी SAFT बिक्री (यानी, सीड, संस्थापक, रणनीतिक और सत्यापनकर्ता दौर) में भाग लेने वाले शुरुआती टोकन धारकों के सभी टोकन अनलॉक कर दिए गए। संस्थापक टीम के सदस्यों ने अपने 50% टोकन अनलॉक किए, और शेष 50% अगले 24 महीनों में धीरे-धीरे अनलॉक किए जाएंगे। गैर-संस्थापक कर्मचारी टोकन भी इस समय पूरी तरह से (100%) अनलॉक किए गए थे, लेकिन बिक्री पर अघोषित प्रतिबंध थे (स्रोत)।

सोलाना की अनलॉक योजना

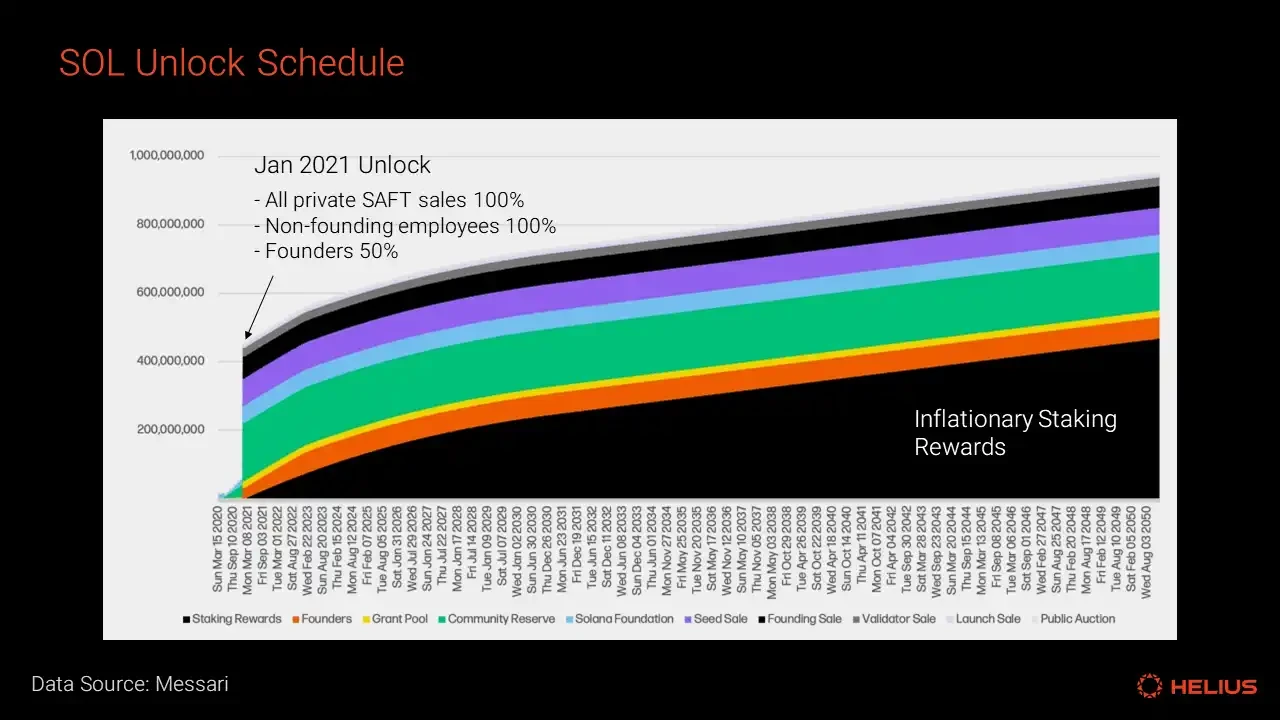

मई 2020 में, शुरुआती सामुदायिक प्रतिक्रिया के जवाब में चिंताएं मार्केट मेकर्स को टोकन उधार देने के बारे में सोलाना फाउंडेशन ने स्थायी रूप से हटा दिया 11.36 मिलियन एसओएल इससे कुल आपूर्ति घटकर 488.64 मिलियन रह गई।

सामुदायिक मतदान के अनुसार, सोलाना मेननेट बीटा की मुद्रास्फीति आधिकारिक तौर पर थी का शुभारंभ किया 10 फरवरी, 2021 को स्लॉट 64800004 (युग 150), 213,841 SOL के प्रथम भुगतान के साथ।

मुद्रास्फीति अनुसूची टोकन जारी करने की अनुसूची का एक नियतात्मक विवरण है जिसमें तीन प्रमुख पैरामीटर शामिल हैं:

प्रारंभिक मुद्रास्फीति दर (8%): वह प्रारंभिक मुद्रास्फीति दर जब मुद्रास्फीति पहली बार शुरू होती है

डी-मुद्रास्फीति दर (-15%): वह दर जिस पर प्रत्येक युग वर्ष में मुद्रास्फीति घटती है

दीर्घकालिक मुद्रास्फीति दर (1.5%): स्थिर दीर्घकालिक अपेक्षित मुद्रास्फीति दर

लेखन के समय, सोलाना की मुद्रास्फीति दर 5.07% है। आप इसे “सोलाना इन्फ्लेशन” कमांड का उपयोग करके देख सकते हैं या आरपीसी विधि सोलाना में “getInflationRate” CLI टूल सूट .

सोलाना की मुद्रास्फीति योजना (स्रोत)

एक युग वर्ष में 182.5 युग होते हैं, जो कि एक वर्ष में युगों की वह संख्या है, यदि प्रत्येक युग ठीक दो दिन तक चले। एक युग में 182.5 युग होते हैं। 432,000 स्लॉट , और प्रत्येक स्लॉट में कम से कम 400 मिलीसेकंड लगने चाहिए। हालाँकि, चूँकि ब्लॉक का समय परिवर्तनशील होता है, इसलिए युग अक्सर इस दो-दिवसीय न्यूनतम से अधिक हो सकता है, जो कई घंटों तक बढ़ सकता है (उदाहरण के लिए, सबसे हाल का युग 661 2 दिन और 4 घंटे था)। शुरुआती वर्षों में, सोलाना के मेननेट क्लस्टर ने अक्सर धीमी तीन-दिवसीय अवधियों का अनुभव किया (उदाहरण के लिए, युग 322 3 दिन और 3 घंटे) था, जिसने मानक वर्षों में गणना करने पर मुद्रास्फीति अनुसूची की प्रगति को काफी हद तक बढ़ा दिया।

उदाहरण के लिए, जैसा कि मैं 30 अगस्त 2024 को यह लिख रहा हूँ, सोलाना वर्तमान में युग 663 पर है। 10 फरवरी 2021 को युग 150 पर मुद्रास्फीति शुरू होने के बाद से यह 513वां युग है, जो 2.81 युग वर्षों के बराबर है, लेकिन 3.55 मानक वर्षों तक फैला हुआ है।

निम्नलिखित चार्ट फरवरी 2021 में प्रारंभिक 488.6 मिलियन एसओएल (500 मिलियन माइनस 11.3 मिलियन बर्न्स) से शुरू होने वाली मुद्रास्फीति अनुसूची के आधार पर वर्तमान कुल आपूर्ति को दर्शाता है।

इन विशिष्ट मापदंडों को कैसे चुना गया, इस बारे में मूल सामुदायिक मंच चर्चा अब उपलब्ध नहीं है। हालाँकि, उस समय, सोलाना के सह-संस्थापक अनातोली याकोवेंको ने एक लेख में कुछ सुराग बताए थे। साक्षात्कार .

"मुझे नहीं लगता कि मुद्रास्फीति के पैरामीटर कॉसमॉस से बहुत अलग होंगे क्योंकि हमारे सत्यापनकर्ता सेट में उस नेटवर्क के साथ बहुत अधिक ओवरलैप है, और यह लगभग वही लोग हैं। इसके अलावा, कॉसमॉस का मुद्रास्फीति शेड्यूल अच्छी तरह से काम करता है, इसलिए हमें प्रयोग करने की ज़रूरत नहीं है। जब चीजें अन्य नेटवर्क के लिए काम करती हैं, तो हम निश्चित रूप से उन विचारों को उधार लेंगे।"

इसके अतिरिक्त, स्टेकिंग पुरस्कारों की एक प्रारंभिक संक्षिप्त रूपरेखा सोलाना GitHub रिपोजिटरी इसमें कैस्पर एफएफजी के प्रभाव का भी उल्लेख किया गया है।

प्रत्यायोजित हिस्सेदारी का प्रमाण (DPoS) सहमति तंत्र सोलाना में मूल रूप से एकीकृत है। उपयोगकर्ता वॉलेट, इकोसिस्टम dApps और विभिन्न तुलना प्लेटफ़ॉर्म के माध्यम से सीधे स्टेकिंग इंटरफ़ेस तक पहुँच सकते हैं। टोकन धारक आसानी से SOL दांव पर लगाएं अपनी पसंद के वैलिडेटर को टोकन सौंप सकते हैं और प्रत्येक युग के अंत में अनस्टेक कर सकते हैं। इसके अलावा, वे स्टेकिंग पूल को टोकन भी सौंप सकते हैं या खरीद सकते हैं लिक्विड स्टेकिंग टोकन , जो वास्तव में स्टेकिंग के बराबर है। सत्यापनकर्ता को टोकन सौंपना सत्यापनकर्ता पर भरोसा दर्शाता है, लेकिन सत्यापनकर्ता को टोकन पर स्वामित्व या नियंत्रण नहीं देता है।

स्टेकिंग रिवॉर्ड को सबसे पहले एपोच के भीतर अर्जित अंकों के आधार पर विभाजित किया जाता है। हर बार जब कोई वैलिडेटर किसी ब्लॉक के लिए वोट करता है, जिसकी बाद में पुष्टि की जाती है और जो अंतिम बन जाता है, तो वैलिडेटर को एक अंक प्राप्त होगा। कुल अंकों में से वैलिडेटर का हिस्सा (यानी, सभी वैलिडेटर अंकों के योग से विभाजित उनके अंक) उन्हें मिलने वाले पुरस्कारों का अनुपात निर्धारित करता है। यह अनुपात स्टेक की गई राशि से भी भारित होता है। यदि किसी वैलिडेटर के पास कुल हिस्सेदारी का 1% है और उनके अंक औसत हैं, तो वैलिडेटर को एक अंक मिलेगा। कुल मुद्रास्फीति पुरस्कारों का लगभग 1% प्राप्त करें यदि अंक औसत से ऊपर हैं, तो पुरस्कार उसी के अनुसार उतार-चढ़ाव करेंगे। वोटिंग अंक सहमति प्रक्रिया में एक व्यक्तिगत सत्यापनकर्ता की भागीदारी और शुद्धता का एक मात्रात्मक माप है। सत्यापनकर्ताओं का ऑफ़लाइन होना (यानी, निष्क्रिय) या चेन के साथ सिंक से बाहर होना उनके पुरस्कारों को महत्वपूर्ण रूप से प्रभावित करेगा।

मुद्रास्फीति पुरस्कारों की गणना की जाती है और युग के अंत में प्रतिनिधियों के दांव वाले खातों में वितरित किया जाता है। चूँकि वहाँ से अधिक हैं एक मिलियन वितरित करने के लिए स्टेक किए गए खातों में संसाधन की खपत बड़ी है, जो नेटवर्क को धीमा कर देगी और युग के अंत में लगातार आम सहमति का कारण बनेगी।

वैलिडेटर अपनी सेवाओं के लिए एक प्रतिशत कमीशन लेते हैं, जो डेलीगेटर्स के लिए मुद्रास्फीति पुरस्कार का हिस्सा है। यह कमीशन आमतौर पर एकल अंकों में होता है, लेकिन सैद्धांतिक रूप से 0% और 100% के बीच कहीं भी हो सकता है। वर्तमान में 200 से अधिक निजी सोलाना वैलिडेटर हैं, जिनके स्टेक किए गए फंड पूरी तरह से ऑपरेटिंग इकाई के स्वामित्व में और स्व-प्रत्यायोजित हो सकते हैं। इन पूरी तरह से स्व-स्टेकिंग SOL वैलिडेटर को उनकी 100% कमीशन दर से पहचाना जा सकता है।

निम्नलिखित सूत्र मुद्रास्फीति पुरस्कारों से अनुमानित स्टेकिंग प्रतिफल का वर्णन करता है:

नाममात्र स्टेकिंग आय = मुद्रास्फीति दर * सत्यापनकर्ता ऑनलाइन दर * (1 - सत्यापनकर्ता कमीशन) * (1 / एसओएल स्टेकिंग प्रतिशत)

एसओएल स्टेकिंग प्रतिशत को इस प्रकार परिभाषित किया गया है:

एसओएल स्टेकिंग प्रतिशत = कुल स्टेक्ड एसओएल / वर्तमान कुल आपूर्ति

स्टेकिंग रिटर्न प्रत्येक युग की मुद्रास्फीति दर, सत्यापनकर्ता प्रदर्शन और कुल सक्रिय हिस्सेदारी में चल रहे परिवर्तनों के साथ उतार-चढ़ाव करेगा।

सोलाना की स्टेकिंग कैसे काम करती है, इस बारे में अधिक जानकारी के लिए हमारा लेख देखें हेलियस स्टेकिंग ब्लॉग डाक।

अनातोली याकोवेंको ने लाइटस्पीड में बताया पॉडकास्ट : "सबसे बड़ी आलोचना यह है कि सोलाना की मुद्रास्फीति दर बहुत अधिक है, जो नेटवर्क के लिए एक लागत है। गणितीय दृष्टिकोण से, मुद्रास्फीति वास्तव में गैर-स्टेकिंग उपयोगकर्ताओं और स्टेकिंग उपयोगकर्ताओं के बीच मूल्य स्थानांतरित कर रही है। यह वास्तव में गैर-स्टेकिंग उपयोगकर्ताओं के लिए एक लागत है, लेकिन साथ ही यह स्टेकिंग उपयोगकर्ताओं के लिए एक लाभ है। बाजार इसके साथ किसी तरह का संतुलन बनाएगा।"

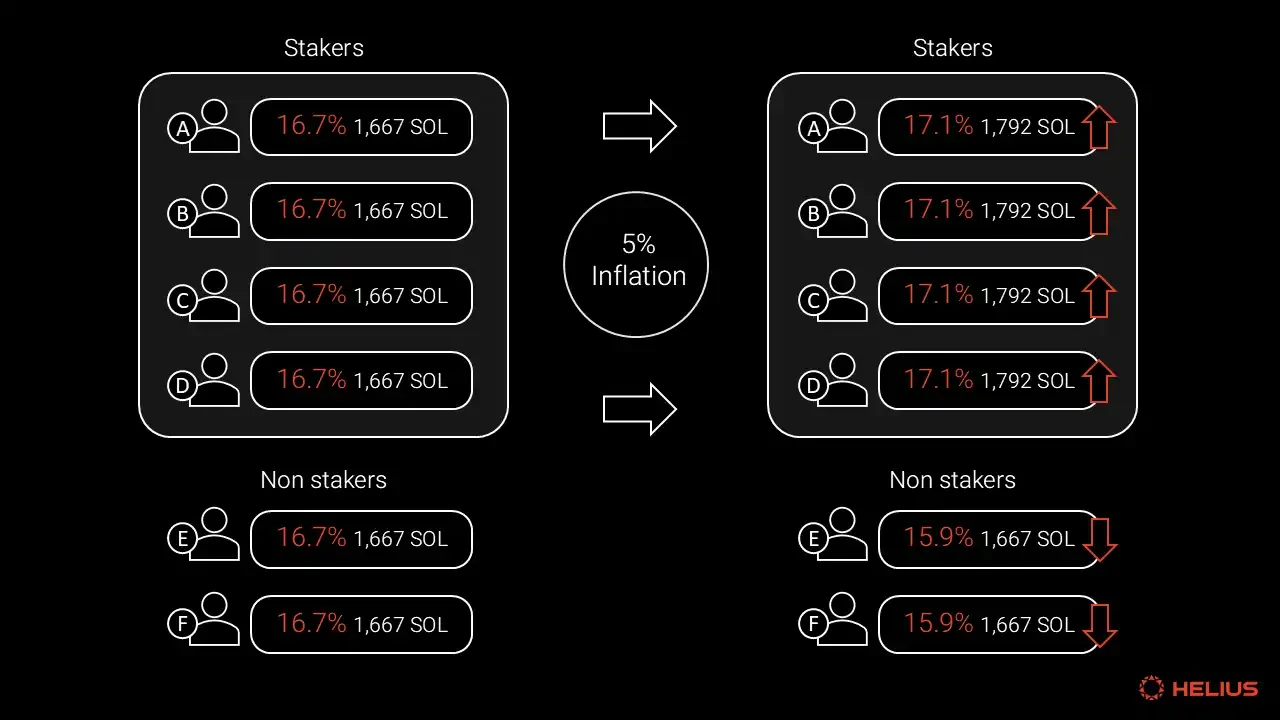

सामान्य तौर पर, प्रूफ ऑफ स्टेक (PoS) मुद्रास्फीति स्टेकर्स के सापेक्ष गैर-स्टेकर्स के नेटवर्क शेयर को कम करती है, और यह कमजोर पड़ना वास्तव में गैर-स्टेकर्स से स्टेकर्स को धन हस्तांतरित करता है। इस घटना को निम्नलिखित मापदंडों के साथ एक सरलीकृत मॉडल द्वारा प्रदर्शित किया जा सकता है:

कुल टोकन आपूर्ति: 10,000

बाजार मूल्य: $1 मिलियन

वार्षिक मुद्रास्फीति पुरस्कार: 5%

प्रारंभिक टोकन धारक: 6 उपयोगकर्ता, प्रत्येक के पास समान संख्या में टोकन होंगे

स्टेकिंग दर: 66% (4 स्टेकिंग उपयोगकर्ता, 2 गैर-स्टेकिंग उपयोगकर्ता)

यह मॉडल दर्शाता है कि जैसे-जैसे मुद्रास्फीति होती है, स्टेकिंग उपयोगकर्ताओं के टोकन की संख्या अपेक्षाकृत बढ़ जाती है, जबकि गैर-स्टेकिंग उपयोगकर्ताओं के शेयर कम हो जाते हैं, जिसके परिणामस्वरूप धन का पुनर्वितरण होता है।

शुरुआत में, प्रत्येक उपयोगकर्ता के पास 1,667 SOL टोकन होते हैं, जो नेटवर्क शेयर के 16.7% और $166,666 के मार्केट कैप का प्रतिनिधित्व करते हैं। एक वर्ष के भीतर, 500 नए टोकन मुद्रास्फीति पुरस्कार के रूप में स्टेकर्स को वितरित किए जाएंगे। एक वर्ष के बाद, चारों स्टेकर्स के पास 1,792 SOL टोकन होंगे, जो 125 टोकन (7.5%) की मामूली वृद्धि है, और उनका नेटवर्क शेयर 0.4% बढ़कर 17.1% हो गया है। इस बीच, दो गैर-स्टेकर्स के पास टोकन की समान संख्या है और उनका नेटवर्क शेयर 0.8% घटकर 15.9% हो गया है। यह मानते हुए कि नेटवर्क का कुल मार्केट कैप $1 मिलियन पर अपरिवर्तित रहता है, प्रत्येक SOL का मूल्य $100 से घटकर $95.23 हो जाएगा। हालांकि, प्रत्येक स्टेकर नेटवर्क शेयर का कुल मूल्य $3,968 (2.4% की वृद्धि) बढ़ जाएगा। इसी प्रकार, प्रत्येक गैर-स्टेकर टोकन का मूल्य $7,936 (4.8% की कमी) घट जाएगा।

यह मॉडल दिखाता है कि कैसे प्रूफ ऑफ स्टेक (PoS) स्टेकिंग न केवल कमजोर पड़ने से बचाता है, बल्कि वास्तव में समय के साथ धारकों के नेटवर्क स्वामित्व को मजबूत करता है। इसके अतिरिक्त, यह सरलीकृत परिदृश्य सोलाना के वर्तमान मुद्रास्फीति पुरस्कारों को सटीक रूप से दर्शाता है। सोलाना की वर्तमान मुद्रास्फीति दर 5.07% और कुल आपूर्ति 583 मिलियन SOL, जिसमें से 378 मिलियन SOL दांव पर लगे हैं (65% की स्टेकिंग दर), उपयोगकर्ता मुद्रास्फीति पुरस्कारों के माध्यम से समान वार्षिक मूल्य हस्तांतरण की उम्मीद कर सकते हैं। स्टेकर नेटवर्क स्वामित्व में लगभग 2.4% प्राप्त करते हैं, जबकि गैर-स्टेकर नेटवर्क स्वामित्व में लगभग 4.8% खो देते हैं। इस सरलीकृत मॉडल के आधार पर, स्टेकर को प्रति वर्ष नाममात्र 7.5% SOL स्टेकिंग रिटर्न प्राप्त करना चाहिए, जो मोटे तौर पर वर्तमान वास्तविक रिटर्न के अनुरूप है। बेशक, वास्तविक स्थिति इस मॉडल की तुलना में अधिक जटिल है, जिस पर हम बाद की चर्चा में विस्तार से चर्चा करेंगे।

यह ध्यान रखना महत्वपूर्ण है कि नेटवर्क स्वामित्व में प्रतिशत लाभ या हानि उपयोगकर्ता द्वारा रखे गए टोकन की पूर्ण संख्या की परवाह किए बिना समान है। दो प्रमुख चर मुद्रास्फीति दर और स्टेक किए गए SOL का प्रतिशत हैं।

उत्पत्ति ब्लॉक के बाद से युग द्वारा दांव पर लगा एसओएल ( स्रोत )

सोलाना की स्टेकिंग दर अन्य उद्योग नेटवर्क की तुलना में अपेक्षाकृत अधिक है, आंशिक रूप से इसकी स्टेकिंग प्रक्रिया की आसानी और उपयोगकर्ता-मित्रता के कारण। हालाँकि, जुलाई 2021 में युग 202 में 370 मिलियन SOL तक पहुँचने के बाद से, स्टेकिंग पुरस्कारों के कारण कुल आपूर्ति की मुद्रास्फीति के बावजूद, स्टेक की गई SOL की मात्रा अपेक्षाकृत स्थिर रही है (जैसा कि ऊपर दिए गए चार्ट में दिखाया गया है)। इसका मतलब है कि सोलाना का SOL स्टेक प्रतिशत समय के साथ धीरे-धीरे कम हो रहा है, जो स्टेकर्स के लिए एक अनुकूल गतिशीलता है।

हालाँकि स्टेक की गई SOL की कुल राशि समग्र रूप से स्थिर बनी हुई है, फिर भी इसमें महत्वपूर्ण उतार-चढ़ाव है, प्रत्येक युग में स्टेक की गई और बिना स्टेक की गई SOL की राशि अक्सर सात अंकों तक पहुँच जाती है। यह उतार-चढ़ाव मुख्य रूप से स्टेकिंग पूल के भीतर फंड के प्रवाह से प्रेरित होता है।

साप्ताहिक स्टेकिंग परिवर्तन ( स्रोत )

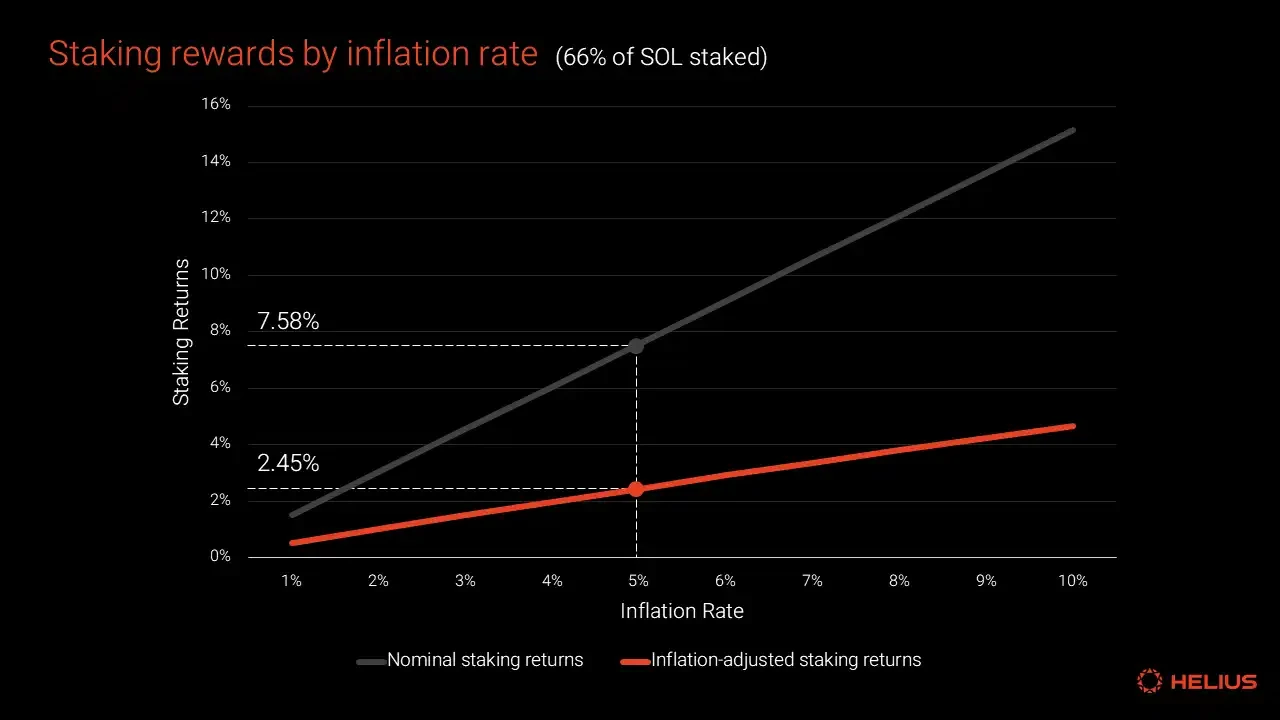

जैसा कि पहले बताया गया है, वर्तमान SOL स्टेकिंग प्रतिशत 65% है और मुद्रास्फीति दर 5.07% है। यह मानते हुए कि स्टेकिंग दर दो-तिहाई पर बनी हुई है, हम स्टेकिंग रिवॉर्ड के मुद्रास्फीति-समायोजित और असमायोजित चार्ट बना सकते हैं, जो क्रमशः नाममात्र रिटर्न और मुद्रास्फीति के लिए समायोजित रिटर्न दिखाते हैं।

66% की स्थिर SOL स्टेकिंग दर मानते हुए नाममात्र और मुद्रास्फीति-समायोजित स्टेकिंग पुरस्कार

इसके बाद, हम सोलाना की मुद्रास्फीति विरोधी शक्तियों का विश्लेषण करेंगे, और हम तीन प्रकारों की पहचान करेंगे: लेनदेन शुल्क विनाश, दंडात्मक कटौती, और उपयोगकर्ता-संबंधित नुकसान। इसके अलावा, हम मुद्रास्फीति पर सोलाना के पट्टे तंत्र के प्रभाव पर विचार करेंगे। यह खंड "शुद्ध मुद्रास्फीति" शब्द का परिचय देता है, जिसे इस प्रकार परिभाषित किया गया है:

शुद्ध मुद्रास्फीति = सकल मुद्रास्फीति – सकल अवस्फीति

इस अनुभाग में सभी ग्राफ़ और डेटा ज़ैन द्वारा प्रदान किए गए डेटासेट पर आधारित हैं शिनोबी सिस्टम्स . कच्चा डेटा उपलब्ध है एक स्प्रेडशीट (देखने के लिए क्लिक करें) पाठकों को अपना स्वयं का विश्लेषण करने के लिए प्रोत्साहित किया जाता है।

ट्रांजेक्शन फीस बर्निंग एकमात्र प्रोटोकॉल मैकेनिज्म है जो सीधे SOL को हटाता है और कुल आपूर्ति को कम करता है। पहले, फीस बर्निंग मैकेनिज्म में प्रत्येक ब्लॉक में सभी ट्रांजेक्शन के बेस फीस के 50% और प्राथमिकता फीस के 50% को बर्न करना शामिल था। बेस फीस (जिसे सिग्नेचर फीस के रूप में भी जाना जाता है) को प्रति सिग्नेचर 5,000 लैम्पॉर्ट्स पर तय किया जाता है, चाहे ट्रांजेक्शन की जटिलता कुछ भी हो - आमतौर पर प्रत्येक ट्रांजेक्शन में एक सिग्नेचर होता है। प्राथमिकता शुल्क तकनीकी रूप से वैकल्पिक है, लेकिन धीरे-धीरे यह मानक अभ्यास बन रहा है। इन फीस की कीमत प्रति कम्प्यूटेशनल यूनिट माइक्रोलैम्पॉर्ट्स (एक लैम्पॉर्ट का दस लाखवाँ हिस्सा) में तय की जाती है।

प्राथमिकता शुल्क = गणना इकाई मूल्य (माइक्रोलैम्पॉर्ट्स) x गणना इकाई सीमा

SIMD के पारित होने के साथ यह संरचना बदल जाएगी – 96, जो कार्यान्वित किया गया वर्तमान रिलीज़ योजना के अनुसार ब्रेकपॉइंट 2024 के तुरंत बाद एगेव 2.0 के साथ। भविष्य में, प्राथमिकता शुल्क का 100% ब्लॉक उत्पादकों को जाएगा, जिससे प्रोटोकॉल के बाहर सौदे करने के लिए उनका प्रोत्साहन समाप्त हो जाएगा।

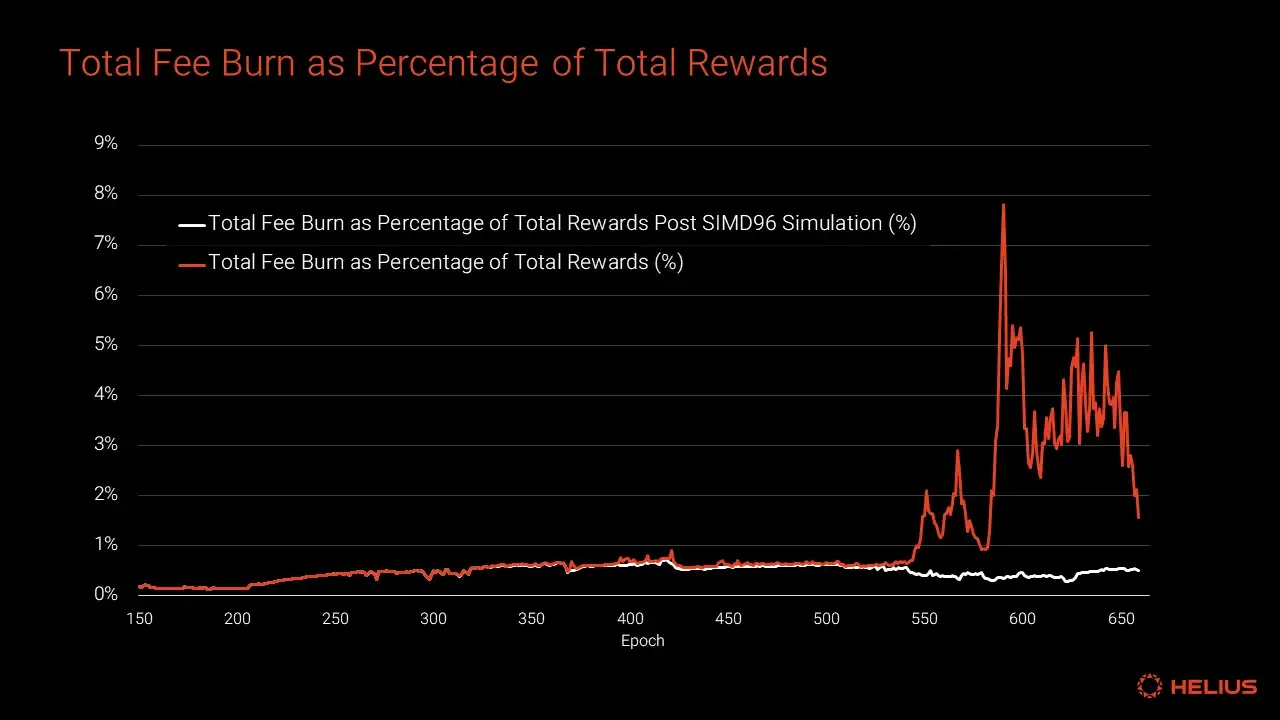

10 दिसंबर, 2023 को युग 544 से शुरू होकर, प्राथमिकता शुल्क में एक स्पष्ट मोड़ आ गया है। सबसे अधिक कुल शुल्क बर्न युग 590 (18 मार्च, 2024 से शुरू) में हुआ, जिसमें कुल 13,212.31 SOL बर्न हुआ। पिछले 100 युगों में, प्रति युग औसत कुल शुल्क बर्न 5,372.16 SOL है।

SIMD-96 से पहले युग के अनुसार कुल SOL शुल्क विनाश (प्राथमिकता + हस्ताक्षर शुल्क)

14 दिसंबर, 2023 को शुरू हुए युग 546 में, फीस बर्न ने पहली बार कुल स्टेकिंग रिवॉर्ड्स के 1% से अधिक का हिसाब लगाया, और 18 मार्च, 2024 को शुरू हुए युग 590 में 7.8% के शिखर पर पहुंच गया। पिछले 100 युगों में, फीस बर्न ने कुल स्टेकिंग रिवॉर्ड्स का औसतन 3.2% किया है। हालाँकि, अगर हम फीस बर्न का अनुकरण करने के लिए SIMD-96 नियम परिवर्तन (प्राथमिकता शुल्क बर्न को हटाना) लागू करते हैं, तो सोलानास के इतिहास में किसी भी बिंदु पर बर्न की गई कुल राशि कुल स्टेकिंग रिवॉर्ड्स के 1% से अधिक नहीं होगी। यदि SIMD-96 परिवर्तन पिछले 100 युगों में लागू किए गए थे, तो कुल जारीकरण 2.81% तक बढ़ जाएगा (उदाहरण के लिए, 5% शुद्ध मुद्रास्फीति वाला युग 5.14% तक बढ़ जाएगा)। इससे पहले, सत्यापनकर्ता समुदाय के सदस्य अनुमानित कुल निर्गम में यह वृद्धि 4.6% पर थोड़ी अधिक हो सकती है।

प्रति युग शुद्ध मुद्रास्फीति का विश्लेषण (कुल स्टेकिंग पुरस्कार घटा कुल शुल्क बर्न के रूप में परिभाषित) दिखाता है कि नए SOL टोकन जारी करना प्रोटोकॉल में टोकन बर्न के प्रभाव से कहीं अधिक है। इसके अलावा, SIMD-96 के कार्यान्वयन के साथ, टोकन बर्न का पहले से ही सीमित प्रभाव और भी कम होकर लगभग नगण्य हो जाएगा।

में सोलाना फोरम में SIMD-96 के बारे में चर्चा , एक टिप्पणी 7 लेयरमैजिक (ओवरक्लॉक वैलिडेटर) ने मुद्रास्फीति पर SIMD-96 के प्रभाव का सारांश दिया:

"यह SIMD लेनदेन शुल्क के लिए महत्वपूर्ण अपस्फीति दबाव बनाना बहुत कठिन बना देगा। जबकि वर्तमान में मुद्रास्फीति टोकन जारी करने से लेनदेन शुल्क बर्न को छुपाया जा सकता है, फिर भी यह संभव है कि भविष्य में शुल्क बर्न का बड़ा प्रभाव होगा - हालाँकि, यह SIMD उन्हें उस संबंध में बहुत अधिक महत्वहीन बनाता है। अपस्फीति दबाव मायने रखता है या नहीं, यह बहस का विषय है।"

ध्यान देने योग्य एक अंतिम बिंदु यह है कि मुद्रास्फीति योजना के विपरीत, जिस पर औपचारिक रूप से समुदाय द्वारा मतदान किया गया था, प्राथमिकता शुल्क के 50% को जलाने का प्रारंभिक निर्णय औपचारिक शासन या आम सहमति प्रक्रिया से नहीं गुजरा था।

उपयोगकर्ता-संबंधित हानि एक व्यापक शब्द है जो उन स्थितियों को संदर्भित करता है जहाँ SOL उपयोगकर्ता त्रुटि, सुरक्षा घटनाओं, प्रोग्राम कमजोरियों या निजी कुंजियों के नुकसान जैसे दुर्भाग्यपूर्ण तरीकों से स्थायी रूप से खो जाता है। उदाहरण के लिए, पिछले अनुमान दिखाते हैं कि इथेरियम (912,296.82 ETH) की कुल आपूर्ति का लगभग 0.76%, जो लेखन के समय लगभग $2.3 बिलियन मूल्य का था, इसी तरह की घटनाओं के कारण स्थायी रूप से खो गया है। इनमें से आधे से अधिक नुकसानों को एक के लिए जिम्मेदार ठहराया जा सकता है सुरक्षा घटना 2017 में, जिसके परिणामस्वरूप 500,000 से अधिक ETH फ्रीज हो गए थे।

खोए हुए ETH प्रकार (स्रोत)

बिटकॉइन एक और उल्लेखनीय उदाहरण है जहां डेटा उपलब्ध है। 1.75 मिलियन बिटकॉइन वॉलेट एक दशक या उससे ज़्यादा समय से इस्तेमाल नहीं किए गए हैं, कुल 1,798,681 BTC हैं, जिनकी कीमत लेखन के समय लगभग $106.3 बिलियन है। इस आंकड़े में लगभग 30,000 वॉलेट शामिल नहीं हैं, जिन्हें बिटकॉइन निर्माता सातोशी नाकामोटो से जुड़ा माना जाता है। ये लंबे समय से निष्क्रिय सिक्के 21 मिलियन बिटकॉइन की कुल निश्चित आपूर्ति का 8.3% प्रतिनिधित्व करते हैं। हालांकि यह सुनिश्चित करना असंभव है, कई को देखते हुए हाई-प्रोफाइल मामले खोई हुई या भूली हुई चाबियों के कारण उपयोगकर्ता अपने बिटकॉइन तक पहुंचने में असमर्थ हो सकते हैं, इनमें से कई सिक्के हमेशा के लिए खो गए होंगे।

जैसे-जैसे सोलाना नेटवर्क की गतिविधि बढ़ती है, उपयोगकर्ता से संबंधित नुकसान अपरिहार्य रूप से होंगे। निजी कुंजियों को लंबे समय तक सुरक्षित रूप से संग्रहीत करना चुनौतीपूर्ण है, और यहां तक कि पेशेवर वॉलेट सेवा प्रदाता भी ऐसा कर सकते हैं गल्तियां करते हैं इसके अतिरिक्त, टोकन धारक मृत्यु से पहले अपनी निजी कुंजी स्थानांतरित नहीं कर सकते हैं, जिसके परिणामस्वरूप टोकन खो जाते हैं।

हालाँकि सोलाना में इस तरह के तंत्र पर विचार किया गया था की प्रारंभिक आर्थिक डिजाइन , कार्यक्रमगत दंडात्मक कटौती अभी तक लागू नहीं की गई है। आधिकारिक दस्तावेज मैन्युअल सोशल स्लैशिंग प्रक्रिया का वर्णन किया गया है जिसका परीक्षण टेस्टनेट पर किया गया है:

"...सुरक्षा भंग होने के बाद, नेटवर्क को निलंबित कर दिया जाएगा। हम डेटा का विश्लेषण कर सकते हैं, जिम्मेदार पक्षों की पहचान कर सकते हैं, और पुनः आरंभ होने के बाद उनकी हिस्सेदारी कम करने की सिफारिश कर सकते हैं।"

पूर्णता के लिए, हम अपने विश्लेषण में स्लैशिंग को उन ज्ञात तरीकों में से एक के रूप में शामिल करते हैं, जिनसे प्रूफ-ऑफ-स्टेक नेटवर्क टोकन आपूर्ति को कम करते हैं। हालाँकि, क्योंकि ऐसा अक्सर नहीं होता है, इसलिए समग्र मुद्रास्फीति दर पर स्लैशिंग का प्रभाव महत्वपूर्ण नहीं हो सकता है। इसके अतिरिक्त, स्वचालित स्लैशिंग के लिए कुछ प्रारंभिक प्रस्ताव सीधे प्रिंसिपल को स्लैश करने के बजाय, कई युगों के लिए स्टेक किए गए टोकन को फ्रीज करने का सुझाव देते हैं, जिससे वे पुरस्कार के लिए अयोग्य हो जाते हैं। इसलिए, ये तरीके वास्तव में टोकन आपूर्ति को कम नहीं कर सकते हैं।

जबकि किराया मुद्रास्फीति को कम करने वाली वास्तविक ताकत नहीं है, फिर भी इस संदर्भ में इस पर चर्चा करना उचित है। सभी सोलाना खातों के लिए न्यूनतम "किराया-मुक्त" एसओएल शेष रखना आवश्यक है, जो भंडारण के लिए भुगतान करने और यह सुनिश्चित करने के लिए आवश्यक है कि खाता सत्यापनकर्ता की मेमोरी में सक्रिय रहे। यह न्यूनतम शेष राशि आवश्यकता संग्रहीत डेटा की मात्रा के अनुपात में है और खाता बंद होने पर पूरी तरह से वापसी योग्य है। सोलाना की किराया दर नेटवर्क-वाइड है और लैम्पॉर्ट्स की संख्या के अनुसार निर्धारित की जाती है प्रति बाइट प्रति वर्ष रनटाइम स्थिरांक पर आधारित। उदाहरण के लिए, एक मानक उपयोगकर्ता टोकन खाता ( लिंक किया गया टोकन खाता ) का किराया-मुक्त शेष 0.002 SOL है। यह तंत्र राज्य के विस्तार को कम करने में मदद करता है और उपयोगकर्ताओं को अप्रयुक्त खातों को बंद करने के लिए प्रोत्साहित करता है।

कई कार्यक्रम उपयोगकर्ताओं के लिए किराया रिफंड का प्रबंधन स्वचालित रूप से करते हैं, और कुछ कार्यक्रम ऐसे भी हैं जो उपयोगकर्ताओं के लिए किराया रिफंड का प्रबंधन करते हैं। एकाधिक अनुप्रयोग इस सहायता उपयोगकर्ताओं को अप्रयुक्त खातों से किराया वापस मिलता है। हालाँकि, इन उपकरणों के बावजूद, कई सोलाना उपयोगकर्ताओं को अभी भी यह अच्छी तरह से समझ नहीं है कि किराया कैसे काम करता है। इसके अतिरिक्त, कुछ एप्लिकेशन उपयोगकर्ताओं को किराया वसूलने का आसान तरीका प्रदान करने में विफल रहते हैं।

ए डाक जुपिटर DAO फोरम पर बड़े पैमाने पर ऑन-चेन DAO वोटिंग के कारण उच्च किराये की लागत की समस्या की ओर इशारा किया गया

प्रत्येक किराया भुगतान एसओएल के एक अस्थायी लॉक का प्रतिनिधित्व करता है, जो कि अगर इसे वसूल नहीं किया जाता है तो उपयोगकर्ता से संबंधित नुकसान का गठन करता है। जबकि एक एकल खाते के लिए किराए की राशि बहुत छोटी है, ये छोटे नुकसान सभी अनुप्रयोगों और उपयोगकर्ताओं पर विचार करने पर काफी कुल में जमा हो सकते हैं। भविष्य में, ZK संपीड़न प्रौद्योगिकी इससे इन उच्च खाता लागतों को आंशिक रूप से कम किया जा सकता है।

"ये बस कुछ संख्याएँ हैं जो एक ब्लैक बॉक्स में घूम रही हैं... मौजूदा मुद्रास्फीति योजना शायद बहुत ज़्यादा है। अगर इसे दस गुना कम भी कर दिया जाए, तो भी सब ठीक रहेगा। मुझे लगता है कि अंत में ये लागतें उतनी महत्वपूर्ण नहीं हैं।" - अनातोली याकोवेंको ( स्रोत )

इस अंतिम मुख्य भाग में, हम सबसे पहले शेष गैर-परिसंचारी आपूर्ति अनलॉकिंग शेड्यूल को संक्षेप में निर्धारित करेंगे। फिर हम सोलाना के टोकन जारी करने को संशोधित करने के लिए तर्कों पर चर्चा करेंगे, जिसमें "नेटवर्क लागत के रूप में जारी करना" की अवधारणा, मुद्रास्फीति की कर अक्षमता, मुद्रास्फीति का नीचे की ओर मूल्य दबाव, नेटवर्क उपयोग पर दंडात्मक प्रभाव और वैकल्पिक सत्यापनकर्ता राजस्व स्रोतों का उदय शामिल है। इसके बाद, हम मुद्रास्फीति अनुसूची को समायोजित करने और मुद्रास्फीति को कम करने के कुछ व्यावहारिक तरीकों का पता लगाएंगे।

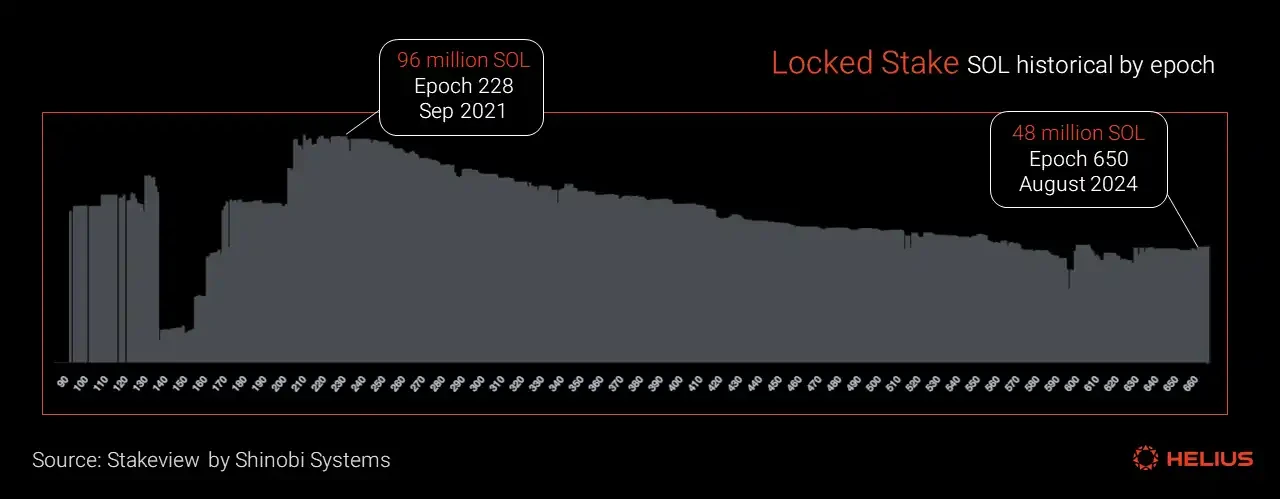

पिछले तीन वर्षों में, सोलाना की लॉक्ड स्टेक अनलॉकिंग दर अपेक्षाकृत स्थिर रही है, जो सितंबर 2021 में 96 मिलियन एसओएल के शिखर से गिरकर सितंबर 2024 में 48 मिलियन एसओएल हो गई है, जो कुल मिलाकर 501टीपी9टी की कमी है।

लॉक्ड स्टेकिंग ऐतिहासिक डेटा (स्रोत)

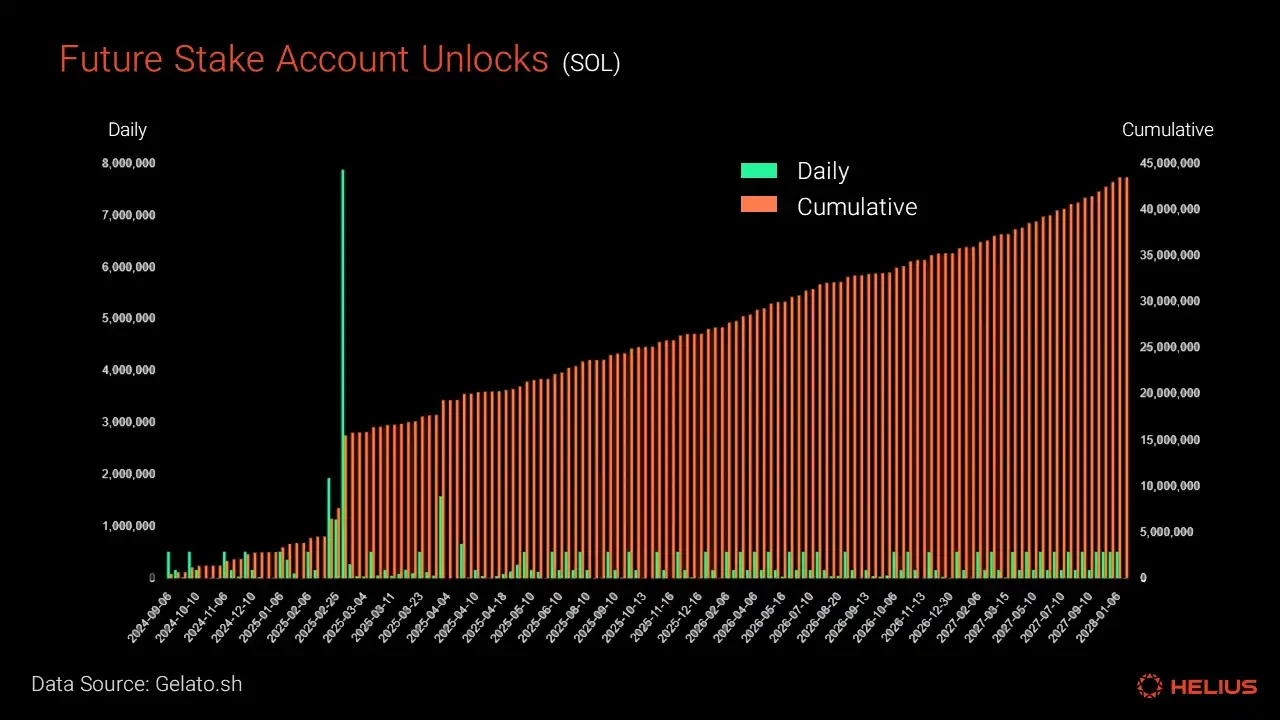

कम से कम 43.5 मिलियन SOL टोकन स्टेकिंग खातों में लॉक हैं, जो वर्तमान आपूर्ति का 7.5% है। इसमें इस साल की शुरुआत में FTX एसेट दिवालियापन कार्यवाही के दौरान गैलेक्सी डिजिटल और पैनटेरा जैसी बड़ी उद्योग संस्थाओं को बेचे गए 41 मिलियन SOL टोकन शामिल हैं। नेप्च्यून डिजिटल एसेट्स जैसी कुछ कंपनियों ने अपनी खरीद के विवरण की सार्वजनिक रूप से घोषणा की है - नेप्च्यून ने $64 प्रति कॉइन पर 26,964 SOL खरीदे। इनमें से 20% टोकन मार्च 2025 में अनलॉक किए जाएंगे, और शेष 2028 की शुरुआत तक हर महीने रैखिक रूप से अनलॉक किए जाएंगे। यह अनलॉकिंग शेड्यूल ऑन-चेन लॉक किए गए स्टेकिंग अकाउंट डेटा (चार्ट देखें) के अनुरूप है।

भविष्य में गिरवी रखे गए खातों को अनलॉक करना (डेटा स्रोत)

नीचे, हम सोलाना के निर्गम को समायोजित करने के कई कारण प्रस्तुत कर रहे हैं।

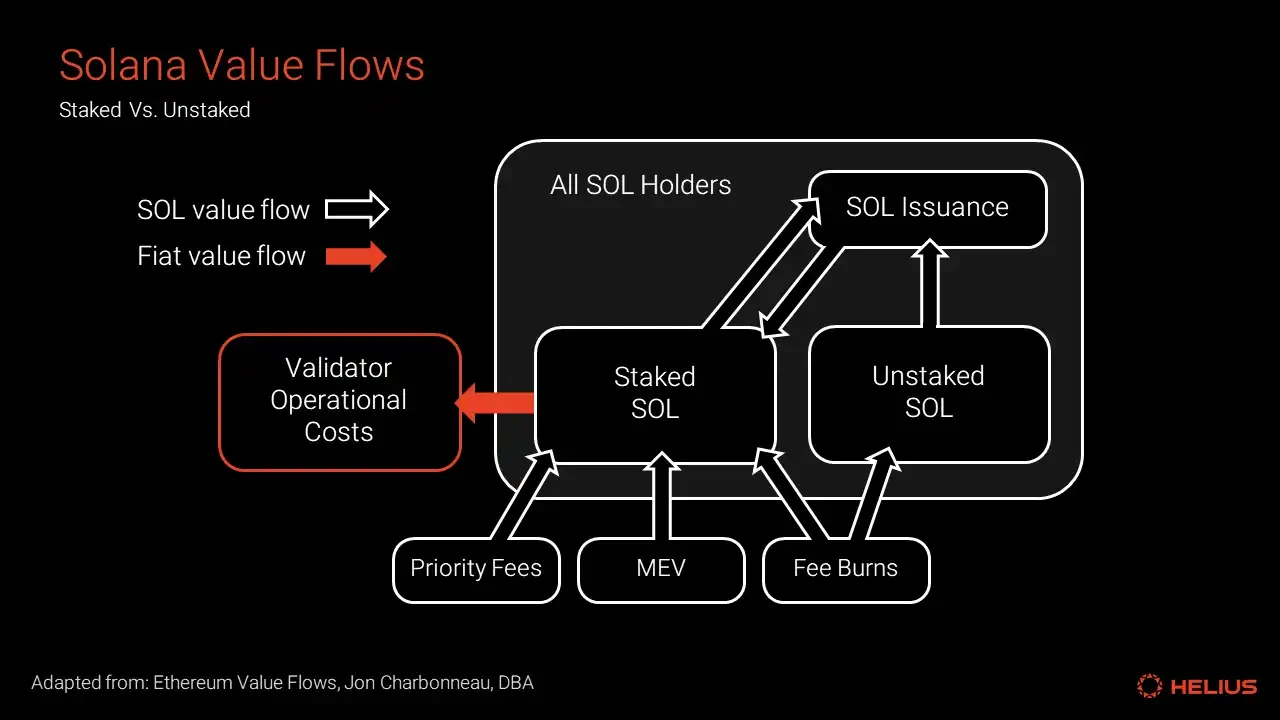

प्रूफ ऑफ स्टेक (PoS) में मुद्रास्फीति के खिलाफ एक आम तर्क यह है कि मुद्रास्फीति नेटवर्क के लिए एक स्पष्ट लागत है और टोकन जारी करना ब्लॉकचेन की लाभप्रदता का हिस्सा है, जिसकी गणना इस प्रकार की जाती है: लाभ = विनाश - जारी करना। हालाँकि, यह तर्क ग़लत है मुद्रास्फीति को इस तरह से नहीं समझा जा सकता है, यह वास्तव में सभी टोकन धारकों और स्टेकरों के बीच धन का पुनर्वितरण है, और सभी टोकन धारकों को इस नकदी प्रवाह को प्राप्त करने का समान अधिकार है।

मुद्रास्फीति से जुड़ी एकमात्र नेटवर्क लागत, मूल्य का वह हिस्सा है जो स्टेकर्स से सत्यापनकर्ताओं तक प्रवाहित होता है, जिसका उपयोग परिचालन व्यय का भुगतान करने के लिए किया जाता है, जैसा कि नीचे दिए गए चित्र में दिखाया गया है।

सोलाना वैल्यू फ्लो, इस से अनुकूलित स्रोत

हम वैलिडेटर को दिए जाने वाले कुल स्टेकिंग रिवॉर्ड कमीशन को देखकर मूल्य के इस प्रवाह को मापना शुरू कर सकते हैं, जो वर्तमान में प्रति युग लगभग 44,000 SOL है। हालाँकि, यह आँकड़ा निजी स्व-स्टेकिंग वैलिडेटर की मौजूदगी से बहुत अधिक बढ़ जाता है, जिन्हें 100% कमीशन दर प्राप्त होती है।

युग के अनुसार सत्यापनकर्ताओं को दिया गया कुल स्टेकिंग पुरस्कार कमीशन

दुनिया भर के कई अधिकार क्षेत्रों में, अतिरिक्त टोकन के रूप में मुद्रास्फीति पुरस्कार प्राप्त करना स्टॉक लाभांश के समान एक कर योग्य घटना माना जाता है। इस प्रकार की आय पर आम तौर पर आयकर के रूप में कर लगाया जाता है। इस कर के बोझ के कारण स्टेकर्स को करों का भुगतान करने के लिए हर साल अपने कुछ टोकन बेचने पड़ सकते हैं, जिससे लगातार बिक्री का दबाव बना रहता है। इस प्रभाव को मापना बेहद मुश्किल है क्योंकि कर कानून जटिल हैं और दुनिया भर में बहुत भिन्न हैं। एक ही अधिकार क्षेत्र के भीतर भी, व्यक्तियों की कर देनदारियाँ काफी भिन्न हो सकती हैं। इसके अलावा, क्योंकि स्टेकिंग अनुमति रहित है, इसलिए किसी व्यक्ति के पास टोकन स्वामित्व का पता लगाना मुश्किल है।

जिटो ब्लॉग भेजा उल्लेख है कि लिक्विड स्टेकिंग टोकन (LST) को रीबेस करने से इस कर के बोझ को कम करने में मदद मिल सकती है:

"सोलाना पर गैर-रीबेस्ड एलएसटी उपयोगकर्ताओं को कर योग्य घटना को ट्रिगर किए बिना पुरस्कारों का दावा करने की अनुमति दे सकता है, क्योंकि वॉलेट में एलएसटी टोकन की संख्या नहीं बदलेगी (कृपया अपनी स्थिति के लिए विशिष्ट सलाह के लिए एक वित्तीय पेशेवर से परामर्श करें)।"

हालाँकि, SOL और स्टेक्ड SOL के बीच रूपांतरण भी अपने आप में कर योग्य घटनाएँ हो सकती हैं। इसके अलावा, जैसा कि हमने पिछले लेख में बताया था एसएफडीपी रिपोर्ट , सोलाना पर LST का समग्र रूप से अपनाया जाना कम बना हुआ है। वर्तमान में स्टेक किए गए SOL का 94% मूल रूप से स्टेक किया गया है, जिसमें केवल 6% एसओएल (24.2 मिलियन एसओएल) का लिक्विड स्टेकिंग किया जा रहा है, जबकि 2024 की शुरुआत में 17 मिलियन एसओएल और एक साल पहले 12.4 मिलियन एसओएल (951टीपी9टी वार्षिक वृद्धि) था।

मुद्रास्फीति दीर्घकालिक, निरंतर नीचे की ओर मूल्य दबाव पैदा कर सकती है, जो बाजार मूल्य संकेतों को विकृत करती है और उचित मूल्य तुलना को रोकती है। पारंपरिक वित्तीय बाजारों से एक सादृश्य का उपयोग यह समझाने के लिए किया जा सकता है: PoS मुद्रास्फीति एक सार्वजनिक कंपनी के समान है जो हर दो दिन में एक छोटा स्टॉक विभाजन करती है। चार्ट, डैशबोर्ड, आकस्मिक पर्यवेक्षक और सीमांत खुदरा निवेशक आमतौर पर अपने विश्लेषण में मुद्रास्फीति के प्रभाव पर विचार नहीं करते हैं।

एक अनुकूल मूल्य चार्ट पारिस्थितिकी तंत्र के लिए सबसे अच्छा विज्ञापन है, न केवल व्यापारियों के लिए बल्कि सभी पारिस्थितिकी तंत्र प्रतिभागियों के लिए। क्रिप्टोकरेंसी जैसे मनोविज्ञान-संचालित बाजार में, मूल्य एक समन्वय बिंदु है और पारिस्थितिकी तंत्र के स्वास्थ्य का संकेत है। मजबूत मूल्य प्रदर्शन हमेशा सबसे अच्छा विपणन होता है - मूल्य कथा को आगे बढ़ाता है।

दो अलग-अलग परिदृश्यों पर विचार करें। मेरे पास वर्तमान में 100 SOL हैं, जिनमें से प्रत्येक का मूल्य $100 है, जिसका कुल मूल्य $10,000 है।

परिदृश्य A: मैं इन SOL को दांव पर लगाने और एक साल तक प्रतीक्षा करने का विकल्प चुनता हूँ। हालाँकि इस अवधि के दौरान कीमत में 5% की गिरावट आई है, लेकिन एक स्टेकर के रूप में, मुझे 12% मुद्रास्फीति पुरस्कार मिले। अब मेरे पास 112 SOL हैं, जिनमें से प्रत्येक का मूल्य $95 है, और कुल होल्डिंग मूल्य $10,650 है।

परिदृश्य बी: मैं दांव नहीं लगाना चाहता। एक साल में SOL की कीमत 5% बढ़ जाती है। मेरे पास अभी भी $105 मूल्य के 100 टोकन हैं, जिनकी कुल होल्डिंग वैल्यू $10,500 है।

पूर्ण रूप से, परिदृश्य A मुझे थोड़ा बेहतर बनाता है। हालाँकि, परिदृश्य B उच्च कीमतों के कारण अधिक संतोषजनक लगता है, भले ही यह धारणा तर्कहीन हो। कीमतों के मनोवैज्ञानिक प्रभाव को अक्सर अनदेखा या कम करके आंका जाता है क्योंकि उन्हें स्वाभाविक रूप से मात्राबद्ध करना मुश्किल होता है। लोग मात्रात्मक डेटा के आधार पर निर्णय या नीतिगत निर्णय लेते हैं, भले ही गुणात्मक कारक समान रूप से या उससे भी अधिक महत्वपूर्ण हो सकते हैं।

प्रूफ-ऑफ-स्टेक (PoS) मुद्रास्फीति वास्तव में उन उपयोगकर्ताओं को दंडित करती है जो सक्रिय रूप से SOL ऑन-चेन का उपयोग करते हैं, जैसे कि लिक्विडिटी पूल में भाग लेना, NFT ट्रेडिंग करना, या ऑर्डर देना - विकास चाहने वाले नेटवर्क को जो प्रोत्साहन देना चाहिए, उसके विपरीत। जबकि सोलाना परिपक्व और मजबूत है लिक्विड स्टेकिंग टोकन (LST) इंफ्रास्ट्रक्चर एसओएल को बिना किसी कमजोरीकरण के सक्रिय रूप से उपयोग करने की अनुमति देकर इन नकारात्मक प्रभावों को आंशिक रूप से कम किया जा सकता है, लेकिन यह अतिरिक्त लागत भी पेश करता है। इन लागतों में उपयोगकर्ता अनुभव में घर्षण, विभिन्न टोकन के बीच तरलता का विखंडन, एलएसटी के बीच रूपांतरण करते समय संभावित फिसलन और उपयोगकर्ताओं पर कमजोरीकरण की अप्रत्यक्ष लागतों से खुद को बचाने के लिए स्टेकिंग तंत्र को समझने का बोझ शामिल है।

कुछ सम्मानित उद्योग टिप्पणीकार नोट किया है अधिकांश मूल टोकन उत्पादक होने चाहिए और आदर्श स्टेकिंग अनुपात 10% के करीब होना चाहिए।

मुद्रास्फीति से कीमतों में गिरावट का दबाव सोलाना की उच्च राज्य भंडारण लागत को कम करने में मदद कर सकता है। ये लागतें तब निर्धारित की गई थीं जब एसओएल की कीमत आज की तुलना में बहुत कम थी। सोलाना डेवलपर समुदाय अक्सर ऑन-चेन प्रोग्रामों को तैनात करने की उच्च लागत के बारे में शिकायत की जाती है, जिसमें अक्सर SOL में सैकड़ों या हजारों डॉलर खर्च होते हैं।

सोलाना डेवलपर समुदाय के सदस्यों ने अपनी राय व्यक्त की (एक्स प्लेटफ़ॉर्म पोस्ट)

जैसा कि हमारे पिछले लेख में बताया गया है एसएफडीपी रिपोर्ट सत्यापनकर्ताओं के पास आय के तीन मुख्य स्रोत हैं: एमईवी (अधिकतम निष्कर्षण योग्य मूल्य) कमीशन, ब्लॉक पुरस्कार और स्टेकिंग पुरस्कार पर कमीशन।

किसी सत्यापनकर्ता के लिए परिचालन आय का स्रोत उसकी स्टेकिंग स्थिति पर निर्भर करता है।

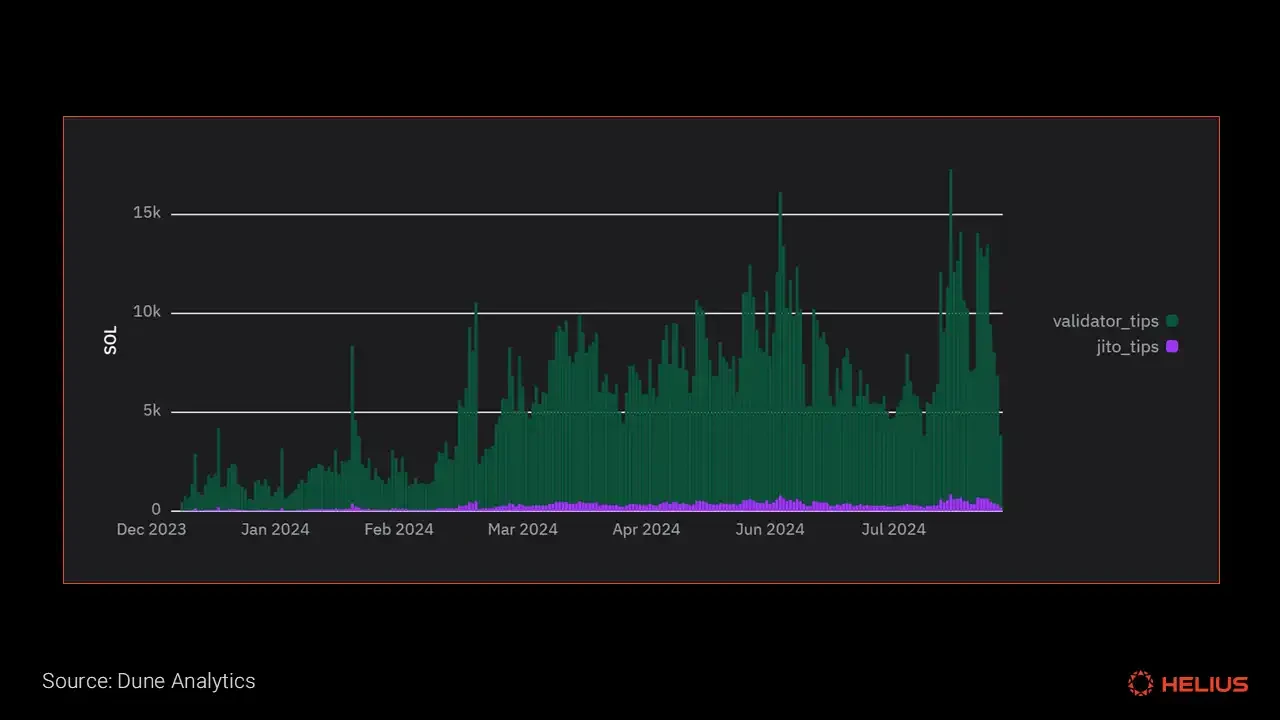

दिसंबर 2023 से MEV कमीशन और ब्लॉक रिवॉर्ड में उल्लेखनीय वृद्धि हुई है। रिपोर्ट के फीस बर्निंग सेक्शन में, हमने प्राथमिकता शुल्क के डेटा पर चर्चा की। निम्नलिखित चार्ट MEV की वृद्धि को दर्शाता है।

2024 में जिटो दैनिक टिप वृद्धि (डैशबोर्ड)

इन तीन आय स्रोतों का अनुपात सत्यापनकर्ता से सत्यापनकर्ता के बीच अलग-अलग होगा, जो सत्यापनकर्ता की कुल हिस्सेदारी, कमीशन स्तर, स्व-प्रत्यायोजित हिस्सेदारी का प्रतिशत, स्टेकिंग पूल या जैसी परियोजनाओं को दिए गए कमीशन पर निर्भर करेगा। दांव नीलामी बाजार जैसे मैरिनेड फाइनेंस, और कुल मिलाकर प्रदर्शन मेट्रिक्स जैसे निष्क्रियता दर और मतदान में देरी।

हालांकि, उच्च मुद्रास्फीति से सबसे अधिक लाभ उठाने वाले सत्यापनकर्ताओं के समूहों की पहचान करना आसान है, जिसमें अत्यधिक स्टेक वाले एक्सचेंज सत्यापनकर्ता शामिल हैं जो ऑफ-चेन खुदरा उपयोगकर्ताओं और कुछ संस्थागत-केंद्रित सत्यापनकर्ताओं की सेवा करते हैं। इन सत्यापनकर्ताओं की आम तौर पर अपेक्षाकृत उच्च कमीशन दरें होती हैं, जैसे कि कॉइनबेस (8%), बिनेंस स्टेकिंग (8%), क्रैकन (100%), और अपबिट (100%)। संस्थागत उदाहरणों में एवरस्टेक (7%), ट्विनस्टेक (10%), हैशकी (7%), और पी2पी (7%) शामिल हैं।

दूसरी ओर, इकोसिस्टम टीमें (जैसे जुपिटर 0%, सोलफ्लेयर 6%, मृगन 0%, हेलियस 0%) और स्वतंत्र सत्यापनकर्ता (जैसे मेलिया 0%, स्टेकहाउस 0%, शिनोबी सिस्टम्स 3%, लेन 5%, सोलाना कम्पास 5%) आम तौर पर कम कमीशन दर प्रदर्शित करते हैं और मुद्रास्फीति आयोगों से कम लाभ उठाते हैं। ऐसा इसलिए है क्योंकि इन सत्यापनकर्ताओं, विशेष रूप से लंबी-पूंछ वाले स्वतंत्र सत्यापनकर्ताओं को चेन पर सक्रिय स्टेकर्स को लक्षित करके बाजार हिस्सेदारी के लिए प्रतिस्पर्धा करनी चाहिए जो वार्षिक उपज (APY) के आधार पर प्रतिक्रिया करते हैं। ये स्टेकर्स सबसे अधिक मूल्य संवेदनशील होते हैं और उच्चतम रिटर्न चाहते हैं।

कुल मिलाकर, मुद्रास्फीति आयोगों के बाहर वैकल्पिक राजस्व स्रोतों में 2024 में उल्लेखनीय वृद्धि हुई है। हालांकि, यह देखा जाना बाकी है कि क्या ये वैकल्पिक राजस्व स्रोत लंबे समय में इतने उच्च स्तर पर बने रह सकते हैं। साथ ही, वे सत्यापनकर्ता समूह जो सबसे अधिक लाभान्वित होते हैं, वे एक्सचेंज और संस्थागत सत्यापनकर्ता हैं जो उच्च शुल्क लेते हैं, जो नेटवर्क के सुपर-अल्पसंख्यक और सुपर-बहुमत के अनुपातहीन हिस्से के लिए जिम्मेदार हैं।

यह अनुभाग निम्न से डेटा का उपयोग करता है सोलाना बीच स्टेकिंग कमीशन के स्रोत के रूप में। सत्यापनकर्ता समुदाय के बारे में और अधिक जानकारी के लिए, हमारा पिछला लेख देखें एसएफडीपी रिपोर्ट .

अनातोली याकोवेंको ( स्रोत ) ने एक बार कहा था: तर्कसंगत रूप से, आपको कोरम चुनने के लिए कुछ स्टेकर्स की आवश्यकता होती है। कोरम नेटवर्क आउटेज जैसे सुरक्षा उल्लंघन का कारण नहीं बनेगा, लेकिन एक अच्छी तरह से प्रबंधित प्रणाली में, कोरम वास्तव में बहुत कुछ नहीं कर सकता है। लोगों को स्टेक करने और इस प्रकार कोरम चुनने के लिए आपको कुछ प्रोत्साहन की आवश्यकता होती है। आपको कुछ दंड तंत्रों की भी आवश्यकता होती है, जैसे कि स्लैशिंग, यह सुनिश्चित करने के लिए कि लोग कोरम चुनने में अच्छा काम करते हैं, बस इतना ही।

मुद्रास्फीति पुरस्कार उपयोगकर्ताओं को अपने टोकन को दांव पर लगाने के लिए प्रोत्साहित करते हैं, जिससे नेटवर्क की सुरक्षा बढ़ जाती है। हालाँकि सोलाना की वर्तमान स्टेकिंग दर 65% पर अपेक्षाकृत अधिक है, मुद्रास्फीति पुरस्कारों में महत्वपूर्ण कमी से स्टेकिंग का संतुलन स्तर बदल सकता है, जिससे संभावित रूप से कुछ अनपेक्षित परिणाम हो सकते हैं, जैसे कि शासन भागीदारी में गिरावट।

मेरा एक मुख्य सिद्धांत हमेशा से यह रहा है कि किसी मान को या तो दोगुना करें या आधा करें। इसे 5%, फिर 5%, फिर एक और 5% से समायोजित करने में समय बर्बाद न करें...बस इसे दोगुना करें और देखें कि क्या यह आपकी अपेक्षा के अनुरूप प्रभाव उत्पन्न करता है। - सिड मीयर, गेम सिविलाइज़ेशन के निर्माता। स्रोत: सिड मेयर्स संस्मरण

इस खंड में, हम सोलाना की मुद्रास्फीति अनुसूची के तीन प्रमुख मापदंडों को समायोजित करके मुद्रास्फीति दर को संशोधित करने के लिए कई काल्पनिक परिदृश्यों का पता लगाएंगे। इस विश्लेषण का उद्देश्य समग्र मुद्रास्फीति दर पर प्रत्येक पैरामीटर के प्रभाव की स्पष्ट समझ प्रदान करना है।

वर्तमान पैरामीटर:

प्रारंभिक मुद्रास्फीति दर: 8%

अवमुद्रास्फीति दर: -15%

दीर्घकालिक मुद्रास्फीति दर: 1.5%

ये प्रक्षेपण डेटा यहां पाया जा सकता है स्प्रेडशीट .

हम निम्नलिखित परिदृश्यों का अन्वेषण करेंगे:

परिदृश्य A: अपस्फीति दर को -15% से दोगुना करके -30% करना

परिदृश्य बी: दीर्घावधि मुद्रास्फीति दर को 1.5% से घटाकर 0.75% करना

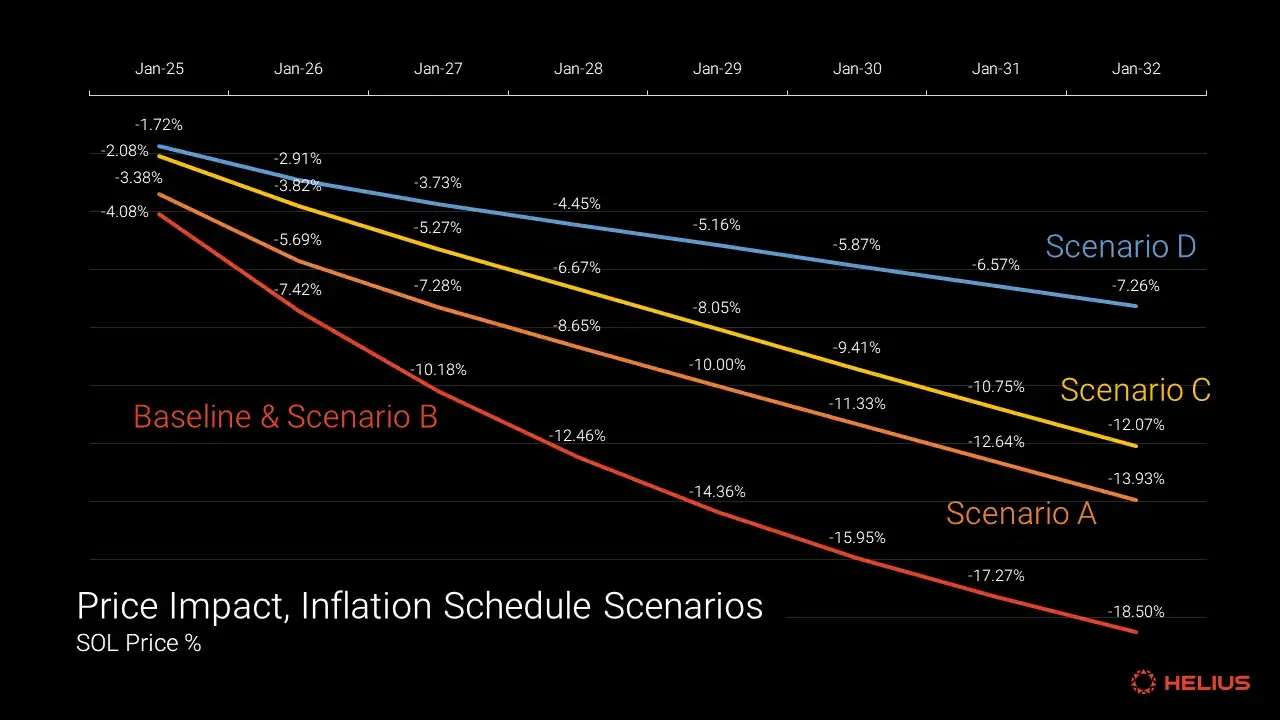

परिदृश्य C: वर्तमान मुद्रास्फीति दर को 5% से तुरंत आधा करके 2.5% कर दें

परिदृश्य डी: वर्तमान मुद्रास्फीति दर को आधा करें, अपस्फीति दर को दोगुना करें, तथा अंतिम मुद्रास्फीति दर को आधा करें

प्रत्येक परिदृश्य को समग्र मुद्रास्फीति दर पर इन प्रमुख समायोजनों के दीर्घकालिक प्रभाव का परीक्षण करने के लिए डिज़ाइन किया गया है, जिससे यह समझने में मदद मिलती है कि विभिन्न रणनीतियाँ SOL की मुद्रास्फीति गतिशीलता को कैसे बदल सकती हैं।

सितंबर 2024 से मौजूदा मुद्रास्फीति दर लगभग 5% होने का अनुमान है, जिसमें कुल आपूर्ति 584 मिलियन SOL है, जो अगले आठ वर्षों में प्रभाव का अनुकरण करती है। जैसा कि पहले दिखाया गया है, सोलाना के टोकन बर्न मैकेनिज्म का SIMD-96 कार्यान्वयन के बाद आपूर्ति पर न्यूनतम प्रभाव पड़ता है, इसलिए इस विश्लेषण में इस कारक को अनदेखा किया गया है। गणना को सरल बनाने के लिए, मुद्रास्फीति की गणना वार्षिक आधार पर की जाती है, जिसमें युग वर्षों को मानक वर्षों के बराबर माना जाता है। इसके अलावा, एक आधार रेखा प्रदान की जाती है जहाँ वर्तमान मुद्रास्फीति अनुसूची अपरिवर्तित रहती है।

दीर्घकालिक मुद्रास्फीति दर को आधा करने (परिदृश्य बी) से अगले आठ वर्षों में मुद्रास्फीति पर बहुत कम प्रभाव पड़ेगा। यह परिवर्तन सितंबर 2032 तक कुल आपूर्ति को केवल 1 मिलियन कम करेगा। अपस्फीति दर को दोगुना करने (परिदृश्य ए) के परिणामस्वरूप आठ वर्षों के बाद कुल आपूर्ति 678 मिलियन हो जाएगी, जो कि आधार रेखा से 5.3% की कमी है। वर्तमान मुद्रास्फीति दर को आधा करने (परिदृश्य सी) के परिणामस्वरूप आठ वर्षों के बाद कुल आपूर्ति 664 मिलियन हो जाएगी, जो कि आधार रेखा से 7.3% की कमी है। अंत में (परिदृश्य डी), वर्तमान मुद्रास्फीति दर को आधा करने, अपस्फीति दर को दोगुना करने और टर्मिनल दर को आधा करने के संयोजन से आठ वर्षों के बाद कुल आपूर्ति 629 मिलियन हो जाएगी, जो कि आधार रेखा से 12.2% की कमी है।

सोलाना कुल आपूर्ति पूर्वानुमान मुद्रास्फीति अनुसूची में चार काल्पनिक परिवर्तनों पर आधारित है।

इन आपूर्ति वृद्धि के आधार पर, हम सोलाना के पूर्ण रूप से पतला मूल्यांकन (यानी टोकन मूल्य वर्तमान कुल आपूर्ति) को स्थिर रखते हुए SOL टोकन मूल्य पर उनके अपेक्षित प्रभाव का अनुकरण कर सकते हैं, जबकि अन्य चर स्थिर रहते हैं (यानी "सेटरिस पैरिबस" धारणा)। उदाहरण के लिए, हम SOL टोकन के लिए $150 की शुरुआती कीमत मानते हैं।

हमारे बेसलाइन परिदृश्य में, मौजूदा मुद्रास्फीति पुरस्कार अनुसूची कीमत पर नीचे की ओर दबाव डालती है, जिससे टोकन की कीमत आठ साल में 18.5% गिरकर $122.25 हो जाती है। अपस्फीति दर (परिदृश्य A) को दोगुना करने से, टोकन की कीमत आठ साल में 13.93% गिरकर $129.10 हो जाती है। वर्तमान मुद्रास्फीति दर (परिदृश्य C) को तुरंत आधा करने से कीमत 12.07% गिरकर $131.90 हो जाती है। अंत में (परिदृश्य D), वर्तमान मुद्रास्फीति दर को आधा करने, अपस्फीति दर को दोगुना करने और टर्मिनल ब्याज दर को आधा करने से कीमत आठ साल में केवल 7.26% गिरकर $139.10 हो जाती है।

मुद्रास्फीति अनुसूची में चार काल्पनिक परिवर्तनों के आधार पर सोलाना मूल्य प्रभाव अनुमान।

भविष्य में आगे के शोध के लिए एक दिशा लंबी-पूंछ वाले स्वतंत्र सत्यापनकर्ता संचालनों द्वारा एकत्र किए गए मुद्रास्फीति आयोगों पर इन परिवर्तनों के प्रभाव का विश्लेषण करना है, और उपयोगकर्ताओं को स्टेकिंग जारी रखने के लिए प्रोत्साहन तंत्र पर समग्र प्रभाव का विश्लेषण करना है।

यह लेख सोलाना की मुद्रास्फीति अनुसूची और टोकन जारी करने की प्रणाली को अतीत, वर्तमान और भविष्य के परिप्रेक्ष्य से खोजता है। हम मुद्रास्फीति की गणना और वितरण के लिए उपयोग किए जाने वाले वर्तमान तंत्रों का विश्लेषण करते हैं और मुद्रास्फीति को कम करने वाली प्रतिकारी शक्तियों की पहचान करते हैं। इसके अलावा, हम SIMD-96 के संभावित प्रभाव का आकलन करते हैं, मुद्रास्फीति दर को समायोजित करने के लिए मुख्य तर्कों पर चर्चा करते हैं, और मॉडलिंग मान्यताओं के माध्यम से मुद्रास्फीति अनुसूची मापदंडों में परिवर्तनों का विश्लेषण करते हैं।

सोलाना के टोकन लॉन्च की जांच कई गलतफहमियों के साथ की गई है, और उम्मीद है कि यह रिपोर्ट कुछ प्रमुख सवालों पर स्पष्टता प्रदान कर सकती है। इन विश्लेषणों के माध्यम से, हमारा लक्ष्य अधिक सूचित चर्चाओं को बढ़ावा देना और सकारात्मक बदलाव लाने वाले रचनात्मक संवाद में योगदान देना है।

यह लेख इंटरनेट से लिया गया है: सोलाना की टोकन अर्थव्यवस्था का व्यापक विश्लेषण: क्या एसओएल की मुद्रास्फीति दर अधिक है?

संबंधित: VC और EigenLayer संस्थापक बहस: क्या Web3 डेटा स्वामित्व एक गलत प्रस्ताव है?

मूल अनुवाद: एलेक्स लियू, फ़ोरसाइट न्यूज़ काइल समानी, मल्टीकॉइन में पार्टनर: मैं अपने डेटा के मालिक होने में विश्वास करता था, लेकिन अब नहीं। तथाकथित "स्वामित्व" वास्तव में "विशिष्टता" के बारे में है। यह सबसे स्पष्ट रूप से तब देखा जाता है जब संपत्ति की बात आती है: a) मेरे पास $5 बिल है और आपके पास नहीं है। इसलिए मैं $5 खर्च कर सकता हूँ और आप नहीं कर सकते। b) मेरे पास $1 मिलियन की कलाकृति है। इसे दूसरों को दिखाने के लिए किसी संग्रहालय को उधार देने के बजाय, मैं इसे अपने आनंद के लिए अपनी दीवार पर लटका देता हूँ। स्वामित्व - और इसलिए विशिष्टता - यही कारण है कि क्रिप्टोकरेंसी वित्त से इतनी निकटता से जुड़ी हुई हैं। अब आइए इस बारे में सोचें कि हमारे डेटा का स्वामित्व होने का क्या मतलब है। ईमानदारी से कहूँ तो, मुझे नहीं पता कि इसका क्या मतलब है। डेटा स्वामित्व की अवधारणा के समर्थक अक्सर आरोप लगाते हैं...