Une nouvelle perspective sur les matières premières numériques, la valeur de l'ETH va-t-elle se redresser ?

Original author: sam.frax, founder of Frax Finance

Traduction originale : zhouzhou, BlockBeats

Editors Note: This article explores the difference between digital commodities (such as L1 tokens) and equity-like tokens, and proposes a new framework for evaluating digital assets, especially for the value of ETH. The author believes that ETH should be regarded as a sovereign commodity rather than an equity-like token because commodities cannot generate cash flow or dividends. At the same time, it points out how to eliminate the vague définition of ETH assets, reiterates the importance of commodity premiums, and points out possible value assessment errors in the future.

Voici le contenu original (pour une lecture et une compréhension plus faciles, le contenu original a été réorganisé) :

Dans le cryptocurrency space, I propose a new system for valuing digital goods such as L1 tokens and the distinction between sovereign goods and governance/equity tokens. This view is critical to ETH and various L2 tokens, and may completely eliminate the ambiguity of ETH assets.

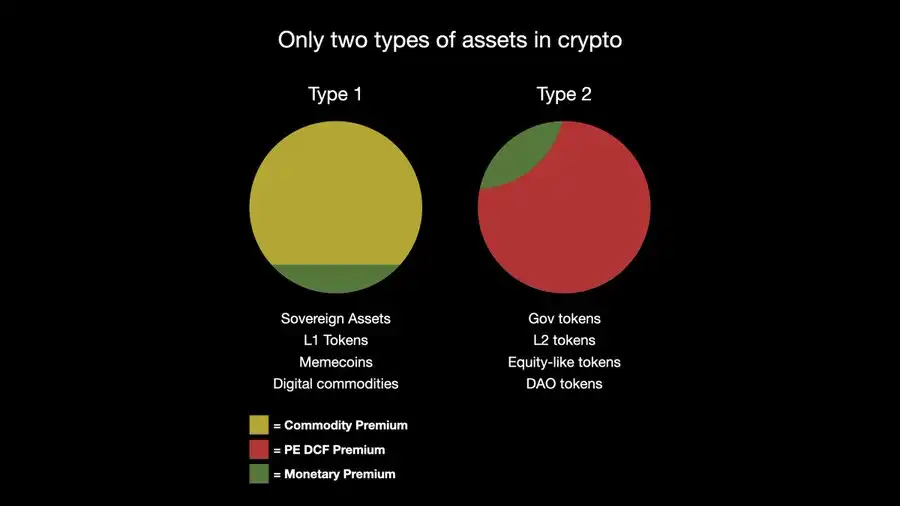

In crypto, there are really only two types of tokens: digital commodities (usually L1 sovereign assets) and equity-like governance tokens. I’ve covered this in more depth in a previous discussion.

Commodities, by definition, cannot pay “dividends” or have “cash flows”, so if an asset is truly a digital commodity and not a governance/equity token, we must abandon this false evaluation criterion. Just as a sovereign cannot meaningfully default on debt denominated in its own currency (only inflation can occur, not default), digital commodities actually have no real issuer, it is a scarce sovereign asset, and therefore cannot meaningfully provide dividends or cash flows if it is truly a commodity.

Assets themselves are products, like BTC. Labor and other real products can only generate economic demand for commodities.

Ethereum (network + chain) is the largest digital nation, a sovereign economy full of innovations from global laborers and builders. This labor is tokenized in the form of governance/equity tokens, which are clearly distinguished from digital commodities such as BTC, ETH, SOL, etc. Where any entity pays holders of digital commodities for any action, whether it is liquidity provision rewards, DeFi incentives, or LSD and LRT, these can be measured empirically.

This metric should be defined as the commodity premium of an asset, rather than a currency premium, sovereign premium or speculative premium, which is a legitimate and fundamentals-focused valuation term for an asset class.

Anywhere in the global economy, anyone pays someone else in the form of labor or equity-like tokens to hold some form of sovereign asset, we can track the flow of value from labor to digital goods. This demand is the global interest rate paid to all forms of ETH holders, including ETH holders who use it in liquidity pools, re-staking, L2, and new DeFi innovations that have yet to appear.

This is the global economic demand for commodities, the commodity premium. Obviously, this has a much greater value accumulation effect on the price and market capitalization of sovereign assets than any PE DCF framework. This is also why BTCs market cap is close to $200 billion without any gas consumption. But in my framework, notice that there is no PE DCF premium in a class of tokens because it is simply impossible.

Only equity-like tokens can have cash flows, and what we think of as “dividends/buybacks/burns” in an asset class is actually just a commodity premium. Likewise, there is no commodity premium in equity-like tokens.

This brings us to the 1559 burn mechanism, which is often viewed as the core value accumulation mechanism of ETH because it is considered to be “Ethereum the enterprise” paying dividends/cash flows to ETH commodity holders.

But this is a ridiculous concept because commodities do not generate cash flows. If a company uses gold in a new industrial use that changes the molecular structure of gold and causes the element to be permanently removed from circulation, we will not start to do a PE or DCF cash flow analysis on gold, but only think that it has a new high-demand industrial use that consumes the commodity. No one will do a PE or DCF analysis on gold.

Likewise, no one does PE or DCF analysis on BTC. Its like gold, but in digital form. The PE DCF premium is not within the socially acceptable range for real or digital goods. Going further, the 1559 burn mechanism stems from user demand within Ethereum and its L2 sovereign economy. This is just another economic demand for $ETH sovereign assets, another industrial use case. This demand is paid through the Ethereum blockchain protocol itself, not through labor or manually issued equity/governance token rewards.

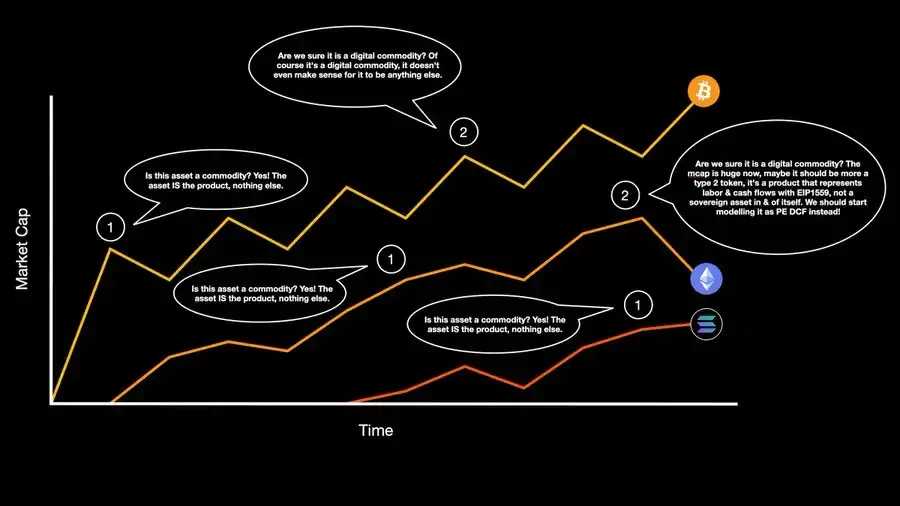

Ethereum is the first project to face the “final boss” challenge in defining its own social identity, but SOL is the next and may struggle with this step once it reaches this stage. Other sovereign assets will face similar problems as they mature to these stages.

My thoughts on the digital commodity life cycle and its associated pitfalls are laid out in a chart. $SOL has not yet reached stage 2, noting that $BTC and $ETH have taken different turns in stage 2 in my opinion.

It is very important for $ETH to establish this social contract now, to show the world before it is too late, that it is not just $BTC that has this privilege. In fact, it is not a privilege, but a social contract for a commodity premium – a very specific, quantifiable, rules-based system.

Note that I do not mention the ill-defined “speculative premium” in my paper. This is because I focus on a well-defined and measurable framework for fundamental value. The speculative premium is simply trading activity that attempts to quantify future fundamentals-based value systems. The speculative premium is not a fundamental framework like the commodity premium or PE DCF premium. The speculative premium is simply market activity that attempts to calculate what framework the asset will be valued in the distant future.

Until now, PE DCF was the only fundamentals-based framework for discussing digital assets, except $BTC. It was incorrectly applied to all assets (except BTC), but should only be used to value assets that represent labor, products, and governance rights, not sovereign digital commodities.

In the next part of this series, I will explain how and why certain technical steps, such as a defined gas token, sovereignty of supply, and consensus, are necessary to establish a social contract for commodity premiums. If $ETH can be accidentally transformed into a second-class token, then it is also possible to transform a second-class token into a first-class token, but it is a very difficult and sensitive process that is prone to error.

This article is sourced from the internet: A new perspective on digital commodities, will the value of ETH recover?

En lien : Alors que le discours sur l’IA s’intensifie, comment la DeFi peut-elle en bénéficier ?

Auteur original : DeSpread Research Traduction originale : TechFlow Avertissement : Le contenu de ce rapport représente les opinions personnelles de l'auteur et est fourni à titre de référence uniquement. Cet article n'a pas pour but de recommander l'achat ou la vente de jetons ou l'utilisation d'un protocole. Rien dans le rapport ne constitue un conseil en investissement et ne doit pas être considéré comme un conseil en investissement. 1. Introduction Avec le développement de l'industrie informatique, l'amélioration de la puissance de calcul et l'application généralisée du big data, les performances des modèles d'intelligence artificielle (IA) se sont également considérablement améliorées. Ces dernières années, les capacités de l'IA ont atteint ou même dépassé les niveaux humains dans de nombreux domaines et ont été rapidement appliquées à des secteurs tels que la santé, la finance et l'éducation. Un exemple typique de commercialisation de l'IA est ChatGPT, une intelligence artificielle générative…