Vom Heißesten zum Schlimmsten: Aufstieg und Fall von Friend.Tech

As the market goes up and down, the prices of some altcoins will never return to their original levels.

Products and businesses may also be gone forever.

In the daily question of What to play today, will anyone mention the name Friend.Tech?

However, you didn鈥檛 say this a year ago: Friend.Tech is the new trend of SocialFi, the darling of Paradigm鈥檚 investment, the hot topic that all research reports are competing to write about, and the god of wealth that liberates the KOL fan economy…

How come he has now become an abandoned pawn that even dogs dont play with?

Attention is not eternal. The once popular encryption products have already fallen from the altar inadvertently.

But the crypto market has memory, so let鈥檚 take a brief look back to see how Friendtech messed up a good hand.

The extreme noise at the peak, the terrifying silence after the disillusionment

Let me tell you a ghost story first.

Data shows that today Friend.Tech has less than 100 daily active users.

During the last round of craze, its daily active users exceeded 77,000, which means that the number of active users has dropped by 99.9%.

But about a year ago, Friend.Tech emerged.

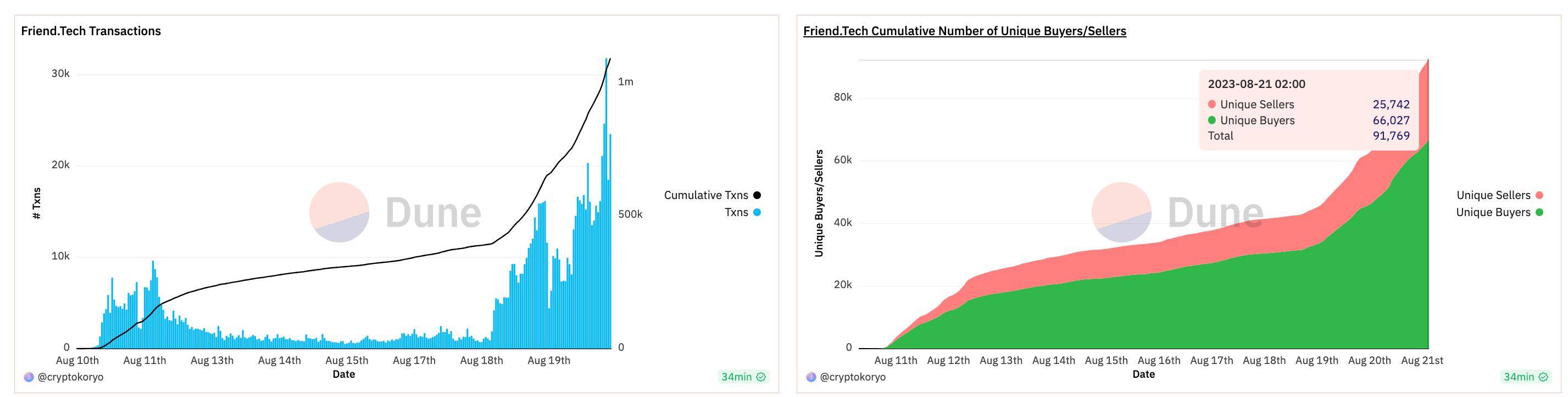

In mid-August last year, friend.tech began to emerge, with a total trading volume of more than 1 million shares (Key), more than 66,000 independent buyers, and 25,000 independent sellers. It can be said to be another encryption product after StepN that almost everyone participates in.

Just two weeks after the launch of FT鈥檚 V1 version, the platform has attracted over 100,000 users and generated approximately $25 million in revenue, marking a significant achievement in terms of user adoption and financial performance.

At that time, FTs financial performance was still healthy, and it was even able to generate so-called real income distribution, distributing approximately US$6 million in revenue to users.

At the time, everyones idea of FOMO was actually very simple. You could make money by buying keys early, and quickly occupying the fan area of celebrity KOLs became the code to wealth. FT also has a points mechanism that determines your point level based on your activity, creating the expectation of winning airdrops.

In the previous dull bear market, it did bring a long-awaited noisy feast of liquidity.

The public data in the crypto world is very transparent, and this hot trend will naturally attract the attention of institutions in the industry. In the same month, FT also announced that it had received seed round financing from top VC Paradigm. The expected airdrop and capital injection pushed the FOMO sentiment to a climax.

New product model, solid user data, endorsement from top VCs… In the last cycle, when people were not arguing about high FDV and low liquidity, and did not regard VC as the opposite, Friend.Tech had these elements and indeed had a good hand.

But you and I both know that the FT selling key model is somewhat flawed and monotonous. Once no more people enter, the natural defects will cause the product to quickly lose popularity;

As you can see, the FT team certainly understands this better, so they have a good hand. The top priority is to manage products, operations and economic expectations well to extend the life cycle and vitality of FT.

But this good hand was played badly.

The operation is as fierce as a tiger, the product is 250

If you rewind time, you will find that the decline of FT can be traced in the details at different time points.

Perhaps it can be summed up in one extreme word: the operation is as fierce as a tiger, but the product is idiotic.

Dont get me wrong, this does not mean that FTs products have no merits. On the contrary, they have the ability to attract traffic and liquidity that other products did not have before. Its just that compared with other operations and direction choices, the product itself seems to be stagnant.

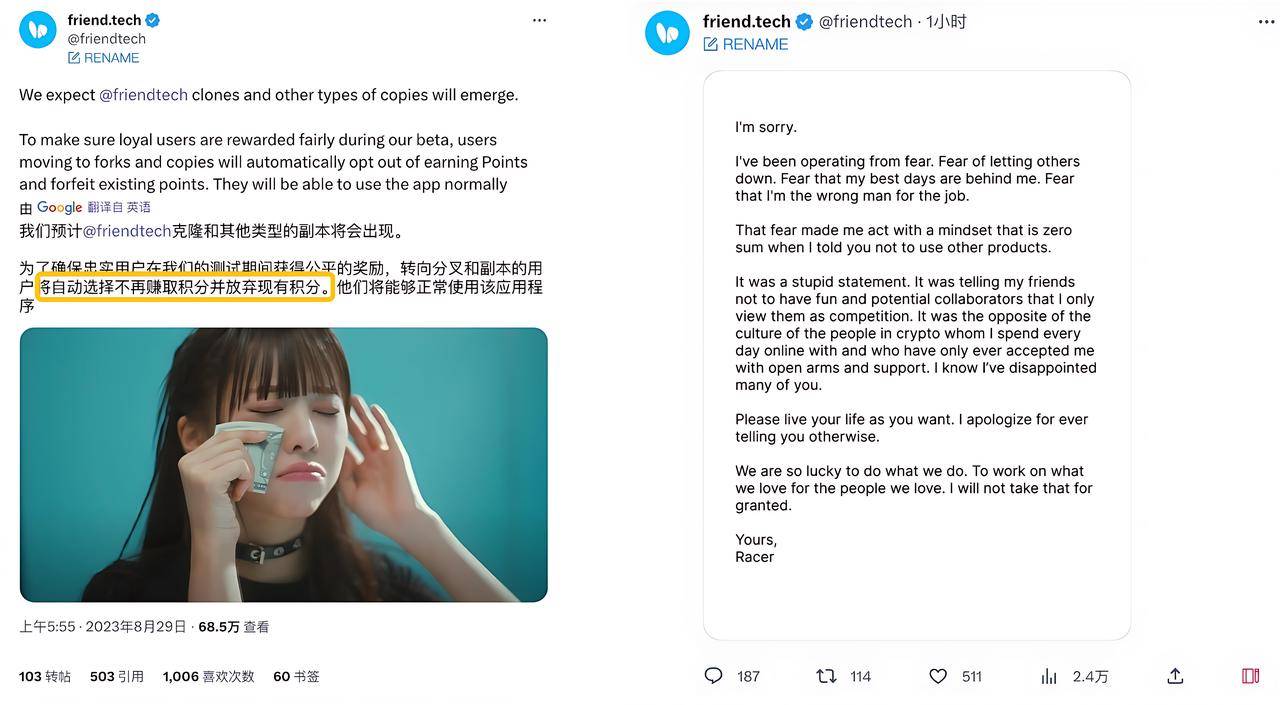

We mentioned the initial signs of this overdoing last year in the article Two-level reversal, friend.tech still agreed to let you be friends with copycats :

At the beginning, FT was extremely opposed to users trying to play other similar imitation platforms, and publicly stated that users could not earn FT points by playing other imitation platforms. After this arbitrary and small-minded approach was boycotted by the community, the founder was afraid of losing users and immediately issued an open letter to apologize. The polar reversal was so fast and unexpected that it was a public relations disaster.

It is very likely that the FT team itself had not figured out how to operate and deal with competitors at the time. For a phenomenal product, this was a bit of a makeshift team, and it was easier to see the big picture from the small details.

Another fierce operation is that the PUA of the V2 version is too fierce.

At the end of April this year, after a long period of silence, Friend.Tech agreed to release the FRIEND token and the new V2 version on the 29th, and the community enthusiasm was ignited again.

However, the release of the token and version was delayed to May 3. The small delay is still within the acceptable range for investors. What really makes people feel uncomfortable is the rules and experience of receiving the FRIEND airdrop:

In addition to following at least 10 users on FriendTech, users must also join a club to receive airdrop tokens; it is obvious that the design of the club is to encourage users to play the V2 version more, to promote activity through the design of the club, and to give users new things to play and continue.

The forced binding of joining first and then receiving the coins is already unpleasant. In addition, on the day of receiving the coins, many people reported difficulties in the collection process and the tokens could not be received for a long time. At the same time, FRIEND began to fall sharply in the secondary market due to insufficient liquidity pool. Many people have not received the coins yet, and the value of the airdrop has been reduced by half.

My coins have all lost value, why would I want to listen to your PUA again?

One netizen joked: After 8 months, the only update we got was the Club, and everyone just used it to claim airdrops.

The misalignment between incentives and product features caused everyone鈥檚 confidence in FT to begin to decline.

But to make matters worse, the FT team then took matters into their own hands. The co-founder Racer publicly stated that it hopes to migrate its products out of the Base network and pointed out that the products were being excluded and isolated in the Base ecosystem.

Distancing oneself from the public chain that one relies on and publicly complaining about it is clearly a dangerous act of playing with fire; the market also voted with its feet, and FT once again suffered a double drop in users and prices.

What is even more impressive is that in June, FT announced that it would soon launch its own proprietary chain, Friendchain, transforming itself from the application layer to the infrastructure layer.

But will the market pay for this shift?

Compared with the overly aggressive operation and direction, the FT product seems to be the same as it was a year ago, with a simple and even crude interface, no separate APP, and the old Ponzi game routine…

The product is of a fools errand, coupled with other internal and external problems, it is not surprising that the phenomenal product fell from the altar.

In contrast, other social products such as Farcaster have launched many other meme coins, such as FRAME, FAR, POINTS, and have been popular one after another. In comparison, FT has really fallen behind.

Is Ponzi scheme a passport for Ponzi schemers?

Perhaps, the FT should not be on a pedestal.

Powered by a modified version of the Ponzi scheme, it can fly higher, but the defects of the aircraft itself cannot be ignored.

Ponzi schemes are indeed a pass for Ponzi schemers, but they do not guarantee that they will continue to operate. FT set the market on fire last year, and there were a variety of factors that came together. There was inevitability in the accident, but this inevitability could not be completely replicated.

People rush in when they seek profit, and rush out when there is no profit. The reason is simple, but the FT process is prolonged.

Ultimately, SocialFi products like FT have not found true product-market fit and are more like short-term speculative products rather than real demand. Coupled with the operational chaos, the outcome is understandable.

But if all phenomenal crypto products are just historical phenomena, the best crypto products will still be speculation.

This article is sourced from the internet: From the hottest to the worst, the rise and fall of Friend.Tech

Related: 0 cost airdrop, Pixelverse Telegram game PixelTap babysitter level guide

Recently, the Ton chain game ecosystem is very popular. NotCoin has been successfully listed on Binance and has seen a good increase. Hamster Kombat has also exceeded 9 million followers on Twitter, which shows that the Tap to Earn type of Telegram games are very popular. Pixelverse, which recently raised 5.5 million in financing, released a Tap-to-Earn battle game PixelTap on the Ton chain and launched a Play-to-Luftabwurf event. The number of monthly active overseas users has reached 7 million, but not many Chinese people pay attention to it. The official clearly stated that the PIXFI token will be listed on the exchange at the end of June, and it is likely to become the next dark horse of the Ton ecosystem. Project Description Pixelverse is a game ecosystem and…