My XP

0

लॉग इन करें

Original author: Crypto_Painter (X: @CryptoPainter_X)

Recently, there has been a hint of panic in the entire market, which is largely related to the huge short positions of CME. As an old investor in the cryptocurrency circle, I vaguely remember that when CME officially launched BTC futures trading, it just ended the epic bull market in 2017!

Therefore, it is of great significance to study these huge short orders on CME!

First, some background:

CME refers to the Chicago Mercantile Exchange, which launched BTC futures trading at the end of 2017 with the commodity code: [BTC 1!]. Subsequently, a large number of Wall Street institutional capital and professional traders entered the BTC market, dealing a heavy blow to the ongoing bull market, causing BTC to enter a 4-year bear market.

As more and more traditional funds enter the BTC market, institutional traders (hedge funds) and professional traders that CME mainly serves begin to participate more and more in BTC futures trading;

During this period, CMEs futures positions have been growing, and last year it successfully surpassed Binance to become the leader in the BTC futures market. As of now, CMEs total BTC futures positions have reached 150,800 BTC, equivalent to approximately US$10 billion, accounting for 28.75% of the entire BTC futures trading market.

Therefore, it is no exaggeration to say that the current BTC futures market is not controlled by traditional cryptocurrency exchanges and retail investors, but has fallen into the hands of professional institutional traders in the United States.

As more and more people have discovered recently, CMEs short positions have not only increased significantly, but have recently broken through historical highs and are still rising. As of the time I am writing this article, CMEs short positions have reached US$5.8 billion, and the trend has not shown any obvious slowdown;

Does this mean that Wall Street鈥檚 elite capital is shorting BTC on a large scale and is completely pessimistic about the future performance of BTC in this bull market?

If we just look at the data, this is indeed the case. Moreover, BTC has never experienced a situation where it has broken through a historical high in a bull market and then remained volatile for more than 3 months. All signs indicate that these big funds may be betting that this round of BTC bull market will be far less than expected.

Is this really the case?

Next, let me explain to you where these huge short positions come from, whether we should be afraid, and what impact this has on the bull market.

First, if you frequently check CME prices, you will find an interesting feature: BTC 1! The price of this futures trading pair is almost always at least a few hundred dollars higher than the Coinbase spot price. This is easy to understand because CMEs BTC futures are delivered on a monthly basis, which is equivalent to the swap contract of the month in traditional cryptocurrency exchanges.

Therefore, when market sentiment is bullish, we can see that swap contracts often have different degrees of premium. For example, the premium of the second quarter contract in a bull market is often very high.

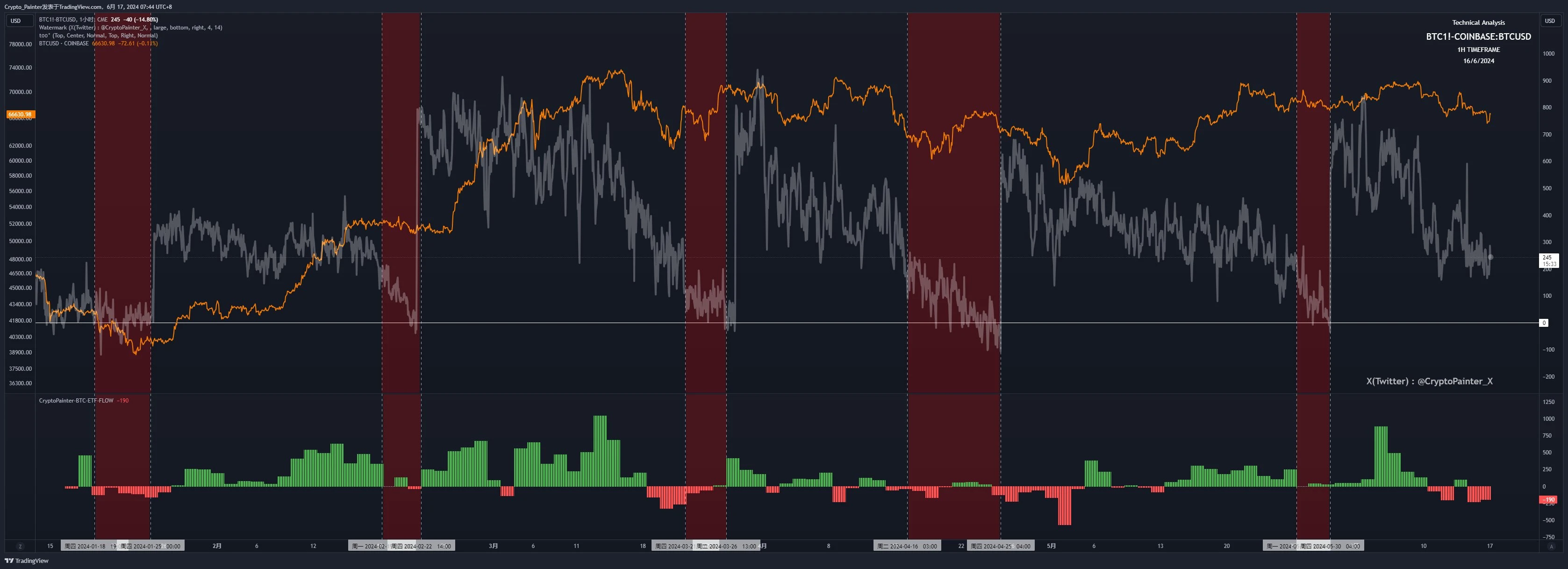

If we subtract Coinbase鈥檚 spot price from CME鈥檚 BTC futures price (they are both USD pairs), we get the following chart:

The orange curve is the trend of BTC price at the 4-hour level, while the gray curve is the premium of CME futures price relative to CB spot price;

It can be clearly seen that the CME futures premium fluctuates regularly with the monthly contract rollover (automatically moving positions to the next months contract), which is similar to the swap contract premium of traditional exchanges in the cryptocurrency circle. They will have a higher premium when the contract is generated, and when the contract is about to expire, the premium is gradually smoothed;

It is precisely because of this rule that we can carry out a certain degree of futures-spot arbitrage. For example, when the quarterly contract of the CEX exchange is generated, if the market has just experienced a period of bull market and its premium has reached 2-3%, then we can take out 2 million US dollars and buy 1 million US dollars of spot respectively, and open a 1 million US dollars short order on the quarterly contract at the same time;

During this period, no matter how the price fluctuates, the short position will hardly be liquidated. As long as the premium is gradually smoothed out before the expiration of the quarterly contract, a stable 2% return of 20,000 US dollars, or 20,000 US dollars, can be obtained without risk.

Don鈥檛 underestimate this little bit of profit. For large funds, this is a high return with almost no risk!

To do a simple calculation, CME generates a new contract once a month on average. Since 2023, its average premium has been 1.2%. Taking into account the handling fee for this operation, lets calculate it as 1%. That means a fixed 1% risk-free arbitrage opportunity every month over the course of a year.

Calculated 12 times a year, the risk-free annualized return is about 12.7%, which is already higher than the yield of most money market funds in the United States, not to mention earning interest by depositing the money in a bank.

Therefore, at present, CMEs futures contracts are a natural arbitrage venue, but there is still a problem. Futures can be opened on CME, but where can spot be bought?

CME serves professional institutions or large funds. These customers cannot open a CEX exchange account and trade like us. Most of their money also belongs to LP, so they must find a compliant and legal channel to purchase BTC spot.

What a coincidence! BTC鈥檚 spot ETF has been approved!

At this point, the closed loop is completed. Hedge funds or institutions make large purchases on US stock ETFs and open equal short orders on CME, making risk-free fixed arbitrage once a month to achieve a stable return of at least 12.7% annualized.

This set of arguments sounds very natural and reasonable, but we cannot just rely on words, we also need to verify it with data. Are institutional investors in the United States actually engaging in arbitrage through ETFs and CME?

As shown below:

I have marked on the chart the periods of extremely low CME futures premium since the ETF was approved, and the sub-chart indicator below is a bar chart of BTC spot ETF net inflows that I wrote myself;

You can clearly see that whenever the CME futures premium starts to shrink significantly and is below $200, the ETFs net inflows also decrease, while when the CME generates a new current month contract, the ETF will see a large amount of net inflows on the first Monday when the new contract starts trading.

This can explain to some extent that a considerable proportion of the ETF鈥檚 net inflows are not simply used to buy BTC, but are used to hedge the high-premium short orders that will be opened on CME.

At this time, you can turn to the top and look at the data chart that counts CME futures short positions. You will find that the time when CMEs short positions really began to soar by 50% is exactly after January 2024.

The BTC spot ETF will also officially start trading after January 2024!

Therefore, based on the above incomplete data, we can draw the following research conclusions:

1. CME鈥檚 huge short positions are likely to be used to hedge spot ETFs, so its actual net short position should be far less than the current $5.8 billion, and there is no need for us to panic because of this data;

2. ETFs have received a net inflow of $15.1 billion so far, and it is likely that a considerable portion of the funds are in a hedging state, which explains why the second-highest single-day net inflow of ETFs in history (US$886 million) in early June and the net inflow of ETFs for the entire week did not lead to a significant breakthrough in the price of BTC;

3. Although CME鈥檚 short positions are very high, they have already seen a significant increase before the ETF was approved. There was no significant liquidation during the subsequent bull market from $40,000 to $70,000. This shows that there is likely to be funds among US institutional investors that are firmly bearish on BTC, and we should not take it lightly.

4. We need to have a new understanding of the daily net inflow data of ETFs. The impact of net inflows on market prices may not necessarily be positively correlated, and there may also be a negative correlation (ETFs buy in large amounts, BTC prices fall);

5. Consider a special case. When the CME futures premium is eaten up by this group of arbitrage systems one day in the future and there is no potential arbitrage space, we will see a significant reduction in CMEs short positions, corresponding to which is a large net outflow of ETFs. If this happens, dont panic too much. This is simply liquidity withdrawing from the BTC market to look for new arbitrage opportunities.

6. The last thought is, where does the premium in the futures market come from? Is the wool really on the sheep? I may do new research on this later.

Well, the above is the summary of this research. This issue is more market research-oriented and does not provide clear directional guidance, so it cannot be of much help to trading. However, it is still very helpful for understanding market logic. After all, when I saw the huge amount of short orders on CME, I was a little scared and even recalled the long bear market from 2017 to 2018…

That bear market was much more disgusting than todays volatile market, but fortunately, at present, BTC is indeed favored by traditional capital. To put it bluntly, hedge funds are willing to come to this market for arbitrage, which is essentially a kind of recognition, although the money is paid by us retail investors, haha.

Finally, if you have any doubts about the special nature of this bull market, you can also read the discussion in the quotation below , Is this bull market more complicated than previous bull markets? It will be better to read it together with this article!

That鈥檚 all, thanks for reading!

This article is sourced from the internet: In-depth research: The subtle relationship between BTC spot ETF and CME鈥檚 huge short positions

Original | Odaily Planet Daily Author | Asher Recently, the sharp fluctuations in BTC prices have caused most altcoins to fall sharply, but TON has risen against the trend and has broken through $8 today, setting a new record high. At the same time, the token NOT of Notcoin, a popular game in the TON ecosystem, rebounded significantly after falling to $0.015, and the current price is $0.0184. If it can effectively break through the resistance level of $0.02 to $0.021, it may be expected to hit the highest price in history again. For those who missed out on Notcoin, the TON ecosystem game Pixelverse is worth paying attention to. In the following, Odaily Planet Daily will introduce the reasons why Pixelverse is worth paying attention to and share the…