Task

Ranking

已登录

Bee登录

Twitter 授权

TG 授权

Discord 授权

去签到

下一页

关闭

获取登录状态

My XP

0

Original author: Cycle Capital Market Hot Topics Review

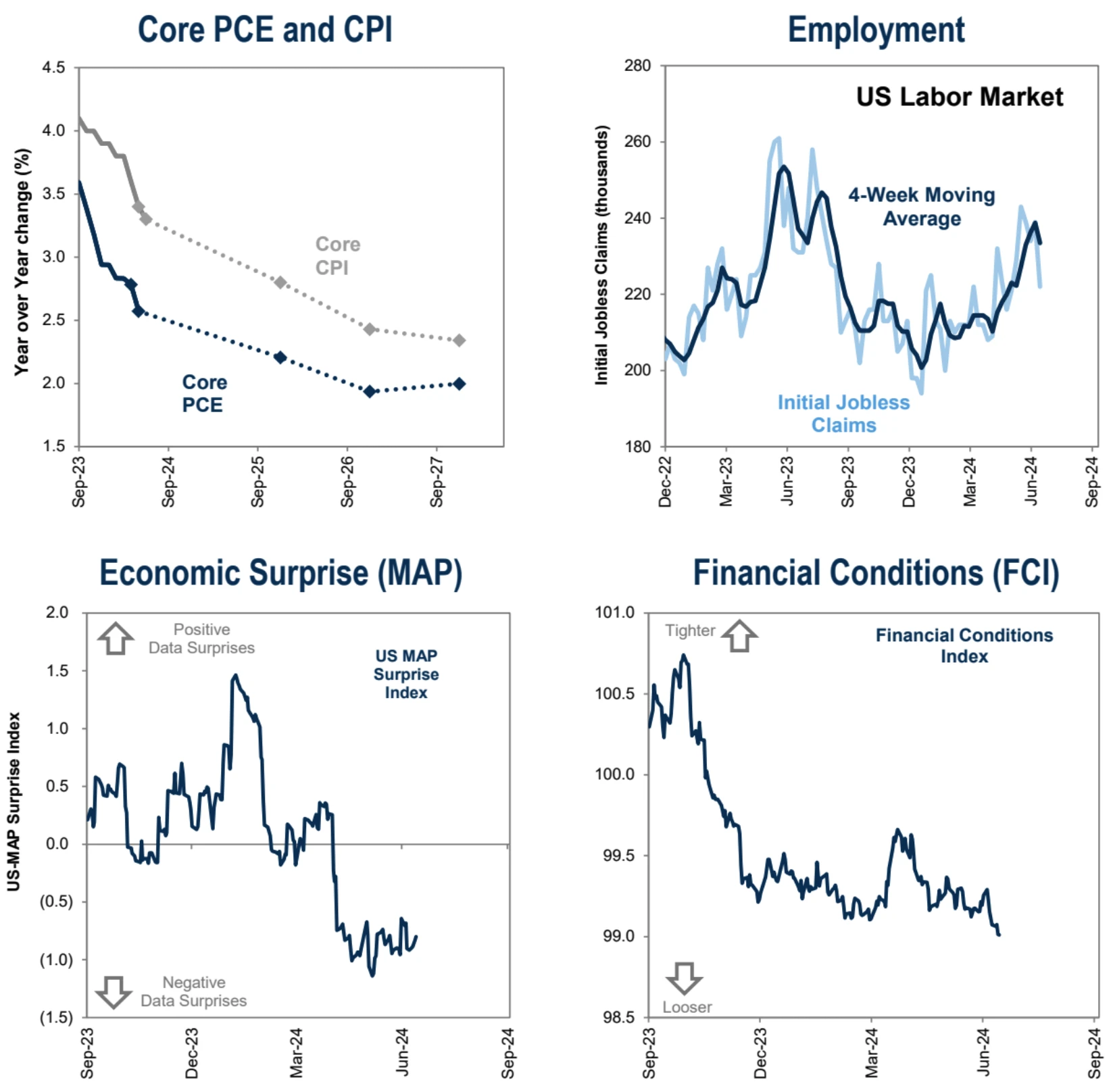

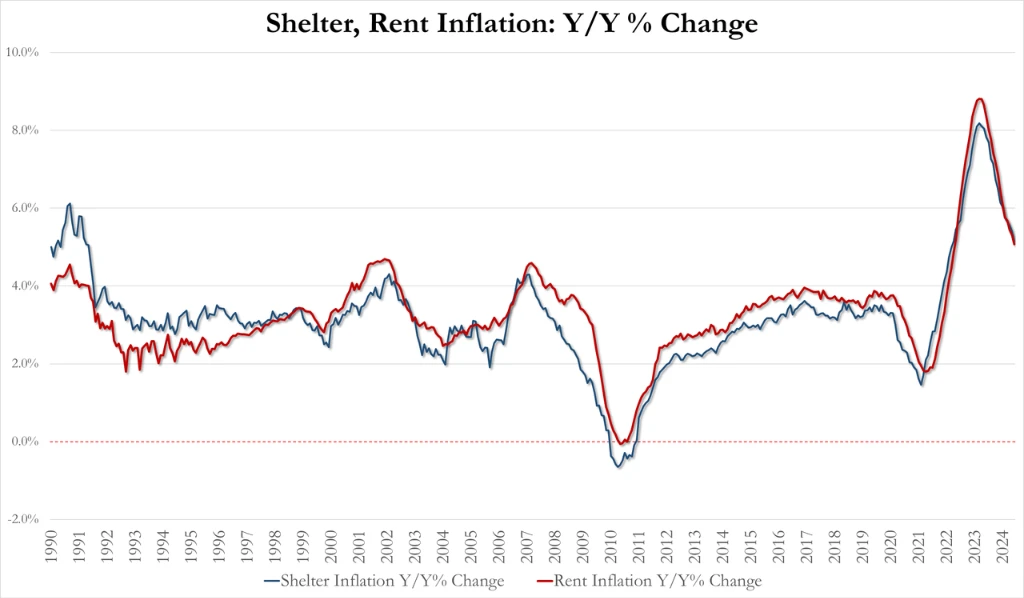

Inflation is cooling down across the board: In the past two months, it has shown a clear downward trend. The US CPI in June turned negative for the first time in four years, and the core year-on-year growth rate hit a three-year low. According to GS forecasts, both will be in a downward channel in the next two years. Housing inflation is slowing down at an accelerated pace.

Job market: The 4-week moving average of initial unemployment claims has risen by about 10% since April, indicating that the job market has weakened slightly, but is still in a relatively balanced and stable state overall.

Economic Surprise Index: It has been at a low point in the past two months, indicating that recent economic data are often lower than expected.

Financial Conditions Index: Shows a continued easing trend, the loosest since the end of 2022.

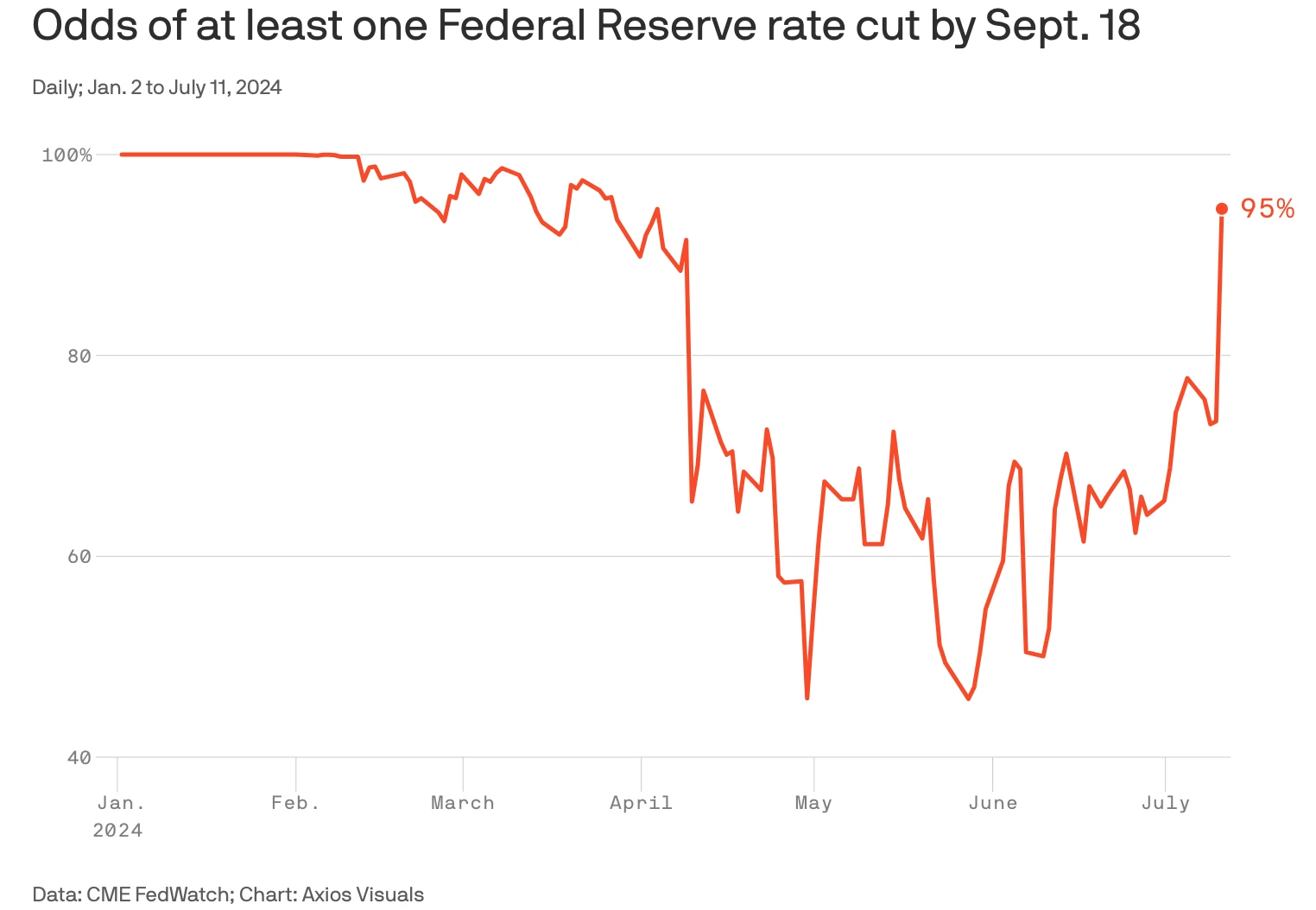

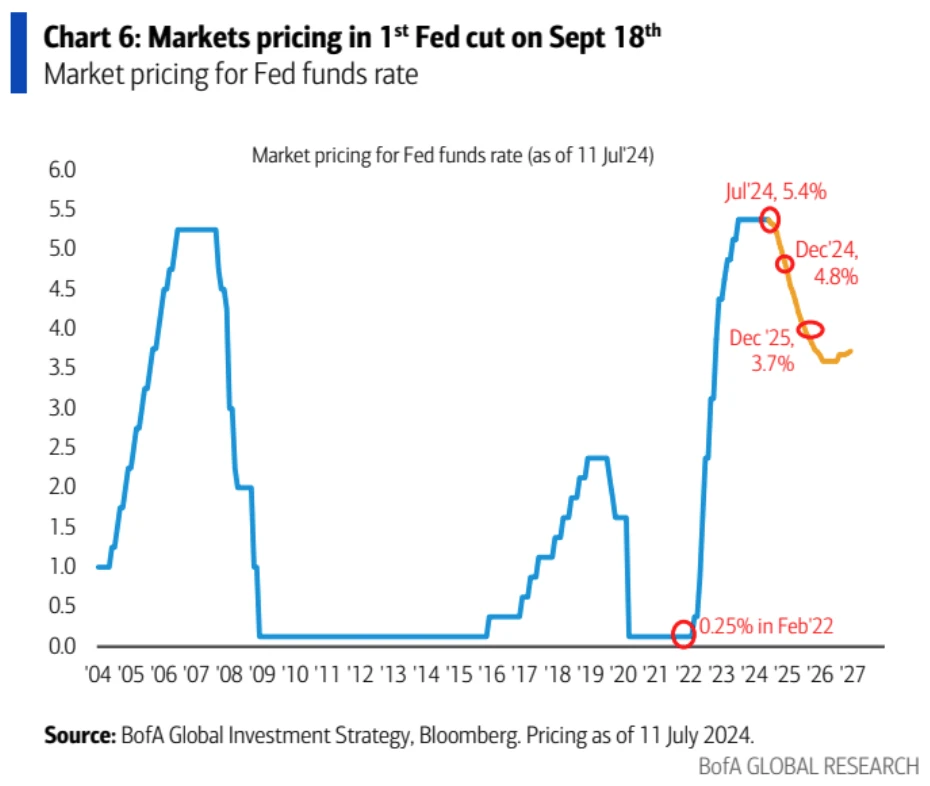

The above background can be said to be a favorite situation for risk asset markets, as investors expect the Federal Reserve to take action to support economic expansion. As time goes by, concerns about inflation at the end of the first quarter have proved to be excessive. Although service industry inflation is still above the central banks target level, commodity inflation has fallen significantly.

As the dollar weakens and the Fed begins to cut rates, emerging markets and cryptocurrencies could benefit, in the absence of a recession. If expectations of a soft landing subsequently turn to a hard landing, there will be a rapid rotation from risky assets such as equities to bonds.

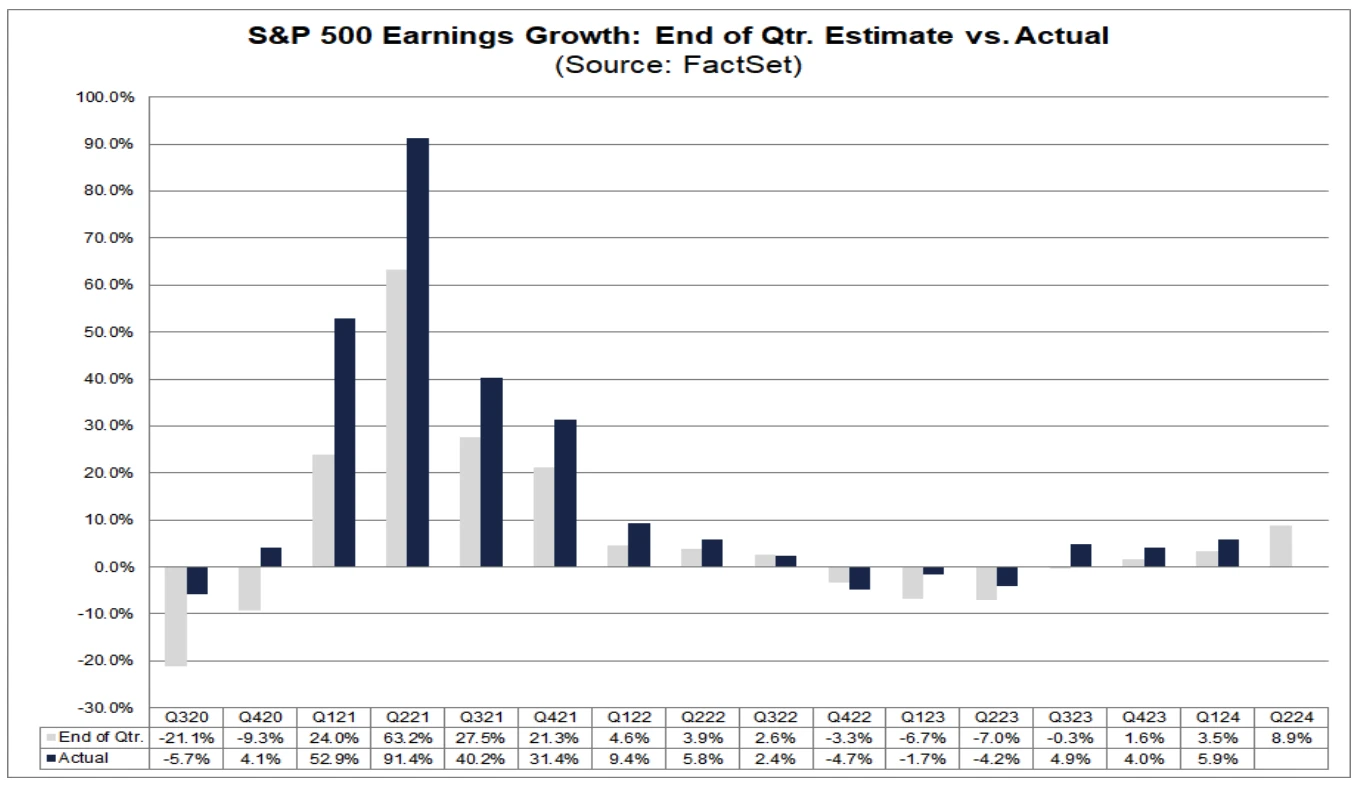

The current market focus is on the earnings season that has already begun. Market expectations for the season are very optimistic, and it may be difficult to achieve the previous level of surprise. Therefore, it is very likely to see some earnings realization or sector switching during the announcement process this season.

Wall Street expects SP 500 earnings to grow 8.9% year-on-year in Q2, which is significantly higher than the 5.9% in the previous quarter. The last time there was such a high earnings growth was in Q1 2022, when the Fed just started to raise interest rates. At that time, the earnings growth rate was 9.4%. It is worth mentioning that the 8.8% earnings expectation is still the result of a downward adjustment. At the end of March, analysts generally expected earnings growth to be 9.1%.

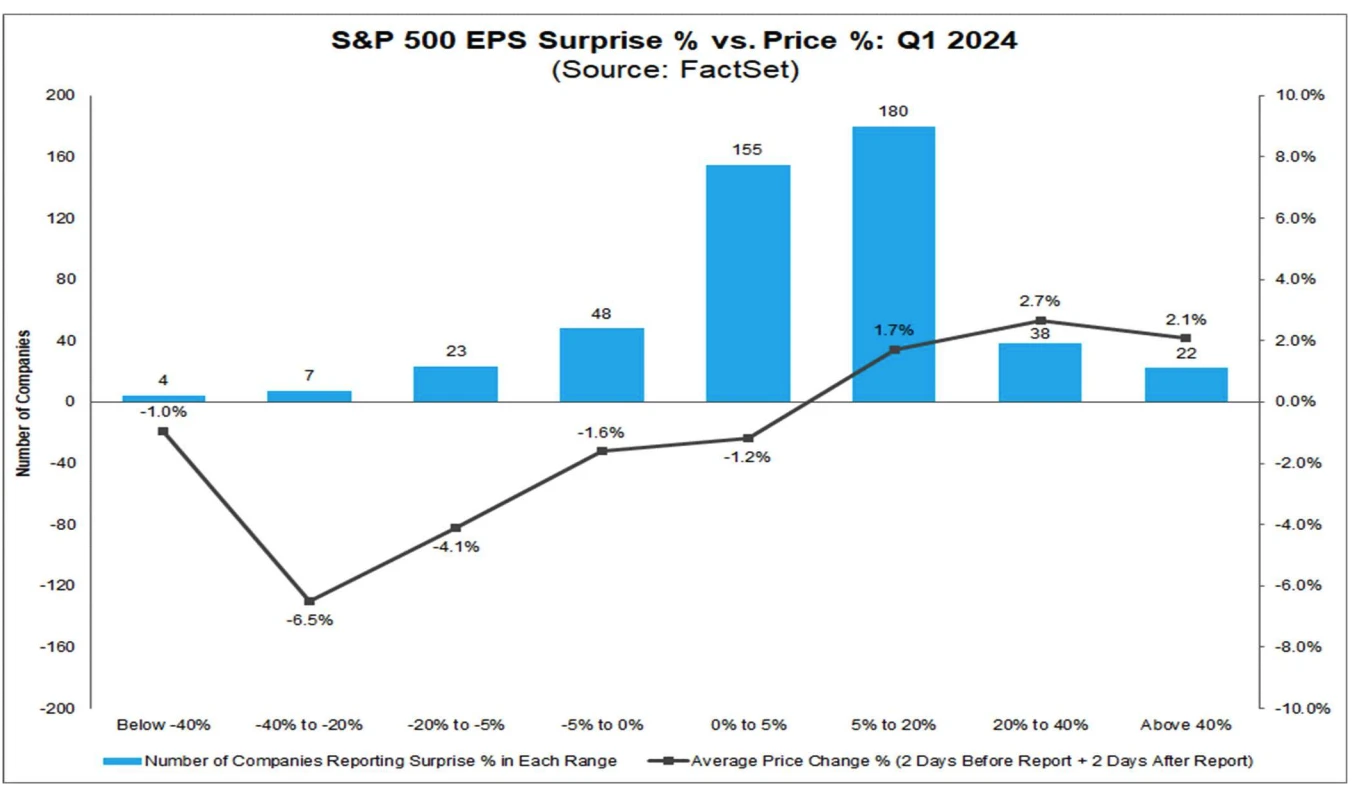

In addition, judging from the short-term market reaction in the first quarter, it is very obvious that the increase in good surprises is not as large as the decrease in bad surprises – the average increase in stock prices of companies with positive EPS surprises is slightly lower than the five-year average. The average decrease in stock prices of companies with negative EPS surprises is slightly larger than the five-year average.

From the performance in the first quarter we can see:

In the range of EPS surprises “less than -40%”, the average stock price change was -6.5%.

In the range of EPS surprises between 0% and 5%, the average stock price change was -1.2%.

In the range of EPS surprises of “5% to 20%”, the average stock price change was 1.7%.

In the range of “20% to 40%” EPS surprise, the average stock price change was 2.7%.

Judging from the market reaction to the second quarter results that have been released, which are mainly financial stocks, the results are even worse than those in the first quarter:

Recently, there have been more and more discussions in the market questioning the profitability of AI. For example, Goldman Sachs recently released a report titled Generative AI: Too Much Cost, Little Benefit? , in which many experts expressed deep skepticism about the economic potential of generative AI. This is the most pessimistic report on AI that I have seen in the past year or so, and it is worth savoring carefully.

Therefore, as big tech stocks come out of the trough of performance in 2022, the possibility that hardware companies such as Nvidia or Tesla will remain strong after the financial report is getting lower and lower. The better result is that the sector switches from Mag 7 to the 493 (NDX lagged behind R2K by 6.3% last week, one of the worst relative performances in the past decade), or the focus of hype can be switched from AI to branch tracks, including humanoid robots and autonomous driving.

From the perspective of the consumer market, the market for humanoid robots obviously has huge prospects, even higher than AI, because it is difficult for end consumers to pay more for AI, at least in the foreseeable future. Robots are different. They may become a must-have item that every family needs to purchase. Now they are just waiting for the iPhone moment to appear.

According to Goldman Sachs statistics, investors current interest in big technology is ranked as follows: NVDA > AMZN > MSFT > AAPL > GOOGL > META.

Last week, Boeing agreed to plead guilty in two criminal cases involving the 737 Max. The background of the two cases was that two Boeing 737 MAX 8 passenger planes crashed in Indonesia and Ethiopia in October 2018 and March 2019, respectively, killing a total of 346 people. The investigation pointed out that the cause of the accident was related to the safety design loopholes of the new software system in this model. Boeing deliberately concealed this risk when applying for trial certification from the Federal Aviation Administration, and did not strengthen pilot training, which led to the air crash. According to court documents filed late on Sunday, Boeing formally admitted that it had deliberately concealed safety risks in the process of applying for FAA certification for the Max model, and was guilty of conspiracy to defraud the US government, and the company was willing to be punished.

Boeing will face a fine of up to $487.2 million, but this is the maximum fine allowed by law, and the actual amount will be determined by the judge. Since Boeing reached a deferred prosecution agreement with the Department of Justice in 2021, paid a criminal fine of $243.6 million, and compensated the victims families for $500 million, this time it needs to pay a second criminal fine of $244 million. After this incident, the company was also required to spend a lot of money to rectify its internal compliance and safety requirements, requiring at least $455 million in three years, and will also be subject to three years of supervision by independent compliance supervisors. Obviously, such a punishment has made many people dissatisfied. Many people say that 244 million is equal to the value of two 737 max for a company as large as Boeing, and a life is only worth 700,000. From a strategic point of view, the manufacturing of large aircraft in the world is basically monopolized by Boeing and Airbus. Obviously, the United States will not make Boeing too miserable.

However, from an investment perspective, this means that Boeings negative news has been exhausted, which is a good thing for the recovery of valuation. This situation is somewhat similar to Binances guilty plea and fine in November 2023, after which BNB soared from $200 to a maximum of $720.

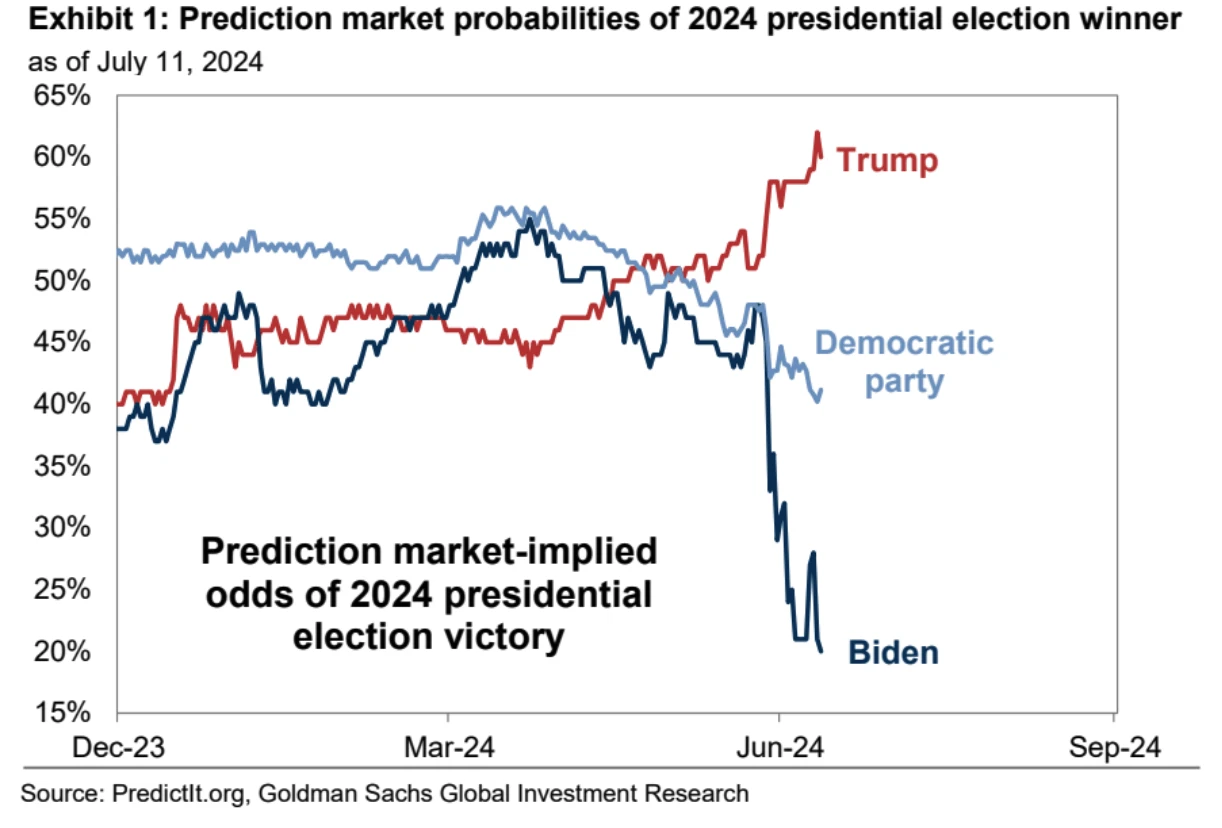

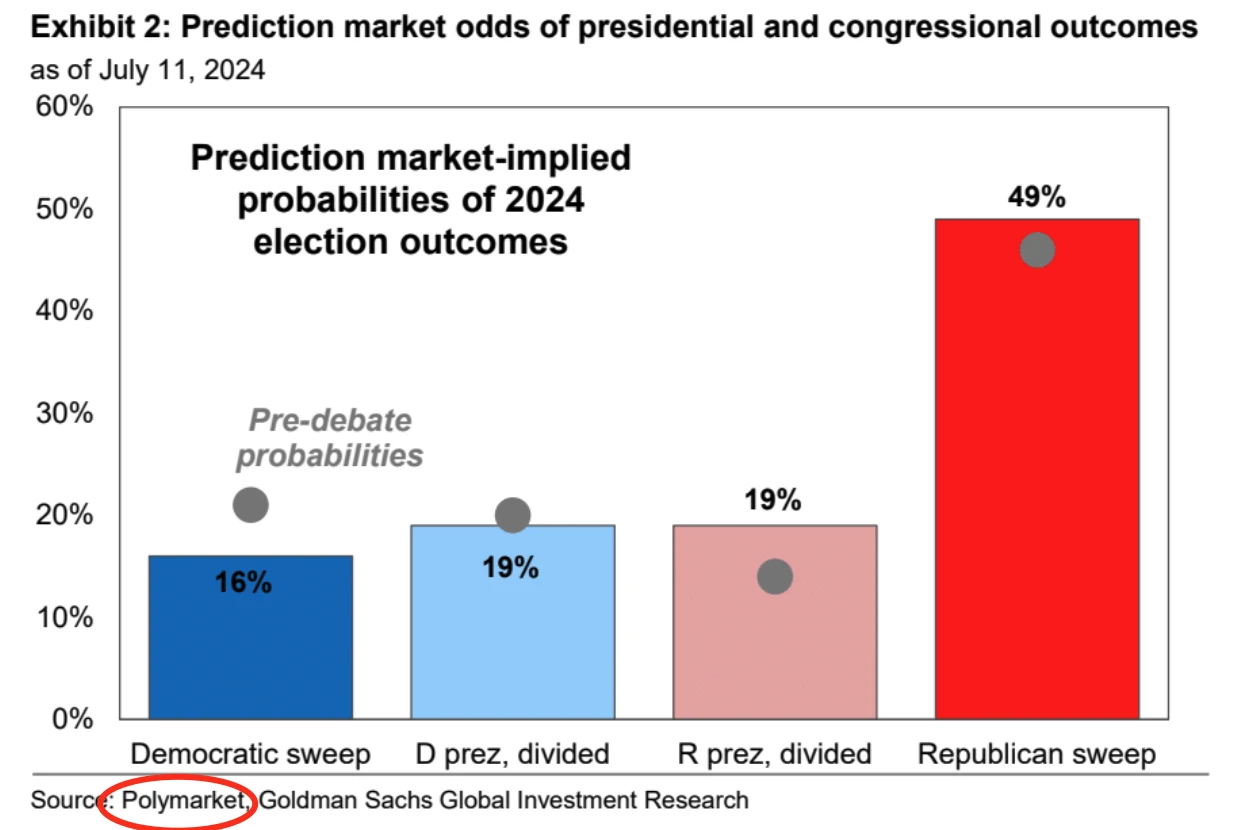

The derivatives market is now very pessimistic about Biden. After the June 27 debate, the prediction market probability of Trumps victory jumped from 40%-50% at the beginning of the year to about 60%. The probability of the Republicans taking both houses of Congress and the presidency (sweep) has also increased, and is currently about 50%. The probability of Bidens victory has fallen below 20%:

It is worth noting that Goldman Sachs cited data from the cryptocurrency prediction platform Polymarket, which is a reflection of the fact that crypto applications are gradually becoming more practical.

Next points:

As expectations of a rate cut by the Federal Reserve stabilize, institutional investors focus is shifting from growth and monetary policy to politics.

The focus is on the changing likelihood of Trump taking office, with investors questions focused on the tariffs, domestic tax policies and regulatory changes that the Trump administration may implement.

After Trump took office, the substantial increase in tariffs is expected to benefit companies that focus on the domestic market rather than those with international operations. Tariffs are expected to slightly drag on US GDP growth, and the impact on Chinese import prices may also push up inflation (which is the opposite of the environment the Fed wants to cut interest rates). The following figure shows that the markets inflation expectations and Trumps chances of winning have recently been on a synchronous upward trend, and may be further linked in the future:

Markets have been less volatile recently with politics and appear to be underestimating the uncertainty surrounding the U.S. election, with the likelihood of a Republican victory high but the possibility of a change in the Democratic ticket also rising rapidly.

Business equipment investment has stalled, and companies may delay projects because of concerns about policy changes from the new administration, such as approvals for oil and gas exploration permits or foreign battery manufacturing plants. Such political uncertainty makes companies more cautious about investing.

(As shown above, despite the strong economic performance, record stock and corporate profits, business equipment investment (in real terms) is below 2019 levels. Although non-residential fixed investment, including structures and intellectual property, has performed better, it is still 8 percentage points below the pre-pandemic trend. The main improvement is due to the governments $1 trillion support through the Semiconductor Incentive Production Act (CHIPS) and the Inflation Reduction Act (IRA).)

A Republican sweep could lead to an extension of tax cuts and increased fiscal spending, although the details have yet to be determined, which would be the most immediate positive for stocks.

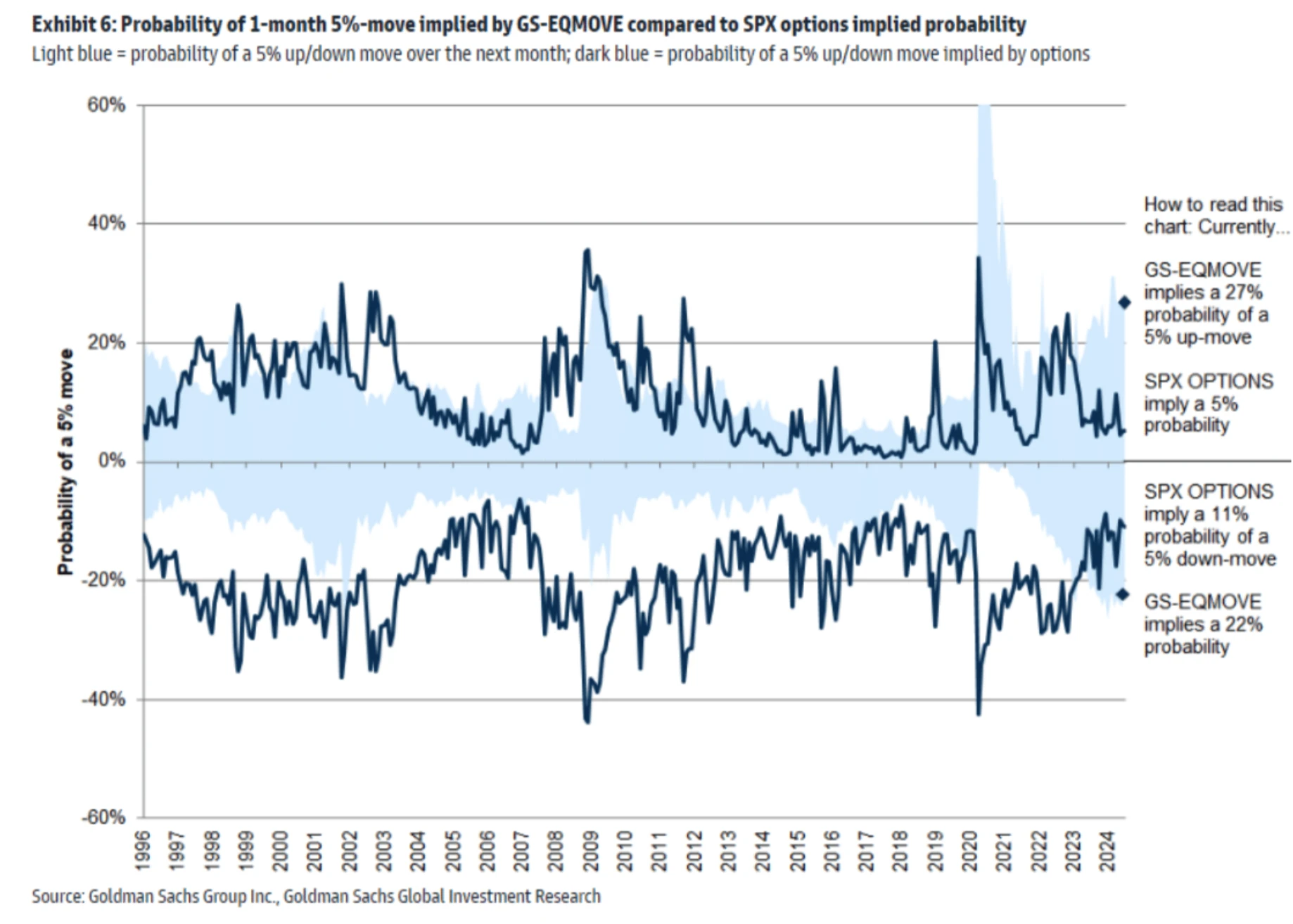

Implied upside and downside volatility in the SPX options market is low:

Renewable Energy and Environmental Policies: If Trump is re-elected, it is expected that there will be some relaxation in environmental policies, which may be beneficial to traditional energy stocks but may be a pressure on renewable energy stocks.

Technology and Big Data: The technology industry may face less stringent antitrust scrutiny under the Trump administration, and large technology companies in particular may benefit from it.

Investment style and market strategy

Growth vs. Value: In the current market environment, growth stocks are likely to continue to attract investors attention, especially in the technology and consumer sectors. However, depending on specific policy changes, value stocks in certain sectors, such as financials and industrials, may also be attractive.

Interest rate sensitive stocks: Given possible changes in economic policies and interest rates, this category of stocks may show significant volatility due to their high sensitivity to interest rate changes.

China is in a deflationary state, and policy measures have also increased excess capacity. As the worlds largest commodity exporter, it is exporting deflation. Its spillover effect contributed to a drop in core commodity inflation by about 0.5 percentage points, and reduced core inflation in Europe and the United States by about 0.1 percentage points. Although the overall effect is mild, it can give the European and American central banks more room to cut interest rates this year, which is good for stocks and crypto

The following figure clearly shows that China has a significant market share in several key export products. In addition to the traditional manufacturing sector, such as home appliances (59%), clothing and textiles (38%) and furniture (33%), Chinas manufacturing capabilities and technical level in high-tech fields have been significantly improved, with market shares in lithium-ion batteries and photosensitive semiconductors (cameras, solar energy) reaching 51% and 53% respectively. :

China has adopted an investment-driven economic growth model for many years, which can quickly increase production capacity and economic output in the short term. The figure below shows that Chinas fixed capital investment accounts for a significantly higher proportion of GDP than consumer spending. This shows that a large amount of money is invested in building new factories, purchasing equipment, and expanding production lines. This model may exceed the growth rate of market demand.

Despite the rapid expansion of China’s production capacity, the global economic slowdown, especially after the global financial crisis, has led to the failure of global demand to grow in tandem, resulting in a large amount of production capacity in China being underutilized, further exacerbating the overcapacity situation.

Capital intensity is particularly high in industries such as steel, coal, chemicals and real estate. These industries are expanding particularly rapidly, but are also most prone to oversupply.

The following figure shows that Chinas capital expenditure level is nearly 10 percentage points higher than other major economies. In US dollars, it is more than 85% higher than that of the United States and the eurozone. Policy-driven overinvestment can easily lead to inefficient resource allocation, with funds and resources being invested in inefficient or even ineffective production areas, while these resources could have been used in more productive industries or fields. In the long run, this inefficient resource allocation will drag down the overall growth potential of the economy.

Morgan Stanley Chinas PPI is not expected to end deflation until the second half of 2025.

The U.S. interest rate market has shown a high sensitivity to inflation surprises this year, with the 10-year Treasury yield fluctuating by 80 basis points in the three days before and after the CPI release.

Although the market is confident that inflation will cool down in the second half of 2023, the unexpected increase in inflation has shaken this confidence, leading to a strong market reaction. The following figure shows that after the second half of 2023, the markets reaction to expectations of cooling inflation is flat, but the unexpected reaction to rising inflation is sharp:

The markets sharp reaction to rising inflation may be due to excessive focus on short-term data, ignoring seasonal factors, the breadth of inflation, long-term trends, and actual economic fundamentals. In addition, expectations of central bank policy adjustments may also be over-inflated. Taking all these factors into consideration, the markets reaction appears to be not entirely reasonable, and the deflationary impact from China will put downward pressure on the US core CPI, and this trend is expected to continue in the future.

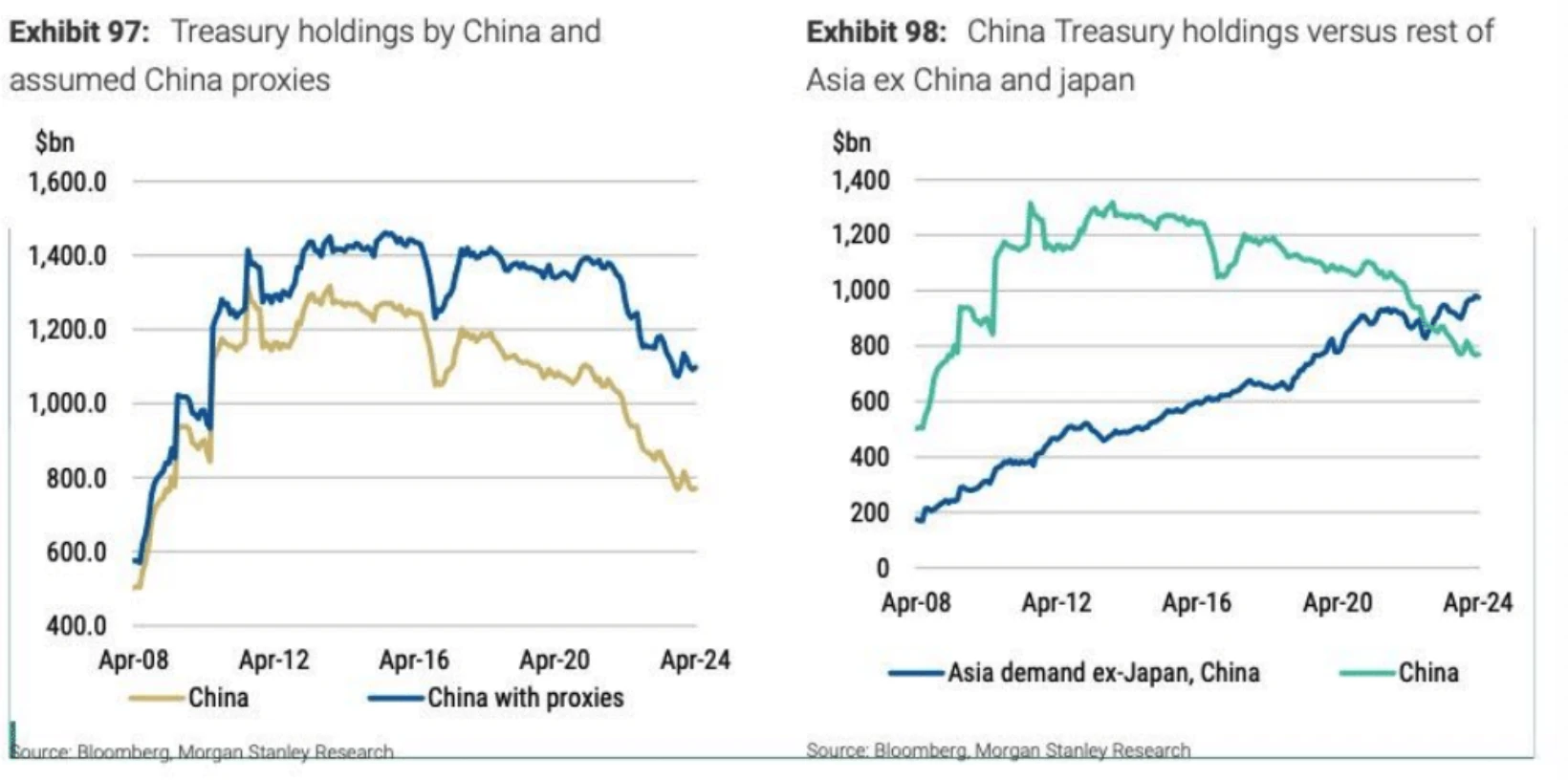

Even as China’s share of the U.S. market has fallen, the dollar value of its net exports has risen, so growth in Chinese exports is likely to increase its demand for U.S. debt, not decrease it.

Figure 97 shows that the amount of US debt held by China and its proxies has declined, but not as sharply as expected. Figure 98 shows that the demand for US debt in other Asian countries, except China, has been growing, partially offsetting the decline in Chinese demand.

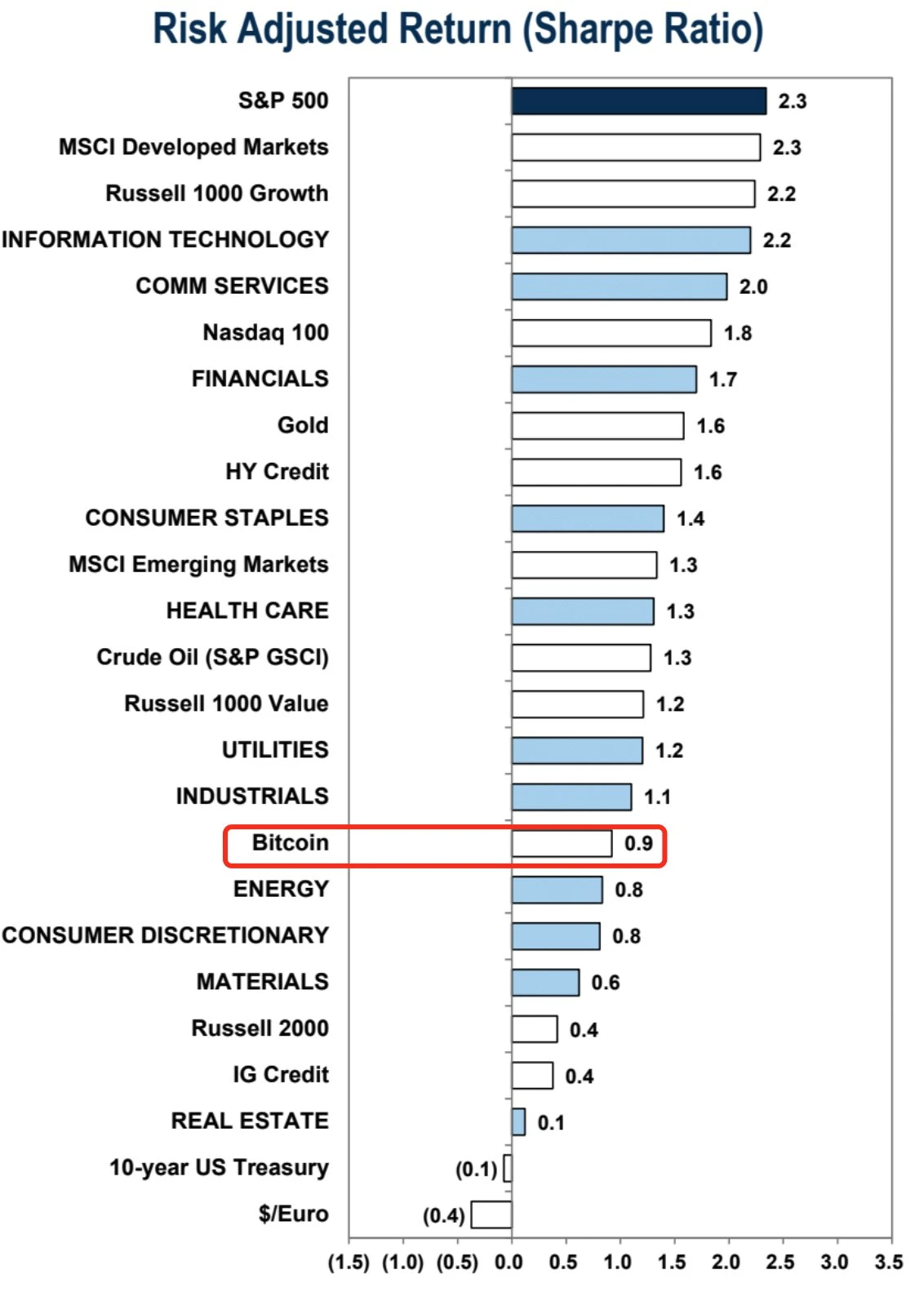

If we take the sample from the beginning of the year to date, the risk-return ratio of BTC is much lower than that of US stocks, which is rare in history. This is mainly due to the unexpected sharp drop in the past month. In early June, the sharpe of BTC YTD was 1.8, higher than that of SSX at 1.7.

Historically, some economic indicators have been seen as reliable signals for predicting recessions, but in this cycle, those rules seem to be breaking down. For example:

Yield curve inversion: The two-year and 10-year Treasury yield curve has inverted for two years, which is traditionally seen as a precursor to a recession, but the U.S. economy has not yet fallen into recession.

Money Supply (M2): M2 fell sharply at the end of 2022, which usually indicates a downturn, but the economy remains solid.

ISM Index: Although the ISM Index has been negative for 19 of the past 20 months, the economy is not in recession.

Sahms Rule: When the unemployment rate rises 0.5 percentage points from its low, it usually indicates a recession. Although the unemployment rate rose from 3.4% to 4.1%, it is mainly due to an increase in labor supply rather than a decrease in demand, and the current unemployment rate is still low.

The U.S. economy experienced a similar situation in the 1990s, when there were also several traditional recession signals, but the economy did not immediately fall into recession, but instead experienced a long period of expansion. This shows that similar signals in history do not always mean an immediate economic recession, and the current economic situation may be similar.

Although there has not been a boom in the RWA market, the industry has continued to make steady progress.

According to Etherscan, BlackRock BUIDL, launched less than four months ago, currently holds $502.8 million worth of tokenized Treasuries.

The milestone was achieved after RWA tokenization firm Ondo Finance purchased more BUIDL and used it as a backing asset for its OUSG token.

Crypto lending platform MakerDAO, the protocol behind the $5 billion stablecoin DAI, announced last week that it plans to invest $1 billion of its reserves in tokenized U.S. Treasury products. Top players in the space, including BlackRock’s BUIDL, Superstate, and Ondo Finance, are lining up to apply for the proposal. $1 billion represents a 55% increase in the size of the outstanding U.S. Treasury RWA tokens!

From the perspective of revenue, the conversion of 1 billion interest-bearing (4.5-5%) assets means an additional revenue of 40-50 million US dollars per year for the protocol, which accounts for nearly half of the current revenue. According to the PE valuation method, this is a clear positive. However, it is also possible to convert from existing assets at that time. If so, there will be no direct financial benefit, but only reduce the risk of underlying custody. However, this can be a key transformation for Maker to jump out of its own small circle and bind with traditional large institutions.

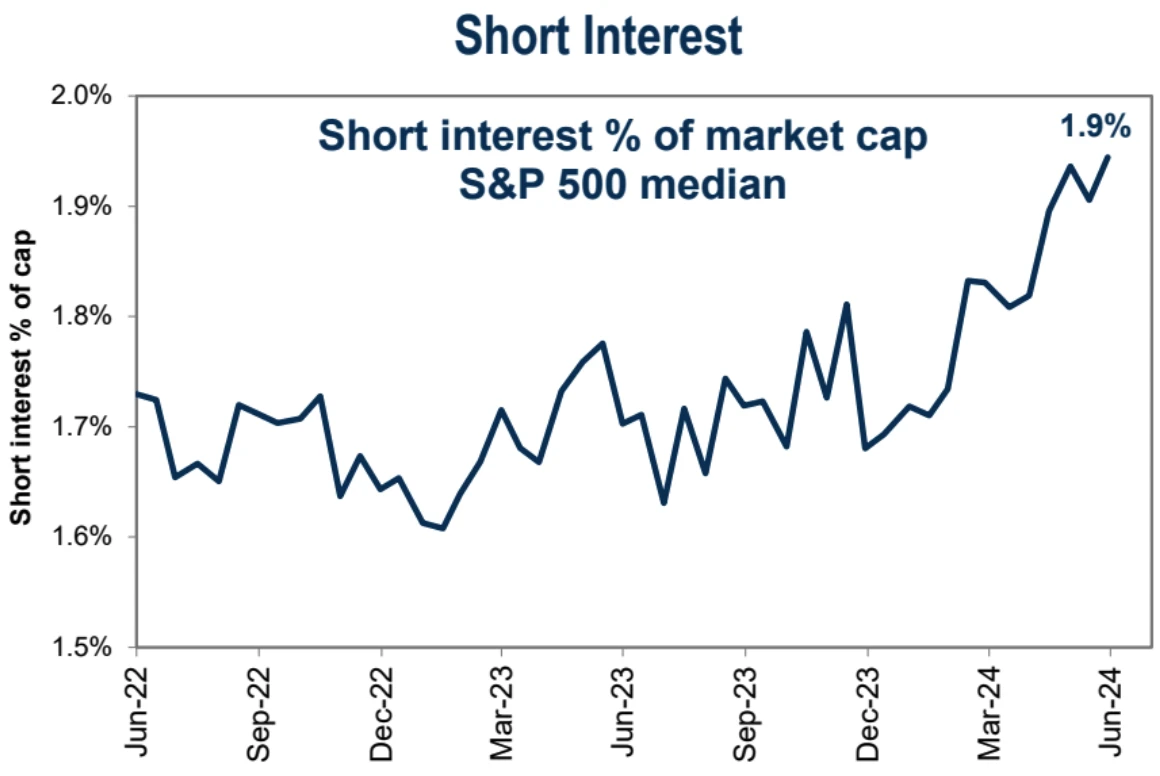

The short position ratio of US stocks rose slightly in June to a level close to the highest level in four years, but the overall level is still not high (it can reach 3-4% at high times):

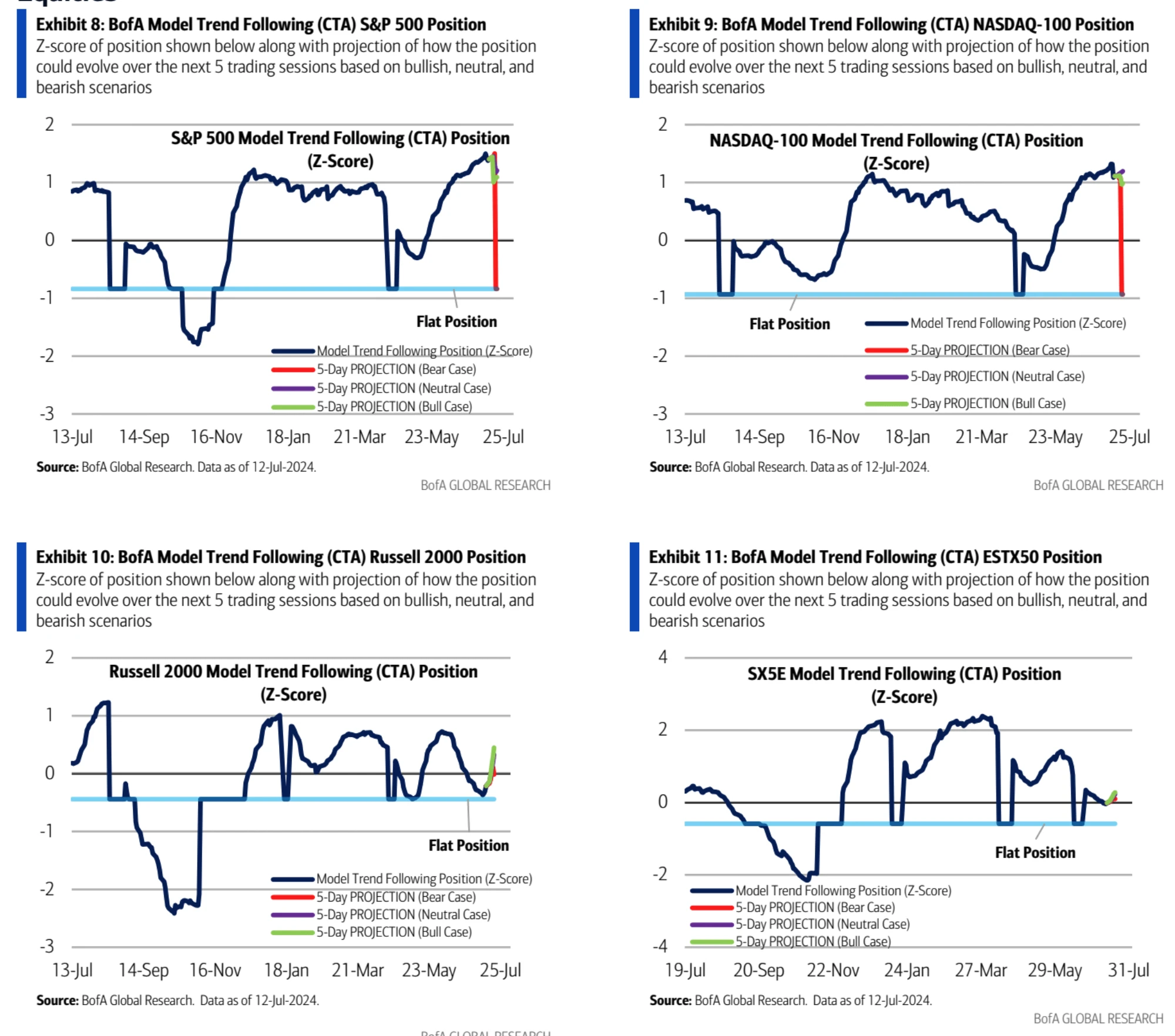

BofAs analysis of CTA positions in different stock indices and forecasts for the next five trading days show that the SP 500 position Z-score is close to 2, with a high position. The NDX Z-score is close to 1, a medium-high level, and the Russell 2000 position is relatively neutral, with a high probability of rising.

Northbound funds in the A-share market bought 15.9 billion yuan this week, hitting an 11-week high and reversing four consecutive weeks of net selling.

This article is sourced from the internet: Cycle Capital: Review of hot market topics

Original author: Steven Ehrlich, Forbes Original translation: Luffy, Foresight News Former CFTC Chairman Christopher Giancarlo is optimistic about the future of cryptocurrencies in the United States Christopher Giancarlo served as the 13th Chairman of the U.S. Commodity Futures Trading Commission (CFTC). He is also a member of the U.S. Financial Stability Oversight Council, the President’s Working Group on Financial Markets, and the Executive Committee of the International Organization of Securities Commissions. Giancarlo is also the author of CryptoDad-The Fight for the Future of Money, which tells his views on the world’s first regulated Bitcoin derivatives market and the upcoming digital network transformation of financial services. Forbes recently spoke with Christopher Giancarlo. In this interview, we discussed the current regulatory landscape for cryptocurrencies, the prospects for new crypto legislation, whether the…