Après un mois et demi sur le marché, comment se comportent les six ETF d'actifs virtuels à Hong Kong ?

Auteur original : Weilin, PANews

Cela fait un mois et demi que les six ETF d'actifs virtuels de Hong Kong ont été cotés le 30 avril, et le marché est toujours en période de rodage. D'une part, les banques traditionnelles n'ont pas encore distribué ces ETF d'actifs virtuels, mais d'autre part, certaines maisons de courtage en font activement la promotion. Par exemple, l'application de trading Victory Securities VictoryX a désormais ouvert les fonctions de dépôt et de retrait de l'USDT et de l'USDC aux investisseurs professionnels.

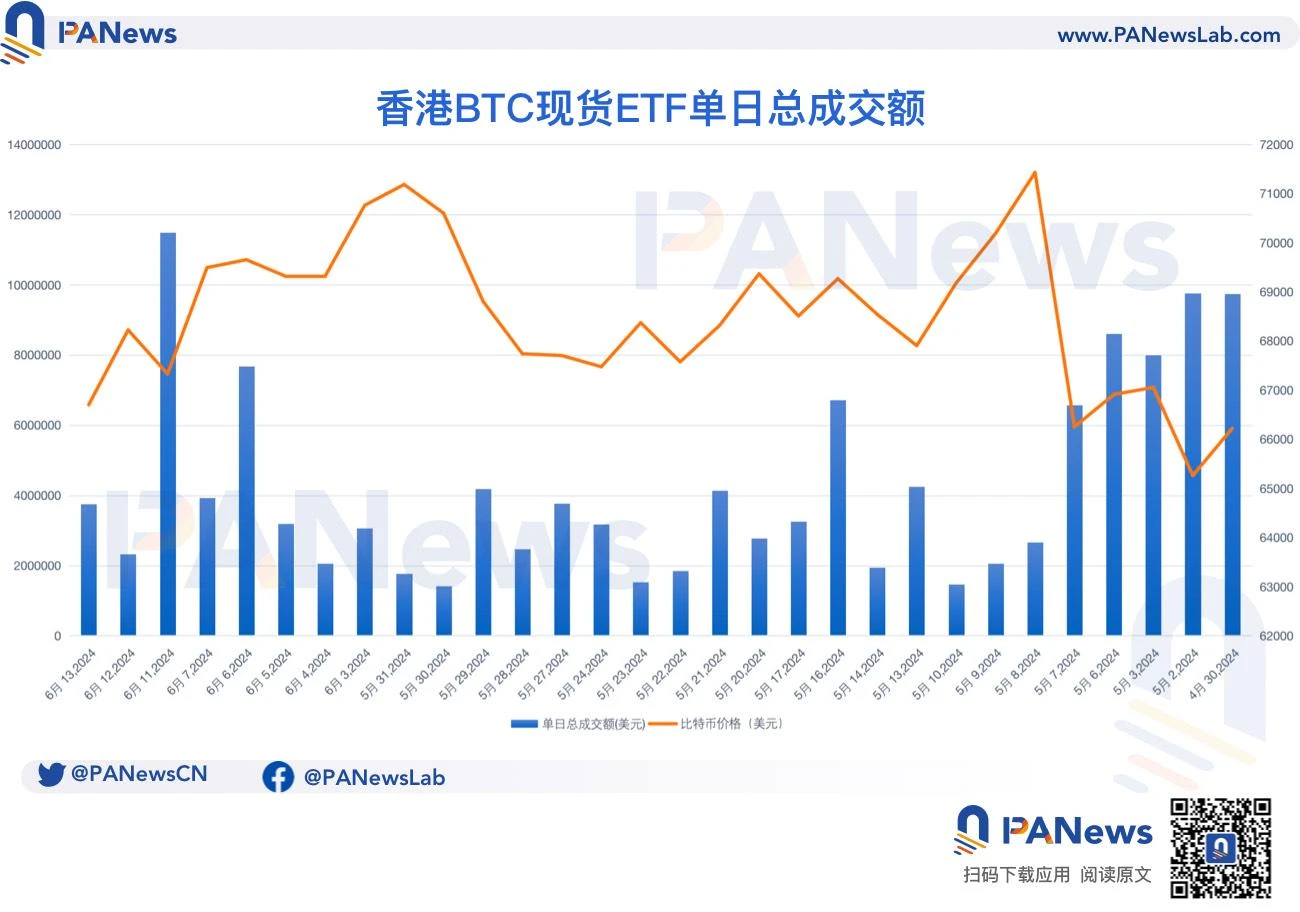

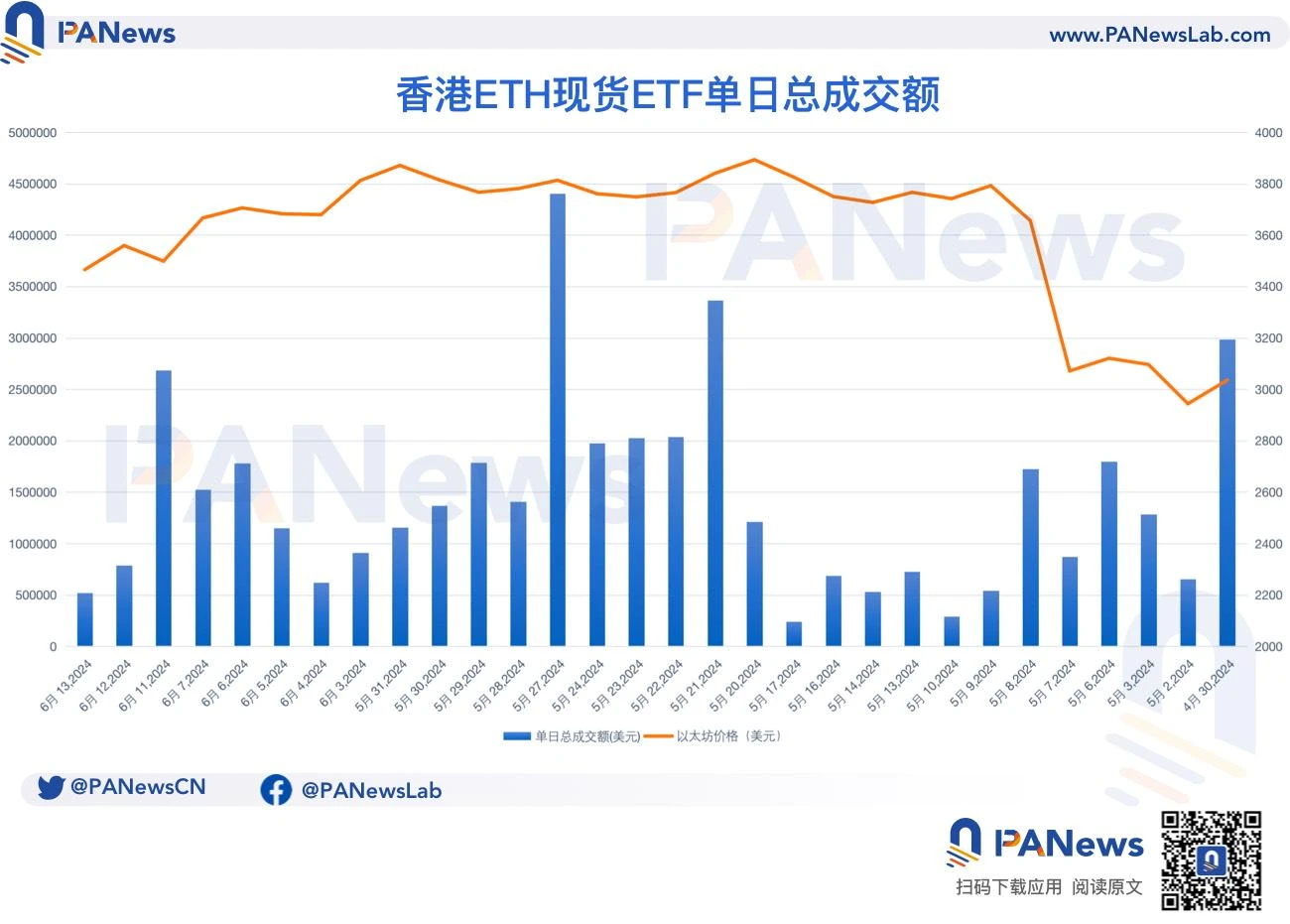

Plus précisément, en termes de performance du volume des transactions sur le marché, les données de SoSo Value montrent que pendant cette période, le volume total quotidien moyen des transactions de l'ETF spot BTC de Hong Kong était de 1 100 T4,3215 millions de dollars américains, atteignant un sommet historique de 1 100 T11,4984 millions de dollars américains le 11 juin ; le volume total quotidien moyen des transactions de l'ETF spot ETH de Hong Kong était de 1 100 T1,4354 million de dollars américains, le point le plus élevé ayant eu lieu le 27 mai, à 1 100 T4,4042 millions de dollars américains.

Les experts du secteur ont analysé que le volume et l'échelle des échanges des ETF d'actifs virtuels de Hong Kong sont inversés, et que les parties prenantes compensent l'approbation précoce des ETF et que différentes institutions interviennent et débloquent les goulots d'étranglement. Deux mois plus tard, cela pourrait être le nœud clé de la croissance du volume.

Après un mois et demi sur le marché, comment se comportent les six ETF d’actifs virtuels ?

Selon les données publiques, l'échelle d'émission des trois ETF Bitcoin spot de Hong Kong le premier jour du 30 avril a atteint 10248 millions de dollars US (l'ETF Ethereum spot était de 1045 millions de dollars US), dépassant de loin l'échelle d'émission initiale de l'ETF Bitcoin spot américain le 10 janvier d'environ 10125 millions de dollars US (hors Grayscale), ce qui montre également que le marché a de grandes attentes quant aux performances ultérieures des ETF cryptographiques de Hong Kong.

Français À en juger par le volume initial des transactions, les critiques du marché à l'égard de ces six ETF cryptographiques de Hong Kong se concentrent sur leur faible performance par rapport aux ETF cryptographiques américains : le premier jour de cotation, le volume total des transactions des six ETF cryptographiques de Hong Kong était de 11,2 millions de dollars américains (HKT), dont le volume des transactions des trois ETF Bitcoin était de 67,5 millions de dollars américains (HKT), ce qui est inférieur à 11,9 milliards de dollars américains (HKT) du volume total des transactions de l'ETF spot Bitcoin américain le premier jour (4,6 milliards de dollars américains).

Selon les données de SoSoValue, au 13 juin, le nombre total de bitcoins détenus par les ETF de Hong Kong était de 4 070, avec une valeur nette d'inventaire totale de 10275 millions de dollars américains. En ce qui concerne les ETF spot Ethereum, le nombre total d'ETH détenus par les ETF de Hong Kong était de 14 030.

En ce qui concerne le volume total des transactions quotidiennes du Hong Kong BTC spot ETF, le 11 juin, le volume total des transactions quotidiennes a atteint 11,4984 millions de dollars américains, atteignant un sommet historique, mais il est rapidement retombé au cours des deux jours suivants. Depuis sa cotation, le volume total moyen des transactions quotidiennes a été de 4,3215 millions de dollars américains. Au cours de cette période, le volume total moyen des transactions quotidiennes du US Bitcoin ETF était de 1,965 milliard de dollars américains.

Données : SoSo Value, Coingecko

Le volume total quotidien de transactions le plus élevé de l'ETF spot Hong Kong ETH était de 1 TP104,4042 millions de dollars US le 27 mai. Depuis sa cotation, le volume total quotidien moyen des transactions a été de 1 TP101,4354 million de dollars US.

Données : SoSo Value, Coingecko

Les banques traditionnelles n’ont pas encore distribué, et deux mois plus tard pourraient être la clé pour augmenter le volume

Cependant, malgré la cotation des ETF spot d'actifs virtuels à Hong Kong depuis plus d'un mois, aucune banque ne les a encore cotés. Chris Barford, responsable des données et de l'analyse chez Ernst Young Hong Kong Financial Services Consulting, a déclaré au Hong Kong Economic Times que les banques traditionnelles sont préoccupées par les risques réglementaires liés à la lutte contre le blanchiment d'argent et à la connaissance du client (KYC), et qu'elles sont donc plus prudentes quant à leur participation à la distribution de produits.

Certains émetteurs ont admis que les banques et les sociétés de valeurs mobilières sont réglementées par des entités différentes, et que la distribution dans les banques doit encore attendre l'approbation de l'organisme de réglementation correspondant, et que la banque peut avoir besoin de temps pour évaluer. Barford a expliqué que la pénurie de talents est un défi majeur. Le marché mondial est confronté à un problème de pénurie de talents. Des talents plus familiers avec le monde des registres distribués et des actifs virtuels sont nécessaires, et combinés avec des services financiers et des connaissances réglementaires. Lors de la mise en œuvre de solutions techniques, il est nécessaire d'atteindre le niveau de contrôle des risques des banques ou des institutions financières traditionnelles avant que ces produits puissent être mieux acceptés.

Parallèlement, en tant qu’institutions financières traditionnelles, certaines sociétés de valeurs mobilières de Hong Kong envisagent de fournir des services de négociation d’actifs virtuels tels que le Bitcoin.

Par exemple, Victory Securities, Tiger Securities, Interactive Brokers et d'autres sociétés de courtage basées à Hong Kong ont lancé des services correspondants, permettant aux investisseurs de négocier des actifs virtuels tels que Bitcoin sur des applications de courtage. Selon China Securities Journal, certaines sociétés de courtage ont déclaré que les revenus liés aux actifs virtuels pourraient représenter environ un quart des revenus de la société. Selon PANews, bien que de nombreuses sociétés de courtage soutiennent l'achat des produits ETF mentionnés ci-dessus, certaines grandes sociétés de courtage ne recommandent pas non plus activement les ETF d'actifs virtuels à leurs clients pour des considérations réglementaires.

Le 6 mai de cette année, Tiger Brokers (Hong Kong) a annoncé le lancement officiel de services de négociation d'actifs virtuels, prenant en charge 18 devises, dont le Bitcoin et l'Ethereum, devenant ainsi le premier courtier en ligne de Hong Kong à prendre en charge le trading de titres et d'actifs virtuels via une plateforme unique. Le 17 juin, Tiger Brokers (Hong Kong) a annoncé qu'elle avait été autorisée par la Commission de réglementation des valeurs mobilières de Hong Kong à mettre à niveau sa licence et à étendre officiellement le service aux investisseurs particuliers de Hong Kong. À l'heure actuelle, les investisseurs particuliers de Hong Kong peuvent négocier des Bitcoins et des Ethereum, ainsi que des actions, des options, des contrats à terme, des obligations du Trésor américain, des fonds et d'autres actifs mondiaux à un coût abordable via Tiger Trade, la plateforme d'investissement phare de Tiger Brokers, pour obtenir une allocation et une gestion transparentes des actifs virtuels et des actifs financiers traditionnels.

En outre, le 24 novembre dernier, Hong Kong Victory Securities a annoncé qu'elle était devenue la première société agréée de Hong Kong à être approuvée par la Securities and Futures Commission pour fournir des services de négociation et de conseil en actifs virtuels aux investisseurs particuliers. Le 24 novembre dernier également, Hong Kong Interactive Brokers a également obtenu une licence pour le trading d'actifs virtuels pour les clients particuliers de Hong Kong, permettant le trading de Bitcoin et d'Ethereum.

Les investisseurs doivent ouvrir un compte d'actifs virtuels pour échanger des actifs virtuels tels que le Bitcoin sur les applications de courtage. Les courtiers ont fixé un seuil d'entrée bas pour le trading d'actifs virtuels, à partir de $100.

Jupiter Zheng, partenaire du fonds secondaire de Hashkey Capitals, a récemment a écrit Le volume et l’échelle des transactions des ETF d’actifs virtuels de Hong Kong sont inversés. Cela reflète en fait un courant structurel sous-jacent : les différentes parties prenantes peaufinent le processus et débloquent les goulots d’étranglement. En particulier pour les souscriptions et les rachats physiques, il est nécessaire de promouvoir le processus et de favoriser le rodage entre différentes institutions telles que les courtiers (PD), les sociétés de valeurs mobilières, les dépositaires/bourses et les teneurs de marché pour débloquer les goulots d’étranglement. Deux mois plus tard, le nœud clé de la croissance du volume pourrait être atteint.

En outre, la force clé de l'expansion des ETF d'actifs virtuels de Hong Kong à l'avenir proviendra des investisseurs institutionnels. L'enquête d'Ernst Youngs a révélé que de nombreux investisseurs institutionnels prévoient d'augmenter leur allocation aux actifs virtuels dans les 2 à 3 prochaines années. Si les actifs sous gestion dépassent 10,5 milliards de dollars américains, la plupart d'entre eux investiront environ 11,9 milliards de dollars américains de leurs actifs dans une forme ou une autre de monnaie virtuelle, et la plupart des family offices s'intéressent également à la monnaie virtuelle. Les grands investisseurs pensent que le taux de rendement des actifs virtuels pourrait surpasser le marché à l'avenir, mais que leur valeur est volatile. Si ce risque peut être géré, les actifs virtuels constituent une classe d'actifs attrayante.

À l'avenir, bien que les performances actuelles des ETF d'actifs virtuels de Hong Kong doivent être améliorées, le potentiel de marché des ETF d'actifs virtuels de Hong Kong mérite toujours d'être observé, car de plus en plus de courtiers fournissent des services connexes, la possibilité de distribution bancaire augmente et l'intérêt des investisseurs institutionnels pour les actifs virtuels augmente.

Cet article provient d'Internet : Après un mois et demi sur le marché, comment se comportent les six ETF d'actifs virtuels à Hong Kong ?

Connexes : jam : nouvel espoir pour l'économie des créateurs dans l'écosystème de base ?

Original|Odaily Planet Daily Auteur : Wenser Le 21 avril, selon les informations officielles, l'application d'économie des créateurs jam.so lancée par Farcaster et le projet écologique LensProtocol jam a enregistré un volume de transactions de plus de 10 millions de dollars américains dans les 72 heures suivant son lancement, avec un total de plus de 47 000 transactions. Selon les données de Dune, le volume actuel des transactions de jam.so a dépassé 270 millions DEGEN. En tant qu'autre nouvelle graine de l'écosystème Farcaster et DEGEN SocialFi, jam a actuellement reçu un don de 1 million de jetons DEGEN, qui seront utilisés pour le développement écologique à l'avenir. Aujourd'hui, Odaily Planet Daily partagera avec vous cette petite et belle application d'économie des créateurs. jam.so : Une version blockchain d'Instagram qui permet aux créateurs de gagner leur premier dollar ? En tant que créateur…