Task

Ranking

已登录

Bee登录

Twitter 授权

TG 授权

Discord 授权

去签到

下一页

关闭

获取登录状态

My XP

0

क्रिप्टोकरेंसी की सामान्य गिरावट में, सीआरवी अप्रत्याशित रूप से सबसे बुरी तरह प्रभावित हुई।

आज सुबह, अरखाम ने एक पोस्ट प्रकाशित की जिसमें बताया गया कि कर्व के संस्थापक माइकल एगोरोव ने वर्तमान में 5 प्रोटोकॉल में 5 खातों पर $95.7 मिलियन स्टेबलकॉइन (मुख्य रूप से crvUSD) उधार दिए हैं, जिसमें $140 मिलियन CRV संपार्श्विक के रूप में हैं। उनमें से, माइकल ने लामालेंड पर उधार लिए गए $50 मिलियन crvUSD के लिए जिम्मेदार है, और एगोरोव के 3 खातों ने प्रोटोकॉल पर उधार लिए गए crvUSD के 90% से अधिक के लिए जिम्मेदार है।

अरखाम ने बताया कि अगर CRV की कीमत में लगभग 10% की गिरावट आती है, तो इन पदों को समाप्त किया जाना शुरू हो सकता है। इसके बाद, CRV की गिरावट का विस्तार जारी रहा, एक बार $0.26 से नीचे गिरकर, एक नए ऐतिहासिक निम्न स्तर पर पहुँच गया, और माइकल्स मल्टीपल एड्रेस पर CRV उधार देने की स्थिति धीरे-धीरे परिसमापन सीमा से नीचे गिर गई।

अतीत में, माइकल अपने आतिथ्य पद को बचाने के लिए अपनी स्थिति को छिपा लेते थे, लेकिन इस बार, ऐसा लग रहा था कि उन्होंने "हार मान ली है"।

एम्बर की निगरानी के अनुसार, माइकल एगोरोव के मुख्य पते की इनवर्स पर उधार देने की स्थिति में कुछ CRV का परिसमापन शुरू हो गया है। लुकऑनचैन की निगरानी के अनुसार, माइकल एगोरोव के पास वर्तमान में चार प्लेटफ़ॉर्म पर 111.87 मिलियन CRV (US$33.87 मिलियन) संपार्श्विक और US$20.6 मिलियन ऋण है।

सीआरवी का संकट दो महीने पहले ही उभरना शुरू हो गया था, जब माइकल की ऋण स्थिति परिसमापन सीमा से नीचे गिर गई थी, लेकिन उस समय माइकल का परिसमापन नहीं किया गया था, न ही माइकल ने कोई सुधारात्मक कार्रवाई की थी।

14 अप्रैल को, जैसे ही बाजार में गिरावट आई, CRV की कीमतें भी $0.42 पर गिर गईं, और कर्व के संस्थापक माइकल एगोरोव की उधार स्थिति फिर से लाल रेखा में प्रवेश कर गई। एम्बर्स मॉनिटरिंग के अनुसार, माइकल ने 5 पतों के माध्यम से 6 उधार प्लेटफार्मों पर कुल 371 मिलियन CRV गिरवी रखे और स्टेबलकॉइन में $92.54 मिलियन उधार दिए। 12 ऋणों में, साइलो उधार स्थिति सबसे खतरनाक है।

नवंबर 2022 से शुरू होकर, जब ऑन-चेन बिग शॉर्ट पोंजीशॉर्टर ने अपने टोकन CRV को शॉर्ट करने का प्रयास किया, जुलाई 2023 के अंत तक, वाइपर कंपाइलर विफलता के कारण कर्व पर हमला किया गया। माइकल ने अपनी स्थिति को बचाने के लिए लगातार कार्रवाई की, जिससे DeFi सूप में हलचल मच गई। लोगों ने इस कार्रवाई की श्रृंखला की तुलना DeFi रक्षा युद्ध से भी की।

पहली रक्षा लड़ाई शायद माइकल्स द्वारा शॉर्ट सेलर्स को लुभाने की कोशिश थी, जिसके कारण CRV की कीमत गिरने के बजाय बढ़ गई, और उसने शॉर्ट सेलर्स के खिलाफ लड़ाई में लाभ कमाया। दूसरी रक्षा लड़ाई OTC की शक्ति पर निर्भर थी, और हालांकि होल्डिंग्स में कमी आई, लेकिन इसने वू जिहान, डू जून, सन युचेन और अन्य शीर्ष खिलाड़ियों के साथ-साथ DWF और अन्य संस्थानों सहित शक्तिशाली समर्थकों का एक समूह प्राप्त किया। यह कहा जा सकता है कि CRV की दो रक्षा लड़ाइयाँ काफी विजयी रहीं।

संबंधित पठन: कर्व्स समस्या डीफिस यील्ड रोग का एक लक्षण है

14 अप्रैल को दोपहर में CRV की कीमत $0.42 पर गिर गई। डीबैंक डेटा के अनुसार, माइकल्स के 12 पदों में से 5 पदों का स्वास्थ्य मूल्य 1.12 या उससे भी कम था। यू जिन ने माइकल्स ऋण स्थिति की लाल रेखा की निगरानी की और परिसमापन पर अटकलें लगाने के लिए ट्वीट किया। उन्होंने बताया कि यदि CRV की कीमत बिना पुनःपूर्ति या पुनर्भुगतान के 10% तक गिरना जारी रहती है, तो परिसमापन प्रक्रिया शुरू की जाएगी।

हालाँकि, जैसे ही लोग सोच रहे थे कि CRV को तीसरे DeFi रक्षा युद्ध का जवाब कैसे देना चाहिए, कुछ दिलचस्प हुआ।

लोगों ने देखा कि उस दिन सुबह 4 बजे CRV की कीमत $0.3592 पर गिर गई, जो पहले ही $0.42 के 10% से नीचे गिर चुकी थी। हालाँकि, माइकल की ऋण स्थिति को समाप्त नहीं किया गया था जैसा कि यू जिन ने कहा था, और यहाँ तक कि माइकल ने खुद भी कोई सुधारात्मक उपाय नहीं किया।

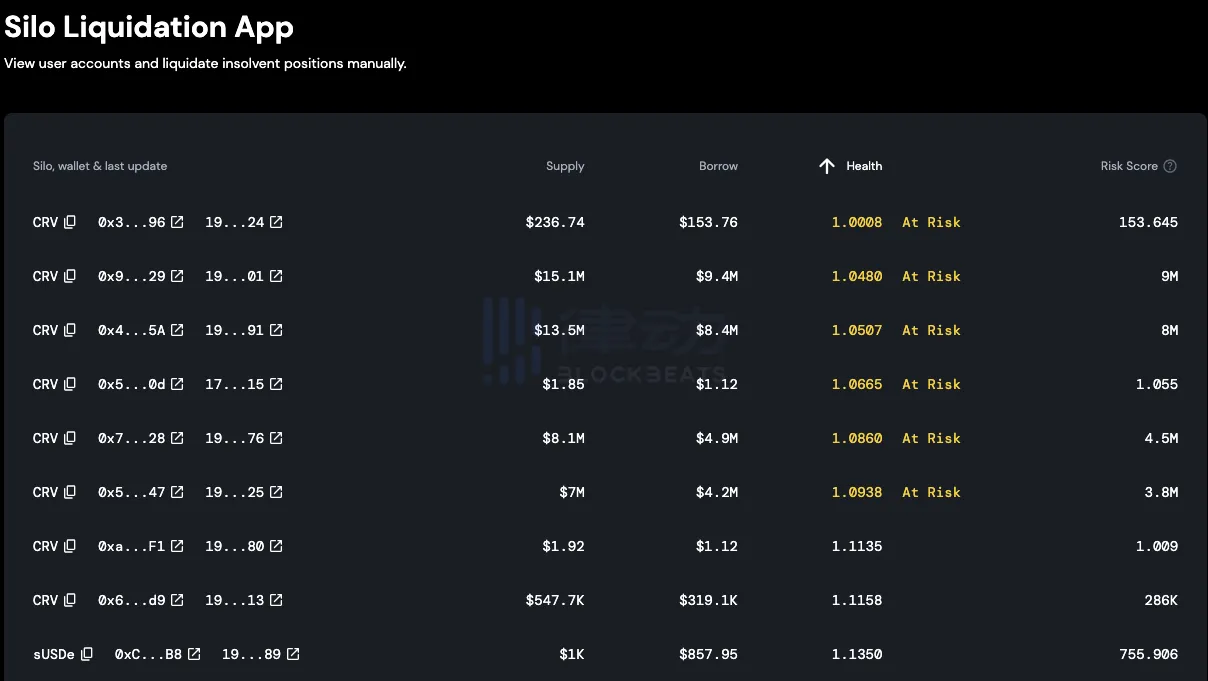

माइकल्स की ऋण स्थिति 6 विभिन्न ऋण प्रोटोकॉल में वितरित की गई है, जिनमें से सबसे विवादास्पद ऋण प्रोटोकॉल साइलो है।

कर्व पर हमला होने के बाद, अधिकांश ऋण प्रोटोकॉल ने अपनी नीतियों को कड़ा कर दिया क्योंकि वे CRV से जुड़े बहुत अधिक जोखिम को सहन करने के लिए तैयार नहीं थे। माइकल द्वारा जुटाए गए ऋणों में से आधे से अधिक साइलो से आए थे। माइकल द्वारा अपने AAVE ऋण की स्थिति को चुकाने की प्रक्रिया में, साइलो ने लगभग सभी आवश्यक ऋण प्रदान किए। यह कहा जा सकता है कि माइकल के लिए अपने ऋणों को चुकाने के लिए साइलो सबसे बड़ा सुदृढ़ीकरण बन गया, और कई समुदाय के सदस्यों ने मजाक में कहा कि वे माइकल के निजी बैंक थे।

उस समय, माइकल की कुल ऋण स्थिति में, साइलो प्रोटोकॉल में कुल लगभग 113 मिलियन CRV जमा थे, और कुल लगभग 27.9 मिलियन अमेरिकी डॉलर के स्थिर सिक्के उधार लिए गए थे, जो माइकल की कुल ऋण स्थिति का 30% था। हालाँकि, कर्व लामालेंड, यूडब्ल्यूयू लेंड और फ्रैक्सलेंड प्रोटोकॉल ने भी माइकल को अधिकांश ऋण प्रदान किए। हालाँकि यह अनुपात साइलो जितना अधिक नहीं था, फिर भी यह 15% से अधिक था, जिसमें से कर्व लामालेंड का हिस्सा 20.7% था, यूडब्ल्यूयू लेंड का हिस्सा 17.9% था, और फ्रैक्सलेंड का हिस्सा 17.3% था।

दूसरी ओर, साइलो ने एक नया प्रोटोकॉल तैयार किया है, साइलो लामा , जो कि crvUSD के लिए विशेष रूप से डिज़ाइन किया गया एक अलग ऋण प्रोटोकॉल है। हालाँकि यह प्रोटोकॉल संदेह से भरा है, लेकिन DeFi को उपयोगकर्ता की भावनाओं से स्वतंत्र होने के लिए डिज़ाइन किया जाना चाहिए। उधार लेने की तुलना में, CRV की लॉक-अप दर CRV की बिक्री पर अधिक प्रभाव डालती है। CRV के लिए एक अलग पूल स्थापित करना DeFi ऋण देने वाले वॉल्ट के काम करने के तरीकों में से एक है, और साइलो टीम के सदस्यों ने एक व्यक्ति के लिए साइलो लामा बनाने के आरोप का भी स्पष्ट रूप से खंडन किया है।

साइलो और कर्व के बीच के रिश्ते को अलग रखते हुए, विवाद का सार यह है कि साइलो ने CRV को लिक्विडेट नहीं किया। अंदरूनी सूत्रों ने कहा कि क्योंकि साइलो पर CRV की स्थिति चेनलिंक ऑरेकल का उपयोग करती है, इसलिए मूल्य अपडेट डीबैंक से पीछे रह जाएगा, इसलिए यह संदिग्ध है कि क्या ऑरेकल लिक्विडेशन मूल्य को ट्रैक करता है।

के अनुसार चेनलिंक डेटा उस समय दर्ज की गई CRV कीमतों से पता चला कि यह 14 अप्रैल को सुबह 5:30 बजे $0.4 से नीचे गिर गई, और $0.36 से $0.38 की सीमा में थी। फिर लेखक ने डेक्सस्क्रीनर, कॉइनगेको, ट्रेडिंगव्यू, कॉइनमार्केट आदि से डेटा की जाँच की। उस समय, CRV 30 मिनट की लाइन पर लगभग $0.36 तक गिर गया।

चूंकि सीआरवी की सबसे कम कीमत सुबह-सुबह हुई थी, इसलिए लेखक वर्तमान में यह सत्यापित करने में असमर्थ है कि उस समय स्वास्थ्य कारक शून्य था या नहीं। लेकिन उस रात सीआरवी और विभिन्न उधार समझौतों के साथ जो कुछ भी हुआ, उससे कोई फर्क नहीं पड़ता, केवल एक चीज की पुष्टि की जा सकती है कि न केवल साइलो, बल्कि माइकल की सभी ऋण स्थितियाँ अभी भी वहीं हैं।

इस संकट के दौरान, कुछ लोगों ने साइलो के मैन्युअल परिसमापन तंत्र पर ध्यान केंद्रित किया है। चूंकि साइलो परिसमापन पूरी तरह से खुला है, इसलिए परिसमापक मैन्युअल या मशीन चुन सकते हैं। जब उनसे पूछा गया कि क्या मैन्युअल परिसमापन चुनने के बाद उन्हें मशीन द्वारा परिसमाप्त नहीं किया जाएगा, तो एक अंदरूनी सूत्र ने कहा कि मैन्युअल परिसमापन केवल प्लेटफ़ॉर्म द्वारा प्रदान किया गया एक व्यक्तिगत परिसमापन प्रवेश द्वार है। जब किसी ऋण का सामना करना पड़ता है, तो व्यक्तियों को अभी भी ऑर्डर के लिए मशीन के साथ प्रतिस्पर्धा करने की आवश्यकता होती है, और अक्सर मशीन के साथ प्रतिस्पर्धा नहीं कर सकते हैं।

इसलिए, परिसमापन शुरू होगा या नहीं, इसका निर्धारण इस बात पर निर्भर करता है कि संपार्श्विक की कीमत वास्तव में परिसमापन मूल्य तक गिरती है या नहीं।

साइलो दस्तावेज़ के अनुसार, ऋण प्रोटोकॉल में परिसमापन आवेदन जिसका उपयोग कोर टीम जोखिमपूर्ण स्थितियों की निगरानी करने और दिवालिया स्थितियों को समाप्त करने के लिए करती है, यदि परिसमापन रोबोट (सिलो सहित) किसी भी कारण से पहले परिसमापन नहीं करते हैं।

19 अप्रैल को CRV फिर से गिरकर $0.4 पर आ गया। एम्बर द्वारा दिए गए माइकल्स पते के अनुसार, साइलो में 0x9, 0x4 और 0x7 से शुरू होने वाले पतों के ऋण स्वास्थ्य कारक सभी 0.1 से नीचे हैं, जो एक खतरनाक स्थिति में है।

के अनुसार साइलो वित्त संपार्श्विक कारक तालिका साइलो प्रोटोकॉल में CRV का लोन-टू-वैल्यू अनुपात (LTV) 65% है और लिक्विडेशन थ्रेशहोल्ड (LT) 85% है। इसका मतलब है कि माइकल्स साइलो लिक्विडेशन कीमत $0.41 से $0.44 की रेंज में है, इसलिए हेल्थ फैक्टर सैद्धांतिक रूप से 0 है।

गणना सूत्र:

परिसमापन मूल्य = कुल ऋण राशि / (संपार्श्विक राशि * LTV * LT)

स्वास्थ्य कारक = 1-ऋण की कुल राशि/(संपार्श्विक की कुल राशि*एलटीवी)

इस संबंध में, ब्लॉकबीट्स ने परियोजना टीम के साथ सत्यापित किया कि इसकी मूल्य ट्रैकिंग केवल ओरेकल फ़ीड मूल्य की जाँच नहीं कर रही है, बल्कि भारित औसत एल्गोरिथ्म का उपयोग कर रही है। इसका मतलब यह है कि एक टोकन का परिसमापन मूल्य ऋणदाताओं की अन्य ऋण परिसंपत्तियों की कीमतों से प्रभावित होगा, इसलिए अकेले CRV की कीमत में गिरावट स्थिति को समाप्त करने के लिए पर्याप्त नहीं है। हालाँकि, जब तरलता आपूर्ति के मुद्दे के बारे में पूछा गया, तो परियोजना टीम ने कोई जवाब नहीं दिया।

जहाँ तक लैमलेंड की बात है, जिस प्लेटफ़ॉर्म पर माइकल की सबसे बड़ी स्थिति है, उसका स्वचालित परिसमापन तंत्र नरम परिसमापन से बचाव कर सकता है। सीधे शब्दों में कहें तो, इसकी परिसमापन प्रक्रिया यह है कि जब कीमत गिरती है, तो संपार्श्विक स्वचालित रूप से स्थिर सिक्कों में परिवर्तित हो जाता है, और जब कीमत बढ़ जाती है, तो संपार्श्विक टोकन वापस बेच दिए जाते हैं, और स्वास्थ्य कारक को बढ़ाने के लिए केवल थोड़ी मात्रा में crvUSD चुकाने की आवश्यकता होती है।

इसके अलावा, अंदरूनी सूत्रों ने ब्लॉकबीट्स को बताया कि वास्तव में, बड़े बाजार उतार-चढ़ाव के मामले में, परिसमापक को स्लिपेज समस्या पर विचार करने की आवश्यकता होती है, जिसमें एक ही समय में crvUSD और CRV का स्लिपेज शामिल होता है। पिछले कुछ बड़े फ़्लोटिंग उतार-चढ़ाव में, ऋण समझौते मशीन का परिसमापन न करना सामान्य बात थी।

पूरे क्रिप्टो बाजार की तरलता पर करोड़ों डॉलर के ऋण स्थिति परिसमापन के प्रभाव को कम करके नहीं आंका जा सकता है। अप्रैल में संकट अभी भी ऋण देने वाले प्लेटफ़ॉर्म के सुरक्षा तंत्र के कारण टल गया था, लेकिन इस बार CRV $0.26 से नीचे गिर गया, और संकट आखिरकार आ ही गया।

जब कीमत न्यूनतम स्तर पर पहुंच जाए तो नीचे से खरीदना है या नहीं, यह भी निवेशकों के लिए चिंता का विषय है, लेकिन कम से कम सीआरवी के मामले में, परिसमापकों ने पहले ही लाभ कमाना शुरू कर दिया है।

ai_9684 xtpa निगरानी के अनुसार, पता 0xF07…0f19E माइकल्स की स्थिति के मुख्य परिसमापकों में से एक है। पिछले एक घंटे में, पते ने $0.2549 की औसत कीमत पर 29.62 मिलियन CRV का परिसमापन किया, जिसमें कुल 7.55 मिलियन FRAX खर्च हुए। वर्तमान में, इन सभी टोकन को Binance में रिचार्ज किया गया है, जिसकी औसत रिचार्ज कीमत $0.2792 है।

एक परिसमापक के रूप में, एक अधिक किफायती तरीका बिनेंस पर CRV शॉर्ट ऑर्डर खोलना (या बेचने के लिए सिक्के उधार लेना) और फिर परिसमापन करना हो सकता है। इस तरह, परिसमापन से प्राप्त टोकन का उपयोग केवल शॉर्ट पोजीशन को बंद करने (या ऋण चुकाने) के लिए किया जाता है, बिना उस अवधि के दौरान मूल्य में उतार-चढ़ाव के कारण होने वाले लाभ या हानि को सहन किए।

लेकिन फिर भी अगर 0xF07…0f19E यदि उसने ऐसा नहीं किया होता, तो भी वह औसत रिचार्ज मूल्य पर बेचकर $720,000 का लाभ कमा सकता था।

लेकिन दूसरी ओर, निवेशकों को संकट का सामना करना पड़ रहा है।

एक तरफ, कीमत में गिरावट ने अन्य ऋण देने वाले प्लेटफ़ॉर्म के परिसमापन को गति दी। फ्रैक्सलेंड्स के ऋणदाताओं को लाखों डॉलर का परिसमापन झेलना पड़ा। लुकऑनचेन के अनुसार निगरानी 2014 के अनुसार, कुछ उपयोगकर्ताओं ने फ्रैक्सलेंड पर 10.58 मिलियन सीआरवी (3.3 मिलियन अमेरिकी डॉलर) का परिसमापन किया था।

इसकी तुलना में, फ्रैक्सलेंड्स लिक्विडेशन मैकेनिज्म को ट्रिगर करना आसान है, और इसके जोखिम अलगाव और गतिशील ब्याज दर तंत्र को माइकल को अपनी पहल पर पैसे चुकाने की अनुमति देने के लिए किसी भी अतिरिक्त उपाय की आवश्यकता नहीं है। पिछले लिक्विडेशन संकटों में, माइकल ने एवे से बड़ी मात्रा में संपत्ति उधार ली और फ्रैक्सलेंड्स के ऋणों को चुकाने के लिए ओटीसी के माध्यम से सिक्के बेचे।

दूसरी ओर, शुरुआती सीआरवी निवेशकों को भारी नुकसान का सामना करना पड़ा।

पिछले साल CRV संकट के बाद से, समुदाय में ऐसी टिप्पणियों की कमी नहीं रही है कि कर्व का हाथ अच्छा था लेकिन माइकल ने इसे गड़बड़ कर दिया। इस CRV संकट के बारे में सबसे उल्लेखनीय बात यह है कि प्रमुख निवेशकों ने पहले माइकल की मदद की थी।

पिछले साल जुलाई के अंत में कर्व के चोरी हो जाने के बाद, विभिन्न ओजी, संस्थानों और वीसी ने मदद की। बिटमैन और मैट्रिक्सपोर्ट के सह-संस्थापक जिहान वू ने सोशल मीडिया पर पोस्ट किया: आगामी आरडब्ल्यूए लहर में, सीआरवी सबसे महत्वपूर्ण बुनियादी ढांचे में से एक है। मैंने इसे सबसे नीचे खरीदा है, जो वित्तीय सलाह नहीं है।

हुआंग लिचेंग ने सोशल मीडिया पर पुष्टि की कि उन्होंने ओटीसी के माध्यम से कर्व के संस्थापक से 3.75 मिलियन सीआरवी खरीदे और उन्हें कर्व प्रोटोकॉल में गिरवी रख दिया। अगले दिन, सन यूचेन के संबंधित पते ने भी ईगोरोव के पते पर 2 मिलियन यूएसडीटी स्थानांतरित किया और 5 मिलियन सीआरवी प्राप्त किए।

इसके बाद यर्न फाइनेंस, स्टेक डीएओ जैसी परियोजनाएं, तथा डीडब्ल्यूएफ जैसी अनेक संस्थाएं और वीसीज़ सीआरवी की समस्या को सुलझाने के अभियान में शामिल हो गईं।

अब CRV एक नए निचले स्तर पर पहुंच चुका है, और माइकल ने खुद इसे बचाने के लिए अभी तक कोई बयान नहीं दिया है। जैसा कि समुदाय ने कहा, लोगों को काटने वाली पार्टी को आखिरकार माइकल ने ही काटा।

यह लेख इंटरनेट से लिया गया है: संस्थापक को अंततः समाप्त कर दिया गया, क्या कर्व्स फ्लाईव्हील पूरी तरह से दिवालिया हो गया है?

24 मई को, ALIENX Chain ने आधिकारिक तौर पर HAL टेस्टनेट लॉन्च किया और 3-सप्ताह का इंटरैक्टिव एयरड्रॉप इवेंट लॉन्च किया। ALIENX एक AI नोड-संचालित और EVM-संगत स्टेकिंग पब्लिक चेन है जिसका उद्देश्य AI तकनीक और ब्लॉकचेन की विकेंद्रीकृत प्रकृति को मिलाकर पारंपरिक AI परियोजनाओं की डेटा सुरक्षा और गोपनीयता के मुद्दों को हल करना और AI Dapp, NFTs और GameFi के बड़े पैमाने पर अनुप्रयोगों को प्राप्त करना है। ALIENX को OKX Ventures, C² Ventures, Next Leader Capital आदि सहित संस्थानों से $17 मिलियन का वित्तपोषण प्राप्त हुआ है। वित्तपोषण के नवीनतम दौर में, ALIENX Chain का मूल्य $200 मिलियन है। ALIENX HAL टेस्टनेट के रिलीज़ होने का मतलब है कि इसके मेननेट का विकास मूल रूप से अंतिम चरण में प्रवेश कर गया है। यह टेस्टनेट एयरड्रॉप इवेंट 3 सप्ताह तक चलेगा। टेस्टनेट एयरड्रॉप के बाद, ALIENX…