My XP

0

Login

मूल लेखक: The Daily Bolt by Revelo Intel

मूल अनुवाद: टेकफ्लो

In this newsletter, we’ll explore Vitalik Buterin’s recent comments on waning interest in DeFi, $ETH’s current underperformance against $BTC and other competitors, and the question of whether $ETH faces an identity crisis, such as whether it serves as “ultrasonic money” or is subject to cannibalization by some L2. $ETH is down 5% year-to-date, which highlights this issue. ETH supporters and others in the crypto space often disagree on semantics when discussing what counts as Ethereum. Whether or not L2s are considered part of Ethereum, L2 developments such as Arbitrum and Base have not been a significant benefit to $ETH as an asset. In the crypto space, people often validate narratives through price because it directly relates to their profitability.

Vitalik Buterin’s recent comments on DeFi have sparked a lively discussion in the cryptocurrency and Ethereum community. Vitalik believes that DeFi in its current form is unsustainable, comparing it to “Ouroboros”, a state of self-eating. This situation highlights the leadership problem in the Ethereum ecosystem. Unlike other competitors with clear leaders, Ethereum faces unique challenges due to its decentralized nature. There is a lack of a clear marketing spokesperson when competing with other blockchains. While Vitalik is a thought leader with a real identity, he is not as active an advocate as Do Kwon once was in the Terra community (maybe there is a reason behind this), nor is he as strong as Anatoli in Solana (Solana has outperformed $ETH and attracted a large number of ordinary investors).

Some community members see DeFi as an important part of Ethereum’s value, and they are concerned about the seeming lack of support from key figures like Vitalik and the Ethereum Foundation (most members simply held or sold $ETH during periods like DeFi Summer). Overall, those closer to Ethereum’s development roadmap and technical implementation seem to be more inclined to prioritize other use cases such as public goods, encrypted information transmission, and quadratic voting – which is very different from the 24/7 infinite casino.

Despite Vitalik Buterin’s skepticism about DeFi, it is worth noting that the current DeFi ecosystem, despite its circular nature, has demonstrated the viability of an on-chain financial system. The infrastructure built for payments, exchanges, lending, and derivatives demonstrates the potential to reduce counterparty risk, increase transparency, and reduce transaction costs. Even if early applications are mostly speculative, these achievements in market efficiency and financial fundamentals should not be ignored.

Meanwhile, current on-chain DeFi seems to have reached a state of stagnation, with the core functionality of exchanges remaining virtually unchanged since Bancor and Uniswap. Rather than becoming simpler, the user experience has become more complex. Users now need to deal with new blockchains and Layer 2 technologies, understand the complexities of cross-chain assets, manage different gas tokens, and handle various token representations. The real innovation may be the introduction of intents and solvers, which effectively centralize order flow into the hands of a handful of established market makers – this goes against the original vision of allowing anyone to become a market maker in a permissionless manner, although relying on professionals does provide users with better prices.

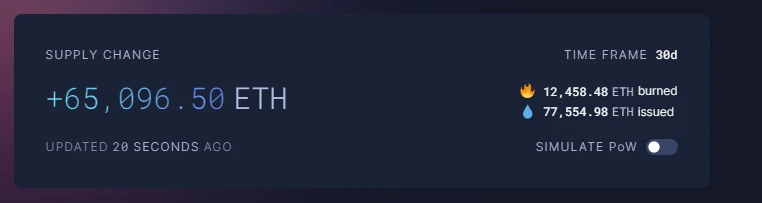

However, Ethereum’s identity crisis extends beyond Vitalik’s comments on DeFi and goes to core issues of value accumulation and network economics. Ethereum’s gas fees have remained low over the past few months, ranging between 2-4 gwei — no longer the deflationary $ETH scenario seen on ultrasound.money in the past. This situation has led to an increase in Ethereum’s supply, challenging the “ultrasound money” theory that was popular during the last bull cycle. Introduced in August 2021, EIP-1559 aims to deflate Ethereum by burning transaction fees. However, in the current low-fee environment, coupled with the emergence of a large (potentially excessive and growing) number of Layer 2s, it has not been as effective as expected, resulting in net inflation rather than the expected deflation.

Ethereum’s focus on Layer-2 solutions and the upcoming ईआईपी-4844 upgrade complicates the issue. Venture capitalist and Solana supporter Kyle Samani believes this strategy is problematic. He notes that Layer 2 could act like a parasite, sucking value away from the main Ethereum network. Samani believes Ethereum’s decision to outsource the execution of transactions and smart contracts to these Layer-2 networks is “terribly bad.” He notes that the main value of a blockchain network comes from MEV (miner extractable value, the profit that validators make by reordering transactions), and Ethereum may have given up on this because of its Layer 2-centric roadmap. This view was first proposed by his Multicoin partner Tushar Jain, who proposed a MEV-based asset ledger valuation framework about two years ago. Multiple Layer 2s lead to fragmentation of liquidity and user activity, creating a poor user experience, which is in stark contrast to a Layer 1 chain like Solana. Samani believes that this fragmentation is a big reason for Ethereum’s recent poor performance and poses a challenge to its future growth and adoption.

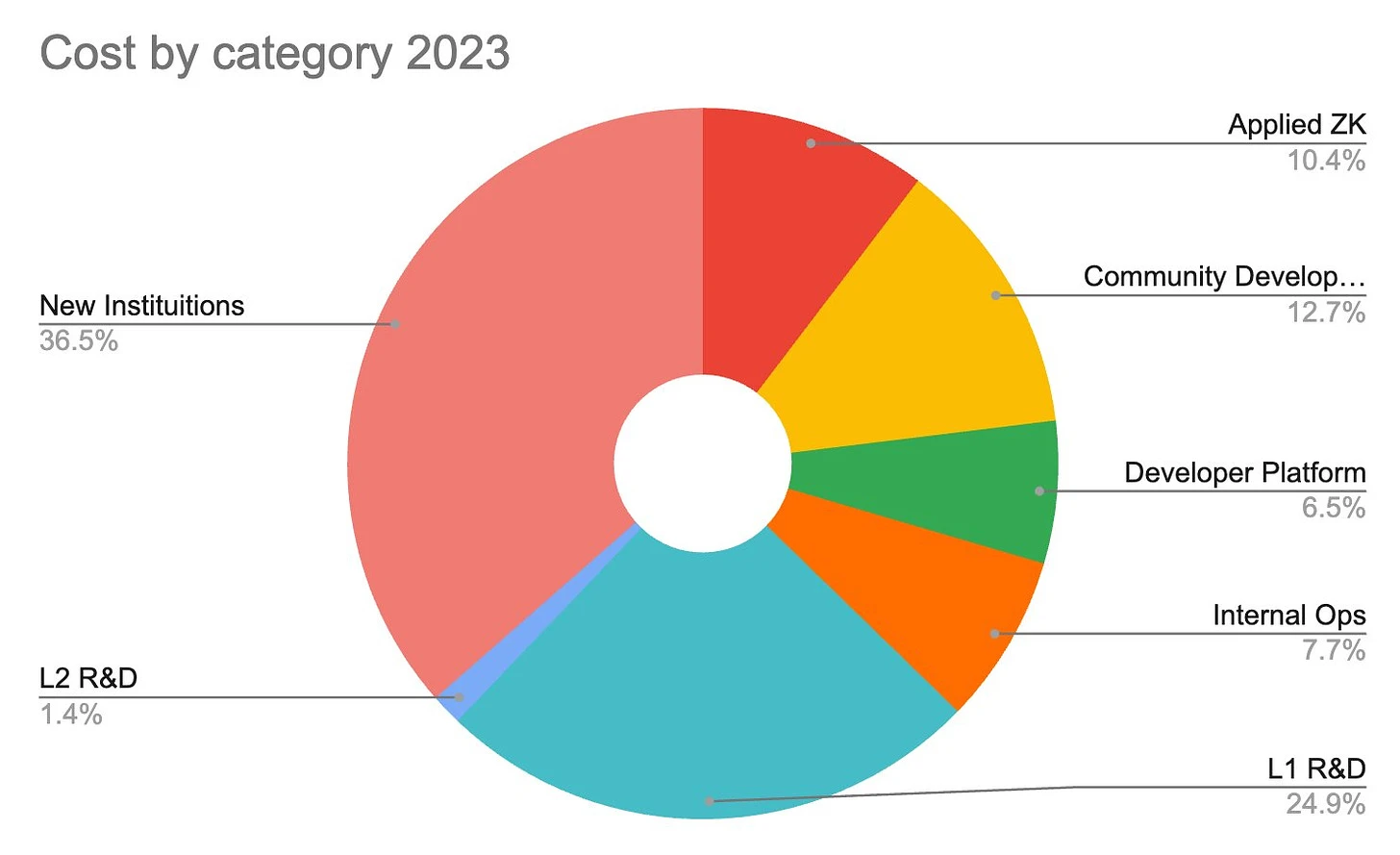

The discussion was intensified by the revelation that the Ethereum Foundation has an annual budget of approximately $100 million. This has sparked controversy over resource allocation and transparency within the ecosystem. Supporters argue that Ethereum’s size and influence justify such an investment of funds, but others question whether it is an efficient use of resources. The Foundation’s decision to sell large amounts of $ETH on exchanges such as Kraken has raised concerns because selling $ETH even during a market downturn has exacerbated selling pressure in the market.

Here are the Ethereum Foundation’s spending costs by category in 2023:

हाल ही में Steady Lads podcast , Justin Bram mentioned that the decision-making power of the Ethereum Foundation is mainly concentrated in the hands of three people, including Vitalik Buterin, a core member, and a hired regulatory expert. This organizational structure raises concerns about transparency and accountability. As the crypto industry continues to mature, people are increasingly looking to foundations and other centralized institutions to clearly explain the allocation of their financial resources. This demand for transparency also involves the governance structure, the decision-making process, and how these align with the overall goals of the platform.

Despite the challenges facing Ethereum and the entire DeFi ecosystem, a potential direction of development is emerging. The key question now is: what will drive the next wave of cryptocurrency adoption, potentially enabling it to achieve 10-100x growth? While Vitaliks concerns about the sustainability of DeFi are worth taking seriously, this does not negate the potential of blockchain technology in the financial sector. The answer may not lie in improving the existing DeFi model or perpetuating the current speculative cycle, but in a more fundamental shift: the tokenization of traditional financial assets or RWAs. This is the largest untapped market for cryptocurrency, with the potential to bring trillions of dollars of capital to the blockchain. This shift may alleviate some of Vitaliks concerns about the circularity of DeFi by introducing a large number of real world assets.

Consider the sheer size of traditional financial markets: BlackRock alone manages nearly five times the assets of the entire crypto market. By tokenizing assets such as bank deposits, commercial paper, treasuries, mutual funds, money market funds, stocks, and derivatives, we can bring unprecedented capital inflows to the crypto ecosystem. This capital can be integrated into the DeFi infrastructure that has already demonstrated its utility in creating more transparent, accessible, and liquid markets. This tokenization potential aligns with Larry Fink’s views on Ethereum and could create a fascinating future for the platform.

As Ethereum continues to mature, the platform is at a critical juncture of innovation and widespread adoption. The discussion around the future direction of Ethereum – whether to continue to focus on DeFi or expand into other application areas – will determine its technological development, market position, and regulatory strategy. Although Vitalik is skeptical of the current DeFi model, this may drive the ecosystem to evolve towards more sustainable and innovative solutions. At the same time, the tokenization of traditional assets has great potential, which may enable Ethereum to take a leading position in the on-chain financial market.

It is critical to maintain a balance of attention to the present while focusing on the future. Financial derivatives emerged to manage risk and speculate on real assets, such as commodities, commodity contracts, and corporate shares. However, cryptocurrencies have almost directly entered the derivatives stage without sufficient underlying assets. This is not the fault of the industry itself, as regulatory issues have hindered the tokenization of many important real-world assets (RWAs). Many of the top crypto assets actually represent a platform for trading and speculation, and the assets traded are themselves highly speculative.

Cryptocurrency is not alone: how many of the most valuable U.S. companies pay dividends? Dividends were once a core attraction for companies going public, but have mostly been replaced by strategies like the greater fool theory. Even gold is highly speculative by nature, as its actual use in semiconductors and other devices is minimal relative to its market value. Therefore, speculation plays a significant role in the market, especially in an inflationary fiat currency regime. No matter how you look at it, $ETHs recent price performance can only be described as disappointing. This is not only true in the cryptocurrency space, but a variety of large-cap U.S. stocks have also outperformed Ethereum in recent years.

Not only that, but some critics point out that more and more protocols like DePIN are choosing to build on Solana and other blockchains instead of Ethereum. As mentioned before, BlackRock has made clear its intention to use Ethereum; but whether other traditional financial institutions will also choose Ethereum over other blockchains, and whether these values can truly and effectively accumulate on $ETH, remains to be seen.

Criticism is sometimes just the motivation that a protocol, company, community, or foundation needs. With the regulatory environment likely to be gradually relaxed, coupled with some interesting new developments in the RWA and DePIN fields, those who look forward to a more real DeFi ecosystem may get what they want, and hopefully that day will come sooner rather than later.

This article is sourced from the internet: DeFi is declining, the market is being eaten away by L2, where is the cure for Ethereum?

Original author | The Decentralised.co Compiled by Nan Zhi ( @Assassin_Malvo ) In the nineteenth episode of The Decentralised.co’s Podcast “ Building on First Principles ”, hosts Joel and Saurabh discussed with Pacman, the founder of Blur and Blast, the origins of Blur and Blast, Pacman’s judgment and analysis methods on the market and products, and Pacman’s judgment on the crypto market cycle. Odaily Planet Daily will compile the key parts of this article. In order to control the length and ensure the reading experience, half of the content has been deleted. Interested readers can listen to the full content in the original podcast . Viewpoint Overview The problem with OpenSea and other NFT markets is that they position their customers as consumers, and they really think that NFT is…