BlackRock sobre Bitcoin: los factores de riesgo y rentabilidad son muy diferentes a los de los activos tradicionales

Original author: Samara Cohen, Robert Mitchnick, Russell Brownback, Blackrock

Traducción original: 1912212.eth, Noticias de previsión

Bitcoin has experienced a journey of ups and downs in the 15 years since its birth, from obscurity in the beginning to becoming an asset held by more and more individuals and institutions in the world.

We believe that Bitcoin, as a global, decentralized, fixed-supply, non-sovereign asset, has risk and return drivers that are distinct from traditional asset classes and fundamentally uncorrelated over the long term. We maintain this belief even as short-term market trading behavior occasionally (and in some cases profoundly) deviates from Bitcoin fundamentals.

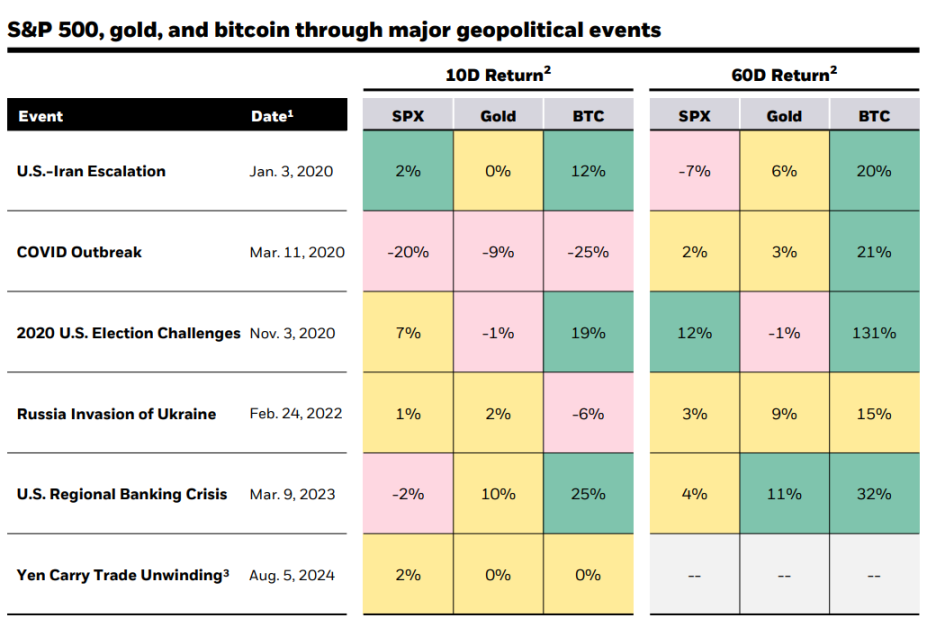

On August 5, 2024, while the SP 500 fell 3%, Bitcoin also experienced a 7% one-day drop as global markets experienced a sharp correction due to the unwinding of yen carry trades. This event coincided with a series of long-pending bankruptcy distributions and liquidations (e.g., Genesis, Mt. Gox) that had unfolded over the previous three days. This was then further exacerbated by the liquidity scramble caused by the global market sell-off.

During these occasional periods of sharp short-term negative correlation with the stock market, Bitcoin prices typically rebound and return to pre-sell-off levels within three days. We view this pattern as an example of fundamentals ultimately triumphing over short-term leveraged trading reactions. As Warren Buffett has said, the stock market is a vehicle for money to flow from the hands of the impatient to the hands of the patient. This insight has also tended to hold true throughout the history of the Bitcoin market.

Key Points

1. Given Bitcoin鈥檚 unique properties and history, investors considering investing in Bitcoin are working hard to understand how it compares to traditional financial assets.

2. Bitcoin is clearly a high-risk asset due to its high volatility. However, most of the risks and potential return drivers faced by Bitcoin are fundamentally different from those of traditional high-risk assets, making it unsuitable for most traditional financial frameworks, including the risk-on asset vs. safe-haven asset framework used by some macro commentators.

3. As a scarce, non-sovereign, decentralized global asset, Bitcoin makes some investors regard it as a safe-haven option when market panics and certain geopolitical turmoil occur.

4. In the long term, Bitcoins adoption trajectory is likely to be driven by the intensity of concerns about global monetary stability, geopolitical stability, U.S. fiscal sustainability, and U.S. political stability. This is the opposite of the general relationship that traditional risk assets are affected by this force.

Introducción

Is Bitcoin a risk-on or safe-haven asset? This is one of the most common questions our clients ask us when considering investing in Bitcoin for the first time. They want to know the long-term correlation of Bitcoin with stocks and bonds, and how it is affected by real interest rates or liquidity in the United States.

We believe the answer is that Bitcoin鈥檚 unique properties make it ill-suited to most other traditional financial frameworks, and that the drivers of Bitcoin鈥檚 long-term returns are fundamentally uncorrelated with, and in some cases even inversely related to, other sources of portfolio returns. Over the long term, we believe the drivers of Bitcoin鈥檚 adoption are likely to be different from, and even inversely related to, the global macro factors that drive most traditional financial assets. While Bitcoin is volatile and has experienced brief co-movements with equities (particularly during periods of extreme market volatility), in this paper we attempt to explain this dynamic.

Why Bitcoin Matters

First, we need to understand the fundamental reasons why Bitcoin is important. Since its creation in 2009, Bitcoin has become the first Internet-native monetary tool to gain widespread global adoption. Its technological innovation lies in the creation of a digitally native, globally universal, scarce, decentralized, and permissionless form of currency. Due to these characteristics, Bitcoin has made significant breakthroughs in solving problems that have plagued other forms of currency for centuries:

1) The supply of Bitcoin is limited to 21 million, which means it will not be easily devalued.

2) Its global and digitally native nature means that it can be transferred around the world in near real time and at near-zero cost, transcending the frictions that have long been inherent in transferring value across political borders.

3) Its decentralized and permissionless nature makes it the world鈥檚 first truly open-access currency system.

Although other crypto assets have emerged since Bitcoin鈥檚 original breakthrough, many of which are pursuing broader use cases, Bitcoin has gained global recognition as the most prominent asset in the field. This makes Bitcoin unique in the crypto asset space as a global currency alternative and an asset with credible scarcity.

Bitcoin鈥檚 Path to $1 Trillion Mercado Tapa

Despite its significant price increase and widespread global adoption, Bitcoins ultimate potential to become a widespread store of value and/or global payment asset remains uncertain, and its changing market value reflects this uncertainty.

Bitcoin has outperformed all major asset classes in seven of the past ten years, resulting in an annualized return of over 100%, an extraordinary performance. Although Bitcoin also had three of the worst performances during this decade, it experienced four pullbacks of over 50%. However, through these historical cycles, Bitcoin has demonstrated the ability to recover from pullbacks and reach new highs, despite the longer duration of these bear market cycles.

These fluctuations in Bitcoin鈥檚 price continue to reflect, in part, the evolving prospects for its widespread adoption as a global currency alternative over time.

Assets that are not correlated with macro variables

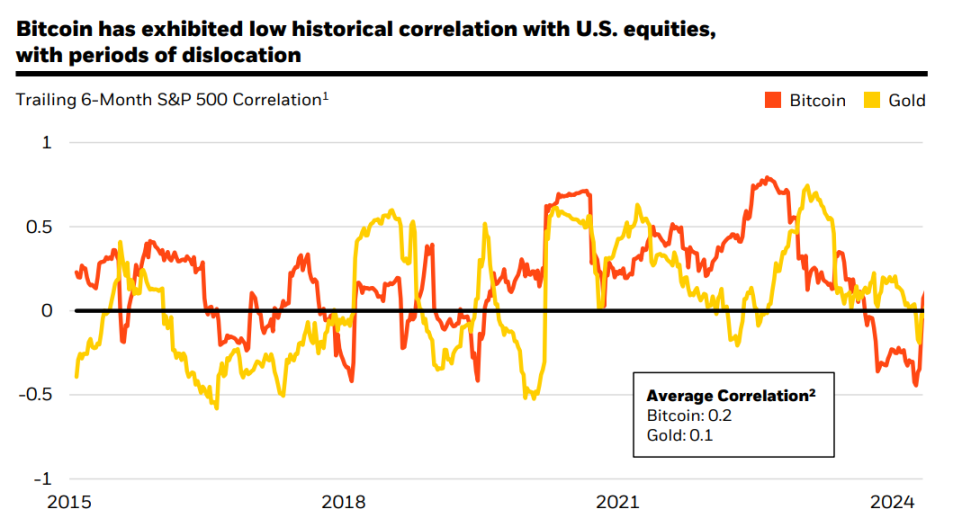

Bitcoin has little fundamental correlation with other macro variables, which is why its long-term average correlation with stocks and other risk assets is low. Although Bitcoins correlation has risen sharply in the short term, especially during periods of sudden changes in US real interest rates or liquidity, it is short-term in nature and has not produced a clear long-term statistically significant correlation.

As the first decentralized, non-sovereign currency alternative to gain widespread global adoption, Bitcoin does not have traditional counterparty risk, is not dependent on any central system, and is not subject to the fate of any single country. These characteristics make Bitcoin fundamentally decoupled from certain key macro risk factors, including banking system crises, sovereign debt crises, currency devaluations, geopolitical turmoil, and other country-specific political and economic risks. In the long term, the trajectory of Bitcoins adoption may be affected by rising or falling concerns about issues such as global monetary instability, geopolitical discord, U.S. fiscal sustainability, and U.S. political stability.

Due to these characteristics, Bitcoin has been viewed by some investors as a safe haven asset during some of the most disruptive events that have occurred globally over the past five years. It is noteworthy that during these events, Bitcoin sometimes experienced a short-lived negative reaction followed by a rebound. We believe that these short-term trading reactions that are difficult to explain with fundamentals can be attributed to the following factors:

1. Bitcoin trades 24 hours a day and can be settled into cash almost instantly, making it a highly marketable asset during periods of tight liquidity in traditional markets, especially on weekends.

Second, the Bitcoin and crypto asset markets are still immature, and investors lack understanding of Bitcoin.

In most cases, including the recent global market sell-off on August 5, 2024, Bitcoin has recovered to its prior levels within a few days or weeks, and in many cases has risen further, as people begin to realize that the positive impact of these disruptive events on Bitcoins fundamentals has taken over.

U.S. debt dynamics return to focus

Based on this, growing concerns about the federal deficit and debt situation both inside and outside the United States have increased the appeal of potential alternative reserve assets as a potential hedge against future events that could affect the dollar. This dynamic also appears to be happening in other countries with significant debt accumulation. Based on our experience with clients to date, this explains much of the recent surge in institutional interest in Bitcoin.

Bitcoin is still a risky asset

None of the previous analysis negates the fact that Bitcoin itself remains a high-risk asset. It is an emerging technology that is still in the early stages of adoption on its path to becoming a global payment asset and store of value. Bitcoin has also been volatile and faces a number of risks including regulatory challenges, uncertainty in its adoption path, and a still immature ecosystem.

The key point, however, is that these risks are unique to Bitcoin and not shared by other traditional investment assets. Bitcoin is therefore a particularly powerful example of why a simple risk-on vs. safe-haven framework may lack the nuance to apply broadly.

From a portfolio perspective, this is why holding a certain position in Bitcoin can have a diversification effect on an investment, while at larger positions, its independent high volatility begins to have too great an impact on increasing portfolio risk.

en conclusión

While Bitcoin sometimes moves in the same direction as stocks and other risk assets in the short term, over the long term its fundamental drivers are very different from, and in many cases the opposite of, those of most traditional investment assets.

As the global investment community faces rising geopolitical tensions, concerns about the state of U.S. debt and deficits, and increased political instability around the world, Bitcoin may be viewed as an increasingly unique portfolio diversifier against the fiscal, monetary, and geopolitical risk factors that investors may face.

This article is sourced from the internet: BlackRock on Bitcoin: Risk and return drivers are very different from traditional assets

Original author: Crypto, Distilled Original translation: TechFlow The Evolution of Cryptocurrency Bull and bear markets have become a relic of history. The cryptocurrency industry has matured and the rules that once existed no longer apply. Here’s an in-depth analysis of the new developments. Rethinking the Market Context: The Quadrant Model The traditional view of bull and bear markets appears outdated. Crypto investor Rancune, one of the top minds in the industry, has proposed a new model for understanding the market. Rancune’s quadrant model provides a more nuanced framework for market analysis based on liquidity and token scarcity. Source: Rancune Liquidity: The Lifeblood of the Crypto Market Liquidity is a key factor in driving prices, but it involves more than just money supply. Unique barriers such as deposit processes and access…